ID : MRU_ 429249 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

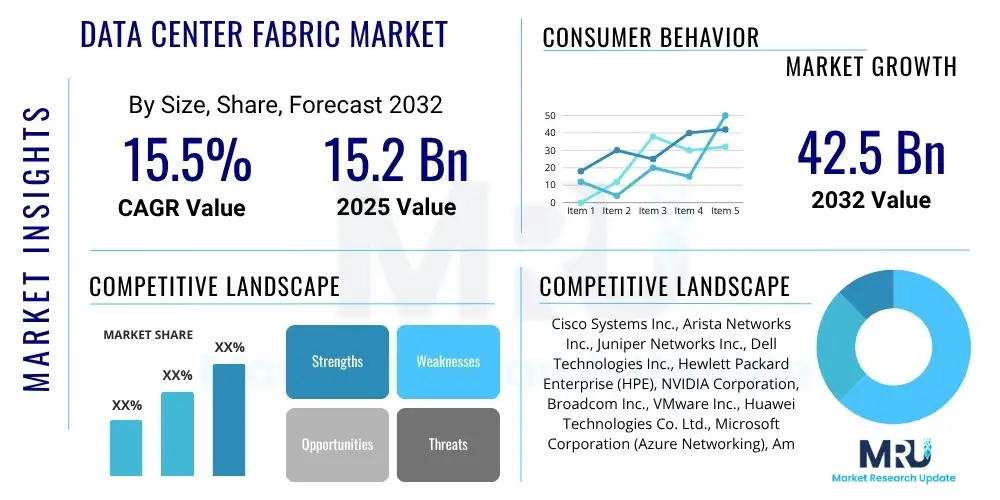

The Data Center Fabric Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2025 and 2032. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 42.5 Billion by the end of the forecast period in 2032.

The Data Center Fabric Market encompasses the advanced networking infrastructure designed to provide high-speed, low-latency, and scalable connectivity within and across data centers. This innovative architecture moves beyond traditional three-tier network designs, offering a flatter, more efficient, and agile network foundation essential for modern, virtualized, and cloud-native environments. It enables seamless communication between servers, storage, and other network devices, addressing the escalating demands of data-intensive applications and the burgeoning traffic within data centers.

The primary products within this market include high-performance switches, routers, network interface cards (NICs), optical modules, and sophisticated network operating systems, alongside orchestration and management software. These components collectively form a unified, high-bandwidth network that supports rapid data transfer and resource sharing. Major applications span hyperscale cloud computing, enterprise data centers, high-performance computing (HPC) clusters, artificial intelligence (AI) and machine learning (ML) workloads, and virtualization platforms where efficient resource allocation and minimal latency are paramount.

The benefits of adopting data center fabric solutions are numerous, including enhanced scalability, improved network agility, significant reductions in operational complexity, and optimized resource utilization. These systems facilitate a more dynamic and automated network environment, capable of adapting swiftly to changing application requirements and traffic patterns. Key driving factors propelling market growth include the exponential increase in data volumes, the widespread adoption of cloud computing services, the pervasive trend of server virtualization, and the rising demand for robust network infrastructures to support emerging technologies like AI, IoT, and edge computing, all of which necessitate superior network performance and flexibility.

The Data Center Fabric Market is experiencing robust expansion, primarily driven by a confluence of evolving business trends, significant regional developments, and dynamic segmentation shifts. Business trends indicate a relentless move towards hyperscale data centers, a surge in demand for hybrid cloud solutions, and the increasing imperative for network automation and orchestration to manage complex, distributed IT environments. Enterprises are increasingly prioritizing highly available, performant, and secure network infrastructures that can flexibly support demanding applications and digital transformation initiatives, moving away from rigid, legacy network architectures to more fluid, programmable fabric models. The emphasis on energy efficiency and sustainability in data center operations also influences technology choices within the fabric market.

Regionally, North America continues to dominate the market, propelled by the presence of major cloud service providers, early technology adoption, and significant investments in advanced data center infrastructure. However, the Asia Pacific region is rapidly emerging as a high-growth market, fueled by accelerating digital transformation across industries, expanding internet penetration, and substantial government and private sector investments in data center build-outs, particularly in countries like China, India, and Japan. Europe is also witnessing steady growth, influenced by stringent data residency regulations, a strong focus on data privacy, and increasing adoption of cloud services by enterprises, which necessitates resilient and compliant data center fabric solutions.

Segmentation trends highlight a strong preference for Ethernet fabric due to its ubiquity and evolving capabilities to support higher speeds (e.g., 400G, 800G). Software-defined networking (SDN) and network function virtualization (NFV) components are gaining significant traction, enabling greater programmability, automation, and operational efficiency. The market is also seeing increased demand for specific solutions tailored for high-performance computing (HPC) and AI/ML workloads, which often require specialized low-latency interconnects like InfiniBand or ultra-low-latency Ethernet. Service segments, including consulting, integration, and managed services, are growing as organizations seek expert assistance in designing, deploying, and managing complex fabric infrastructures, reflecting a broader trend towards outsourced specialized IT services.

The advent and proliferation of Artificial Intelligence (AI) and Machine Learning (ML) workloads are profoundly reshaping the Data Center Fabric Market, presenting both significant challenges and opportunities for innovation. Common user questions frequently revolve around how AI impacts existing fabric requirements, the need for specialized network architectures to support AI training and inference, the implications for network latency and bandwidth, and how AI itself can be leveraged to enhance fabric management and optimization. Users are particularly concerned about the capabilities of current data center fabrics to handle the intense, east-west traffic patterns and bursty nature of AI workloads, which differ significantly from traditional enterprise applications.

The primary themes emerging from these concerns highlight an urgent demand for ultra-low latency, massively scalable bandwidth, and intelligent traffic management within data center fabrics. AI training models, especially those involving large language models (LLMs) and complex neural networks, require extensive data exchange between graphics processing units (GPUs) and other accelerators, creating bottlenecks if the underlying network cannot keep pace. Expectations include the development of more deterministic and congestion-free fabrics, capable of ensuring consistent performance for sensitive AI tasks. Furthermore, there is a growing anticipation for AI-driven automation tools that can monitor network performance, predict potential issues, and optimize resource allocation proactively, thereby simplifying the management of increasingly complex fabric infrastructures.

In essence, AI is not only a consumer of advanced data center fabric capabilities but also a catalyst for its evolution, driving the need for more intelligent, higher-performing, and self-optimizing networks. This dual impact necessitates a strategic shift in how data center fabrics are designed, deployed, and managed, pushing towards architectures that are inherently aware of workload demands and can dynamically adapt to meet the unique requirements of AI applications, from foundational research to widespread commercial deployment, ensuring robust and efficient operation.

The Data Center Fabric Market is shaped by a complex interplay of drivers, restraints, and opportunities, collectively forming the impact forces that dictate its growth trajectory and competitive landscape. A primary driver is the surging volume of data generated globally, fueled by digital transformation, IoT, and online activities, which necessitates robust and high-capacity network infrastructures to store, process, and transmit this information efficiently within data centers. The widespread adoption of cloud computing, both public and private, along with the growing prevalence of virtualization, also acts as a significant catalyst, as these environments demand agile, scalable, and software-defined networks to maximize resource utilization and ensure service delivery. Furthermore, the imperative for low-latency communication in real-time applications, AI/ML workloads, and financial trading platforms underscores the need for advanced fabric solutions.

However, the market also faces notable restraints. The substantial initial investment required for deploying advanced data center fabric solutions, including high-performance hardware and sophisticated software, can be a significant barrier for smaller enterprises or those with limited IT budgets. The inherent complexity associated with designing, implementing, and managing these next-generation networks, often requiring specialized skills and extensive planning, poses another challenge. Concerns around vendor lock-in, where organizations become dependent on a single vendor's ecosystem, and evolving cybersecurity threats targeting critical network infrastructure, also act as deterrents, compelling businesses to carefully weigh their options and invest in comprehensive security measures.

Amidst these challenges, significant opportunities are emerging. The proliferation of edge computing, driven by IoT and 5G networks, is creating new demand for localized data center fabrics that can process data closer to its source, reducing latency and bandwidth costs. The ongoing integration of 5G infrastructure into enterprise and cloud networks also presents a fertile ground for growth, as it will necessitate higher-performance and more resilient backhaul networks. Additionally, the increasing focus on open networking initiatives and disaggregated hardware/software solutions is fostering innovation, promoting interoperability, and potentially lowering total cost of ownership by allowing greater flexibility and choice for customers. The continuous evolution of AI and ML technologies offers a perpetual demand driver, pushing the boundaries of network performance and intelligence within the data center fabric ecosystem.

The Data Center Fabric Market is comprehensively segmented to provide granular insights into its diverse components, technologies, applications, and end-user adoption patterns. This segmentation allows for a detailed analysis of market dynamics, identifying growth hotspots and understanding the specific needs of various industry verticals and technological preferences. The market can be broadly categorized by component type, distinguishing between the tangible hardware infrastructure, the intelligent software that orchestrates and manages the network, and the crucial services that support deployment and ongoing operations. Further delineation by type explores the underlying networking technologies, while application-based segmentation highlights the primary use cases driving demand. Finally, segmenting by end-user provides a clear picture of which industries are adopting these advanced networking solutions most aggressively.

The value chain for the Data Center Fabric Market is intricate, involving multiple stages from component manufacturing to end-user consumption, each contributing to the overall product and service delivery. This chain begins with upstream activities focused on research, development, and production of foundational technologies. This includes semiconductor manufacturers producing high-speed network processors, ASICs, and specialized chipsets that power network devices, as well as optical component manufacturers developing transceivers, fiber optic cables, and connectors critical for high-bandwidth data transmission. Software developers also play a crucial upstream role in creating network operating systems, SDN controllers, and orchestration platforms that enable the intelligence and automation within the fabric.

Moving downstream, the value chain involves the assembly, integration, and deployment of these components into complete data center fabric solutions. This stage includes hardware vendors who design and manufacture switches, routers, and servers, often integrating third-party components. System integrators and value-added resellers (VARs) then play a pivotal role in combining these diverse hardware and software elements, customizing them to meet specific customer requirements, and deploying them within data center environments. Managed service providers (MSPs) and cloud service providers (CSPs) represent another key downstream segment, consuming data center fabric solutions to build and operate their own infrastructure, which they then offer to end-users.

Distribution channels for data center fabric solutions are multifaceted, encompassing both direct and indirect models. Direct sales typically occur for large enterprises and hyperscale cloud providers, where vendors engage directly with customers to provide tailored solutions and dedicated support. Indirect channels involve a network of channel partners, including VARs, system integrators, and distributors, who extend the market reach of vendors, provide local support, and offer value-added services such as consulting, installation, and ongoing maintenance. This hybrid approach ensures that products and services reach a broad spectrum of end-users, from small and medium-sized businesses to global corporations, while maintaining specialized support where required for complex deployments. The efficiency of these channels directly impacts market penetration and customer satisfaction within the highly competitive data center fabric landscape.

The Data Center Fabric Market caters to a diverse range of potential customers, all seeking to enhance the performance, scalability, and agility of their network infrastructure to meet the demands of modern digital operations. The primary end-users and buyers of these advanced networking solutions are large enterprises across various sectors, hyperscale cloud service providers, and telecommunication companies. These entities share a common need for high-speed, low-latency, and resilient networks that can efficiently handle massive volumes of data traffic, support virtualized environments, and facilitate the rapid deployment of new services and applications. Their purchasing decisions are often driven by factors such as the total cost of ownership, ease of management, compatibility with existing infrastructure, and the ability to scale infrastructure on demand.

Cloud service providers, including giants like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, represent a significant customer segment. Their business model inherently relies on highly efficient, automated, and scalable data center fabrics to deliver reliable and high-performance cloud services to millions of customers globally. They invest heavily in cutting-edge fabric technologies to minimize latency, maximize throughput, and ensure the seamless operation of their extensive virtualized and containerized environments. Similarly, large enterprises in sectors such as BFSI, healthcare, manufacturing, and retail are increasingly adopting data center fabrics to support their digital transformation initiatives, manage big data analytics, deploy enterprise-wide cloud strategies, and ensure business continuity for critical applications.

Furthermore, telecommunication companies are key buyers as they modernize their networks to support 5G, edge computing, and virtualized network functions (NFV). They leverage data center fabrics to build out central offices re-architected as data centers (CORD) and to deploy distributed cloud infrastructure closer to their subscribers. Government and defense organizations also represent a crucial segment, prioritizing secure, robust, and high-performance fabrics for mission-critical applications and data storage. Educational institutions and research organizations, particularly those involved in high-performance computing (HPC) and scientific simulations, also constitute a significant customer base, demanding the ultra-low latency and massive bandwidth capabilities that data center fabrics provide for their intensive computational workloads.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2032 | USD 42.5 Billion |

| Growth Rate | CAGR 15.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems Inc., Arista Networks Inc., Juniper Networks Inc., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), NVIDIA Corporation, Broadcom Inc., VMware Inc., Huawei Technologies Co. Ltd., Microsoft Corporation (Azure Networking), Amazon Web Services Inc. (AWS Networking), Google LLC (Google Cloud Networking), Intel Corporation, Extreme Networks Inc., Ciena Corporation, Nokia Corporation, IBM Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Data Center Fabric Market is characterized by a rapidly evolving and sophisticated technology landscape, driven by the relentless pursuit of higher performance, greater flexibility, and enhanced automation. At its core, the shift from traditional three-tier networks to flat, high-density fabric architectures is enabled by technologies such as Software-Defined Networking (SDN) and Network Function Virtualization (NFV). SDN decouples the network's control plane from the data plane, allowing for centralized management, programmatic control, and agile configuration of network resources. NFV virtualizes network services, enabling them to run on standard server hardware, thereby improving resource utilization and reducing operational costs. These foundational technologies are crucial for building scalable, resilient, and highly programmable data center fabrics.

Further advancements in the technology landscape include the widespread adoption of Ethernet fabrics, which leverage high-speed Ethernet (e.g., 100 Gigabit Ethernet, 400 Gigabit Ethernet, and emerging 800 Gigabit Ethernet) to create a unified network for various traffic types, including server-to-server, server-to-storage, and inter-data center communication. For specialized, ultra-low-latency applications like HPC and AI/ML, InfiniBand continues to be a critical technology, offering unparalleled performance through its high-speed interconnects and remote direct memory access (RDMA) capabilities. Technologies like NVMe-oF (NVMe over Fabrics) are also gaining traction, enabling high-performance storage to be shared across the network with NVMe-level performance, crucial for data-intensive workloads.

Emerging technologies such as Data Processing Units (DPUs) or SmartNICs are further transforming the fabric, offloading network and security tasks from general-purpose CPUs, thus freeing up server resources and improving overall system efficiency. The concept of disaggregated infrastructure and composable architectures is also gaining momentum, allowing compute, storage, and networking resources to be pooled and dynamically allocated on demand, optimizing resource utilization and agility. Optical technologies, including advanced transceivers and active optical cables (AOCs), are essential for supporting the increasing distances and bandwidth requirements within and between data centers. These technological innovations collectively enable the creation of highly efficient, resilient, and intelligent data center fabrics that can adapt to the dynamic demands of modern digital infrastructure.

Data center fabric is an advanced networking architecture that creates a high-speed, low-latency, and scalable network connecting all resources within a data center, including servers, storage, and network devices, to enable efficient data transfer and resource sharing.

It is crucial for modern data centers as it supports the demands of virtualization, cloud computing, AI/ML workloads, and big data analytics by providing a flattened, agile, and automated network infrastructure that ensures high performance, scalability, and optimal resource utilization.

Unlike traditional three-tier networks with distinct access, aggregation, and core layers, data center fabric employs a flatter, often spine-leaf, architecture. This design reduces hop counts, minimizes latency, provides predictable performance, and simplifies management, offering greater scalability and agility for east-west traffic.

Key benefits include enhanced scalability and flexibility, improved network performance with lower latency and higher bandwidth, greater operational efficiency through automation, better resource utilization, and a more resilient and secure infrastructure to support evolving business demands.

SDN is a foundational technology for data center fabric, enabling centralized control and programmatic management of the network. It allows administrators to dynamically configure and optimize network resources, automate tasks, and adapt the network to application requirements, significantly enhancing agility and efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.