ID : MRU_ 430152 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

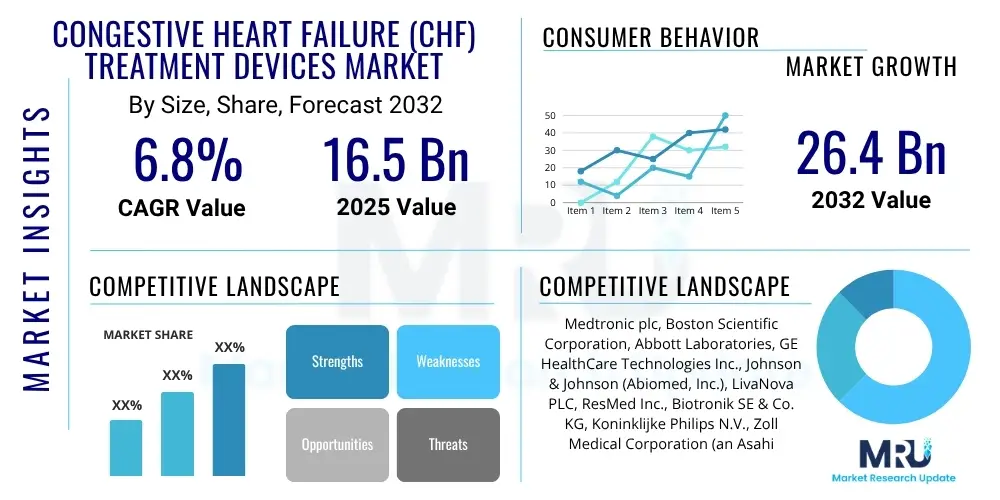

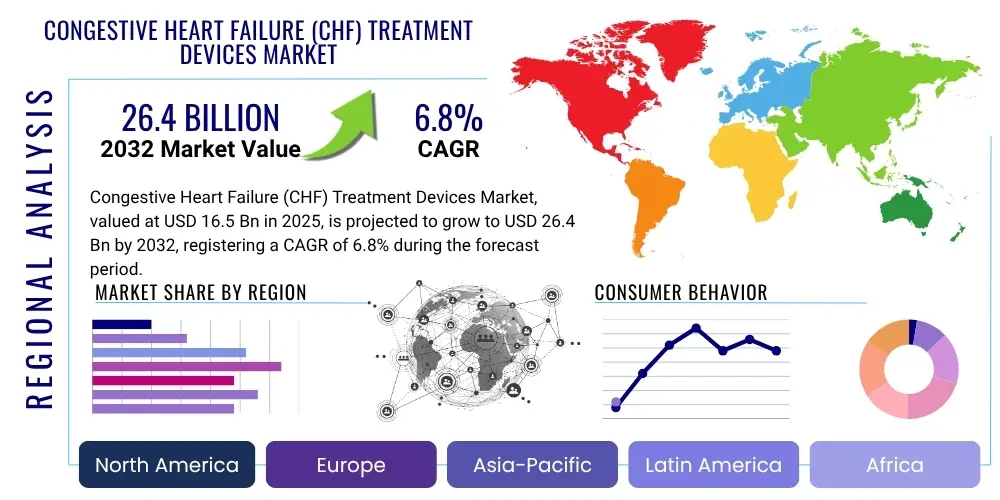

The Congestive Heart Failure (CHF) Treatment Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at $16.5 billion in 2025 and is projected to reach $26.4 billion by the end of the forecast period in 2032.

The Congestive Heart Failure (CHF) Treatment Devices Market represents a highly specialized and rapidly evolving segment within the broader medical devices industry, entirely dedicated to the development, manufacturing, and commercialization of advanced technological solutions for the precise diagnosis, continuous monitoring, and effective therapeutic management of patients afflicted with chronic heart failure. Congestive heart failure itself is a complex and progressively debilitating clinical syndrome characterized by the heart's fundamental inability to pump a sufficient volume of blood to meet the metabolic requirements of the body's tissues and organs. This physiological impairment invariably leads to a cascade of distressing symptoms such as severe dyspnea, profound fatigue, peripheral edema, and widespread fluid retention, significantly reducing functional capacity and overall quality of life. The advent and continuous evolution of these sophisticated medical devices have profoundly revolutionized the prognosis for CHF patients, offering critical interventions that not only extend survival but also substantially alleviate symptoms, significantly enhance patient quality of life, and ultimately aim to restore or augment compromised cardiac function and stabilize electrical rhythms for this vulnerable population.

The extensive product portfolio within this market is remarkably diverse, featuring several distinct categories of high-technology solutions tailored to different clinical needs and disease stages. These prominently include implantable cardioverter-defibrillators (ICDs), which are meticulously engineered to detect and automatically correct life-threatening ventricular tachyarrhythmias, thereby serving as a vital preventative measure against sudden cardiac death in at-risk individuals. Cardiac resynchronization therapy (CRT) devices, comprising both CRT-defibrillators (CRT-D) and CRT-pacemakers (CRT-P), are specifically designed to synchronize the contractions of the heart's ventricles. This synchronization improves the heart's overall pumping efficiency and significantly alleviates symptoms in specific CHF patient cohorts exhibiting electrical dyssynchrony. Furthermore, ventricular assist devices (VADs), which include left ventricular assist devices (LVADs), right ventricular assist devices (RVADs), and biventricular assist devices (BiVADs), offer indispensable mechanical circulatory support for patients with advanced, end-stage heart failure, serving either as a bridge to heart transplantation or as a long-term destination therapy when transplantation is not an option. Beyond these implantable therapeutic devices, the market also incorporates advanced remote patient monitoring systems, which leverage sophisticated telemetry and sensor technologies to provide continuous, non-invasive surveillance of crucial physiological parameters, enabling early detection of clinical deterioration and facilitating proactive, data-driven clinical management, even from the comfort and convenience of a patient's home environment.

The major applications of these cutting-edge medical devices span a broad and critical clinical spectrum within cardiology. They are critically employed in the primary prevention of sudden cardiac death in individuals identified as being at high risk due to severe left ventricular dysfunction, and for crucial secondary prevention in those who have already experienced life-threatening arrhythmias. CRT devices find their primary application in improving ventricular synchronization and thereby alleviating symptoms in patients with moderate to severe CHF who meet specific criteria, significantly enhancing their functional status and exercise tolerance. VADs, on the other hand, are applied in more advanced stages of heart failure, providing life-sustaining circulatory support for patients whose condition is refractory to conventional medical therapy. The profound and clinically significant benefits derived from the widespread adoption of these sophisticated technologies are multifaceted. They include statistically robust improvements in patient survival rates, a marked reduction in costly and debilitating hospital readmissions attributable to acute heart failure exacerbations, superior and more consistent management of chronic and acute symptoms such as severe dyspnea and debilitating fatigue, and a considerable enhancement in the patient's overall functional capacity and their ability to participate meaningfully in daily activities. This holistic improvement in patient outcomes and quality of life firmly establishes the indispensable and growing role of CHF treatment devices in contemporary cardiac care, highlighting their transformative impact on patient prognosis and well-being.

The market's sustained and robust expansion is fundamentally propelled by a powerful convergence of global demographic shifts, escalating epidemiological trends, and relentless technological innovation. A primary driving factor is the escalating global prevalence of congestive heart failure, which is intrinsically linked to the rapidly expanding global geriatric population. As individuals age, their susceptibility to various cardiovascular diseases, including CHF, significantly increases, creating an ever-larger patient pool requiring advanced interventions. Concomitantly, the rising incidence of prevalent chronic conditions such as hypertension, type 2 diabetes mellitus, obesity, and coronary artery disease, which are well-established and modifiable risk factors for heart failure, further contributes substantially to the growing number of individuals needing sophisticated cardiac device therapies. Moreover, the continuous evolution and maturation of medical device technology, encompassing breakthroughs in device miniaturization, extended battery life, enhanced biocompatibility of materials, and the sophisticated integration of artificial intelligence and machine learning algorithms, are consistently bringing forth more effective, safer, and less invasive treatment solutions. These innovations expand the eligible patient population, improve clinical outcomes, and thereby significantly stimulate market demand. Additionally, increasing awareness among both healthcare professionals and the general public regarding the profound advantages of early diagnosis, proactive intervention with device therapy, and continuous patient monitoring, substantially fuels market growth. Furthermore, the presence of supportive and favorable reimbursement policies in developed economies, particularly in North America and Western Europe, acts as a crucial financial catalyst, facilitating broader patient access to these often high-cost yet life-saving therapeutic devices, making them more affordable and accessible to those in dire need.

The Congestive Heart Failure (CHF) Treatment Devices Market is currently experiencing a period of dynamic and robust growth, underpinned by a continuously expanding global patient demographic and an unwavering commitment to pioneering technological innovation across the industry. Business trends within this sector are indicative of a strategic imperative towards consolidation, collaboration, and diversification, frequently manifesting through an observable increase in mergers, acquisitions, and strategic partnerships among key market players. These corporate strategies are designed to strengthen individual market presence, broaden existing product portfolios, and enhance competitive advantages through synergistic capabilities that leverage complementary expertise and resources. Parallel to this, there is a substantial and ongoing commitment to research and development (R&D) activities, with significant investments channeled into the creation of next-generation devices. These innovations typically boast enhanced functionalities, such as advanced miniaturization for improved patient comfort and reduced invasiveness, extended battery longevity to minimize re-interventions, and sophisticated connectivity features for seamless data transmission and comprehensive remote monitoring. A notable and impactful shift towards personalized medicine is also distinctly evident across the industry, where companies are increasingly focusing on tailoring device therapies and programming to the unique physiological profiles, genetic predispositions, and clinical needs of individual CHF patients. This patient-centric approach fosters greater differentiation within the market, allows for more effective treatment outcomes by optimizing therapeutic delivery, and ultimately carves out sustainable competitive advantages for companies that successfully implement such bespoke solutions.

From a comprehensive geographical perspective, the current market landscape for CHF treatment devices is predominantly influenced by and centered within North America and Europe. These regions maintain their dominant positions due to the convergence of several critical factors: highly developed and sophisticated healthcare infrastructures capable of supporting advanced medical procedures, a high degree of both public and professional awareness regarding advanced cardiac care options, and robust, well-established reimbursement policies that effectively facilitate widespread patient access to often expensive, yet critically advanced, treatment technologies. The United States, in particular, stands out as a pivotal and leading market within this segment, driven by its substantial healthcare expenditure, a large and aging population grappling with CHF, and an innovation-driven medical device ecosystem that consistently pushes the boundaries of medical technology. However, looking ahead to the forecast period, the Asia Pacific region is rapidly ascending as a high-growth epicenter, projected to register the most substantial Compound Annual Growth Rate (CAGR). This accelerated growth is fundamentally attributable to a confluence of factors including improving healthcare access across its vast and diverse population, rapidly burgeoning disposable incomes that permit greater investment in advanced medical care, and a substantial, expanding geriatric demographic that is increasingly susceptible to chronic cardiovascular diseases. Similarly, other emerging markets such as Latin America and the Middle East and Africa are progressively gaining significant traction, propelled by increasing governmental healthcare expenditures directed towards modernizing medical facilities and a rising patient demand for state-of-the-art cardiac care solutions that were previously unavailable or unaffordable.

A granular analysis of market segmentation further illuminates distinct and evolving trends across various device categories and end-user segments. Implantable cardioverter-defibrillators (ICDs) and cardiac resynchronization therapy (CRT) devices continue to collectively command a substantial share of the market, a testament to their long-standing clinical efficacy, proven safety profiles, and established guideline recommendations in managing life-threatening arrhythmias and optimizing ventricular function, respectively. These devices remain foundational elements of CHF management. The segment dedicated to ventricular assist devices (VADs) is currently demonstrating an impressive acceleration in growth, particularly spurred by their increasing adoption in both bridge-to-transplant applications for patients awaiting heart donors and as destination therapy for those ineligible for transplantation. This surge reflects significant advancements in device reliability, durability, and a continuous improvement in patient outcomes, making VADs a more viable long-term solution. Concurrently, remote monitoring systems represent another high-growth segment, gaining immense traction due to the broader global paradigm shift towards value-based care models, preventative health strategies, and the imperative for continuous, proactive patient management that extends beyond the traditional confines of acute clinical settings. These systems enable timely interventions, reduce the frequency of costly hospital readmissions, and empower patients with greater self-management capabilities through continuous data feedback, thereby contributing significantly to reducing overall healthcare burdens and enhancing long-term patient well-being.

Common user inquiries concerning the profound and multifaceted impact of Artificial Intelligence (AI) on the Congestive Heart Failure (CHF) Treatment Devices Market frequently center around AI's transformative potential across the entire continuum of patient care, from early diagnosis to long-term management and device optimization. Users are keenly interested in understanding precisely how AI can significantly enhance the precision and timeliness of CHF diagnosis, leveraging vast datasets to identify subtle disease markers. There is also significant interest in how AI enables the development of highly personalized and adaptive treatment regimens tailored to individual patient needs, moving beyond one-size-fits-all approaches. Furthermore, users inquire about AI's role in optimizing the complex operational parameters of implantable cardiac devices for maximum efficacy and its ability to substantially bolster the efficiency and accuracy of predictive analytics for anticipating disease progression or impending cardiac complications before they become critical. There is a strong, pervasive expectation among stakeholders that the strategic integration of AI will herald an era of more proactive and preventative interventions, leading directly to a substantial reduction in costly and debilitating hospital readmissions for CHF exacerbations. Moreover, a shared anticipation exists that AI will contribute significantly to the extended longevity and reliability of medical devices through predictive maintenance algorithms that can flag potential issues before failure, and ultimately, will profoundly elevate overall patient outcomes by facilitating more precise, dynamically adaptive, and truly patient-centric care strategies for individuals living with the challenging condition of congestive heart failure. The convergence of AI with medical device technology is perceived as a pivotal advancement towards smarter, more efficient, and demonstrably more effective cardiac device management solutions, promising a revolution in personalized and preventative cardiology.

The Congestive Heart Failure (CHF) Treatment Devices Market is intricately shaped by a complex interplay of inherent drivers, formidable restraints, and promising opportunities, all operating under the pervasive influence of various industry impact forces that dictate its current trajectory and future potential. The primary catalysts propelling market expansion are deeply rooted in profound global demographic shifts and escalating epidemiological trends. Foremost among these is the inexorable increase in the geriatric population worldwide, a demographic segment inherently more susceptible to the onset and progressive worsening of CHF due to age-related cardiac degeneration and cumulative comorbidities. This demographic shift creates a continuously expanding patient pool requiring advanced and sustained interventions to manage their cardiac health effectively. Concomitantly, the rising global prevalence of chronic comorbidities such as hypertension, type 2 diabetes mellitus, obesity, and coronary artery disease—all well-established and modifiable risk factors for developing heart failure—further contributes significantly to the growing number of individuals needing sophisticated cardiac device therapies. Complementing these demographic and epidemiological factors are the relentless and rapid advancements in medical device technology. These include breakthroughs in component miniaturization, extended battery life for implantable devices, enhanced biocompatibility of materials, and the sophisticated integration of artificial intelligence and machine learning algorithms. Such innovations consistently bring forth more effective, safer, and less invasive treatment solutions, thereby expanding the eligible patient population, improving clinical outcomes, and significantly stimulating market demand. Furthermore, the presence of supportive and evolving reimbursement policies in economically developed regions, particularly in North America and Western Europe, acts as a crucial financial catalyst, facilitating broader patient access to these often high-cost yet life-saving therapeutic devices by making them more financially attainable and accessible for individuals who desperately need them, often covering a significant portion of their cost.

Conversely, the market's otherwise robust growth trajectory is significantly tempered by several formidable restraining factors that pose ongoing challenges for manufacturers, healthcare providers, and patients alike. A paramount hurdle is the inherently high cost associated with CHF treatment devices. This encompasses not only the substantial initial acquisition cost of the device itself but also the significant expenses related to the complex surgical implantation procedures, subsequent post-operative care, long-term monitoring requirements, and the potential for future device replacements or upgrades. This considerable financial burden can present a formidable barrier to patient access, particularly within underserved healthcare systems in developing economies or for patient populations lacking comprehensive insurance coverage, often forcing difficult choices regarding treatment. Adding to these economic hurdles are the increasingly stringent and protracted regulatory approval processes mandated by governing bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). These rigorous requirements necessitate extensive pre-clinical testing, prolonged and costly multi-phase clinical trials, meticulous validation periods, and exhaustive documentation, often leading to substantial delays in product commercialization and significantly inflated research and development costs for device manufacturers. Moreover, a persistent global shortage of highly specialized medical professionals, including skilled cardiologists, electrophysiologists, and cardiac surgeons adept at implanting, programming, and managing these intricate devices, particularly in rural or medically underserved geographical areas, severely limits broader market penetration and optimal patient care delivery. Occasional product recalls, often triggered by unforeseen technical malfunctions, software glitches, or emergent safety concerns, further erode patient and physician confidence in the reliability and safety of these devices, leading to temporary market slowdowns, potential litigation risks, and significant reputational damage for affected companies, thereby directly impacting overall market growth and adoption rates over time.

Despite these considerable challenges, the CHF treatment devices market is replete with substantial opportunities for future growth, innovation, and expansion into untapped segments. Untapped emerging markets, particularly within the rapidly developing regions of Asia Pacific and Latin America, represent highly fertile ground for future market expansion. This is driven by their rapidly improving healthcare infrastructures, burgeoning middle-class populations with increasing disposable incomes, and a steadily growing public awareness regarding advanced cardiac care solutions. The escalating global emphasis on telehealth and remote patient monitoring, a trend dramatically accelerated by recent public health crises such as the COVID-19 pandemic, presents a monumental and enduring avenue for market growth. This paradigm shift promotes continuous, proactive patient management outside traditional clinical settings, facilitating earlier clinical interventions, enhancing patient convenience, and significantly reducing the burden of frequent in-person hospital visits and associated healthcare costs. Furthermore, ongoing research and development efforts are diligently focused on pioneering less invasive device implantation procedures, seamlessly integrating advanced artificial intelligence and machine learning for predictive analytics and highly personalized therapeutic adjustments, and exploring novel combination therapies. These innovations collectively aim to enhance patient comfort, improve long-term clinical outcomes, and broaden the applicability of CHF treatment devices to a wider patient population. The impact forces profoundly shaping the competitive dynamics of this market include the substantial bargaining power of buyers, primarily large hospital systems and Group Purchasing Organizations (GPOs), who consistently seek cost-effective yet high-quality solutions while negotiating for bulk discounts. The bargaining power of specialized suppliers remains relatively high due to the proprietary nature and technological complexity of critical components, often supplied by a limited number of vendors. The threat of substitutes is generally low, given that these devices often represent life-critical interventions with few comparable or equally effective alternatives that can provide similar physiological benefits. The threat of new entrants is moderate, as the market is characterized by exceptionally high research and development costs, stringent regulatory hurdles, and strong brand loyalty among established players, creating significant barriers to entry. Lastly, intense competitive rivalry among a cadre of well-established global players drives continuous innovation, product differentiation, and strategic alliances to maintain and expand market leadership, pushing the boundaries of what is possible in cardiac care.

The Congestive Heart Failure (CHF) Treatment Devices Market undergoes an extensive and meticulous segmentation process to furnish a profoundly granular and comprehensive understanding of its multifaceted components, intricate internal dynamics, and prevailing industry trends. This detailed segmentation serves as an indispensable analytical framework, empowering stakeholders to precisely analyze current market trends, accurately identify nascent growth opportunities across diverse product categories, delineate specific end-user applications, and pinpoint evolving technological platforms that are shaping the future of cardiac care. The primary level of segmentation typically distinguishes between various classifications of device types, thereby encapsulating the broad spectrum of therapeutic and monitoring solutions that are currently available for CHF patients. Each device category is meticulously engineered and clinically validated to address distinct pathophysiological aspects of the complex heart failure syndrome, reflecting the varied clinical needs and disease stages encountered in the patient population. This detailed categorization ensures that market analysis is both thorough and relevant to specific product development and commercialization strategies, allowing companies to focus their efforts where they can achieve maximum impact and meet critical clinical demands effectively.

Further analytical granularity is strategically achieved through additional segmentation based on the specific end-user facilities where these advanced medical devices are predominantly utilized and where patients receive critical, ongoing cardiac care. This nuanced categorization is instrumental in discerning specific demand patterns originating from large, tertiary hospital networks with advanced cardiology and cardiothoracic surgery departments, specialized outpatient cardiac clinics focusing on long-term management and follow-up, the burgeoning sector of ambulatory surgical centers (ASCs) which are increasingly performing less invasive procedures due to their efficiency, and, with growing prominence, homecare settings driven by the expansion of remote patient monitoring and telehealth services. Such precise insights are crucial for manufacturers to effectively tailor their sales and distribution strategies, develop targeted marketing campaigns that resonate with specific customer segments, and optimize their service offerings to meet the unique operational requirements and patient demographics of each facility type. Moreover, segmentation by both the underlying technology employed in the devices and the specific therapy type they enable provides invaluable elucidation into the core innovations that are driving device efficacy and the precise treatment modalities they are designed to deliver. This segment-specific analysis offers critical foresight into current therapeutic advancements, evolving patient management paradigms, and potential future directions for cardiac care, allowing for highly precise market positioning and strategic investment in R&D to address emerging needs.

This comprehensive and multi-layered segmentation framework is far more than an academic exercise; it forms the foundational bedrock for all strategic business planning, targeted marketing efforts, and informed decision-making processes for every participant within the CHF treatment devices ecosystem. By dissecting the total market into these discernible and analyzable components, industry players can gain a much deeper understanding of the competitive landscapes, accurately identify currently unmet clinical needs within specific patient subgroups, and effectively allocate their precious resources for focused research, agile development, and optimized market penetration initiatives. The rich insights gleaned from such a detailed segmentation are absolutely pivotal for fostering continuous innovation, refining product development pipelines to be more responsive to clinical demands, and ultimately ensuring that the most appropriate, effective, and accessible treatment devices reach the patients who need them most. This strategic clarity not only drives sustainable market growth but also makes a profound positive impact on global cardiac health outcomes, contributing to both improved longevity and enhanced quality of life for millions of CHF sufferers worldwide. The ability to precisely segment allows for tailored solutions addressing unique market demands and maximizing therapeutic benefit.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $16.5 billion |

| Market Forecast in 2032 | $26.4 billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, GE HealthCare Technologies Inc., Johnson & Johnson (Abiomed, Inc.), LivaNova PLC, ResMed Inc., Biotronik SE & Co. KG, Koninklijke Philips N.V., Zoll Medical Corporation (an Asahi Kasei company), MicroPort Scientific Corporation, ReliantHeart Inc., Syncardia Systems LLC, Jarvik Heart, Inc., CardioMech AS, Edwards Lifesciences Corporation, Teleflex Incorporated, Nevro Corp., Impulse Dynamics N.V., Carmat SA, Berlin Heart GmbH, Getinge AB, Asahi Kasei Corp. (Cardiac Rhythm Management), Baxter International Inc., AtriCure, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.