ID : MRU_ 428360 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

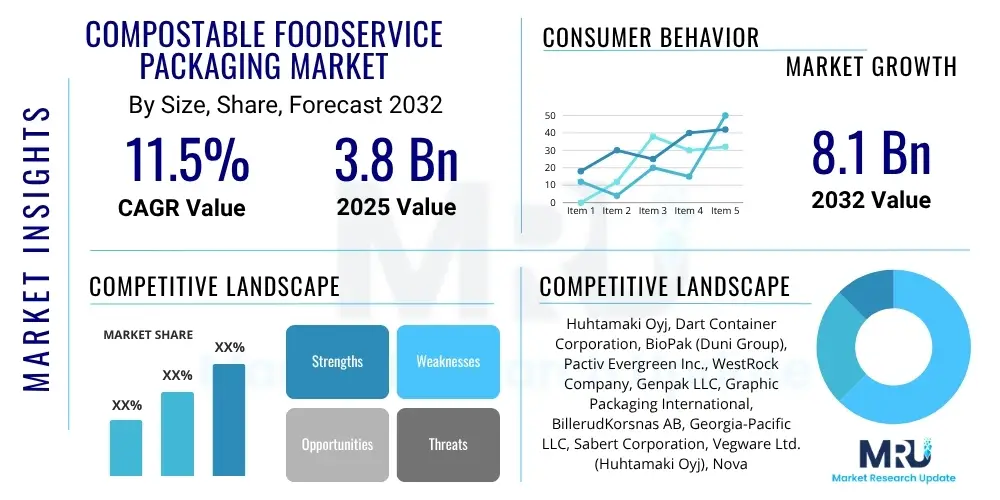

The Compostable Foodservice Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2032. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 8.1 Billion by the end of the forecast period in 2032.

The Compostable Foodservice Packaging Market encompasses a range of disposable products designed to break down into natural elements in a composting environment, significantly reducing landfill waste and environmental pollution. These products serve as an eco-friendly alternative to conventional single-use plastics, addressing mounting global concerns over plastic waste accumulation and its ecological impact. The primary goal of these offerings is to provide functional packaging solutions that align with sustainability principles, supporting a circular economy model where waste is minimized and resources are regenerated.

Products within this market segment are typically manufactured from renewable resources such as plant-based bioplastics like Polylactic Acid (PLA) and Crystallized Polylactic Acid (CPLA), sugarcane bagasse, molded fiber, and paper or paperboard with compostable linings. They are widely utilized across various foodservice operations, including quick-service restaurants, cafes, catering services, corporate canteens, and large-scale events. The adoption of compostable packaging is primarily driven by its tangible environmental benefits, such as biodegradability and reduction in carbon footprint, alongside increasing regulatory pressures and a growing consumer preference for sustainable practices.

The increasing global emphasis on environmental protection, coupled with evolving consumer consciousness regarding the ecological footprint of their consumption choices, acts as a significant catalyst for this market's expansion. Businesses are increasingly integrating compostable solutions into their operations not only to comply with legislative mandates but also to enhance their brand image and meet the ethical demands of their customer base. This convergence of factors underscores the strategic importance and rapid growth trajectory of the compostable foodservice packaging sector.

The Compostable Foodservice Packaging Market is experiencing robust growth, fueled by several overarching business trends. Companies are increasingly prioritizing sustainability initiatives, driven by consumer demand for eco-friendly products and the desire to enhance corporate social responsibility. This shift is leading to significant investments in research and development for new materials and improved production processes, aimed at making compostable options more cost-effective and functionally competitive with traditional plastics. Strategic partnerships across the value chain, from raw material suppliers to foodservice operators, are becoming more common to establish efficient supply chains and robust composting infrastructure.

Regional trends play a crucial role in shaping market dynamics. North America and Europe are at the forefront of adoption, propelled by stringent government regulations, widespread public awareness, and established composting facilities. Countries in these regions are actively implementing bans on single-use plastics, thereby creating a strong impetus for the transition to compostable alternatives. In contrast, the Asia Pacific region is emerging as a high-growth market, driven by rapid urbanization, increasing disposable incomes, and a nascent but growing environmental consciousness among consumers and policymakers, particularly in populous countries like China and India where waste management is a critical concern.

Segment-wise, the market is observing strong demand across various product categories. Compostable cups, plates, bowls, and cutlery are among the most sought-after products, reflecting their pervasive use in daily foodservice operations. There is a discernible trend towards innovation in these segments, with manufacturers focusing on improving barrier properties, heat resistance, and overall durability to match or exceed the performance of conventional plastics. The expansion of these product lines, coupled with ongoing advancements in material science, is expected to sustain the market's upward trajectory throughout the forecast period, addressing the diverse needs of the global foodservice industry.

User questions related to the impact of AI on the Compostable Foodservice Packaging Market frequently revolve around how artificial intelligence can optimize the entire lifecycle of these products. Common inquiries explore AI's role in improving the efficiency of sustainable material sourcing, enhancing the design and manufacturing processes for biodegradability, and streamlining the complex logistics of composting infrastructure. Users also express interest in AI's potential for predictive analytics to forecast demand for compostable solutions and its ability to ensure stringent quality control and compliance with evolving environmental standards. The key themes underscore a desire to understand how AI can drive greater sustainability, cost-effectiveness, and operational excellence within this eco-conscious industry.

The Compostable Foodservice Packaging Market is profoundly influenced by a complex interplay of drivers, restraints, and opportunities, all shaped by significant impact forces. A primary driver is the escalating global concern over environmental pollution and climate change, which has galvanized consumers, businesses, and governments to seek sustainable alternatives to conventional plastics. This environmental imperative is further bolstered by increasingly stringent regulatory frameworks worldwide, including outright bans on single-use plastics and mandates for compostable or recyclable packaging, compelling the foodservice industry to adapt rapidly. Consumer preference for eco-friendly products also exerts substantial market pull, with brands leveraging sustainable packaging as a competitive differentiator and a means to enhance corporate social responsibility.

Despite these powerful drivers, the market faces notable restraints. The relatively higher production cost of compostable materials compared to fossil-fuel-based plastics presents a significant barrier, particularly for small and medium-sized enterprises. Furthermore, the limited availability and uneven distribution of industrial composting infrastructure globally hinder the proper disposal and actualization of the compostable promise, leading to confusion and improper waste management practices. Performance limitations, such as reduced shelf life for certain food items or lower heat resistance compared to some plastic counterparts, also pose challenges that manufacturers are continuously working to overcome through material innovation.

Opportunities for growth are abundant within this evolving landscape. Advances in material science are continuously yielding new biopolymers and plant-based composites with improved performance characteristics and reduced costs, expanding the applicability of compostable packaging across a wider range of foodservice scenarios. The development of more robust and widely accessible composting facilities, potentially supported by government incentives and private investments, will unlock the full potential of these products. Moreover, emerging economies in Asia Pacific and Latin America present vast untapped markets where increasing environmental awareness and economic growth are creating fertile ground for sustainable packaging solutions, alongside the potential for developing closed-loop systems that integrate packaging production with composting and agricultural use.

The Compostable Foodservice Packaging Market is comprehensively segmented to provide a detailed understanding of its diverse components, allowing for targeted analysis and strategic planning. These segmentations are critical for identifying specific market niches, understanding product adoption patterns, and tracking growth across different material types, product formats, applications, and end-user categories. The detailed breakdown highlights the breadth of solutions available and the varied demands from the global foodservice industry, ranging from quick-service restaurants to institutional catering and specialized events, all striving for more sustainable operational practices.

The value chain for the Compostable Foodservice Packaging Market begins with the upstream sourcing of renewable raw materials. This segment involves agricultural suppliers providing feedstock such as corn starch, sugarcane, wood pulp, and other plant fibers, which are then processed by specialized chemical companies into biopolymers like PLA or directly by pulp and paper mills into molded fiber. Key players in this initial stage focus on sustainable cultivation practices and efficient conversion technologies to ensure a consistent and environmentally responsible supply of base materials, forming the fundamental building blocks of compostable packaging products. The quality and sustainability certifications of these raw materials are critical at this juncture.

The midstream of the value chain involves the manufacturing and conversion processes. Here, biopolymer resins and pulp are transformed into finished compostable foodservice packaging items through various techniques such as extrusion, thermoforming, injection molding, and pulp molding. This stage demands significant technological expertise and investment in specialized machinery capable of handling these distinct materials. Converters focus on designing products that meet specific functional requirements, such as heat resistance, moisture barrier properties, and structural integrity, while adhering to compostability standards and certifications. Innovations in this segment often lead to enhanced product performance and cost-effectiveness.

The downstream segment encompasses the distribution and end-use of compostable packaging. Products reach end-users, including quick-service restaurants, cafes, catering companies, and institutional foodservice providers, through a combination of direct sales, wholesalers, and specialized foodservice distributors. Direct channels are often preferred by large restaurant chains seeking custom solutions or bulk orders, while distributors serve a broader base of smaller businesses and independent operators. The effectiveness of the distribution network is crucial for market penetration, ensuring that these sustainable packaging solutions are readily available where demand exists. Post-consumer, the value chain extends to waste collection and industrial composting facilities, closing the loop on the product's lifecycle and returning nutrients to the soil.

The Compostable Foodservice Packaging Market caters to a diverse and expanding base of potential customers, primarily comprising entities within the food and beverage industry that utilize single-use packaging for serving meals and drinks. These end-users are driven by a combination of factors, including regulatory compliance, corporate sustainability goals, and evolving consumer preferences for environmentally responsible practices. The breadth of potential customers spans from global enterprises with extensive supply chains to local businesses deeply integrated into community values, all seeking to reduce their environmental impact and enhance their public image through sustainable packaging choices.

Key segments of end-users include quick-service restaurants (QSRs) and full-service restaurants, which generate substantial volumes of disposable packaging for dine-in, takeout, and delivery services. Cafes and coffee shops represent another significant customer group, heavily relying on disposable cups, lids, and stirrers. Additionally, catering services, hotels, and event organizers regularly require a wide array of plates, bowls, cutlery, and containers for their operations, making them crucial consumers of compostable solutions. The demand from these commercial entities is often driven by operational efficiency, brand reputation management, and the need to align with increasingly green consumer expectations.

Beyond the commercial sector, institutional foodservice providers such as schools, universities, hospitals, and corporate canteens also represent a substantial segment of potential customers. These institutions frequently serve meals to a large and consistent population, and their adoption of compostable packaging is often influenced by public sector mandates, internal sustainability policies, and a commitment to fostering healthier and more environmentally conscious environments. As awareness of plastic pollution grows and regulations become more pervasive, the pool of potential customers is expected to expand further, encompassing nearly all entities involved in the preparation and serving of food outside the home.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2032 | USD 8.1 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Huhtamaki Oyj, Dart Container Corporation, BioPak (Duni Group), Pactiv Evergreen Inc., WestRock Company, Genpak LLC, Graphic Packaging International, BillerudKorsnas AB, Georgia-Pacific LLC, Sabert Corporation, Vegware Ltd. (Huhtamaki Oyj), Novamont S.p.A., Natur-Tec (Northern Technologies International Corp.), Avantium N.V., TotalEnergies Corbion, International Paper Company, Stora Enso Oyj, Eco-Products Inc. (subsidiary of Novolex), Dixie (Georgia-Pacific LLC), CKF Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Compostable Foodservice Packaging Market is continuously evolving due to significant advancements in its underlying technology landscape. A critical area of innovation lies in the development of novel biopolymers and bio-based materials that offer improved performance characteristics, such as enhanced heat resistance, moisture barrier properties, and durability, closely mimicking traditional plastics while ensuring complete compostability. Technologies like advanced polymerization techniques for PLA and CPLA, along with the formulation of new blends using starch, cellulose, and lignin, are central to expanding the functional capabilities and applications of these sustainable alternatives. Researchers are also focused on reducing the cost of these materials to enhance their market competitiveness.

Furthermore, manufacturing processes for converting these raw materials into finished packaging products have seen considerable technological evolution. Techniques such as advanced extrusion, thermoforming, and injection molding are being refined to optimize material usage, reduce energy consumption, and increase production efficiency for bioplastics. The molded fiber technology, particularly from sugarcane bagasse and other agricultural byproducts, is experiencing a renaissance with advancements in precision molding and surface finishing, allowing for the creation of more intricate and aesthetically pleasing designs. These manufacturing innovations are crucial for scaling production to meet growing market demand without compromising on quality or compostability.

Beyond material and production, the technology landscape also encompasses sophisticated coating and additive solutions designed to improve the functional properties of paper and molded fiber products without impeding their compostability. These include bio-based waxes, biodegradable barrier coatings, and natural fiber reinforcements that extend the shelf life of packaged food items and protect against grease and moisture. Concurrently, the development of robust certification and testing methodologies, utilizing advanced analytical techniques to verify compostability according to international standards (e.g., ASTM D6400, EN 13432), is essential for building consumer trust and ensuring the environmental integrity of compostable foodservice packaging. The continuous integration of these technological advancements drives market growth and facilitates the broader adoption of sustainable packaging solutions.

The main materials include plant-based bioplastics such as Polylactic Acid (PLA) and Crystallized Polylactic Acid (CPLA), along with natural fibers like sugarcane bagasse, molded wood pulp, and paper or paperboard often combined with compostable barrier coatings.

Key challenges include the relatively higher production cost compared to conventional plastics, the limited and often inadequate global composting infrastructure, potential performance limitations (e.g., heat or moisture resistance), and the lack of universally standardized certification and labeling for compostability.

Compostable products are specifically designed to break down completely into non-toxic components in a controlled composting environment within a defined timeframe, enriching the soil. Biodegradable products simply break down naturally, but often without specific time limits or requirements for nutrient return, and may not fully decompose in all environments.

Government regulations, including bans on single-use plastics and mandates for sustainable packaging, are significant drivers for the compostable foodservice packaging market. These policies compel businesses to adopt eco-friendly alternatives, accelerating innovation and market expansion while promoting environmental protection.

The market is projected for substantial growth, fueled by increasing global environmental awareness, continuous technological advancements in material science, and an expanding landscape of supportive regulatory frameworks. This upward trend indicates a sustained shift towards more sustainable and circular foodservice operations worldwide.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.