ID : MRU_ 428162 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

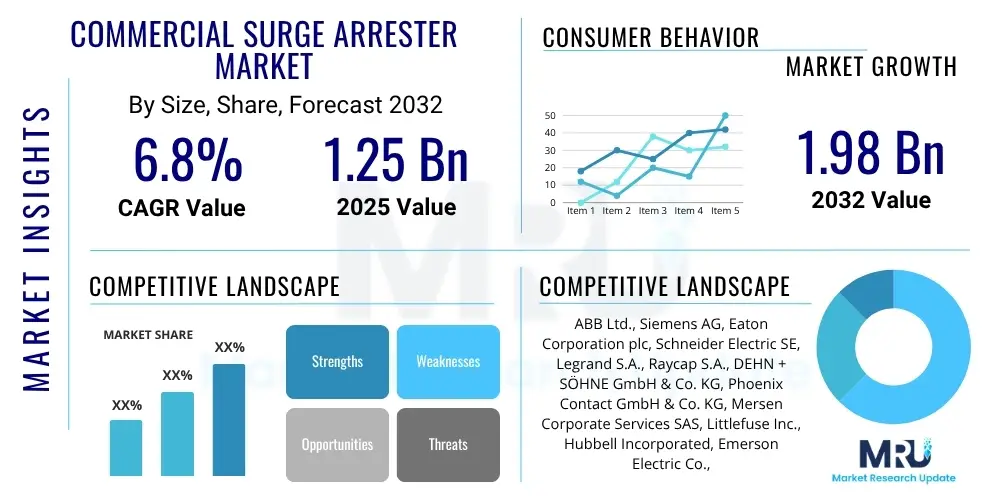

The Commercial Surge Arrester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 1.98 Billion by the end of the forecast period in 2032.

The Commercial Surge Arrester Market is a critical component within modern electrical infrastructure, primarily designed to protect sensitive electronic equipment and electrical systems from transient overvoltages. These overvoltages, often caused by lightning strikes, utility switching, or electrical faults, can lead to significant damage, operational downtime, and costly repairs. Surge arresters divert excess voltage to the ground, thereby safeguarding connected assets and ensuring continuity of operations. The market encompasses a broad range of products, from low-voltage devices for commercial buildings to medium and high-voltage arresters crucial for industrial facilities and utility grids. As digitalization intensifies across commercial sectors, the reliance on stable power supply and robust protection mechanisms for sophisticated electronics grows exponentially, making surge arresters indispensable for maintaining operational integrity and data security. The continuous advancement in material science and engineering practices further enhances the performance and reliability of these devices, providing tailored solutions for an ever-growing array of commercial and industrial applications.

Key product descriptions within this market vary by voltage level, protection capacity, and underlying technology. Low-voltage surge arresters are typically used for protection at the service entrance of commercial buildings and within power distribution panels, often employing Metal Oxide Varistor (MOV) or Silicon Avalanche Diode (SAD) technologies. Medium and high-voltage arresters, vital for industrial plants, data centers, and telecommunications infrastructure, utilize more robust MOVs or Gas Discharge Tubes (GDTs, particularly for outdoor applications) to handle higher energy surges. The major applications span across utilities, industrial manufacturing, data centers, telecommunications, healthcare, and commercial real estate, where uninterrupted power and equipment longevity are paramount. The benefit derived from these devices is substantial, extending beyond mere equipment protection to encompass enhanced operational safety, reduced maintenance costs, and prolonged asset life, directly contributing to business resilience against unpredictable electrical disturbances.

Driving factors for the market's expansion are multifaceted, including the escalating global demand for reliable electricity, rapid industrialization and urbanization, particularly in emerging economies, and the increasing adoption of renewable energy sources that integrate complex grid infrastructure requiring advanced protection. Furthermore, the rising proliferation of sensitive electronic equipment in commercial and industrial settings, coupled with a growing awareness among businesses regarding the economic repercussions of power quality issues, fuels the demand for robust surge protection solutions. Regulatory mandates and evolving international standards for electrical safety also play a significant role in stimulating market growth. The ongoing modernization of aging electrical grids and the strategic investments in smart city projects worldwide further underscore the vital role of commercial surge arresters in ensuring energy security and infrastructure longevity. This confluence of technological advancements, economic development, and heightened safety consciousness positions the commercial surge arrester market for sustained growth over the forecast period.

The Commercial Surge Arrester Market is currently experiencing robust growth, primarily driven by increasing investments in smart grid infrastructure, the proliferation of sensitive electronic equipment across various commercial sectors, and a heightened focus on electrical safety and operational continuity. Business trends indicate a strong shift towards advanced, intelligent surge protection devices that offer not only superior performance but also integrate monitoring and diagnostic capabilities, allowing for predictive maintenance and enhanced system reliability. The expansion of data centers, telecommunication networks, and industrial automation facilities globally further necessitates sophisticated surge protection solutions, as any downtime due to power transients can result in significant financial losses and operational disruptions. Furthermore, evolving regulatory landscapes and stricter compliance standards for electrical installations are compelling businesses to adopt high-quality surge arresters, thereby bolstering market demand and driving innovation towards more efficient and compact designs. Companies are increasingly exploring customization and integrated solutions to cater to diverse industry requirements, reflecting a dynamic and competitive market environment.

Regionally, the market exhibits varied growth trajectories, with Asia Pacific emerging as a dominant force due to rapid industrialization, extensive infrastructure development projects, and substantial investments in smart cities and renewable energy in countries like China and India. North America and Europe, characterized by established grids and early adoption of advanced technologies, show steady growth, driven by grid modernization initiatives, aging infrastructure replacement, and stringent safety regulations. Latin America and the Middle East & Africa are poised for significant expansion, fueled by increasing electrification rates, urbanization, and burgeoning industrial sectors. These regions represent substantial untapped potential, as economic development invariably leads to greater demand for reliable power supply and protective electrical equipment. The strategic focus of manufacturers on expanding distribution networks and localized production capabilities in these high-growth regions is a testament to their rising importance in the global market landscape.

Segment-wise, the market is primarily categorized by voltage type, technology, application, and deployment. The low-voltage segment holds a substantial share due to its widespread application in commercial buildings, IT infrastructure, and various small to medium-sized enterprises. However, the medium and high-voltage segments are experiencing accelerated growth, propelled by large-scale industrial projects, utility grid expansions, and the integration of renewable energy farms. Technology-wise, Metal Oxide Varistors (MOVs) continue to dominate due to their effectiveness and cost-efficiency, while Gas Discharge Tubes (GDTs) and Silicon Avalanche Diodes (SADs) cater to niche applications requiring ultra-fast response or specific voltage characteristics. The application segment sees utilities and industrial sectors as major consumers, but the commercial and telecommunications segments are rapidly expanding, driven by data center proliferation and the rollout of 5G networks. This granular segmentation allows manufacturers to tailor their product offerings and marketing strategies to specific end-user needs, fostering innovation and competitive differentiation within the dynamic commercial surge arrester market.

The integration of Artificial Intelligence (AI) is set to profoundly transform the Commercial Surge Arrester Market by shifting from reactive protection to proactive, intelligent power management. Users are increasingly concerned with how AI can enhance the reliability and efficiency of surge protection, particularly in complex smart grid environments and highly sensitive data centers. Common questions revolve around AI's ability to predict surge events, optimize arrester performance, facilitate predictive maintenance, and enable seamless integration with broader smart infrastructure systems. There is a strong expectation that AI will move surge arresters beyond passive devices to active, data-driven components capable of contributing to overall grid stability and resilience. The key themes include enhanced monitoring, diagnostic capabilities, optimized lifespan, and a reduction in operational expenditures through intelligent management of electrical transients. This shift reflects a broader industry move towards intelligent asset management and condition-based monitoring, where AI plays a pivotal role in transforming traditional electrical components into smart, connected devices.

The Commercial Surge Arrester Market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities, all shaped by various impact forces. A primary driver is the accelerating global demand for uninterrupted and high-quality power supply, fueled by increasing digitalization across all commercial and industrial sectors. The proliferation of sensitive electronic equipment in data centers, telecommunication hubs, smart buildings, and manufacturing facilities makes these entities highly vulnerable to even minor power transients, thereby boosting the necessity for robust surge protection. Furthermore, the rising adoption of renewable energy sources, such as solar and wind, introduces new complexities and transient risks into power grids, necessitating advanced surge arresters for protection at every stage, from generation to distribution. Increasing awareness among businesses about the financial losses and operational disruptions caused by power quality issues also acts as a significant catalyst, compelling investments in preventive protection measures, thereby propelling market growth substantially.

Despite these strong drivers, the market faces certain restraints. High initial investment costs for advanced surge protection systems, particularly for smaller enterprises or in developing economies with budget constraints, can impede widespread adoption. Additionally, a lingering lack of comprehensive awareness regarding the specific benefits and long-term cost savings associated with high-quality surge arresters in some end-user segments can lead to underinvestment. Technical complexities in integrating diverse surge arrester technologies with existing legacy infrastructure can also pose challenges, requiring specialized expertise and potentially adding to installation costs. The absence of stringent, universally standardized regulations in all regions concerning surge protection levels can lead to market fragmentation and a preference for less robust, cheaper alternatives, hindering the adoption of premium solutions and potentially compromising safety standards within certain jurisdictions, impacting overall market potential.

Opportunities for growth are abundant and strategically aligned with global trends. The burgeoning expansion of smart grid initiatives worldwide presents a significant avenue for integrating intelligent surge arresters capable of real-time monitoring and communication, enhancing grid resilience. The rapid build-out of 5G infrastructure, with its dense network of sensitive electronic components, creates substantial demand for sophisticated surge protection in telecommunications. Moreover, the increasing focus on industrial automation and the Internet of Things (IoT) in manufacturing and other industrial settings necessitates advanced protection for interconnected machinery and control systems. Developing economies, undergoing rapid urbanization and industrialization, offer vast untapped market potential as they build out new electrical infrastructure. Impact forces such as technological advancements in material science and digital integration, evolving regulatory frameworks, growing environmental concerns pushing for energy efficiency, and macroeconomic conditions influencing infrastructure spending collectively shape the trajectory and competitive landscape of the commercial surge arrester market, demanding continuous innovation and adaptive strategies from market participants to capitalize on emerging opportunities and mitigate existing restraints.

The Commercial Surge Arrester Market is comprehensively segmented to provide a detailed understanding of its diverse landscape and to enable targeted strategies for market players. These segmentations are critical for analyzing market dynamics, identifying growth opportunities, and understanding the specific needs of various end-user applications and technological preferences. The market can be broadly categorized based on several key attributes, including the voltage level they are designed to protect, the underlying technology utilized, their primary application across different sectors, and their typical deployment environment. Each segment offers distinct growth drivers and challenges, reflecting the varied requirements of commercial and industrial electrical systems. Understanding these distinctions is fundamental for stakeholders looking to optimize product development, distribution channels, and marketing efforts within this specialized and essential market. The detailed breakdown highlights the nuanced demand patterns and technological progressions shaping the industry's future.

The value chain for the Commercial Surge Arrester Market is a complex network of interconnected activities, starting from raw material sourcing and extending through manufacturing, distribution, and ultimate end-user application. Upstream analysis reveals the critical role of suppliers providing specialized materials such as zinc oxide for Metal Oxide Varistors (MOVs), ceramic components for insulating housings, and advanced polymers for external casings. The quality and availability of these raw materials directly impact the performance, durability, and cost-effectiveness of the final surge arrester product. Research and development also represent a significant upstream activity, driving innovation in arrester technology, improving surge handling capabilities, and enhancing product lifespan. Manufacturers often engage in strategic partnerships with material suppliers to ensure a stable supply chain and to collaborate on developing advanced composites and semiconductor materials that can withstand increasingly demanding electrical environments, thereby forming the foundational layer of the value chain.

Midstream activities involve the core manufacturing processes, where raw materials are transformed into finished surge arresters through precision engineering, assembly, and rigorous testing. This stage includes sophisticated processes such as sintering for MOVs, encapsulation, and integration of monitoring electronics for smart arresters. Manufacturers invest heavily in automated production lines and quality control measures to ensure that products meet stringent industry standards and performance specifications. Downstream analysis focuses on the distribution channels and end-user engagement. Distribution channels are varied and typically include direct sales to large utilities and industrial clients, sales through electrical wholesalers and distributors to commercial contractors and smaller businesses, and increasingly, specialized system integrators who incorporate surge arresters into broader electrical protection solutions. The effectiveness of these channels is crucial for market penetration, ensuring products reach diverse customer segments efficiently across different geographical regions.

The direct and indirect distribution channels play a pivotal role in market reach. Direct sales are often preferred for high-value projects or complex industrial applications where technical expertise and customized solutions are required, fostering strong direct relationships between manufacturers and large-scale buyers. Indirect channels, involving a network of wholesalers, retailers, and online platforms, cater to a broader market, including small to medium-sized commercial enterprises and electrical installers. After-sales support, including installation guidance, maintenance services, and warranty provisions, forms an integral part of the value chain, enhancing customer satisfaction and brand loyalty. Understanding and optimizing each stage of this value chain, from upstream material innovation to efficient downstream delivery and support, is crucial for companies operating in the Commercial Surge Arrester Market to maintain competitive advantage, ensure product quality, and effectively meet evolving customer demands in a rapidly electrifying world.

The Commercial Surge Arrester Market serves a diverse array of potential customers, all united by their critical need to protect electrical infrastructure and sensitive equipment from transient overvoltages. The primary end-users or buyers of these products include large-scale utility companies responsible for power generation, transmission, and distribution. These entities require high-voltage and medium-voltage surge arresters to safeguard substations, transmission lines, and essential grid components, ensuring grid stability and reliable electricity supply to millions. Industrial sectors, encompassing manufacturing plants, oil and gas facilities, mining operations, and heavy industries, represent another significant customer base. Their reliance on complex machinery, automation systems, and continuous production processes makes them highly vulnerable to power disturbances, leading to substantial demand for robust surge protection at various points within their electrical networks, from main incoming feeds to individual machine protection.

Beyond traditional industrial applications, the rapidly expanding data center and telecommunications sectors are becoming increasingly pivotal customers. Data centers, which house mission-critical IT infrastructure and process vast amounts of data, cannot afford any downtime caused by power surges; hence, they invest heavily in multi-stage surge protection systems to protect servers, networking equipment, and power distribution units. Similarly, telecommunication companies, particularly with the global rollout of 5G networks, require extensive surge protection for their base stations, transmission equipment, and network infrastructure to maintain uninterrupted connectivity and service quality. Any disruption in these sectors can lead to massive financial losses, data corruption, and significant reputational damage, making surge arresters an indispensable investment for business continuity and operational resilience, underscoring their importance in modern digital economies.

Furthermore, the commercial real estate sector, including large office buildings, retail complexes, healthcare facilities, educational institutions, and smart city projects, constitutes a growing segment of potential customers. These establishments rely on sophisticated building management systems, IT networks, medical equipment, and consumer electronics, all of which are susceptible to power surges. Healthcare facilities, in particular, require uncompromising power quality to ensure the safe operation of life-support systems and diagnostic equipment. The increasing adoption of Building Management Systems (BMS) and smart technologies within commercial infrastructure further elevates the need for comprehensive surge protection at service entrances, distribution panels, and critical load points. Moreover, renewable energy developers and operators, especially those managing solar farms and wind power plants, are vital customers, requiring specialized surge arresters to protect inverters, turbines, and control systems from both direct lightning strikes and switching transients, ensuring the longevity and efficiency of their green energy investments. This broad spectrum of end-users highlights the pervasive and essential role of commercial surge arresters across the economic landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2032 | USD 1.98 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, Eaton Corporation plc, Schneider Electric SE, Legrand S.A., Raycap S.A., DEHN + SÖHNE GmbH & Co. KG, Phoenix Contact GmbH & Co. KG, Mersen Corporate Services SAS, Littlefuse Inc., Hubbell Incorporated, Emerson Electric Co., Rockwell Automation Inc., Delta Electronics Inc., CG Power and Industrial Solutions Limited, Prolec GE, TE Connectivity Ltd., Bourns Inc., Advanced Protection Technologies, EATON (Cooper Bussmann) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Commercial Surge Arrester Market is characterized by a dynamic and evolving technology landscape, continuously driven by the need for enhanced protection, higher reliability, and integration with modern electrical systems. At the core of surge arrester technology are Metal Oxide Varistors (MOVs), which leverage the non-linear voltage-current characteristics of zinc oxide materials to divert surge currents effectively. Recent advancements in MOV technology focus on improving energy absorption capabilities, reducing clamping voltages for better protection of sensitive electronics, and increasing the operational lifespan under repeated surge events. Manufacturers are developing MOVs with superior thermal performance and enhanced resistance to degradation, making them more suitable for diverse and demanding commercial and industrial applications where consistent performance over time is crucial. The continuous refinement of MOV formulations and fabrication processes remains a significant area of research and development, aiming to provide more compact yet powerful protection devices for critical infrastructure.

Beyond MOVs, other foundational technologies include Gas Discharge Tubes (GDTs) and Silicon Avalanche Diodes (SADs). GDTs, known for their high current handling capability and robust construction, are widely used as a primary protection stage, especially in outdoor environments or applications requiring discharge of very high surge currents. Innovations in GDT technology involve miniaturization, faster response times, and improved reliability across a wider temperature range. SADs, on the other hand, offer extremely fast response times and precise clamping voltages, making them ideal for protecting sensitive data lines and electronic circuits within commercial and IT environments. The development of hybrid arresters, which combine the strengths of MOVs, GDTs, and SADs, represents a significant technological trend. These hybrid solutions provide multi-stage protection, offering comprehensive defense against a broad spectrum of transient overvoltages, from rapid low-energy events to high-energy lightning strikes, thereby providing a more versatile and robust solution for complex commercial installations.

The emerging technological frontier in the commercial surge arrester market includes the integration of smart capabilities and advanced monitoring systems. This involves embedding microcontrollers and communication modules into surge arresters, allowing them to provide real-time status updates, log surge events, and communicate with building management systems or smart grid infrastructure. Such "smart arresters" facilitate predictive maintenance, remote diagnostics, and condition-based monitoring, moving beyond passive protection to active participation in power quality management. Furthermore, advancements in materials science are exploring novel compounds and nano-materials to create more efficient and durable arrester components. The drive towards miniaturization, higher energy density, and enhanced environmental resilience is pushing innovation, ensuring that commercial surge arresters continue to evolve as indispensable assets for safeguarding electrical systems in an increasingly interconnected and electrified world. These technological shifts are pivotal in meeting the escalating demands for reliable and secure power in commercial and industrial settings, ensuring continuity and operational safety.

A commercial surge arrester is an electrical device designed to protect equipment and systems in commercial or industrial settings from transient overvoltages, often caused by lightning, utility switching, or electrical faults. It diverts excess voltage to the ground, preventing damage, downtime, and ensuring operational continuity for sensitive electronics and critical infrastructure.

AI is transforming surge protection by enabling predictive maintenance, optimizing arrester performance, and facilitating smart grid integration. It allows for real-time monitoring, diagnostic insights, and potentially adaptive protection, moving from reactive defense to proactive, intelligent power quality management, thereby enhancing reliability and reducing operational costs.

The main types include Low Voltage, Medium Voltage, and High Voltage surge arresters, categorized by their voltage protection levels. Key technologies deployed within these types are Metal Oxide Varistors (MOVs), Gas Discharge Tubes (GDTs), and Silicon Avalanche Diodes (SADs), often combined in hybrid solutions for comprehensive protection.

Primary end-users include utility companies for grid protection, industrial sectors (manufacturing, oil & gas) for machinery protection, data centers and telecommunications for sensitive IT infrastructure, and commercial real estate (offices, hospitals, retail) for building management systems and critical equipment. Renewable energy facilities also represent a significant customer segment.

Key drivers include rapid digitalization and the proliferation of sensitive electronics, increasing demand for power quality and grid modernization, growing adoption of renewable energy sources, and heightened awareness of potential financial losses from power disruptions. Stringent safety regulations and infrastructure development in emerging economies also contribute significantly to market expansion.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.