ID : MRU_ 430624 | Date : Nov, 2025 | Pages : 249 | Region : Global | Publisher : MRU

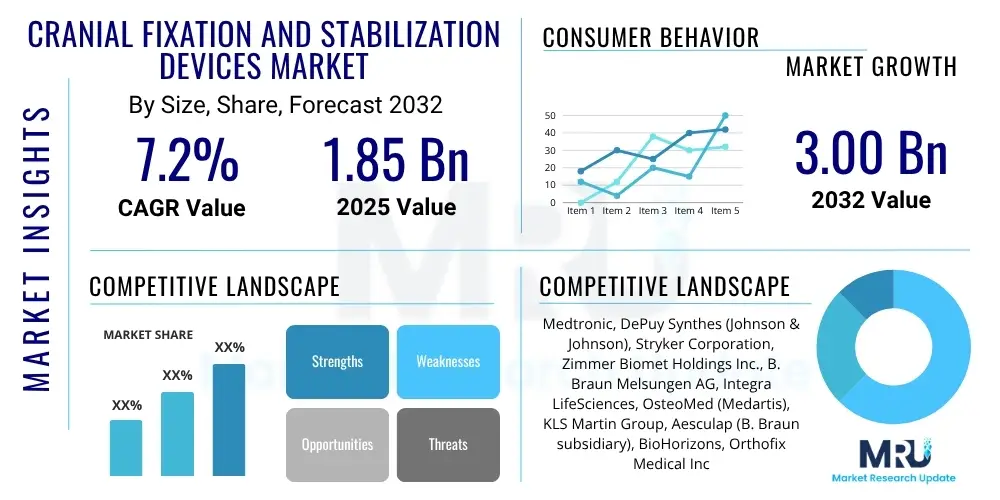

The Cranial Fixation and Stabilization Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2032. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.00 Billion by the end of the forecast period in 2032.

The Cranial Fixation and Stabilization Devices Market encompasses a range of specialized medical instruments and implants designed to secure bone fragments, stabilize the skull, or facilitate access during neurosurgical, craniofacial, and trauma-related procedures. These devices are crucial for maintaining anatomical integrity, promoting proper healing, and protecting delicate brain tissue following injury, tumor resection, or congenital defects. The primary objective of these products is to provide rigid internal fixation, ensuring that cranial bones remain in their intended position throughout the recovery phase.

Product descriptions within this market segment include various plates, screws, meshes, clamps, and halo systems, each engineered for specific applications and anatomical requirements. Cranial plates, often made from titanium or bioresorbable polymers, come in different shapes and sizes to bridge gaps or reinforce weakened areas of the skull. Corresponding screws secure these plates, while meshes offer broader coverage for larger defects. Major applications for these devices span neurosurgery, treating traumatic brain injuries, performing reconstructive surgery for congenital anomalies or post-surgical defects, and managing conditions requiring temporary external cranial stabilization. The devices are instrumental in procedures such as craniotomies, cranioplasties, and the repair of skull fractures, ensuring precise and stable fixation.

The benefits derived from advanced cranial fixation and stabilization devices are significant, contributing to improved patient outcomes by minimizing post-operative complications, reducing recovery times, and enhancing the aesthetic and functional results of cranial reconstruction. These devices provide mechanical stability, which is vital for preventing displacement of bone fragments and facilitating osseointegration. Key driving factors propelling market growth include the escalating global incidence of traumatic brain injuries due to accidents, the increasing prevalence of neurological disorders requiring surgical intervention, the expansion of the geriatric population prone to such conditions, and continuous technological advancements in implant design and materials science, particularly in biocompatible and customizable options.

The Cranial Fixation and Stabilization Devices Market is experiencing robust growth, primarily driven by advancements in neurosurgical techniques and an increasing global burden of neurological disorders and traumatic head injuries. Business trends indicate a strong emphasis on research and development, leading to innovative product launches that offer enhanced biocompatibility, improved surgical outcomes, and greater patient comfort. Strategic collaborations, mergers, and acquisitions are common as companies seek to expand their product portfolios and geographical reach, consolidating market presence and leveraging specialized expertise. Furthermore, there is a rising demand for patient-specific implants enabled by advanced manufacturing processes like 3D printing, which addresses unique anatomical challenges and reduces operative time, reflecting a shift towards personalized medicine within the neurosurgical landscape.

Regional trends reveal North America and Europe as dominant markets, attributed to sophisticated healthcare infrastructures, high awareness of advanced treatment options, and significant healthcare expenditure. However, the Asia Pacific region is poised for substantial growth, driven by a rapidly expanding patient pool, improving healthcare access, increasing medical tourism, and rising disposable incomes. Emerging economies in Latin America and the Middle East and Africa are also showing promising growth trajectories, albeit from a smaller base, as these regions invest in modernizing their healthcare systems and adopting advanced medical technologies. Local manufacturers in these regions are also increasingly contributing to market dynamics, often offering cost-effective solutions tailored to local market needs.

Segmentation trends highlight the increasing preference for bioresorbable materials over traditional metallic implants in specific applications, particularly in pediatric cases, due to their ability to degrade over time and eliminate the need for secondary removal surgeries. Titanium remains a cornerstone material due to its strength and biocompatibility, but PEEK (Polyetheretherketone) is gaining traction for its radiolucency and mechanical properties akin to bone. Within applications, neurosurgery and trauma surgery continue to be the largest segments, though reconstructive surgery for congenital defects and oncology-related resections is also growing steadily. Hospitals remain the primary end-users, but the expansion of ambulatory surgical centers (ASCs) is creating new avenues for market penetration, particularly for less complex procedures, driven by cost-effectiveness and patient convenience.

User inquiries concerning AI's influence on the Cranial Fixation and Stabilization Devices Market frequently revolve around how artificial intelligence can enhance surgical planning, improve precision during procedures, personalize device design, and ultimately lead to safer and more effective patient outcomes. Common themes include the integration of AI with advanced imaging for more accurate diagnoses and surgical roadmaps, the role of machine learning in predicting patient responses to different fixation techniques, and the potential for AI-driven robotics to assist in implant placement. Users also express interest in how AI could streamline regulatory processes, reduce development costs for new devices, and facilitate the adoption of complex technologies, alongside concerns about data privacy, algorithmic bias, and the need for rigorous validation of AI-powered tools in clinical settings. The overarching expectation is that AI will revolutionize the precision and customization of cranial interventions, moving towards a future of highly individualized and outcome-optimized treatments.

The Cranial Fixation and Stabilization Devices Market is primarily driven by the escalating global incidence of neurological disorders such as brain tumors, epilepsy, and hydrocephalus, which often necessitate surgical interventions requiring cranial fixation. A significant factor is the rising number of traumatic brain injuries (TBIs) resulting from road accidents, sports injuries, and falls, particularly within the growing geriatric population, which is more susceptible to these injuries and subsequent surgical needs. Technological advancements in biomaterials, such as the development of bioresorbable implants and improved titanium alloys, coupled with sophisticated imaging and navigation systems, further propel market expansion by offering more effective and less invasive treatment options. The increasing demand for minimally invasive surgical techniques also encourages innovation in device design, aiming to reduce patient morbidity and accelerate recovery.

Despite these drivers, the market faces several significant restraints. The high cost associated with advanced cranial fixation devices and the complex surgical procedures they entail can be a major barrier, particularly in developing economies or for patients with limited insurance coverage. Stringent regulatory approval processes, especially in mature markets like North America and Europe, can extend product development timelines and increase costs for manufacturers, potentially hindering innovation and market entry for smaller players. Furthermore, the inherent risks of post-operative complications, such as infection, implant failure, or adverse tissue reactions, can deter both patients and healthcare providers. Limited reimbursement policies for certain advanced devices or procedures in various healthcare systems also pose a challenge, impacting market penetration and adoption rates.

Opportunities for growth are abundant, particularly in emerging markets across Asia Pacific and Latin America, where healthcare infrastructure is rapidly improving, and access to advanced medical treatments is expanding. These regions present untapped potential due to their large populations and increasing healthcare expenditure. The development of customized and patient-specific implants, facilitated by advancements in 3D printing and CAD/CAM technologies, represents a significant opportunity to address complex anatomical variations and improve surgical precision, fostering a personalized medicine approach. Furthermore, the continued integration of advanced imaging and surgical navigation systems, coupled with robotic assistance, promises to enhance surgical efficiency and safety, making complex procedures more accessible and attractive. The expansion of outpatient surgical settings, or ambulatory surgical centers (ASCs), also offers a cost-effective alternative for certain procedures, driving market growth in specialized settings.

The Cranial Fixation and Stabilization Devices Market is meticulously segmented based on various factors, providing a comprehensive understanding of its intricate dynamics and identifying key areas of growth and investment. These segments allow for a detailed analysis of product adoption patterns, material preferences, application specificities, and end-user demands, offering valuable insights for stakeholders across the healthcare value chain. Understanding these segmentations is critical for market players to tailor their product development, marketing strategies, and distribution networks to effectively address the diverse needs of the global market. The market can be broadly categorized by product type, material, application, and end-user, each with its distinct characteristics and growth drivers.

The value chain for the Cranial Fixation and Stabilization Devices Market begins with upstream activities involving the sourcing and processing of raw materials. This typically includes suppliers of medical-grade titanium alloys, high-performance polymers like PEEK, and biocompatible bioresorbable materials such as PLA and PGA. These raw material providers adhere to stringent quality and regulatory standards to ensure the safety and efficacy of the final medical devices. Research and development phases, including material science innovation, biomechanical testing, and prototype development, also form a critical upstream component, requiring significant investment and specialized expertise to create advanced, durable, and biocompatible devices.

Midstream activities involve the design, manufacturing, and assembly of the cranial fixation and stabilization devices. This stage employs advanced manufacturing technologies such as precision machining, additive manufacturing (3D printing), and injection molding to produce plates, screws, meshes, and other components. Quality control and assurance are paramount throughout the manufacturing process to meet international medical device regulations and certifications. Packaging, sterilization, and inventory management are also key midstream functions, ensuring that products are ready for safe and effective use in clinical settings. Intellectual property protection and regulatory compliance, including obtaining FDA approvals and CE markings, are integral to this stage, enabling market access.

Downstream activities focus on the distribution, sales, and post-sales support of the devices. Distribution channels can be both direct and indirect. Direct distribution involves manufacturers selling directly to hospitals, neurosurgical centers, and other healthcare facilities, often through their dedicated sales forces who provide technical expertise and training. Indirect distribution relies on a network of authorized distributors, wholesalers, and group purchasing organizations (GPOs) that facilitate broader market reach, especially in geographically diverse or emerging markets. These distributors often manage warehousing, logistics, and local customer support. Post-sales services include technical support, product training for surgeons and surgical staff, and handling any product-related inquiries or issues, ensuring optimal device usage and patient safety. The efficacy of both direct and indirect channels is critical for market penetration and customer relationship management.

The primary potential customers for Cranial Fixation and Stabilization Devices are diverse healthcare entities and medical professionals actively involved in neurosurgery, craniofacial reconstruction, and trauma care. The largest segment of end-users consists of hospitals, particularly those with specialized neurosurgery departments, trauma centers, and advanced operating theaters equipped to handle complex cranial procedures. These institutions require a steady supply of a wide range of devices for various patient conditions, from emergency trauma cases to elective reconstructive surgeries. The demand from hospitals is consistently high due to the comprehensive nature of care provided and the volume of intricate surgical interventions performed.

Ambulatory Surgical Centers (ASCs) represent a growing segment of potential customers, particularly for less complex or elective procedures that do not require extended hospital stays. As healthcare systems increasingly seek cost-effective alternatives to traditional inpatient hospital care, ASCs are becoming more prevalent for specific cranial and facial surgical interventions, driving demand for efficient and easy-to-use fixation devices. These centers focus on patient convenience and streamlined processes, influencing the types of devices they procure.

Specialty clinics, such as those focusing on craniofacial surgery, plastic and reconstructive surgery, and specialized ENT (Ear, Nose, and Throat) practices, also constitute a significant customer base. These clinics often cater to specific patient populations, including pediatric cases or individuals requiring aesthetic and functional restoration of the craniofacial region. Furthermore, research and academic institutions, while not direct end-users in patient care, are vital potential customers for advanced and experimental devices used in clinical trials, anatomical studies, and the development of new surgical techniques, contributing to the innovation pipeline and future market growth.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2032 | USD 3.00 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet Holdings Inc., B. Braun Melsungen AG, Integra LifeSciences, OsteoMed (Medartis), KLS Martin Group, Aesculap (B. Braun subsidiary), BioHorizons, Orthofix Medical Inc., Globus Medical, Craniotech, Fixus Surgical, Jeil Medical Corporation, Xtant Medical, Invibio Ltd., Articular Engineering, GE Healthcare, Renishaw plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Cranial Fixation and Stabilization Devices Market is profoundly shaped by a rapidly evolving technological landscape, with innovations continuously enhancing the precision, efficacy, and safety of cranial procedures. One of the most impactful technologies is Computer-Aided Design (CAD) and Computer-Aided Manufacturing (CAM), which enable the creation of highly customized and patient-specific implants (PSIs). These systems integrate directly with advanced imaging modalities like CT and MRI, allowing surgeons to design implants that perfectly match a patient's unique anatomical contours and pathological defects, significantly improving fit and reducing operating time. This personalization is a major driver, moving away from off-the-shelf solutions towards tailored medical interventions.

Additive manufacturing, commonly known as 3D printing, is another transformative technology. It facilitates the rapid and cost-effective production of complex implant geometries that are impossible to achieve with traditional manufacturing methods. 3D printing allows for the creation of porous structures that promote better bone ingrowth and reduces overall implant weight, while also enabling the fabrication of custom titanium meshes and PEEK implants with precise anatomical conformity. Furthermore, advancements in material science are critical, particularly the development of advanced biocompatible materials such as improved titanium alloys with enhanced mechanical properties and bioresorbable polymers that eliminate the need for secondary removal surgeries, reducing patient burden and healthcare costs, especially relevant in pediatric applications.

Beyond implant manufacturing, surgical navigation systems and robotics are increasingly being integrated into cranial procedures. Navigation systems, using optical or electromagnetic tracking, provide real-time guidance to surgeons, overlaying instrument positions onto patient imaging data, thereby improving accuracy in screw placement and implant positioning, minimizing risk to vital structures. Robotic-assisted surgery, while still emerging in neurosurgery, holds immense potential for enhancing precision and consistency in complex tasks. Furthermore, intraoperative imaging, such as mobile CT scans, provides immediate feedback, allowing for adjustments during surgery. These technologies collectively contribute to improved surgical outcomes, reduced complications, and greater patient safety, underpinning the market's trajectory towards highly precise and individualized cranial interventions.

Cranial fixation and stabilization devices are specialized medical implants and instruments used in neurosurgery, trauma surgery, and reconstructive surgery to secure bone fragments, stabilize the skull, or facilitate access to the brain. They are essential for repairing skull fractures, stabilizing cranial bone flaps after craniotomies, and reconstructing craniofacial defects, ensuring proper healing and protecting brain tissue.

Common materials include medical-grade titanium and its alloys due to their high strength, biocompatibility, and MRI compatibility. Polyetheretherketone (PEEK) is also widely used for its radiolucency, allowing clear post-operative imaging, and mechanical properties similar to bone. Additionally, bioresorbable polymers like Polylactic Acid (PLA) and Polyglycolic Acid (PGA) are gaining popularity, especially in pediatric applications, as they safely degrade over time, eliminating the need for a second surgery to remove the implant.

Artificial intelligence is significantly impacting the market by enhancing surgical planning through advanced imaging analysis, enabling the design of patient-specific implants with greater precision, and improving intraoperative navigation. AI-driven analytics can predict optimal implant characteristics and assist in robotic-assisted surgery, leading to more accurate placement, reduced operative time, and ultimately, better patient outcomes and personalized treatment strategies.

The primary growth drivers include the rising global incidence of traumatic brain injuries and neurological disorders, the increasing geriatric population prone to such conditions, and continuous technological advancements in implant materials and surgical techniques. The growing demand for minimally invasive procedures and patient-specific solutions also significantly contributes to market expansion across various regions.

North America and Europe currently lead in market adoption due to their robust healthcare infrastructures, high healthcare expenditure, and early integration of advanced medical technologies. However, the Asia Pacific region is anticipated to exhibit the fastest growth, driven by improving healthcare access, a large patient pool, and increasing investments in medical device technologies in countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.