ID : MRU_ 428393 | Date : Oct, 2025 | Pages : 251 | Region : Global | Publisher : MRU

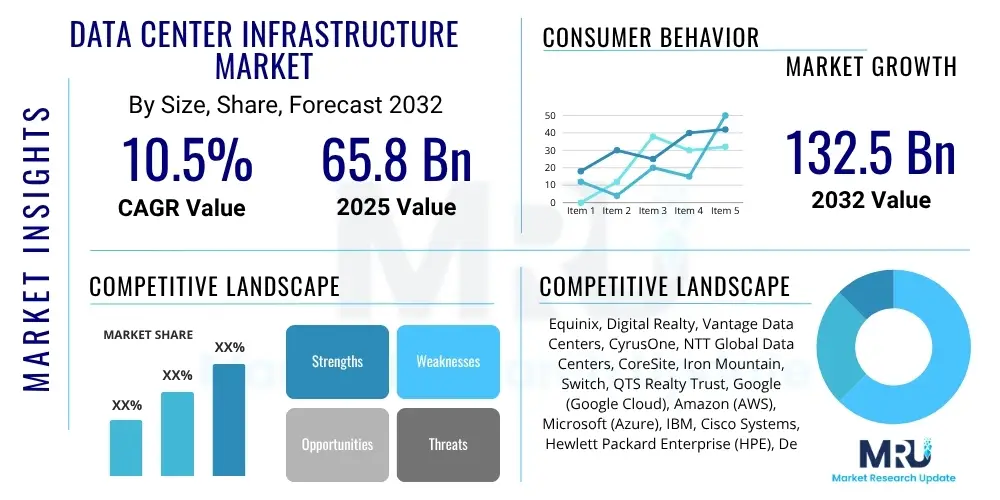

The Data Center Infrastructure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2032. The market is estimated at $65.8 Billion in 2025 and is projected to reach $132.5 Billion by the end of the forecast period in 2032.

The Data Center Infrastructure Market encompasses the essential components and services required for the operation of modern data centers, serving as the foundational backbone for digital information storage, processing, and distribution. This market involves a broad spectrum of products including power infrastructure such as UPS systems, generators, and power distribution units; cooling systems like CRAC/CRAH units, chillers, and liquid cooling solutions; networking equipment including switches, routers, and cabling; and physical security systems. Beyond hardware, it also comprises essential software solutions such as Data Center Infrastructure Management (DCIM) for monitoring and managing data center operations, security software, and automation tools. Major applications span enterprise computing, cloud computing, edge computing, and colocation services across diverse industries. The inherent benefits of robust data center infrastructure include enhanced reliability, improved performance, stringent security, energy efficiency, and scalability, all crucial for supporting the ever-increasing demands of digital transformation. The market is primarily driven by the escalating global data traffic, widespread adoption of cloud computing services, the proliferation of artificial intelligence and machine learning workloads, the rapid deployment of 5G technology, and the continuous need for digital innovation across all sectors. As businesses and individuals generate unprecedented volumes of data, the imperative for advanced, resilient, and efficient data center infrastructure becomes even more pronounced, shaping a dynamic and expanding market landscape.

The Data Center Infrastructure Market is currently experiencing robust growth, driven by an accelerating pace of digital transformation across global enterprises and the relentless expansion of cloud computing paradigms. Business trends highlight a significant shift towards hybrid and multi-cloud architectures, necessitating flexible and scalable infrastructure solutions capable of seamlessly integrating on-premise, colocation, and public cloud environments. There is also a pronounced emphasis on energy efficiency and sustainability, with businesses increasingly investing in green data center technologies and renewable energy sources to reduce operational costs and environmental impact. The demand for edge computing infrastructure is rapidly increasing, spurred by the need for low-latency processing closer to data sources for applications such as IoT, autonomous vehicles, and real-time analytics. Regional trends indicate North America and Europe as mature markets with high adoption of advanced data center technologies and significant investment in hyperscale facilities. The Asia Pacific region is emerging as the fastest-growing market, propelled by rapid digitalization, expanding internet penetration, and substantial investments from both domestic and international players in countries like China, India, and Japan. Latin America, the Middle East, and Africa are also witnessing considerable growth as digital infrastructure develops and cloud services proliferate. Segment-wise, the market is seeing strong performance in cooling solutions, particularly liquid cooling, due to the increased power density of AI and HPC workloads. DCIM software is gaining traction for its critical role in optimizing resource utilization and operational efficiency. Furthermore, the colocation and cloud data center types are dominating market share, reflecting the ongoing trend of outsourcing data center operations to specialized providers, while edge data centers represent a high-growth segment poised for significant expansion in the coming years.

Common user questions regarding AI's impact on the Data Center Infrastructure Market frequently revolve around how artificial intelligence and machine learning workloads are transforming traditional data center design, power requirements, cooling strategies, and overall operational efficiency. Users are concerned about the substantial increase in power consumption demanded by AI-accelerators, the need for advanced cooling solutions to manage extreme heat densities, and the implications for existing infrastructure scalability. They also inquire about the role of AI in optimizing data center operations, such as predictive maintenance, resource allocation, and energy management, and how this affects staffing and skill requirements. Furthermore, there is interest in understanding how AI influences the development of new, purpose-built data center architectures and the integration of specialized hardware. The overarching theme is a recognition of AI as both a significant challenge requiring fundamental shifts in infrastructure planning and a powerful tool offering unprecedented opportunities for optimization and innovation within the data center ecosystem.

The Data Center Infrastructure Market is primarily propelled by several powerful drivers that reflect the global digital transformation. The exponential growth in data generation from various sources, coupled with the increasing adoption of cloud computing, edge computing, and AI/ML technologies, mandates continuous investment in robust and scalable data center infrastructure. Organizations are migrating legacy systems to modern data center environments to achieve greater agility, efficiency, and cost savings, further fueling market expansion. Regulatory mandates concerning data privacy, localization, and security also necessitate specific infrastructure investments and compliance requirements, creating demand for sophisticated solutions. However, the market faces significant restraints, including the immensely high initial capital expenditure required for building and equipping state-of-the-art data centers, which can be a barrier for smaller enterprises. Concerns regarding substantial energy consumption and the associated environmental impact are also pressing, prompting operators to seek more sustainable solutions but also adding to design and operational complexity. Moreover, the increasing complexity of managing diverse infrastructure components, coupled with a shortage of skilled personnel, poses operational challenges. Opportunities abound for innovation, particularly in the development of green data centers powered by renewable energy, modular data center designs that offer rapid deployment and scalability, and advanced AI-driven management tools that optimize resource utilization and predictive maintenance. The growing demand for specialized infrastructure to support high-performance computing (HPC) and AI workloads presents a lucrative niche. Impact forces on the market are multifaceted, with technological advancements continually reshaping infrastructure capabilities and efficiency, from advanced cooling techniques to next-generation networking. The evolving regulatory landscape, particularly around data governance and environmental standards, significantly influences design and operational practices. Economic shifts, including global growth rates and investment cycles, directly affect spending on new data center projects. Geopolitical stability and supply chain resilience also play a critical role, influencing equipment availability and pricing, thereby impacting market dynamics and strategic planning for data center operators worldwide.

The Data Center Infrastructure Market is comprehensively segmented to provide a detailed understanding of its diverse components and applications. This segmentation allows for precise market analysis, identifying key trends and growth opportunities across various technological offerings, types of data centers, service tiers, and end-user industries. The market's complexity necessitates a granular view to address the specific needs and challenges faced by different stakeholders, from component manufacturers to service providers and end-users. Each segment reflects unique demand patterns, technological preferences, and investment considerations, contributing distinctly to the overall market landscape. Understanding these segments is crucial for strategic planning, product development, and market entry decisions for businesses operating within or looking to enter the data center infrastructure space.

The segmentation extends across various dimensions, including the type of hardware and software solutions, the model of data center deployment, the level of redundancy and uptime required, and the specific vertical industries leveraging these infrastructures. This multi-dimensional approach highlights the market's adaptability and the specialized nature of solutions required to meet the stringent demands of modern digital operations. For instance, the needs of a hyperscale cloud provider differ significantly from those of an enterprise running mission-critical applications or an edge computing facility supporting real-time IoT analytics. Consequently, this detailed segmentation is instrumental in deciphering the intricate dynamics of supply and demand, technological innovation, and competitive positioning across the expansive data center infrastructure ecosystem.

The value chain of the Data Center Infrastructure Market is a complex ecosystem involving multiple stages, from raw material suppliers to end-users, with distinct players at each level contributing to the final delivery of comprehensive data center solutions. At the upstream end, the value chain begins with suppliers of critical components such as semiconductor manufacturers, metal fabricators for racks and enclosures, and chemical companies for cooling fluids. These suppliers provide the foundational materials and advanced chips that are integrated into various infrastructure components. Moving further along, component manufacturers specialize in producing power systems (UPS, PDUs), cooling units (CRAC/CRAH, chillers), networking hardware (switches, routers, cabling), and security systems. These manufacturers often engage in extensive research and development to innovate and meet evolving industry standards for efficiency, performance, and reliability. Integration and assembly then transform these disparate components into functional units and complete data center systems. This stage often involves systems integrators who design and configure solutions tailored to specific client requirements, ensuring compatibility and optimal performance of all interconnected parts. The distribution channels for data center infrastructure are multifaceted, encompassing direct sales from manufacturers to large hyperscale or enterprise clients, indirect sales through a network of distributors and resellers, and value-added resellers (VARs) who bundle products with their own services. Direct sales are common for large-scale projects where bespoke solutions and close collaboration are required, while indirect channels cater to a broader market, offering specialized expertise and localized support. Downstream activities involve the deployment, installation, and ongoing maintenance of the data center infrastructure. This includes construction companies specializing in data center facilities, professional services for installation, and managed service providers who handle the day-to-day operations and upkeep of the infrastructure. The direct buyers of these integrated solutions are typically large enterprises, cloud service providers, and colocation operators, while indirect beneficiaries include businesses and consumers who rely on the digital services hosted within these data centers. The efficiency and effectiveness of this entire value chain are critical for ensuring the timely delivery, reliable operation, and continuous evolution of data center capabilities globally.

The Data Center Infrastructure Market serves a diverse and expanding base of potential customers, each with unique requirements and operational scales, underscoring the universal need for robust digital foundations. Foremost among these are large enterprises across all industry verticals, including BFSI, healthcare, manufacturing, and retail, which operate their own private data centers to host mission-critical applications, manage proprietary data, and ensure compliance with stringent industry regulations. These organizations seek high-performance, secure, and scalable infrastructure solutions that can support their internal IT operations, data analytics, and digital transformation initiatives, often prioritizing reliability and customization. Another significant segment comprises hyperscale cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, which build and operate massive data centers to offer Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) to millions of global customers. Their demand focuses on extreme scalability, energy efficiency, automation, and highly standardized components to achieve massive economies of scale. Colocation service providers represent another crucial customer group, offering shared data center space, power, cooling, and connectivity to multiple tenants. Businesses that choose colocation often do so to reduce capital expenditure, benefit from specialized data center management, and access premium network connectivity. Their infrastructure needs are centered around modularity, multi-tenancy support, and robust physical security. Furthermore, telecommunication companies are major buyers, investing in data center infrastructure to support their core network operations, mobile services, and the rollout of 5G technology, which inherently requires distributed processing capabilities and edge computing facilities. Emerging customer segments include smaller businesses and startups leveraging hosted or hybrid cloud solutions, and organizations involved in specialized fields like scientific research, government defense, and media production, all requiring significant computational power and storage. The increasing prevalence of edge computing is also creating a new class of potential customers, particularly in industries like smart manufacturing, IoT, and autonomous systems, which require localized data processing closer to the data source to minimize latency and improve real-time decision-making. These varied customer profiles collectively drive the continuous innovation and expansion of the Data Center Infrastructure Market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $65.8 Billion |

| Market Forecast in 2032 | $132.5 Billion |

| Growth Rate | CAGR 10.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Equinix, Digital Realty, Vantage Data Centers, CyrusOne, NTT Global Data Centers, CoreSite, Iron Mountain, Switch, QTS Realty Trust, Google (Google Cloud), Amazon (AWS), Microsoft (Azure), IBM, Cisco Systems, Hewlett Packard Enterprise (HPE), Dell Technologies, Huawei, Eaton, Schneider Electric, Vertiv |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Data Center Infrastructure Market is characterized by a rapidly evolving technological landscape, driven by the relentless pursuit of higher efficiency, greater scalability, enhanced reliability, and reduced operational costs. One of the most critical technologies is advanced cooling solutions, moving beyond traditional air-based systems to accommodate the escalating heat densities from modern high-performance computing (HPC) and AI workloads. This includes widespread adoption of liquid cooling, such as direct-to-chip cooling, immersion cooling, and rear-door heat exchangers, which are significantly more efficient at dissipating heat. Power management technologies are also central, with innovations in Uninterruptible Power Supply (UPS) systems, intelligent Power Distribution Units (PDUs), and energy storage solutions like lithium-ion batteries, all designed to ensure continuous operation and optimize power utilization. Furthermore, the integration of renewable energy sources and microgrids is becoming a key trend for sustainable and resilient data centers. In the networking domain, high-speed, low-latency interconnects are paramount, with technologies like 400 Gigabit Ethernet (400GbE) and InfiniBand becoming standard for intra-data center communication to support massive data transfers required by AI and big data analytics. Software-defined networking (SDN) and network function virtualization (NFV) are also gaining traction, offering greater flexibility and automation in network management. Data Center Infrastructure Management (DCIM) software plays a crucial role, providing comprehensive monitoring, management, and orchestration capabilities for power, cooling, space, and asset utilization. These platforms integrate AI and machine learning algorithms for predictive maintenance, anomaly detection, and capacity planning, transforming reactive operations into proactive management. Physical security technologies, including biometric access control, advanced surveillance systems, and environmental sensors, are continually advancing to protect critical assets. The adoption of modular and prefabricated data center designs is another significant technological shift, enabling rapid deployment, scalability, and enhanced energy efficiency through standardized, factory-built components. Moreover, the emergence of specialized hardware for AI, such as Graphics Processing Units (GPUs) and Application-Specific Integrated Circuits (ASICs), is influencing server and rack design, pushing the boundaries of traditional infrastructure to support specialized computing needs. These technological advancements collectively define the cutting-edge capabilities and future direction of the data center infrastructure market.

Primary components include power infrastructure (UPS, PDUs), cooling systems (CRAC/CRAH, chillers), networking equipment (switches, routers, cabling), physical security systems, and Data Center Infrastructure Management (DCIM) software for operational oversight.

AI significantly impacts data center design by increasing power density and heat generation, driving demand for advanced liquid cooling solutions and high-bandwidth networks. Operationally, AI is used for predictive maintenance, resource optimization, and energy management, enhancing efficiency and reliability.

Edge computing extends data processing closer to the data source, reducing latency and bandwidth usage. It drives demand for smaller, distributed data centers with robust infrastructure to support real-time applications like IoT, autonomous vehicles, and local AI processing.

Key sustainability trends include the adoption of renewable energy sources, energy-efficient cooling and power systems, optimization through DCIM software, modular designs for reduced construction waste, and carbon footprint reduction strategies.

North America and Europe are mature markets with high investment in hyperscale and advanced technologies. Asia Pacific is the fastest-growing region, driven by rapid digitalization, cloud adoption, and significant infrastructure development in countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.