ID : MRU_ 429660 | Date : Nov, 2025 | Pages : 242 | Region : Global | Publisher : MRU

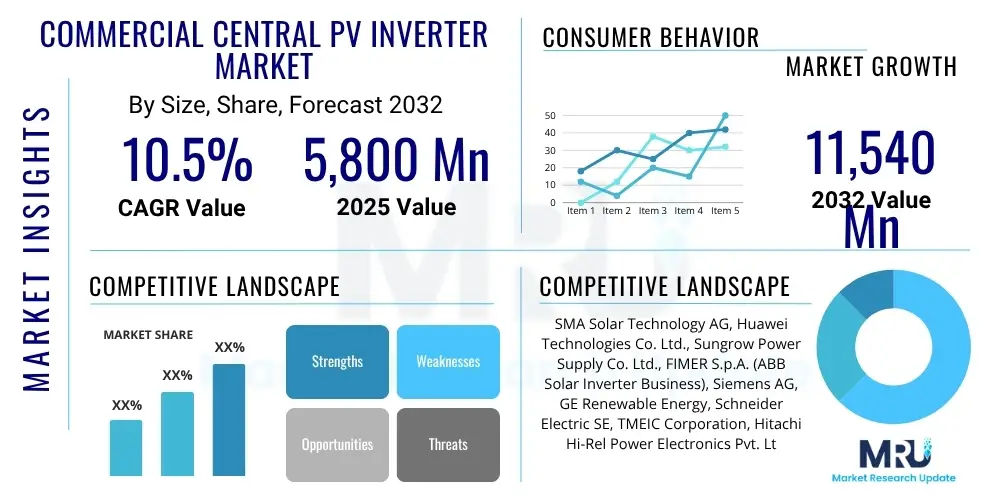

The Commercial Central PV Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2032. The market is estimated at USD 5,800 million in 2025 and is projected to reach USD 11,540 million by the end of the forecast period in 2032.

The Commercial Central PV Inverter Market represents a foundational and dynamically expanding segment within the global renewable energy ecosystem, dedicated to the vital technology that converts direct current (DC) electricity generated by photovoltaic (PV) solar panels into grid-compatible alternating current (AC) electricity. These sophisticated power electronics are meticulously engineered and optimized for large-scale solar installations, encompassing extensive utility-scale solar farms, significant commercial and industrial rooftop projects, and vast ground-mounted solar power systems. Central PV inverters are distinguished by their inherent robust construction, impressive high power output capabilities, and integrated advanced control features, all of which are absolutely essential for seamless, reliable integration into national electricity grids and for precisely optimizing energy harvesting from sprawling arrays of solar modules, thereby making a critical contribution to the ongoing global energy transition and decarbonization efforts. Their capacity to manage vast amounts of power makes them indispensable for commercial viability.

The core product, a central PV inverter, typically embodies a centralized architecture where multiple individual strings of solar panels are efficiently consolidated and directed to feed into a single, high-capacity, and powerful inverter unit. This specific design paradigm offers profound advantages, particularly in terms of significant cost-effectiveness per kilowatt (kW) installed for very large-scale solar power systems, streamlined installation processes, and simplified, more manageable maintenance routines due to fewer, larger, and more accessible components. Major applications for these high-performance inverters span from multi-megawatt (MW) ground-mounted solar power plants that meticulously feed electricity directly into national transmission networks, to large commercial complexes, extensive industrial facilities, and even large agricultural operations aiming for substantial reductions in their electricity bills, enhanced energy security, and improved corporate sustainability profiles. Key benefits associated with their deployment include exceptionally high power conversion efficiency rates, guaranteeing maximum energy yield from the solar array, superior operational reliability over extended periods of time, and integrated advanced grid management functionalities such as precise reactive power control, dynamic voltage stabilization, and critical frequency regulation, all of which are vital for maintaining grid stability and ensuring optimal power quality in modern, complex electricity networks.

Several potent and intertwined driving factors continue to fuel the vigorous expansion of this market. Foremost among these is the accelerating global imperative for sustainable and clean energy solutions, powerfully spurred by intensifying climate change concerns, increasingly stringent carbon emission reduction targets, and a profound worldwide strategic shift away from carbon-intensive fossil fuels towards renewable alternatives. Government policies, including generous capital subsidies, favorable tax incentives, attractive long-term feed-in tariffs, and ambitious renewable portfolio standards, play a consistently crucial role in creating a highly conducive and predictable investment environment for large-scale solar projects. Concurrently, continuous innovations and significant economies of scale achieved in manufacturing processes have led to a sustained and notable decline in the overall installed cost of solar photovoltaic panels and associated balance-of-system components, including the inverters themselves, making solar power increasingly competitive and often more economical than traditional energy sources. Furthermore, relentless technological advancements in core inverter design, encompassing dramatically improved efficiency metrics, enhanced thermal management systems, deeper integration with smart grid communication technologies, and robust advanced cybersecurity features, consistently boost the appeal, performance, and long-term viability of central inverters for increasingly ambitious and complex renewable energy projects across diverse geographies.

The Commercial Central PV Inverter Market is currently experiencing a period of robust growth and profound strategic transformation, primarily propelled by an escalating global commitment to renewable energy deployment and the undeniable economic advantages associated with large-scale solar power generation. Prominent business trends within this dynamic sector include a marked transition towards developing inverters with even higher power densities, allowing for more compact installations and reduced balance-of-system costs, alongside enhanced modularity, facilitating easier installation and maintenance for massive projects. There is also a significant emphasis on incorporating more sophisticated monitoring, control, and diagnostic systems, often leveraging cutting-edge artificial intelligence and machine learning algorithms, to proactively optimize performance, predict potential equipment issues before they escalate, and streamline operational management. Moreover, a growing focus on seamlessly integrated solutions that combine advanced PV inversion capabilities with robust battery energy storage systems (BESS) is fundamentally reshaping market offerings, providing greater grid flexibility, improved energy resilience, and creating diverse new revenue streams for project developers. The competitive landscape remains intensely innovative, with leading manufacturers consistently investing substantial resources into advanced research and development to introduce next-generation power electronics, sophisticated software solutions, and enhanced grid-support functionalities, ensuring continuous technological leadership and strong market differentiation in a rapidly evolving industry.

From a regional perspective, the Asia Pacific (APAC) region continues to exert its formidable dominance over the global market, primarily propelled by unparalleled investments in utility-scale solar projects across economic powerhouses like China, India, and Australia. These nations benefit significantly from highly supportive governmental frameworks, a vast and rapidly expanding energy demand driven by sustained economic growth and urbanization, and readily available, cost-effective manufacturing capabilities. North America and Europe represent mature yet robust growth markets, driven by increasingly ambitious renewable energy mandates, attractive federal and state-level incentives, and the increasing strategic adoption of solar power within the commercial and industrial sectors that are actively seeking long-term energy cost stability, enhanced energy security, and improved corporate environmental compliance. These regions are further characterized by a strong focus on extensive grid modernization initiatives and the deep integration of smart inverter functionalities to manage complex distributed energy resources. Emerging markets across Latin America, the Middle East, and Africa are concurrently demonstrating significant and accelerating growth potential, as these regions strategically prioritize renewable energy development to address persistent power deficits, foster sustainable economic development, and proactively mitigate environmental impacts, often supported by international financing initiatives and a wealth of untapped solar resources.

Segmentation trends within the market underscore several key shifts in demand, technological preference, and application focus. A pervasive and compelling trend involves the escalating demand for central inverters with increasingly higher power ratings, which deliver substantial economies of scale for large utility-scale projects by minimizing the number of discrete inverter units required, simplifying overall system design, reducing installation complexity, and lowering total balance-of-system costs. Furthermore, there is a distinct and growing move towards modular and scalable inverter designs that offer greater operational flexibility, easier capacity expansion to meet future energy demands, and improved serviceability throughout the inverter's lifecycle. While utility-scale solar farms unequivocally remain the predominant application segment and largest consumer of central PV inverters, the commercial and industrial (C&I) sector is exhibiting accelerating adoption rates, driven by businesses’ imperatives to lower operating expenses, improve corporate sustainability profiles, and enhance energy resilience against grid disturbances. The widespread integration of advanced functionalities such as precise maximum power point tracking, predictive analytics for component health, sophisticated fault detection mechanisms, and intelligent energy management systems is rapidly becoming a standard expectation for next-generation inverters, signifying the market's progression towards more intelligent, resilient, and high-performing solar energy solutions capable of meeting the rigorous demands of modern grids.

User inquiries frequently coalesce around the profound and transformative potential of Artificial Intelligence (AI) to revolutionize the efficiency, reliability, and grid integration capabilities of Commercial Central PV Inverter systems. Common questions extensively explore how AI can be leveraged to achieve unprecedented levels of energy yield optimization under dynamic conditions, precisely predict maintenance requirements before any critical failures occur, significantly enhance overall grid stability through intelligent and responsive control strategies, and substantially improve the long-term performance and economic viability of large-scale solar assets. There is a palpable and growing curiosity regarding AI's profound capacity to render vast solar farms more autonomous in their operation, drastically reduce operational expenditures (OpEx) by minimizing manual interventions and unplanned outages, and effectively mitigate the inherent intermittency challenges intrinsically associated with renewable energy sources. Stakeholders across the entire value chain hold strong, positive expectations that AI will unlock new paradigms of operational performance, significantly extend the effective lifespan of inverter systems, and ultimately forge a more robust, intelligent, interconnected, and resilient solar energy infrastructure capable of adapting to future energy demands and grid complexities.

The application of AI in the commercial central PV inverter market represents a pivotal and strategic shift towards smarter, more autonomous energy management and optimized operational processes. AI algorithms possess the capability to continuously analyze vast, real-time datasets, including intricate weather patterns, subtle panel degradation rates, complex grid demand fluctuations, and internal inverter health metrics, to make instantaneous and dynamic adjustments to inverter parameters. This intelligent, proactive optimization not only significantly boosts power conversion efficiency and overall energy harvesting but also ensures the inverter consistently operates within its most efficient and safest operational envelope, adapting to constantly changing conditions. Furthermore, AI-driven predictive maintenance capabilities leverage advanced machine learning models to detect subtle anomalies in inverter operation, component temperatures, or power output signatures that often precede major equipment failures. By accurately identifying these intricate patterns, maintenance teams can intervene pre-emptively and precisely, minimizing unexpected downtime, dramatically reducing costly emergency repairs, and extending the operational life of the entire solar power system, thereby enhancing the overall return on investment for asset owners and contributing to greater grid stability.

The Commercial Central PV Inverter Market is profoundly shaped by a dynamic interplay of potent driving factors, significant restraints, and compelling emerging opportunities, all operating under the persistent influence of broader socioeconomic, technological, and environmental impact forces. Key market drivers include the escalating global commitment to renewable energy deployment, rigorously underpinned by increasingly stringent environmental regulations, ambitious national decarbonization strategies, and a profound worldwide strategic shift away from carbon-intensive fossil fuels towards clean, sustainable alternatives. Supportive government policies, such as lucrative capital subsidies, favorable long-term tax credits, attractive feed-in tariffs, and ambitious renewable portfolio standards, collectively create a highly conducive and predictable investment climate for large-scale solar projects globally. Furthermore, a consistent and substantial reduction in the overall installed cost of solar electricity generation, powerfully driven by relentless advancements in module technology and significant manufacturing economies of scale, dramatically enhances the economic competitiveness of solar power. Concurrently, continuous and rapid technological advancements in core power electronics, materials science (e.g., wide-bandgap semiconductors like SiC and GaN), and sophisticated digital control systems are consistently improving inverter efficiency, reliability, longevity, and grid integration capabilities, making central inverters an increasingly attractive and indispensable component for ambitious renewable energy ventures worldwide. The ever-growing demand for sustainable, resilient, and cost-effective energy solutions across the commercial and industrial sectors further propels market expansion, as businesses globally seek to aggressively reduce their carbon footprint, achieve greater energy independence, and strategically hedge against volatile conventional energy prices.

Despite this robust growth trajectory and numerous advantages, the market navigates several notable and persistent restraints that require strategic mitigation. The substantial initial capital investment required for developing and deploying large-scale solar projects, which invariably includes the significant cost of central inverters and associated complex infrastructure, can often pose a considerable financial barrier for some investors and developers, frequently necessitating complex and innovative financing structures. Persistent concerns regarding grid stability and resilience, particularly in regions with less robust or aging electrical infrastructure, due to the inherent intermittency and variability of solar power generation, present ongoing technical and operational challenges that demand sophisticated forecasting and management solutions. Furthermore, the global supply chain, which is critically important for sourcing highly specialized electronic components and essential raw materials, remains susceptible to disruptions caused by geopolitical tensions, international trade disputes, or unforeseen global events like pandemics, leading to potential price volatility, extended lead times, and significant project delays. Intense competition among a growing number of domestic and international manufacturers, while fostering crucial innovation, can also lead to pervasive price erosion and compressed profit margins, especially in highly mature and saturated markets. The complexity and variability of regulatory frameworks and grid codes across different national and regional jurisdictions also pose significant hurdles for market entry and seamless cross-border expansion, demanding tailored compliance strategies and agile adaptation from market participants.

Nonetheless, the Commercial Central PV Inverter Market is brimming with substantial opportunities for accelerated growth and groundbreaking innovation. A particularly promising and rapidly expanding area is the increasingly synergistic integration of central PV inverters with advanced battery energy storage systems (BESS). This powerful hybrid approach offers enhanced grid flexibility, enables crucial peak shaving capabilities, provides essential grid ancillary services (like frequency regulation), and creates diverse new revenue streams for project developers, thereby dramatically increasing the overall value proposition and attractiveness of large-scale solar installations. Emerging markets in developing economies across Latin America, Africa, and parts of Asia, characterized by vast, largely untapped solar potential, rapidly increasing electricity demand, and often lacking extensive conventional grid infrastructure, represent fertile ground for substantial future expansion and investment. The ongoing development and deployment of advanced grid-forming inverters, capable of operating autonomously and providing critical black-start and grid-support functionalities, opens exciting new possibilities for strengthening grid resilience, facilitating robust microgrid development, and enabling powerful remote power solutions in off-grid or weak-grid areas. Additionally, the broader global emphasis on comprehensive digital transformation within the energy sector, coupled with the accelerating adoption of sophisticated smart grid infrastructure, provides a fertile ecosystem for continuous innovation and strategic expansion for manufacturers of advanced central PV inverters, enabling the construction of smarter, more resilient, and deeply interconnected energy systems worldwide.

The Commercial Central PV Inverter Market is meticulously segmented to offer a granular and exhaustive understanding of its intricate dynamics, catering to the diverse operational requirements and technological preferences across the global solar energy industry. This comprehensive segmentation facilitates an in-depth analysis of various product classifications based on inverter technology, specific power output capabilities, target application sectors, and distinct end-use categories, each characterized by unique market forces and specific growth trajectories. Such detailed market stratification is indispensable for all industry stakeholders, including manufacturers, project developers, investors, and policymakers, enabling them to precisely identify high-potential growth segments, strategically refine product portfolios, develop highly competitive pricing strategies, and formulate highly targeted and effective market entry and expansion initiatives. The market is primarily categorized based on the underlying inverter technology employed, the specific power rating the unit delivers, and the intended application or end-use environment where these high-capacity inverters are deployed, collectively reflecting the breadth and profound depth of the market's operational landscape and its multifaceted demands.

Understanding these granular segments is paramount for informed strategic planning and successful market navigation. For instance, the 'By Type' segmentation distinctly differentiates between central, string, and micro inverters, with central inverters unequivocally dominating large-scale commercial and utility applications due to their inherent high power output, superior efficiency, and cost-effectiveness for vast arrays. The 'By Power Rating' segment critically highlights the escalating demand for increasingly higher capacity units, particularly those above 1 MW, a trend powerfully driven by the compelling economies of scale achievable in utility-scale project development. The 'By Application' dimension clearly delineates the primary use cases, with utility-scale solar farms consistently representing the largest and most significant consumer segment, though commercial and industrial rooftops and ground-mounted systems are rapidly gaining substantial traction as businesses prioritize energy independence and sustainability. Finally, the 'By End-Use' segment details the ultimate buyers and beneficiaries, ranging from independent power producers managing colossal solar assets to diverse commercial businesses seeking significant energy cost reductions and greater energy self-sufficiency. Each segment's specific drivers, unique challenges, and competitive dynamics necessitate a highly tailored approach from market participants to effectively capture value, innovate, and foster sustainable growth within their chosen niches across the global solar energy value chain.

The value chain for the Commercial Central PV Inverter Market is a complex, multi-layered, and highly interconnected network of activities, commencing with the meticulous sourcing of raw materials and highly specialized electronic components, progressing through advanced manufacturing and assembly, and culminating in the long-term operation, maintenance, and comprehensive support of deployed inverter systems. The upstream segment of this value chain is fundamentally characterized by the procurement of critical and advanced electronic components and essential raw materials. This includes high-performance semiconductors, such as cutting-edge Silicon Carbide (SiC) and Gallium Nitride (GaN) for power switches, robust high-grade capacitors, specialized magnetic components like inductors and transformers, efficient cooling systems, and durable, weather-resistant enclosures. These crucial components are sourced from a highly specialized and often global network of suppliers who possess deep expertise in precision manufacturing, advanced material science, and stringent quality control. Manufacturers of central PV inverters heavily rely on these strategic suppliers to consistently ensure the superior quality, unwavering reliability, and compelling cost-effectiveness of their intricate end products, frequently engaging in long-term strategic partnerships to secure stable supply chains, foster collaborative innovation in component technology, and mitigate supply risks.

The midstream phase primarily encompasses the sophisticated manufacturing, precise assembly, and meticulous integration processes skillfully undertaken by inverter manufacturers. This critical stage involves the intricate design and advanced engineering of the inverter architecture, meticulously incorporating state-of-the-art power electronics, complex digital control algorithms, and multi-protocol communication interfaces. Manufacturers invest substantial resources and intellectual capital in continuous research and development to relentlessly optimize power conversion efficiency, enhance operational reliability, ensure robust grid compatibility under diverse conditions, and embed smart features such as predictive analytics, remote diagnostics, and advanced cybersecurity measures. Rigorous multi-stage quality control, extensive environmental and electrical testing, and strict adherence to stringent international certification standards (e.g., UL, IEC, CE, TUV) are absolutely paramount to ensure the utmost safety, superior performance, and extended longevity of the central inverters before they are ultimately dispatched to the global market. This phase also includes the development of proprietary software and firmware that enables sophisticated advanced monitoring, granular control, and precise diagnostic capabilities, adding substantial and enduring value to the core hardware product.

The downstream segment of the value chain is focused on the critical activities of distribution, strategic sales, meticulous installation, and comprehensive post-sales support services. Central PV inverters reach their ultimate end-users through a combination of highly efficient direct and indirect distribution channels tailored to market size and complexity. Direct sales are particularly prevalent for very large utility-scale projects, where manufacturers establish direct, long-term relationships with major utility companies, independent power producers (IPPs), and large Engineering, Procurement, and Construction (EPC) contractors, facilitating large volume transactions and bespoke solutions. Indirect channels involve a robust and extensive network of authorized distributors, specialized wholesalers, and value-added resellers who effectively cater to a broader spectrum of commercial and industrial customers, including smaller EPC firms, local system integrators, and independent installers. The installation process typically involves highly specialized solar integrators and experienced EPC contractors who are responsible for the comprehensive design, efficient procurement, and precise physical implementation of the entire solar power system, seamlessly integrating the inverters with solar panels, cabling, and grid connections. Crucially, comprehensive post-sales services, encompassing robust warranty provisions, ongoing proactive maintenance agreements, sophisticated remote monitoring capabilities, and responsive technical support, form an absolutely vital part of the downstream chain. These services ensure the sustained optimal performance, maximize uptime, and guarantee the long-term economic viability and return on investment of the installed central PV inverter systems, thereby cementing strong customer loyalty and driving valuable repeat business in a highly competitive market.

The Commercial Central PV Inverter Market serves a remarkably diverse and continuously expanding base of potential customers, primarily composed of entities deeply involved in large-scale electricity generation, extensive commercial operations, and heavy industrial processes that actively seek robust, highly reliable, and sustainable energy solutions to meet their growing power demands. The most significant and impactful segment of buyers comprises major utility companies, often publicly or privately owned, alongside Independent Power Producers (IPPs). These powerful entities are the primary developers, owners, and operators of colossal utility-scale solar farms, which are strategically designed to feed substantial amounts of electricity directly into national or regional power grids. Their demand for central inverters is unequivocally characterized by the need for exceptionally high power ratings, unparalleled efficiency metrics, long-term operational reliability, seamless scalability to gigawatt-scale projects, and the critical capability to provide essential grid support functions such as precise voltage and frequency regulation, which are absolutely vital for maintaining grid stability and ensuring optimal power quality in complex transmission networks. Purchasing decisions for these sophisticated customers are typically influenced by a comprehensive assessment of factors like total cost of ownership (TCO), a proven track record of performance and reliability, superior inverter efficiency metrics, robust and extensive warranty terms, and the manufacturer's ability to offer comprehensive technical support, innovative financing solutions, and custo

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 5,800 million |

| Market Forecast in 2032 | USD 11,540 million |

| Growth Rate | 10.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SMA Solar Technology AG, Huawei Technologies Co. Ltd., Sungrow Power Supply Co. Ltd., FIMER S.p.A. (ABB Solar Inverter Business), Siemens AG, GE Renewable Energy, Schneider Electric SE, TMEIC Corporation, Hitachi Hi-Rel Power Electronics Pvt. Ltd., Power Electronics S.L., Fronius International GmbH, Kostal Solar Electric GmbH, Ginlong Technologies (Solis), Delta Electronics, Inc., Growatt New Energy Technology Co. Ltd., Enphase Energy, SolarEdge Technologies, Inc., GoodWe Technologies Co. Ltd., Canadian Solar Inc., Gamesa Electric S.A.U. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

A Commercial Central PV Inverter is an advanced electrical device specifically engineered for large-scale solar installations, encompassing vast utility-scale solar farms and extensive commercial or industrial projects. Its primary function is to efficiently and reliably convert the direct current (DC) electricity generated by photovoltaic (PV) solar panels into grid-compatible alternating current (AC) electricity, making it suitable for utilization by commercial applications or for seamless feeding into the national electricity grid. These inverters are typically robust, high-power units serving multiple strings of solar panels and are critical for maximizing energy harvest and ensuring stable grid integration.

Deploying Central PV Inverters in large-scale solar projects offers several crucial benefits and advantages. These include exceptionally high power conversion efficiency, which significantly maximizes energy yield from the vast solar array, leading to greater electricity generation. They provide substantial cost-effectiveness due to economies of scale and simplified installation processes for extensive installations. Furthermore, they offer robust operational reliability over long lifespans and integrate advanced grid management features, such as precise reactive power control, dynamic voltage stabilization, and critical frequency regulation, all vital for maintaining grid stability and ensuring optimal power quality in modern, complex electrical grids.

Artificial Intelligence is profoundly transforming the Commercial Central PV Inverter Market by significantly enhancing performance and reliability across multiple dimensions. AI algorithms optimize energy yield through real-time adaptive control mechanisms, precisely predict and prevent maintenance issues via sophisticated analytics, and bolster grid stability by intelligently managing reactive power and voltage. Moreover, AI improves fault detection, integrates PV systems with energy storage for optimal dispatch, and strengthens cybersecurity protocols, leading to more efficient, resilient, and autonomous solar energy operations, thereby optimizing investment returns and operational continuity.

The Asia Pacific (APAC) region, particularly spearheaded by countries like China and India, is currently experiencing the most significant growth and investment in the Commercial Central PV Inverter Market due to massive utility-scale project development and robust government support. North America and Europe also demonstrate strong, consistent growth, driven by ambitious renewable energy mandates and increasing commercial and industrial solar adoption. Emerging markets in Latin America and the Middle East and Africa are rapidly expanding, fueled by abundant solar resources, rising energy demands, and strategic investments in renewable infrastructure.

The primary technological advancements driving innovation and competitiveness include the increasing adoption of wide bandgap semiconductors (SiC, GaN) for enhanced efficiency and compactness, the integration of advanced Maximum Power Point Tracking (MPPT) algorithms for optimal energy harvesting, and the development of grid-forming capabilities to provide essential grid support functions. Furthermore, extensive digitalization, cloud-based monitoring platforms, robust cybersecurity features, and highly modular designs are key innovations contributing to smarter, more reliable, higher-performing, and cost-effective central PV inverter solutions that meet evolving market demands and regulatory requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.