ID : MRU_ 430588 | Date : Nov, 2025 | Pages : 241 | Region : Global | Publisher : MRU

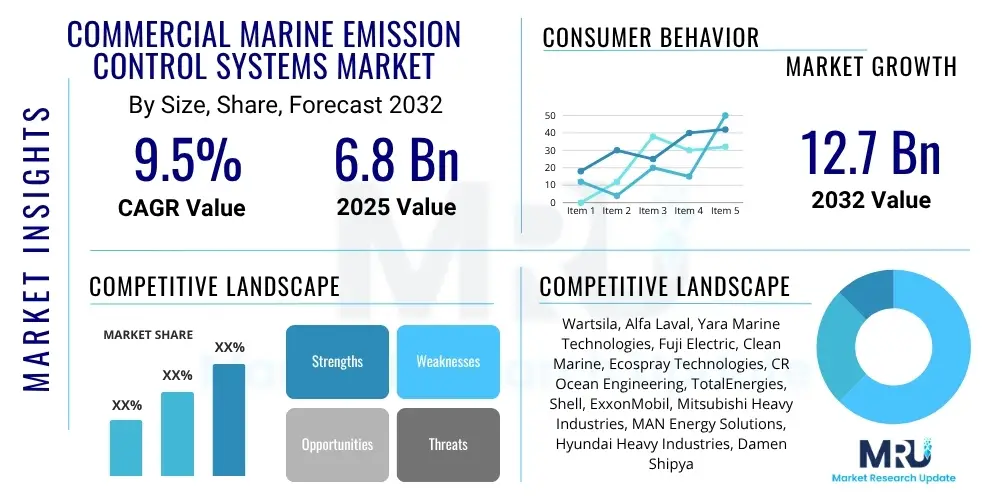

The Commercial Marine Emission Control Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 12.7 Billion by the end of the forecast period in 2032.

The Commercial Marine Emission Control Systems market is undergoing significant transformation driven by an imperative to mitigate the environmental impact of global shipping. These systems encompass a range of technologies designed to reduce harmful emissions such as sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter (PM) from marine engines. Products include Exhaust Gas Cleaning Systems (EGCS), also known as scrubbers, Selective Catalytic Reduction (SCR) systems, and various fuel optimization solutions. Major applications span across diverse vessel types, including container ships, bulk carriers, oil tankers, cruise liners, and ferries, all striving for compliance with international and regional environmental regulations.

The primary benefits of implementing these control systems include adherence to stringent regulations like the IMO 2020 sulfur cap, reduction of air pollution in coastal areas and port cities, and improved public perception of the shipping industry. Moreover, some technologies allow vessels to continue using more cost-effective high-sulfur fuel while meeting emissions limits, potentially offering operational cost advantages. Key driving factors for market growth involve the escalating global trade volumes necessitating increased shipping activity, the continuous tightening of environmental protection laws by international bodies such as the International Maritime Organization (IMO) and local authorities, and growing societal awareness concerning climate change and marine ecosystem preservation.

The Commercial Marine Emission Control Systems market is characterized by robust business trends emphasizing technological innovation, strategic partnerships, and a shift towards integrated solutions. Companies are investing heavily in research and development to offer more efficient, compact, and cost-effective systems that simplify retrofitting and minimize operational disruption. There is a discernible trend towards digitalization, with solutions incorporating data analytics and automation for enhanced performance monitoring and predictive maintenance. Consolidation within the market is also observed, as larger entities acquire specialized technology providers to expand their product portfolios and market reach, fostering an environment of competitive advancement.

Regionally, the market exhibits dynamic growth with Asia Pacific emerging as a dominant force, propelled by its extensive shipbuilding industry, bustling trade routes, and increasing adoption of emission control technologies, particularly in countries like China, South Korea, and Japan. Europe continues to be a crucial market, driven by its stringent environmental directives and a strong commitment to decarbonization within its maritime sector, fostering innovation and early adoption. North America is also a significant market due to its Emission Control Areas (ECAs) along its coasts. Segment trends indicate a sustained demand for EGCS, especially hybrid scrubbers, as they provide operational flexibility. Simultaneously, the adoption of SCR systems is accelerating to address NOx emissions, while interest in alternative fuels like LNG, methanol, and ammonia is shaping the long-term trajectory of the market, necessitating adaptable emission control solutions.

User inquiries regarding the impact of Artificial Intelligence (AI) on Commercial Marine Emission Control Systems frequently center on how AI can enhance efficiency, reduce operational costs, and ensure continuous regulatory compliance. Users express interest in AI's potential for predictive maintenance, optimizing system performance in real-time, and enabling more sophisticated data analysis from diverse sensor inputs. There is also a notable expectation that AI could play a pivotal role in the future of autonomous shipping and integrate seamlessly with next-generation propulsion systems, contributing to overall vessel decarbonization strategies. Concerns often revolve around the initial investment costs, the complexity of integrating AI with existing legacy systems, data security vulnerabilities, and the need for skilled personnel to manage and interpret AI-driven insights within the maritime context.

The Commercial Marine Emission Control Systems market is profoundly shaped by a combination of powerful drivers, challenging restraints, and promising opportunities, all influenced by dynamic impact forces. Drivers predominantly include increasingly stringent global and regional environmental regulations, such as the IMO 2020 sulfur cap and forthcoming IMO greenhouse gas reduction targets, compelling shipowners to invest in compliant technologies. The rising public and corporate pressure for sustainable shipping practices, alongside a growing understanding of the environmental and health impacts of marine emissions, further accelerates market demand. Technological advancements enabling more efficient and cost-effective solutions also serve as a significant catalyst.

However, the market faces notable restraints, primarily the high upfront capital expenditure required for installing and retrofitting emission control systems, which can be a substantial barrier for smaller shipping companies. The operational costs associated with maintenance, consumables (like urea for SCRs), and waste disposal (for closed-loop scrubbers) also present financial challenges. Furthermore, the complexity of integrating these advanced systems into existing vessel infrastructure and the limited global availability of bunkering infrastructure for alternative fuels like LNG or methanol can hinder widespread adoption. These factors necessitate careful financial planning and strategic decision-making by fleet operators.

Opportunities within the market are vast and evolving, encompassing the development of hybrid and electric propulsion systems, the integration of advanced digital and AI-driven solutions for emission optimization, and the innovation in carbon capture and storage technologies for marine applications. The growing demand for sustainable maritime transport fuels also presents an avenue for emission control system manufacturers to develop adaptable solutions for these next-generation energy sources. Impact forces such as geopolitical shifts affecting global trade, economic volatility influencing shipping company investments, and the continuous evolution of environmental science and policy play critical roles in shaping the market's trajectory, requiring stakeholders to remain agile and forward-thinking.

The Commercial Marine Emission Control Systems market is comprehensively segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market trends, technological preferences, and application-specific demands, enabling stakeholders to identify key growth areas and formulate targeted strategies. The market is primarily categorized by technology type, fuel type, application, and vessel type, each revealing distinct adoption patterns and future potential. This multi-faceted approach ensures that the analysis captures the full spectrum of solutions addressing maritime emissions.

The value chain for Commercial Marine Emission Control Systems encompasses several critical stages, from the sourcing of raw materials and component manufacturing to the final installation, operation, and maintenance of these complex systems. Upstream activities involve a diverse network of suppliers providing specialized components such as catalysts, pumps, filters, sensors, and structural materials essential for building scrubbers, SCR units, and fuel treatment systems. These suppliers, often global, must meet stringent quality and performance standards to ensure the reliability and efficacy of the final emission control product. Research and development also play a significant upstream role, driving innovation in materials science and system design to meet evolving regulatory demands and performance expectations.

Midstream in the value chain, original equipment manufacturers (OEMs) and system integrators design, assemble, and test the complete emission control solutions. This phase involves intricate engineering to customize systems for various vessel types and operational profiles, ensuring seamless integration with existing engine and exhaust infrastructures. Downstream activities focus on the installation, commissioning, and aftermarket services. Shipyards and specialized marine engineering firms are responsible for the physical installation, either for newbuilds or retrofits, which often requires significant planning and technical expertise. Distribution channels are varied, incorporating direct sales from OEMs to shipowners, partnerships with shipyards, and a network of distributors and agents who facilitate sales, logistics, and localized support globally. Both direct sales, offering close client relationships and customized solutions, and indirect channels through established marine equipment suppliers are crucial for market penetration and customer reach, ensuring comprehensive coverage and support throughout the lifecycle of the emission control systems.

The primary potential customers and end-users of Commercial Marine Emission Control Systems comprise a broad spectrum of entities within the global maritime industry, all driven by the imperative to comply with environmental regulations and enhance their operational sustainability. Shipping companies, ranging from large multinational corporations operating extensive fleets of container ships, bulk carriers, and oil tankers, to smaller regional operators of general cargo vessels and ferries, represent the largest segment of buyers. These entities require emission control solutions to ensure their vessels can operate legally and efficiently across international waters and within Emission Control Areas (ECAs).

Cruise lines constitute another significant customer base, often requiring advanced and aesthetically integrated emission control systems due to their direct interaction with passengers and frequent calls at environmentally sensitive port cities. Ferry operators, particularly those serving coastal and inland waterways, also form a critical segment, facing localized environmental pressures and regulations. Furthermore, offshore oil and gas companies operating specialized support vessels, platform supply vessels, and anchor handling tug supply (AHTS) vessels increasingly invest in these systems to meet stringent environmental standards in their operational zones. Government agencies and naval forces, though not strictly commercial, may also procure such systems for their auxiliary fleets to demonstrate environmental stewardship and comply with similar standards to commercial shipping.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2032 | USD 12.7 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Wartsila, Alfa Laval, Yara Marine Technologies, Fuji Electric, Clean Marine, Ecospray Technologies, CR Ocean Engineering, TotalEnergies, Shell, ExxonMobil, Mitsubishi Heavy Industries, MAN Energy Solutions, Hyundai Heavy Industries, Damen Shipyards Group, Kongsberg Maritime, Schottel, Andritz AG, VDL AEC Maritime, SAACKE GmbH, Valmet Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Commercial Marine Emission Control Systems market is defined by a dynamic and continuously evolving technology landscape, with innovations aimed at improving efficiency, reducing operational costs, and ensuring compliance with increasingly strict environmental regulations. Exhaust Gas Cleaning Systems (EGCS), commonly known as scrubbers, remain a prominent technology, available in open-loop, closed-loop, and hybrid configurations. These systems remove sulfur oxides (SOx) from exhaust gases, allowing vessels to continue using heavy fuel oil while meeting sulfur emission limits. Advancements in scrubber technology focus on compactness, ease of installation, and improved wastewater treatment for closed-loop systems, making them more adaptable to various vessel sizes and operational profiles. The development of modular and hybrid designs offers greater flexibility for shipowners, balancing operational costs with environmental performance.

Selective Catalytic Reduction (SCR) systems are crucial for controlling nitrogen oxide (NOx) emissions, particularly for engines operating in Emission Control Areas (ECAs). SCR technology involves injecting a reducing agent, typically urea, into the exhaust gas stream, which then reacts with NOx over a catalyst to convert it into harmless nitrogen and water. Recent developments in SCR focus on optimizing catalyst life, reducing the footprint of the system, and improving performance across varying engine loads. Additionally, technologies related to marine fuel optimization, such as fuel emulsification systems and fuel additive solutions, are gaining traction by improving combustion efficiency and thereby reducing particulate matter and black carbon emissions. The burgeoning interest in alternative fuels like Liquefied Natural Gas (LNG), methanol, and ammonia is also driving innovation in specialized fuel handling and combustion technologies, along with the associated emission after-treatment systems tailored for these new energy sources, representing a significant shift towards future marine propulsion solutions.

Commercial Marine Emission Control Systems are technologies installed on vessels to reduce harmful emissions from marine engines, such as sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter, ensuring compliance with international and regional environmental regulations.

These systems are crucial for protecting air quality and marine ecosystems by reducing pollutants. They enable shipping companies to comply with global regulations like IMO 2020 and regional Emission Control Areas (ECAs), while also enhancing corporate sustainability profiles and avoiding penalties.

IMO 2020 is a regulation by the International Maritime Organization that mandates a global sulfur cap of 0.5% for marine fuel. It significantly impacts the market by driving demand for Exhaust Gas Cleaning Systems (scrubbers) or the use of compliant low-sulfur fuels, boosting the market for emission control solutions.

Key technologies include Exhaust Gas Cleaning Systems (EGCS), also known as scrubbers, for SOx reduction; Selective Catalytic Reduction (SCR) systems for NOx reduction; and various fuel optimization solutions. Other emerging technologies involve alternative fuels and carbon capture systems.

AI enhances marine emission control by enabling predictive maintenance, real-time operational optimization of systems, improved data analysis for compliance reporting, and contributing to overall vessel energy efficiency. It aids in proactive management and decision-making for sustainable shipping operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.