ID : MRU_ 428262 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

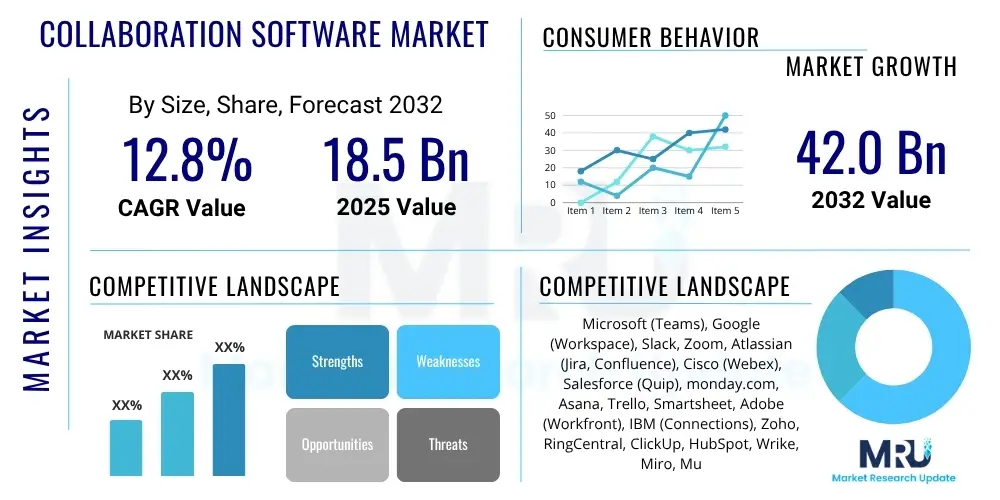

The Collaboration Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2032. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 42.0 Billion by the end of the forecast period in 2032.

The collaboration software market encompasses a wide array of tools and platforms designed to facilitate teamwork, communication, and information sharing among individuals and groups, regardless of their geographical location. These solutions are becoming indispensable for modern businesses, enabling seamless interaction and enhancing productivity in an increasingly remote and hybrid work environment. Products range from basic instant messaging applications to comprehensive suites integrating video conferencing, project management, document collaboration, and workflow automation functionalities.

Major applications of collaboration software span across virtually all industries and organizational sizes. Businesses leverage these tools for daily internal communications, project planning and execution, client meetings, document co-creation, and strategic planning. Educational institutions utilize them for virtual classrooms and administrative coordination, while healthcare providers adopt them for secure team communication and remote consultations. The overarching benefits include improved operational efficiency, streamlined workflows, enhanced team cohesion, accelerated decision-making, and increased overall productivity, leading to a significant return on investment for adopting organizations.

Key driving factors propelling the growth of this market include the widespread adoption of remote and hybrid work models, which necessitate robust digital communication and collaboration infrastructure. The ongoing trend of digital transformation across industries further fuels demand, as organizations seek to modernize their operations and leverage cloud-based solutions. Moreover, globalization and the increasing prevalence of geographically dispersed teams necessitate effective tools to maintain seamless communication and project continuity. Technological advancements, such as the integration of artificial intelligence and enhanced mobile accessibility, also continue to expand the capabilities and appeal of collaboration software.

The collaboration software market is experiencing robust expansion, primarily driven by evolving business models and the sustained prominence of remote and hybrid work arrangements globally. Key business trends include a pronounced shift towards integrated platforms that offer a comprehensive suite of tools, from messaging and video conferencing to project and document management, consolidating various functionalities into a single ecosystem. This integration enhances user experience and streamlines workflows, appealing to organizations seeking efficiency and simplified IT landscapes. Furthermore, the market is characterized by intense competition, fostering continuous innovation in features like AI-powered automation, advanced security protocols, and intuitive user interfaces. The SaaS model remains dominant, providing scalability and accessibility, making these solutions attractive to businesses of all sizes.

Regional trends indicate North America and Europe as mature markets, characterized by high adoption rates and a demand for sophisticated, enterprise-grade solutions with strong compliance features. The Asia Pacific (APAC) region, however, is emerging as a significant growth engine, fueled by rapid digital transformation initiatives, increasing internet penetration, and a burgeoning number of SMEs embracing digital tools. Latin America and the Middle East & Africa (MEA) are also showing promising growth, albeit from a smaller base, driven by improving digital infrastructure and a growing awareness of the benefits of collaborative technologies. These regions are increasingly targeted by global vendors looking to expand their footprint and capture new market share.

Segmentation trends highlight continued growth across all application areas, with particular emphasis on video conferencing and project management tools, which have become fundamental to distributed workforces. Messaging platforms continue to evolve, integrating deeper with other business applications and offering more advanced features beyond basic communication. Cloud-based deployment remains the preferred mode due to its flexibility, scalability, and reduced infrastructure overhead, while on-premise solutions cater to organizations with stringent security or regulatory requirements. Large enterprises are investing in comprehensive, highly customized platforms, whereas Small and Medium-sized Enterprises (SMEs) are opting for cost-effective, easy-to-deploy, and user-friendly solutions, underscoring the diverse needs within the market.

The integration of Artificial Intelligence (AI) is profoundly reshaping the collaboration software market, addressing common user questions about how technology can enhance productivity and streamline interactions. Users are keen to understand how AI can automate routine tasks, provide intelligent insights, and improve communication efficiency without compromising data privacy or creating an overly complex user experience. There is a strong expectation for AI to transform meeting summaries, facilitate easier information retrieval, and personalize collaborative environments, making teamwork more intuitive and less labor-intensive. Concerns often revolve around the accuracy of AI-generated content, potential biases, and the secure handling of sensitive organizational data, alongside the impact on job roles and the need for new skill sets to effectively leverage these advanced capabilities.

The evolving landscape of collaboration software is heavily influenced by these user expectations and concerns. Vendors are now focusing on embedding AI-driven functionalities that directly address these needs, aiming to deliver tangible value. This includes developing AI features that can intelligently filter notifications, suggest relevant content based on conversation context, and provide real-time language translation for global teams. The goal is to move beyond simple automation to truly intelligent assistance that anticipates user needs and proactively enhances the collaborative experience. This strategic direction is critical for maintaining competitiveness and meeting the escalating demands of modern enterprises for smarter, more efficient collaboration tools, all while ensuring robust security and ethical AI practices are in place.

The widespread adoption of AI within collaboration platforms is seen as a key differentiator, moving these tools from mere communication conduits to intelligent productivity engines. This shift implies a future where collaboration software will not only connect people but also augment their capabilities, making every interaction more impactful and every project more efficient. The continuous development in machine learning algorithms, natural language processing, and predictive analytics ensures that AI's role in collaboration will only grow, promising innovative solutions to long-standing challenges in teamwork and communication. However, managing user expectations and ensuring data governance will remain paramount as these technologies become more pervasive.

The collaboration software market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities, alongside various impact forces that shape its competitive landscape and growth trajectory. Key drivers include the pervasive shift towards remote and hybrid work models globally, which has fundamentally redefined how organizations operate and necessitated robust digital communication infrastructures. The acceleration of digital transformation initiatives across industries further propels demand, as businesses seek to modernize their workflows and enhance operational efficiency through integrated collaborative tools. Additionally, increasing globalization necessitates seamless communication across geographically dispersed teams, making collaboration software an indispensable asset for multinational corporations and international projects. The continuous evolution of cloud computing technologies also acts as a strong driver, offering scalable, flexible, and accessible solutions that reduce IT overhead for enterprises.

Despite these powerful drivers, the market faces several notable restraints. Data security and privacy concerns remain a paramount challenge, as organizations handle sensitive information across diverse platforms, leading to hesitation in adopting new solutions without stringent security assurances. The complexity of integrating collaboration software with existing legacy systems and other business applications can also hinder adoption, particularly for larger enterprises with intricate IT ecosystems. Furthermore, the perceived high initial investment for comprehensive enterprise-grade solutions, especially for Small and Medium-sized Enterprises (SMEs), can act as a barrier to entry. User resistance to change, requiring significant training and cultural shifts, also presents a soft restraint that vendors must address through intuitive design and robust support.

Opportunities for growth are abundant within the collaboration software market. The ongoing development and integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities offer significant potential for enhancing productivity through automation, intelligent insights, and personalized experiences. There is also a growing demand for vertical-specific collaboration solutions tailored to the unique needs of industries such as healthcare, finance, and education, allowing for deeper functionality and compliance. Moreover, untapped potential exists in emerging economies, where digital infrastructure is rapidly developing, and businesses are increasingly recognizing the value of digital collaboration. The continuous innovation in user interfaces, mobile optimization, and real-time communication protocols further expands the market's reach and attractiveness.

The impact forces influencing the market are multifaceted. The bargaining power of buyers is moderate to high, driven by a highly competitive market with numerous vendors offering diverse solutions, allowing customers significant choice and leverage. The bargaining power of suppliers, primarily technology providers for underlying infrastructure or specific components, is generally moderate. The threat of new entrants is moderate, as while barriers to entry exist in terms of development costs and market penetration, the SaaS model lowers some initial hurdles, and niche players can emerge. The threat of substitutes is low to moderate, as traditional communication methods are increasingly inadequate for modern business needs, though highly integrated enterprise resource planning (ERP) or customer relationship management (CRM) systems with built-in basic collaboration features can offer partial alternatives. Finally, the intensity of rivalry is high, with established giants and innovative startups fiercely competing on features, pricing, and market share, leading to continuous product development and aggressive marketing strategies.

The collaboration software market is extensively segmented to reflect the diverse needs and preferences of its global user base, providing a granular view of market dynamics across various dimensions. This segmentation helps identify specific growth opportunities, target distinct customer groups, and understand the competitive landscape more thoroughly. The primary segmentation criteria include deployment mode, component type, application area, enterprise size, and industry vertical, each revealing unique market trends and adoption patterns. Analyzing these segments provides strategic insights for vendors to tailor their offerings and for businesses to select solutions that best align with their operational requirements and strategic objectives. The detailed breakdown highlights how different technological preferences, operational scales, and industry-specific demands shape the demand for collaboration software.

The value chain for the collaboration software market involves several critical stages, from initial software development to its deployment and ongoing support, each contributing significantly to the final product and its market delivery. The upstream analysis primarily focuses on the foundational elements, including research and development, software coding, and infrastructure provisioning. This stage involves significant investment in talent for software engineering, user experience design, and cybersecurity expertise. Key upstream partners include cloud infrastructure providers (e.g., AWS, Azure, Google Cloud) that offer scalable computing resources and storage, as well as third-party component developers providing APIs, integration tools, and specialized modules that enhance the core functionality of collaboration platforms. Additionally, data analytics and AI/ML solution providers play a crucial role in enabling intelligent features, driving innovation at the very beginning of the value creation process.

Moving downstream, the value chain encompasses distribution, implementation, and post-sales support activities that bring the software to the end-users and ensure its effective utilization. This stage is critical for market penetration and customer satisfaction. Implementation services involve customizing the software to meet specific organizational needs, integrating it with existing enterprise systems, and migrating data. Training and onboarding services ensure that users can effectively leverage the new tools, maximizing adoption rates and productivity gains. Post-sales support, including technical assistance, maintenance, and regular updates, is paramount for maintaining customer loyalty and ensuring long-term product viability. Value-added resellers (VARs) and system integrators often play a vital role in this downstream segment, offering specialized expertise and localized support.

Distribution channels for collaboration software are typically a mix of direct and indirect approaches, designed to reach a broad customer base efficiently. Direct sales involve vendors selling their software directly to end-users, often through their websites, dedicated sales teams, or direct enterprise contracts. This channel allows for greater control over the customer relationship and provides opportunities for tailored solutions and direct feedback. Indirect channels, on the other hand, leverage a network of partners, including channel partners, resellers, distributors, and cloud marketplaces. These partners extend the vendor’s reach, particularly to SMEs or specific geographical regions, and often provide additional services like implementation and support. Cloud marketplaces (e.g., Salesforce AppExchange, Microsoft AppSource) are increasingly significant, offering a streamlined purchasing process and integrated solutions, further enhancing market accessibility and fostering an ecosystem of complementary applications.

The collaboration software market serves a vast and diverse ecosystem of potential customers, spanning across nearly every industry and organizational size. Fundamentally, any entity that requires coordinated effort, shared information, and effective communication among its members or with external stakeholders is a potential buyer. This includes the smallest startups aiming for agile team communication to the largest multinational corporations managing complex projects across global time zones. The universality of the need for teamwork makes the customer base exceptionally broad, but distinct segments emerge based on specific operational requirements, budget constraints, and industry-specific compliance demands. Understanding these nuances is crucial for vendors to tailor their offerings and marketing strategies effectively to maximize market penetration and address varied user needs.

Large enterprises represent a significant segment of potential customers, characterized by their demand for highly scalable, secure, and feature-rich collaboration suites that can integrate seamlessly with extensive existing IT infrastructures. These organizations often require advanced administrative controls, robust security features, extensive data governance capabilities, and comprehensive reporting tools to manage a large number of users and complex workflows. Industries such as Banking, Financial Services, and Insurance (BFSI), IT & Telecommunication, and Government & Public Sector are prominent in this segment, driven by their need for compliance, high-volume communication, and secure data handling. Their purchasing decisions often involve lengthy procurement processes and a focus on long-term value, reliability, and vendor support, making enterprise-grade solutions a critical investment.

Small and Medium-sized Enterprises (SMEs) constitute another substantial and rapidly growing customer segment. These businesses typically seek cost-effective, easy-to-deploy, and intuitive solutions that can quickly enhance productivity without requiring significant IT overhead or specialized technical expertise. For SMEs, the immediate benefits of improved communication, streamlined project management, and enhanced remote work capabilities are often the primary drivers for adoption. Industries like professional services, retail, and education, which benefit greatly from flexible and accessible collaboration tools, are key within this segment. The increasing availability of cloud-based, subscription-model software makes these solutions highly accessible and appealing to SMEs, enabling them to leverage enterprise-level functionalities without the prohibitive upfront costs. Furthermore, specialized solutions catering to niche needs within various industry verticals also broaden the customer base, ensuring that diverse operational demands are met.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2032 | USD 42.0 Billion |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Microsoft (Teams), Google (Workspace), Slack, Zoom, Atlassian (Jira, Confluence), Cisco (Webex), Salesforce (Quip), monday.com, Asana, Trello, Smartsheet, Adobe (Workfront), IBM (Connections), Zoho, RingCentral, ClickUp, HubSpot, Wrike, Miro, Mural, Box, Dropbox, Nextcloud, Mattermost, Rocket.Chat |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The collaboration software market is continuously shaped by a dynamic and evolving technology landscape, with advancements in various domains directly influencing the features, performance, and security of these platforms. At its core, cloud computing remains the foundational technology, enabling the scalability, accessibility, and cost-effectiveness of collaboration solutions delivered as Software-as-a-Service (SaaS). This allows users to access tools from anywhere, on any device, facilitating global and remote workforces. Beyond basic cloud infrastructure, the adoption of advanced cloud architectures, such as microservices and serverless computing, further enhances the agility and resilience of collaboration platforms, enabling rapid feature deployment and improved user experience. The pervasive nature of these cloud technologies underpins virtually all modern collaboration offerings.

Another critical area of technological innovation is Artificial Intelligence (AI) and Machine Learning (ML). These technologies are increasingly integrated to provide intelligent automation, personalized experiences, and actionable insights. AI powers features such as automated meeting transcription, smart scheduling, sentiment analysis in communications, and intelligent content recommendations, significantly boosting productivity and streamlining workflows. Natural Language Processing (NLP) is vital for understanding and processing human language in chat, voice, and video interactions, improving search capabilities and enabling sophisticated virtual assistants. The continuous refinement of AI algorithms allows collaboration tools to learn from user behavior, adapt to evolving needs, and proactively assist teams in their daily tasks, transforming the software from mere communication conduits to intelligent productivity partners.

Furthermore, real-time communication protocols and multimedia processing technologies are essential for high-quality video conferencing and instant messaging. WebRTC (Web Real-Time Communication) and other similar protocols ensure low-latency, secure communication directly within web browsers, eliminating the need for plug-ins. Enhanced audio and video codecs, coupled with AI-powered noise cancellation and background blurring, significantly improve the clarity and professionalism of virtual meetings. Cybersecurity technologies are also paramount, including end-to-end encryption, multi-factor authentication (MFA), and advanced threat detection systems, to protect sensitive organizational data and ensure compliance with global privacy regulations like GDPR and CCPA. Mobile integration, enabled by robust APIs and responsive design principles, ensures a seamless user experience across various devices, reflecting the increasingly mobile nature of the modern workforce and solidifying the market's technological backbone.

Collaboration software encompasses digital tools designed to facilitate teamwork, communication, and information sharing among individuals. It's essential for modern businesses due to the rise of remote and hybrid work, enabling seamless connectivity, improved productivity, streamlined workflows, and enhanced decision-making regardless of geographical location. It consolidates communication, project management, and document sharing into integrated platforms.

AI is significantly enhancing collaboration software by automating tasks like meeting summaries and transcriptions, providing intelligent content recommendations, optimizing schedules, and offering real-time language translation. It also contributes to personalized user experiences, enhanced security, and predictive analytics, transforming tools into smarter productivity partners that anticipate user needs and streamline operations.

Key drivers include the widespread adoption of remote and hybrid work models, accelerated digital transformation initiatives, and increasing globalization. Major restraints involve data security and privacy concerns, complexities in integrating with legacy systems, high initial costs for comprehensive solutions, and potential user resistance to new technologies, requiring careful vendor strategies.

Collaboration software sees widespread adoption across diverse industries. The largest adopters include IT & Telecommunication, Banking, Financial Services, and Insurance (BFSI), Healthcare & Life Sciences, and Government & Public Sector due to their complex operational needs and demand for secure, efficient communication. Education, Retail, and Manufacturing also represent significant and growing segments for these solutions.

The key deployment modes are cloud-based (public, private, hybrid) and on-premise solutions. Cloud-based deployment is generally the most preferred due to its inherent flexibility, scalability, accessibility, and lower upfront infrastructure costs. On-premise solutions cater to organizations with specific stringent security, compliance, or data sovereignty requirements, offering greater control over the infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.