ID : MRU_ 429474 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

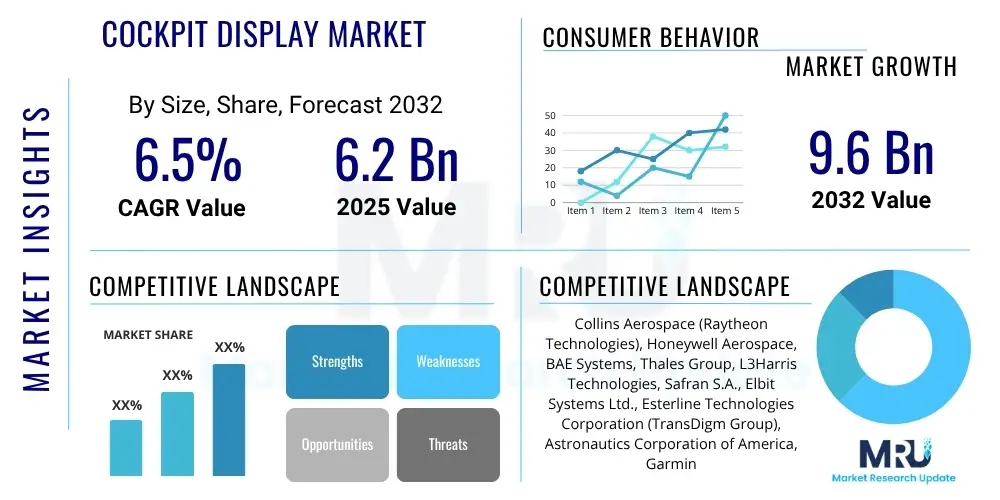

The Cockpit Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2032.

The Cockpit Display Market encompasses the design, manufacturing, and integration of advanced display systems used in aircraft cockpits to provide pilots with critical flight information, navigation data, and system status. These displays have evolved significantly from traditional analog gauges to highly integrated digital systems, enhancing situational awareness and reducing pilot workload. Modern cockpit displays are integral to aircraft operation, offering functionalities such as primary flight display (PFD), multi-function display (MFD), engine indicating and crew alerting system (EICAS), and head-up displays (HUDs).

Key products within this market include various types of display units, ranging from smaller, dedicated screens to large-format integrated displays that consolidate multiple information streams. These systems utilize sophisticated graphics processing and display technologies, such as LCD and OLED, to present data clearly and intuitively. Major applications span across commercial aircraft, military aviation, business jets, and helicopters, with increasing adoption in emerging segments like urban air mobility (UAM) and unmanned aerial systems (UAS). The primary benefits derived from these advanced displays include improved flight safety through enhanced data presentation, reduced operational costs due to streamlined maintenance, and increased operational efficiency through better decision-making support.

The market is primarily driven by the continuous modernization of existing aircraft fleets, the growing demand for new aircraft deliveries globally, and the relentless pursuit of reducing pilot workload while enhancing overall flight safety. Technological advancements, such as the integration of synthetic vision systems (SVS) and augmented reality (AR) into cockpit displays, further propel market expansion. Additionally, stringent aviation regulations mandating advanced avionics for improved safety and air traffic management play a crucial role in driving the adoption of sophisticated cockpit display solutions across the aviation industry.

The Cockpit Display Market is experiencing robust growth, primarily driven by the ongoing digitization of aircraft cockpits and the increasing demand for enhanced situational awareness and operational efficiency. Business trends indicate a strong shift towards larger, integrated display units, touch-screen interfaces, and the incorporation of advanced functionalities such as synthetic vision, augmented reality, and data fusion capabilities. Manufacturers are focusing on modular open systems architectures (MOSA) to offer greater flexibility and easier upgrades, catering to both new aircraft builds and the lucrative retrofit market for older fleets. There is also a notable emphasis on developing displays with improved readability under various lighting conditions, higher reliability, and reduced weight.

Regionally, North America continues to dominate the market due to the presence of major aircraft manufacturers, significant defense spending, and early adoption of advanced aerospace technologies. Europe also holds a substantial share, propelled by key aerospace players and a strong focus on research and development in avionics. The Asia Pacific region is projected to exhibit the highest growth rate, fueled by expanding air travel, a surge in new aircraft orders, and increasing defense modernization programs, particularly in countries like China and India. Latin America, the Middle East, and Africa are showing steady growth, driven by fleet expansion and the upgrading of existing aircraft to meet modern aviation standards.

Segmentation trends highlight the increasing preference for large-format displays that can integrate multiple functions, thereby reducing the number of individual screens and simplifying the cockpit environment. Multi-function displays (MFDs) and head-up displays (HUDs) are particularly prominent, offering pilots critical information directly in their line of sight. The aftermarket segment for retrofitting older aircraft with newer, more capable display systems is also a significant contributor to market growth. Technologically, OLED displays are gaining traction due to their superior contrast and viewing angles, although LCDs remain widely used. The market is also seeing a rise in the adoption of displays featuring enhanced cybersecurity measures to protect critical flight data from potential threats.

User inquiries regarding AI's impact on the Cockpit Display Market frequently center on how artificial intelligence will transform human-machine interface (HMI), enhance decision-making capabilities, and affect the role of pilots. Common questions explore the potential for AI to introduce more autonomous functions, improve data interpretation, and provide predictive insights, while also raising concerns about reliability, certification challenges, and the potential for over-reliance or automation complacency. Users are keen to understand if AI will lead to more intuitive and less cluttered displays, and how it might handle complex or unforeseen situations. The overarching theme is a balance between leveraging AI for efficiency and maintaining robust human oversight and safety. Expectations are high for AI to support advanced flight management and error detection without compromising the pilot's ultimate authority and control.

The Cockpit Display Market is profoundly influenced by a complex interplay of drivers, restraints, and opportunities, all shaped by significant impact forces. Key drivers include the escalating demand for advanced avionics to enhance flight safety and operational efficiency, driven by increasing air traffic globally and the continuous modernization programs undertaken by airlines and defense forces. The necessity to reduce pilot workload through intuitive, integrated display systems is another crucial driver. Furthermore, regulatory mandates from aviation authorities for improved cockpit technology and data presentation also propel market growth, as operators strive to comply with evolving standards and improve airworthiness. The introduction of new aircraft models with state-of-the-art cockpits also naturally boosts demand for advanced display solutions, integrating modern digital interfaces.

However, the market faces several significant restraints. The exceptionally high development costs associated with research, design, and manufacturing of advanced cockpit display systems present a substantial barrier to entry for new players and can slow innovation. The complex and lengthy certification processes required by aviation regulatory bodies, such as the FAA and EASA, add significant time and expense to product development and deployment. The long operational lifecycles of aircraft also mean that upgrade cycles for avionics can be extended, leading to slower market adoption for newer technologies. Additionally, growing concerns over cybersecurity threats to integrated digital cockpits necessitate robust security measures, increasing design complexity and cost. Supply chain disruptions, particularly for critical electronic components and rare earth materials, can also impact production schedules and market stability.

Opportunities within the market are abundant, particularly in the retrofit and upgrade segment for aging aircraft fleets, where operators seek to extend the life of their assets with modern avionics. The burgeoning urban air mobility (UAM) and unmanned aerial systems (UAS) markets present entirely new avenues for cockpit display applications, requiring specialized compact and highly intuitive interfaces. Integration of advanced technologies like augmented reality (AR) and virtual reality (VR) into next-generation displays offers significant potential for enhanced pilot training and real-time situational awareness. The shift towards personalized cockpits that adapt to individual pilot preferences and mission requirements also presents a novel growth opportunity. Furthermore, the development of more sustainable and energy-efficient display technologies aligned with environmental initiatives could carve out new market niches. These opportunities are heavily influenced by impact forces such as rapid technological advancements in display and processing power, the dynamic regulatory framework governing aviation safety and autonomy, the prevailing global economic conditions affecting defense and commercial aviation budgets, and geopolitical stability which impacts both manufacturing and operational environments.

The Cockpit Display Market is extensively segmented based on various critical parameters, allowing for a detailed analysis of market dynamics and growth opportunities across different product types, technologies, aircraft applications, display sizes, and end-use sectors. This segmentation helps in understanding specific demand patterns, technological preferences, and operational requirements unique to each category, thereby providing a comprehensive view of the market landscape. The intricate nature of aviation requirements dictates a diverse range of display solutions, from basic indicators to highly advanced, integrated flight decks.

The segmentation enables stakeholders to identify key growth areas, competitive advantages, and potential challenges. For instance, the distinction between OEM and aftermarket provides insights into the lifecycle demands of aircraft, while segmentation by aircraft type highlights the varying technological sophistication and regulatory needs across commercial, military, and general aviation sectors. Understanding these segments is crucial for strategic planning, product development, and market entry strategies within the highly specialized aerospace industry.

The value chain for the Cockpit Display Market is intricate, involving numerous specialized stages from raw material procurement to end-user application. The upstream segment is characterized by a reliance on highly specialized component manufacturers and raw material suppliers. This includes companies providing high-grade semiconductors for processors and graphics cards, display panel manufacturers (LCD, OLED), specialized glass and transparent conductors, and manufacturers of durable, lightweight housing materials. These suppliers often operate within a global network, requiring stringent quality control and supply chain management due to the critical nature of aerospace components. Research and development activities also form a crucial part of the upstream value chain, driving innovation in display technology, processing power, and interface design to meet evolving aviation demands.

Moving downstream, the value chain extends to system integrators and aircraft manufacturers (OEMs). These entities take the specialized components and integrate them into complete cockpit display systems, ensuring compatibility with the aircraft's avionics architecture and adherence to rigorous aviation safety standards. This phase involves extensive software development for display functionalities, human-machine interface design, and rigorous testing and certification processes. After the initial OEM installation, the distribution channel for cockpit displays primarily bifurcates into direct sales to major aircraft manufacturers for new builds and an indirect channel catering to the aftermarket. The direct channel involves close collaboration between display manufacturers and OEMs, often through long-term contracts and co-development efforts.

The indirect distribution channel primarily serves the aftermarket, which includes airlines, MRO (Maintenance, Repair, and Overhaul) facilities, and defense contractors involved in upgrading existing aircraft fleets. This channel often utilizes specialized avionics distributors and authorized service centers that provide sales, installation, and support for replacement and upgrade display units. These distributors play a vital role in reaching a broader customer base, including smaller airlines, private jet operators, and general aviation clients who may not have direct procurement relationships with the primary manufacturers. The aftermarket segment is particularly robust, driven by the need to modernize aging fleets with newer, more efficient, and compliant display technologies, extending the operational life and improving the safety profile of in-service aircraft.

The Cockpit Display Market caters to a diverse range of end-users and buyers, each with unique requirements and purchasing considerations, reflecting the multifaceted nature of the aviation industry. Commercial airlines represent a significant customer segment, driven by the need to equip their new fleet additions with advanced, integrated cockpits and to retrofit existing aircraft to enhance safety, efficiency, and comply with evolving air traffic management regulations. Military forces globally constitute another crucial segment, demanding highly robust, secure, and technologically superior displays for fighter jets, transport aircraft, and helicopters to support complex mission profiles and tactical operations.

Beyond large-scale operators, private jet owners and business aviation operators are key buyers, prioritizing sophisticated, user-friendly, and often customized cockpit display solutions that enhance comfort, reduce pilot workload, and support efficient executive travel. Helicopter operators, both commercial and military, also form a distinct customer group, requiring specialized displays optimized for rotorcraft-specific flight dynamics and mission types, such as search and rescue, offshore transport, and medical evacuation. General aviation pilots and aircraft owners, while perhaps seeking more cost-effective solutions, still demand reliable and increasingly advanced display technologies for their smaller aircraft.

Lastly, aircraft manufacturers (OEMs) are primary customers, as they integrate these display systems into new aircraft designs, often collaborating closely with display technology providers from the early stages of aircraft development. Additionally, Maintenance, Repair, and Overhaul (MRO) facilities and avionics upgrade centers serve as indirect customers, procuring cockpit displays and related components for their extensive retrofit and modernization projects. These diverse customer segments underscore the broad applicability and critical importance of advanced cockpit display systems across the entire aviation ecosystem, from initial manufacturing to ongoing operational support and upgrades.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $6.2 Billion |

| Market Forecast in 2032 | $9.6 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Collins Aerospace (Raytheon Technologies), Honeywell Aerospace, BAE Systems, Thales Group, L3Harris Technologies, Safran S.A., Elbit Systems Ltd., Esterline Technologies Corporation (TransDigm Group), Astronautics Corporation of America, Garmin Ltd., Universal Avionics (Elbit Systems of America), General Electric (GE Aviation), Curtiss-Wright Corporation, Saab AB, Leonardo S.p.A., Diehl Aerospace GmbH, Nordam Group Inc., EDMO Distributors Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Cockpit Display Market is at the forefront of aerospace technological innovation, constantly integrating cutting-edge advancements to enhance flight safety, efficiency, and pilot experience. The core of this landscape lies in the evolution of display panel technologies, with high-resolution LCDs continuing to dominate due to their maturity and reliability, while OLED and AMOLED displays are gaining significant traction. OLED technology offers superior contrast ratios, faster response times, and wider viewing angles, making it ideal for critical information display in varying light conditions. Furthermore, the integration of touch-screen interfaces is becoming standard, replacing traditional buttons and knobs to streamline pilot interaction and simplify cockpit layouts, though tactile feedback remains a design challenge.

Beyond the display panels themselves, advanced graphics processors and computing power are crucial for rendering complex visual information, including synthetic vision systems (SVS) that provide a clear 3D representation of the outside world regardless of visibility, and enhanced vision systems (EVS) that fuse infrared and other sensor data to improve visibility in low-light or adverse weather conditions. The trend towards large format displays (LFDs) is also prominent, consolidating multiple functionalities onto a single, expansive screen, thereby reducing panel clutter and improving information flow. These LFDs often feature modular open systems architecture (MOSA), allowing for easier upgrades, customization, and integration of new applications and software modules.

Future technological developments are geared towards integrating augmented reality (AR) and virtual reality (VR) capabilities directly into cockpit displays, particularly for advanced training simulations and real-time mission overlays. Data fusion technologies are becoming increasingly sophisticated, combining inputs from various onboard sensors and external data sources to present pilots with a comprehensive and intuitive operational picture. Cybersecurity technologies are also evolving rapidly, embedding robust encryption and intrusion detection systems to protect critical avionics data from potential cyber threats. Additionally, there is ongoing research into more resilient and power-efficient display materials, as well as haptic feedback systems for touch interfaces, ensuring that the cockpit display remains a secure, reliable, and highly interactive hub for flight operations.

The Cockpit Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032, driven by ongoing modernization and new aircraft deliveries.

Key drivers include the demand for advanced avionics to enhance safety and efficiency, aircraft modernization programs, efforts to reduce pilot workload, and stringent regulatory requirements for cockpit technology.

AI is enhancing displays through intelligent data fusion, predictive analytics, adaptive interfaces, and providing advanced decision support, leading to increased automation and improved situational awareness for pilots.

North America currently leads the market, closely followed by Europe. The Asia Pacific region is expected to show the fastest growth due to significant investments in new aircraft and defense modernization.

Key advancements include high-resolution OLED displays, touch-screen interfaces, synthetic and enhanced vision systems (SVS/EVS), large format integrated displays, and modular open systems architecture (MOSA) for greater flexibility.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.