ID : MRU_ 429035 | Date : Oct, 2025 | Pages : 243 | Region : Global | Publisher : MRU

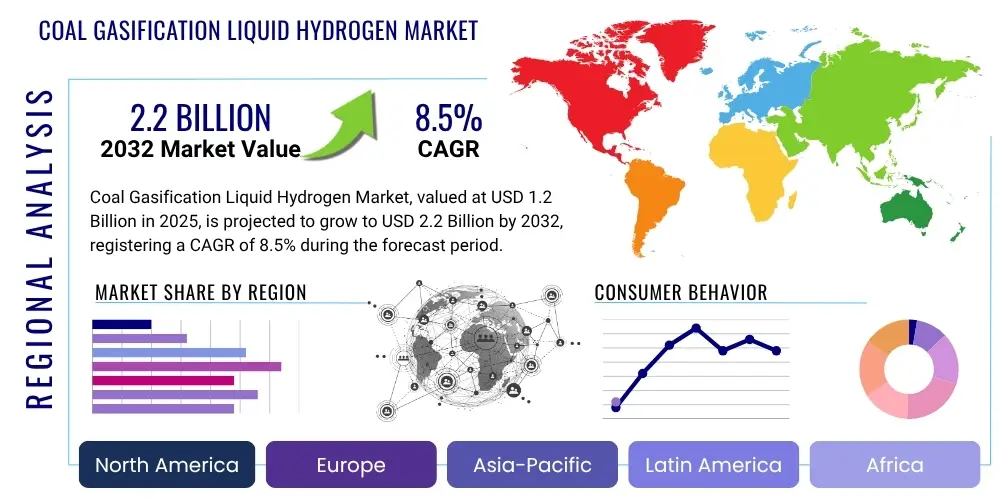

The Coal Gasification Liquid Hydrogen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.2 Billion by the end of the forecast period in 2032.

The Coal Gasification Liquid Hydrogen Market represents a significant emerging segment within the broader hydrogen economy, focusing on the production of high-purity liquid hydrogen through the gasification of coal. This process involves converting coal into syngas, a mixture primarily of hydrogen and carbon monoxide, which is then further processed to isolate and purify hydrogen. Subsequently, this hydrogen is liquefied at extremely low temperatures for efficient storage and transportation, addressing the challenges associated with gaseous hydrogen handling. This method leverages abundant coal resources to meet the growing global demand for hydrogen, offering a pathway for large-scale production, particularly in regions with significant coal reserves and developing hydrogen infrastructure.

The primary product, liquid hydrogen, finds extensive applications across various sectors due to its high energy density and clean combustion properties. Major applications include its use as an industrial feedstock in the production of ammonia for fertilizers, methanol, and in petroleum refining processes. Furthermore, liquid hydrogen is gaining traction as a clean fuel for advanced transportation systems, especially in fuel cell electric vehicles (FCEVs), heavy-duty trucks, maritime vessels, and even in aerospace applications. The benefits of this approach include the potential for energy independence, utilization of existing fossil fuel infrastructure, and the capability to produce hydrogen at scale. However, the environmental impact, particularly carbon emissions, necessitates the integration of Carbon Capture, Utilization, and Storage (CCUS) technologies to align with global decarbonization efforts and enhance its sustainability profile.

Driving factors for the market include the escalating global demand for hydrogen as a clean energy carrier and industrial raw material, coupled with the imperative for energy security in many nations. Technological advancements in gasification processes, syngas purification, and hydrogen liquefaction are continuously improving efficiency and reducing costs, making this production method more viable. Additionally, government incentives and supportive policies aimed at fostering the hydrogen economy, alongside significant investments in hydrogen infrastructure development, are propelling market expansion. The strategic importance of diversifying hydrogen production sources, beyond electrolysis from renewables or natural gas reforming, also underpins the interest in coal gasification as a robust foundational technology for large-scale hydrogen supply.

The Coal Gasification Liquid Hydrogen Market is characterized by dynamic business trends driven by the global energy transition and the increasing emphasis on hydrogen as a clean energy vector. A key trend involves strategic collaborations and partnerships between energy companies, industrial gas suppliers, and technology providers to develop integrated hydrogen production facilities, often incorporating CCUS solutions. There is a noticeable shift towards optimizing the entire value chain, from coal sourcing to liquid hydrogen distribution, with a strong focus on cost efficiency and reducing the carbon footprint. Investment in research and development for advanced gasification technologies and more efficient liquefaction processes is also a prominent business trend, aiming to improve scalability and economic viability.

Regionally, Asia Pacific stands out as the dominant force in the Coal Gasification Liquid Hydrogen Market, primarily propelled by countries like China and India, which possess vast coal reserves and a rapidly expanding industrial base. These nations are actively investing in large-scale hydrogen production projects to meet their burgeoning energy demands and achieve decarbonization goals while leveraging readily available resources. North America and Europe are also showing significant interest, albeit with a stronger emphasis on integrating CCUS technologies to produce "blue hydrogen" from coal gasification, aligning with their stringent environmental regulations and climate targets. Latin America, the Middle East, and Africa are emerging as potential markets, driven by their own resource endowments and growing industrialization, coupled with a desire for energy diversification.

Segment-wise, the market is experiencing significant trends across various applications and technologies. In terms of applications, the industrial feedstock segment remains a cornerstone, with sustained demand from chemical manufacturing and refining. However, there is a rapidly emerging trend in the mobility and power generation sectors, as liquid hydrogen gains traction as a fuel for heavy-duty transport and as a storage medium for renewable energy. Technologically, the adoption of advanced entrained flow gasifiers, known for their high carbon conversion efficiency, is on the rise. Furthermore, the integration of advanced hydrogen purification technologies, such as pressure swing adsorption (PSA) and membrane separation, is crucial for achieving the high purity levels required for fuel cell applications, reflecting a key segment trend towards technological refinement and higher product specifications.

User inquiries regarding AI's impact on the Coal Gasification Liquid Hydrogen Market frequently revolve around optimizing complex operational processes, enhancing safety protocols, and integrating environmental sustainability. Users are keen to understand how artificial intelligence can streamline the intricate stages of coal gasification, from feed quality monitoring to syngas conversion and hydrogen purification, thereby driving efficiency and reducing operational costs. A significant area of concern and expectation is AI's role in improving the effectiveness and economic viability of Carbon Capture, Utilization, and Storage (CCUS) technologies, which are critical for mitigating the environmental footprint of coal-derived hydrogen. Furthermore, questions arise about AI's capacity for predictive maintenance, ensuring facility uptime, and mitigating risks inherent in high-pressure, high-temperature chemical processes, indicating a strong user desire for safer and more reliable operations. The overarching theme is the anticipation of AI as a transformative tool for making coal gasification liquid hydrogen production more competitive, environmentally responsible, and operationally robust.

The Coal Gasification Liquid Hydrogen Market is shaped by a confluence of driving forces, significant restraints, emerging opportunities, and broader impact forces that dictate its growth trajectory and adoption. Key drivers include the ever-increasing global demand for hydrogen as a versatile energy carrier and industrial feedstock, especially in sectors aiming for decarbonization where large-scale, consistent supply is crucial. The abundance of coal reserves worldwide provides a readily available and economically competitive raw material, positioning coal gasification as a viable option for hydrogen production, particularly in energy-resource-rich nations. Moreover, ongoing technological advancements in gasification efficiency, syngas purification, and hydrogen liquefaction are making the process more economically attractive and environmentally manageable. Government support through policies, subsidies, and R&D funding for the hydrogen economy, often including provisions for low-carbon hydrogen pathways, further acts as a significant catalyst.

However, the market faces notable restraints that could hinder its full potential. High capital expenditure (CAPEX) required for building sophisticated coal gasification and liquefaction plants, along with the associated hydrogen infrastructure, presents a significant barrier to entry and expansion. Environmental concerns surrounding greenhouse gas (GHG) emissions from coal use, even with gasification, remain a major restraint, particularly if Carbon Capture, Utilization, and Storage (CCUS) technologies are not fully integrated or are deemed too costly. Competition from alternative hydrogen production methods, such as electrolysis using renewable energy (green hydrogen) or steam methane reforming with CCUS (blue hydrogen from natural gas), also poses a challenge as these methods gain technological maturity and cost competitiveness. Public perception and stringent regulatory frameworks regarding coal-based energy projects can further complicate market development.

Despite these challenges, substantial opportunities exist for market growth and innovation. The widespread integration of advanced CCUS technologies offers a robust pathway to significantly reduce the carbon footprint of coal-derived hydrogen, positioning it as "blue hydrogen" and enhancing its acceptability in sustainability-focused markets. Continued innovation in gasification and hydrogen processing technologies promises to further reduce production costs and improve energy efficiency, making the product more competitive. Furthermore, the development of export markets for liquid hydrogen, particularly to energy-deficient regions or those heavily investing in hydrogen infrastructure, presents significant revenue potential. The opportunity to diversify the energy mix and enhance energy security for nations reliant on fossil fuels, while transitioning to a hydrogen economy, also fuels strategic interest in this sector.

Broader impact forces also play a critical role in shaping the market. Evolving regulatory pressures for decarbonization and stricter emission standards globally will compel greater investment in CCUS and cleaner production methods. Geopolitical shifts and energy security considerations will influence national strategies towards indigenous resource utilization, potentially favoring coal gasification in some regions. Public and corporate environmental, social, and governance (ESG) commitments increasingly demand sustainable and low-carbon solutions, pushing for continuous improvement in environmental performance. Finally, breakthrough technological innovations in catalysis, materials science, and digital optimization (including AI) could dramatically alter the economics and environmental profile of coal gasification liquid hydrogen production, creating new paradigms for its development and adoption.

The Coal Gasification Liquid Hydrogen Market is comprehensively segmented to provide a detailed understanding of its diverse components, technologies, applications, and end-user industries. This segmentation helps in identifying key market dynamics, growth drivers, and emerging trends across different operational aspects and consumer bases. The market can be broadly categorized by the specific gasification technology employed, the various applications for which liquid hydrogen is utilized, and the distinct end-use industries that constitute the primary consumer base. Each segment exhibits unique characteristics and growth potentials, reflecting varying stages of technological maturity, adoption rates, and market penetration. Understanding these segments is crucial for strategic planning, investment decisions, and product development within the burgeoning hydrogen economy, ensuring that solutions are tailored to specific needs and capabilities.

The value chain for the Coal Gasification Liquid Hydrogen Market encompasses a complex series of stages, starting from the extraction of raw materials and extending through sophisticated processing, purification, liquefaction, and finally, distribution to end-users. At the upstream end, the process begins with coal mining and its subsequent transportation to gasification facilities. This stage involves the procurement of various types of coal (sub-bituminous, bituminous, lignite), along with the manufacturing of specialized equipment such as gasifiers, heat exchangers, and cryogenic liquefaction units. Efficiency in coal sourcing and delivery, coupled with reliable equipment supply, is paramount for the overall economic viability of hydrogen production. Upstream activities also include research and development into advanced gasification catalysts and materials resistant to high temperatures and pressures.

Moving downstream, the core of the value chain involves the coal gasification process itself, where coal is converted into syngas. This syngas then undergoes extensive purification to remove impurities like sulfur, ash, and carbon dioxide. A critical step is the water-gas shift reaction, which increases hydrogen yield, followed by further purification techniques such as Pressure Swing Adsorption (PSA) or membrane separation to achieve the high purity levels required for various applications, especially fuel cells. The purified gaseous hydrogen is then subjected to liquefaction, a highly energy-intensive cryogenic process that converts it into liquid hydrogen. This liquid form facilitates efficient storage in insulated tanks and transportation, reducing volume significantly. Downstream also includes the development and operation of hydrogen storage infrastructure and the various end-use applications of liquid hydrogen across industries.

The distribution channel for liquid hydrogen plays a crucial role in connecting producers with consumers, ensuring timely and cost-effective delivery. Direct distribution often involves large industrial gas suppliers or energy companies delivering liquid hydrogen via cryogenic tankers or specialized pipelines to major industrial consumers such as chemical plants, refineries, and power generation facilities. These direct sales form a substantial portion of the market, catering to consistent, high-volume demand. Indirect distribution channels primarily involve smaller volumes supplied to hydrogen refueling stations for fuel cell electric vehicles (FCEVs) or to niche industrial applications. This includes a network of distributors and logistics providers specializing in cryogenic fluid transport. The choice of distribution channel heavily depends on geographical proximity, demand volume, and the specific purity requirements of the end-user, with a continuous focus on safety and efficiency throughout the supply chain to minimize boil-off losses during transport and storage.

The Coal Gasification Liquid Hydrogen Market targets a diverse array of potential customers across various industrial and emerging energy sectors, primarily driven by the need for large-scale, reliable hydrogen supply. Chemical manufacturers represent a significant customer segment, particularly those involved in the production of ammonia for fertilizers, methanol, and other petrochemicals, where hydrogen serves as a crucial feedstock. Oil refineries also form a core customer base, utilizing hydrogen for hydrotreating and hydrocracking processes to remove impurities from crude oil and upgrade petroleum products, enhancing efficiency and meeting environmental standards. These industries require consistent, high-volume hydrogen supply, making coal gasification an attractive option due to its scalability and resource availability.

Beyond traditional industrial applications, emerging sectors are increasingly becoming potential customers. The burgeoning fuel cell industry, encompassing both stationary power generation and various transportation applications such as heavy-duty trucks, buses, trains, and even maritime vessels, seeks high-purity liquid hydrogen. For these applications, liquid hydrogen offers a clean, high-energy-density fuel solution, supporting decarbonization efforts. Power generation companies are also exploring the use of hydrogen, either through direct combustion in turbines or blending with natural gas, to lower carbon emissions from their operations. The aerospace industry, with its long-standing use of liquid hydrogen as a rocket propellant, continues to be a niche but high-value customer segment, driven by advanced space exploration and launch requirements, which prioritize performance and reliability above all else.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2032 | USD 2.2 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Air Products and Chemicals, Inc., Linde plc, Sinopec Group, China Energy Investment Corporation, Shell plc, Mitsubishi Heavy Industries, Ltd., GE Power, Siemens Energy AG, Thyssenkrupp Uhde GmbH, BASF SE, Johnson Matthey, Reliance Industries Limited, Sasol Limited, Topsoe, Woodside Energy Group Ltd., Fluor Corporation, Honeywell UOP, Coke Gas AG, JGC Holdings Corporation, Messer Group GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Coal Gasification Liquid Hydrogen Market relies on a sophisticated and evolving technology landscape, encompassing several critical stages from raw coal processing to the final production of high-purity liquid hydrogen. At the core are the various gasification technologies designed to convert coal into syngas. Entrained flow gasifiers, such as those developed by Shell, GE, and Mitsubishi Heavy Industries, are prominent due to their high carbon conversion efficiency, ability to handle diverse coal types, and production of ash as a vitrified slag. Fluidized bed gasifiers, like the Winkler process, are also employed, suitable for lower-rank coals and offering good thermal control. Moving bed gasifiers, historically exemplified by Lurgi technology, are generally simpler but have lower operating temperatures and pressures. Continuous advancements in these gasifier designs aim to improve efficiency, reduce operational costs, and enhance environmental performance, particularly by increasing carbon capture readiness.

Following gasification, a series of advanced processing and purification technologies are essential to convert syngas into high-purity hydrogen. This includes shift conversion reactors, where carbon monoxide reacts with steam to produce more hydrogen and carbon dioxide. Subsequently, sophisticated gas purification systems are employed, with Pressure Swing Adsorption (PSA) being a widely adopted technology for separating hydrogen from other gases to achieve very high purity levels (up to 99.999%). Membrane separation technologies are also gaining traction, offering potentially lower energy consumption for certain separation tasks. These purification steps are critical not only for end-use applications like fuel cells but also for preparing the gas stream for subsequent carbon capture if a blue hydrogen pathway is pursued. Innovation in catalyst development for the water-gas shift reaction and improved sorbents for impurity removal are key areas of technological focus.

The final crucial stage is hydrogen liquefaction, which is highly energy-intensive and requires advanced cryogenic engineering. This process involves cooling gaseous hydrogen to its boiling point of approximately -253 degrees Celsius (-423 degrees Fahrenheit) at atmospheric pressure. Technologies include various refrigeration cycles, such as helium expansion cycles or mixed refrigerant cycles, often employing turboexpanders for efficiency. Continuous improvements in liquefaction plant designs focus on reducing energy consumption, enhancing reliability, and scaling up capacity to meet growing demand while minimizing hydrogen boil-off losses during storage and transport. Furthermore, the integration of Carbon Capture, Utilization, and Storage (CCUS) technologies is a significant part of the overall technology landscape, particularly pre-combustion capture techniques applied directly to the syngas stream, ensuring that the entire production chain aligns with global decarbonization goals and evolving environmental regulations, positioning the product as low-carbon "blue" hydrogen.

Coal gasification liquid hydrogen is a form of hydrogen produced by converting coal into syngas (a mixture primarily of hydrogen and carbon monoxide) through a high-temperature, high-pressure process. The syngas is then purified to isolate hydrogen, which is subsequently liquefied for efficient storage and transportation. This method leverages abundant coal resources to generate clean-burning hydrogen.

Without mitigation, coal gasification can lead to significant greenhouse gas emissions. However, integrating Carbon Capture, Utilization, and Storage (CCUS) technologies is crucial to significantly reduce the carbon footprint, transforming it into a "blue hydrogen" pathway. This makes the process more environmentally acceptable and aligns with global decarbonization goals, although comprehensive lifecycle assessments are essential.

Coal gasification offers a large-scale, consistent supply of hydrogen, leveraging abundant and often cost-effective coal resources, potentially providing better energy security than natural gas or renewables alone. Compared to "green hydrogen" (from renewable electrolysis), it can be more cost-effective for large volumes but requires CCUS to match its environmental profile. Compared to "grey hydrogen" (from natural gas without CCUS), it can be a cleaner option with CCUS integration.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.