ID : MRU_ 430725 | Date : Nov, 2025 | Pages : 248 | Region : Global | Publisher : MRU

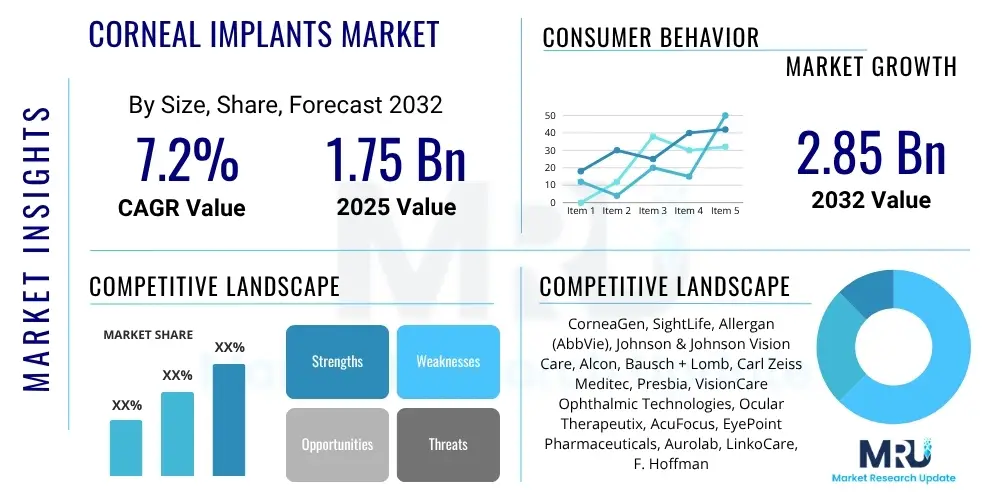

The Corneal Implants Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2032. The market is estimated at $1.75 Billion in 2025 and is projected to reach $2.85 Billion by the end of the forecast period in 2032.

The Corneal Implants Market encompasses a range of medical devices designed to replace or repair damaged corneal tissue, restoring vision and alleviating symptoms for patients suffering from various corneal disorders. These implants, which can be synthetic, biological, or a combination, address conditions such as keratoconus, Fuchs' dystrophy, corneal ulcers, and other forms of corneal opacity or damage. The primary objective of corneal implantation is to improve visual acuity, reduce pain, and enhance the overall quality of life for individuals whose sight is compromised by corneal pathology, offering a viable alternative or complement to traditional corneal transplantation.

Product descriptions within this market vary significantly, ranging from allogenic tissue grafts (donor corneas) to advanced artificial corneas and specialized intracorneal ring segments. Major applications include the treatment of ectatic corneal diseases, infectious keratitis, and bullous keratopathy, where the cornea's structural integrity or transparency is severely compromised. The fundamental benefits of these implants include significant vision improvement, reduced reliance on spectacles or contact lenses, and often, a quicker recovery time compared to full corneal transplants. Key driving factors propelling market growth include the escalating global prevalence of corneal blindness, an aging population more susceptible to ocular diseases, and continuous advancements in biomaterials and surgical techniques, which are expanding the indications and success rates of these innovative devices.

The Corneal Implants Market is experiencing robust expansion driven by a confluence of factors, including increasing awareness of corneal disorders, technological innovations in implant materials, and improved surgical outcomes. Business trends indicate a strong focus on research and development, particularly in biodegradable and bio-integrated materials, and a growing number of strategic collaborations among pharmaceutical and medical device companies aimed at expanding product portfolios and market reach. The competitive landscape is characterized by both established global players and emerging specialized firms vying for market share through product differentiation and geographical expansion. Furthermore, the market is witnessing a shift towards minimally invasive procedures and personalized implant solutions, aligning with broader healthcare trends.

Regional trends highlight North America and Europe as dominant markets due to well-developed healthcare infrastructures, high adoption rates of advanced medical technologies, and significant research funding. However, the Asia Pacific region is poised for the most rapid growth, fueled by a large patient pool, increasing healthcare expenditure, and improving access to advanced ophthalmic care in developing economies. Latin America and the Middle East and Africa are also emerging as promising markets, albeit with slower adoption rates, as healthcare facilities and patient awareness continue to improve. Segment trends demonstrate a rising demand for artificial corneas in cases where donor tissue is scarce or unsuitable, alongside continued innovation in biomaterial-based implants offering superior biocompatibility and integration. The market also sees growth in indications such as keratoconus and bullous keratopathy, driving demand for specific implant types tailored to these conditions, while end-user segments like hospitals and specialized ophthalmic clinics remain primary consumers of these devices.

User inquiries regarding Artificial Intelligence's influence on the Corneal Implants Market frequently revolve around its potential to revolutionize diagnostics, personalize treatment plans, enhance surgical precision, and accelerate material development. Common themes include how AI can improve the early and accurate detection of corneal diseases, leading to timely intervention, and whether AI algorithms can predict optimal implant designs for individual patients based on their unique ocular parameters. There are also significant expectations concerning AI's role in guiding surgeons during complex implantation procedures, potentially reducing human error and improving success rates. Furthermore, users are keen on understanding if AI can streamline the R&D process for novel biomaterials and analyze vast datasets from clinical trials to identify patterns for better implant efficacy and safety, alongside questions about the ethical implications and data privacy challenges posed by AI integration in such a sensitive medical field.

The Corneal Implants Market is significantly shaped by a dynamic interplay of driving forces, inherent restraints, and burgeoning opportunities that collectively determine its growth trajectory and competitive landscape. Key drivers include the escalating global prevalence of corneal disorders such as keratoconus, Fuchs' dystrophy, and infectious keratitis, which necessitate advanced interventional solutions. The aging global population, being more susceptible to age-related ocular conditions, further amplifies the demand for corneal repair and replacement options. Technological advancements in biomaterials, surgical techniques, and diagnostic imaging are continuously improving implant efficacy, safety, and patient outcomes, thereby expanding their adoption. Additionally, rising healthcare expenditure and increasing patient awareness regarding available treatment options contribute substantially to market growth, particularly in developing regions where access to quality eye care is improving.

However, several significant restraints impede the market's full potential. The high cost associated with corneal implant procedures, encompassing the implant itself, surgical fees, and post-operative care, can be a major barrier for many patients, especially in lower-income settings. The persistent global shortage of donor corneas remains a critical challenge, underscoring the need for synthetic and artificial alternatives. Post-operative complications such as infection, rejection, and glaucoma, although increasingly rare, can deter both patients and clinicians. Furthermore, stringent regulatory approval processes for novel devices, particularly for innovative biomaterials and complex implants, often lead to extended development timelines and increased R&D costs, impacting market entry and product commercialization. These restraints necessitate ongoing innovation to develop more affordable, readily available, and safer implant solutions, driving the search for effective substitutes for donor tissues.

Opportunities in the market are abundant, primarily stemming from the untapped potential in emerging economies where a large patient population coexists with improving healthcare infrastructure and growing disposable incomes. Advancements in regenerative medicine and stem cell research hold promise for developing biologically integrated and self-healing corneal tissues. The continuous innovation in advanced biomaterials, including smart polymers and nanotechnology-enabled implants, offers avenues for enhanced biocompatibility and functional integration. The integration of artificial intelligence and machine learning in diagnostics, personalized implant design, and surgical guidance represents a transformative opportunity for precision medicine in ophthalmology. Additionally, the development of affordable, scalable manufacturing processes for artificial corneas could mitigate the donor tissue shortage, expanding access to treatment globally. These opportunities, when strategically pursued, can overcome existing restraints and propel the market toward substantial growth and wider patient benefit.

The Corneal Implants Market is comprehensively segmented to provide a detailed understanding of its diverse components, allowing for targeted analysis of growth drivers and challenges across various product types, indications, end-users, and materials. This segmentation helps stakeholders, including manufacturers, healthcare providers, and investors, to identify key market trends, unmet needs, and lucrative opportunities. The intricate nature of corneal pathologies and the varied approaches to their treatment necessitate a granular view of the market, distinguishing between different implant technologies and their specific applications. Each segment possesses unique characteristics influencing its adoption rate, pricing dynamics, and competitive landscape.

Understanding these segments is crucial for strategic planning, product development, and market positioning. For instance, the demand for artificial corneas is driven by the scarcity of donor tissues and complex cases where conventional grafts fail, while biological corneas continue to be the gold standard when available. Similarly, the prevalence of specific indications like keratoconus or bullous keratopathy directly influences the demand for tailored implant solutions. Analyzing these segments provides insights into patient demographics, clinical preferences, technological advancements, and regulatory environments, offering a holistic perspective on the market's structure and potential for future growth across different geographical regions and healthcare settings.

The value chain for the Corneal Implants Market is a complex ecosystem involving multiple stages, from raw material sourcing and research to patient implantation and post-operative care. Upstream activities begin with the meticulous acquisition and processing of raw materials. This includes the sourcing of donor corneas from eye banks for biological implants, ensuring rigorous screening and preservation protocols. For artificial and synthetic implants, it involves procuring high-grade medical polymers like PMMA, hydrogels, and specialized biocompatible materials from chemical and biotech suppliers. Extensive research and development efforts are paramount at this stage, focusing on novel biomaterials, advanced manufacturing techniques, and clinical testing to enhance implant efficacy, safety, and integration with host tissue, driving innovation and intellectual property generation.

Midstream, manufacturers transform these raw materials and R&D insights into finished corneal implant products. This stage encompasses design, precision manufacturing, sterilization, and rigorous quality control to meet strict medical device regulations. These companies often invest heavily in cleanroom facilities and advanced production lines to ensure product integrity. Downstream activities involve the distribution and delivery of these specialized implants to end-users. Distribution channels are typically highly specialized due to the sensitive nature of the products, particularly for biological grafts which have limited shelf life and require specific storage conditions. Both direct sales forces, employed by major manufacturers to engage directly with hospitals and ophthalmic clinics, and indirect channels, through third-party distributors and medical device wholesalers, play critical roles in market penetration and product accessibility. Ethical considerations, regulatory compliance, and logistical efficiency are critical across all stages of this value chain, ensuring that patients receive safe and effective treatments.

The distribution network for corneal implants involves a carefully managed logistics process. Direct channels facilitate closer relationships between manufacturers and large hospital groups or key opinion leaders, allowing for immediate feedback and tailored support. Indirect channels, through specialized medical distributors, are vital for reaching a broader network of smaller clinics and surgical centers, particularly in geographically dispersed or emerging markets. These distributors often provide warehousing, local market expertise, and logistical support. The selection of distribution channel is often dictated by factors such as product type (e.g., biological grafts might require direct, specialized handling), regulatory requirements, market size, and the manufacturer's strategic objectives. Both direct and indirect models are crucial for ensuring the widespread availability of corneal implants, ultimately impacting patient access to these vision-restoring therapies and driving market growth.

The primary potential customers and end-users of corneal implants are healthcare institutions and individual patients suffering from various corneal diseases that lead to vision impairment. Hospitals, particularly those with dedicated ophthalmology departments and surgical capabilities, represent a significant segment of buyers. These facilities procure implants for a broad range of surgical procedures, from emergency treatments for corneal trauma to elective surgeries for chronic conditions like keratoconus. Their purchasing decisions are often influenced by clinical efficacy, product safety, cost-effectiveness, and the availability of advanced surgical support, as well as institutional affiliations with specific manufacturers or distributors. Large academic medical centers and university hospitals also serve as key customers due to their involvement in complex cases, clinical trials, and training of future ophthalmic surgeons.

Specialized ophthalmic clinics and ambulatory surgical centers (ASCs) also form a crucial customer base. These facilities, often focusing exclusively on eye care, are increasingly performing corneal implant procedures due to advancements in surgical techniques that allow for outpatient settings. Their demand is driven by the growing number of patients seeking specialized eye care and the economic benefits of performing procedures in a more streamlined environment compared to traditional hospitals. Surgeons within these clinics play a pivotal role in product selection, often based on their experience, training, and perceived benefits of particular implant types or brands. Ultimately, while the institutions are the direct purchasers, the underlying demand is generated by millions of patients worldwide suffering from corneal blindness or severe vision impairment, seeking restoration of their sight and improvement in their quality of life.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $1.75 Billion |

| Market Forecast in 2032 | $2.85 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | CorneaGen, SightLife, Allergan (AbbVie), Johnson & Johnson Vision Care, Alcon, Bausch + Lomb, Carl Zeiss Meditec, Presbia, VisionCare Ophthalmic Technologies, Ocular Therapeutix, AcuFocus, EyePoint Pharmaceuticals, Aurolab, LinkoCare, F. Hoffmann-La Roche Ltd, KeraMed, Inc., Dioptx, Inc., Cornea Biosciences, EyeYon Medical, Alpha Cornea. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Corneal Implants Market is profoundly shaped by a rapidly evolving technological landscape, where innovations across various scientific disciplines are enhancing the efficacy, safety, and accessibility of treatments. A cornerstone of this advancement lies in the development of advanced biomaterials, moving beyond inert polymers like PMMA to include more biocompatible and bio-integrated substances such as hydrogels, collagen-based materials, and synthetic polymers designed to mimic the natural corneal extracellular matrix. These materials aim to reduce rejection rates, promote cellular integration, and improve long-term visual outcomes. Emerging technologies like 3D bioprinting hold immense promise for creating patient-specific corneal tissues and artificial corneas with precise anatomical and functional properties, potentially overcoming the critical shortage of donor corneas and offering a truly personalized treatment approach for complex cases of corneal damage or disease.

Surgical techniques have also undergone significant transformation with the advent of femtosecond lasers and other precision instruments, enabling more accurate and minimally invasive procedures. These technologies allow for lamellar keratoplasty, where only the diseased layers of the cornea are replaced, preserving healthy tissue and leading to quicker recovery times and reduced complications compared to full-thickness penetrating keratoplasty. Advanced imaging technologies, such as Optical Coherence Tomography (OCT) and corneal topography, are crucial for precise pre-operative planning, intra-operative guidance, and post-operative monitoring, ensuring optimal implant placement and assessing graft integration. Furthermore, drug delivery systems incorporated into implants are being explored to provide sustained release of therapeutic agents, preventing infection or inflammation, and improving overall success rates. The integration of artificial intelligence and machine learning in diagnostics and surgical planning is another frontier, promising to refine patient selection, optimize implant design, and enhance surgical precision, thereby driving the market towards more personalized and successful patient outcomes.

Corneal implants are medical devices or engineered tissues designed to replace or repair a damaged cornea, the transparent front part of the eye. They differ from traditional corneal transplants, which involve grafting donor human corneal tissue, by often using synthetic or advanced biomaterials. Implants can be partial (e.g., intracorneal ring segments) or full (artificial corneas), offering alternatives when donor tissue is scarce, unsuitable, or when specific corneal conditions require a non-biological solution.

An ideal candidate for a corneal implant procedure typically suffers from conditions that cause corneal opacity, distortion, or structural weakness, leading to significant vision impairment or pain. Common indications include advanced keratoconus, severe bullous keratopathy, corneal scarring from infections or trauma, and conditions where traditional corneal transplants have failed or are not feasible due to a shortage of donor tissue or high risk of rejection. A comprehensive ophthalmic evaluation is essential to determine suitability.

Key benefits of corneal implants include significant improvement in visual acuity, relief from pain and discomfort caused by corneal pathology, and a potential reduction in the dependency on corrective lenses. For some conditions, implants offer a more predictable outcome or a faster recovery time compared to full-thickness corneal transplants. They also provide a vital treatment option in regions or for patients where donor corneal tissue is unavailable or contraindicated, thereby restoring quality of life and functional vision.

As with any surgical procedure, corneal implants carry potential risks and complications, although modern techniques have significantly minimized them. These can include infection, inflammation, implant rejection (particularly for biological materials), glaucoma, cataract formation, implant extrusion, and vision fluctuations. Careful patient selection, meticulous surgical technique, and diligent post-operative care are crucial for managing these risks and ensuring the best possible long-term outcomes for patients.

Artificial intelligence is profoundly impacting the future of corneal implants by enhancing diagnostic precision, enabling personalized implant design, and improving surgical outcomes. AI algorithms can analyze complex corneal imaging data for early and accurate disease detection, predict optimal implant shapes for individual patient anatomy, and guide surgeons during procedures for increased precision. Furthermore, AI accelerates the discovery of novel biomaterials and helps in analyzing vast clinical trial data to refine implant efficacy and safety, leading to more advanced and tailored treatment solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.