ID : MRU_ 428018 | Date : Oct, 2025 | Pages : 249 | Region : Global | Publisher : MRU

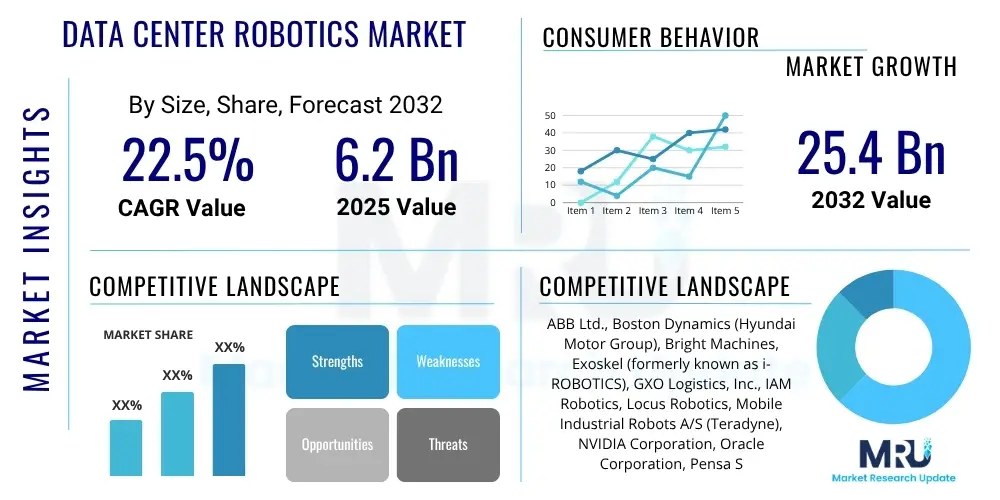

The Data Center Robotics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2032. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 25.4 Billion by the end of the forecast period in 2032.

The Data Center Robotics Market encompasses the development, deployment, and integration of automated robotic systems designed to operate within data center environments. These robots are engineered to perform a wide array of tasks, ranging from physical security patrols and environmental monitoring to complex asset management, server installation, and maintenance operations. The primary objective is to enhance operational efficiency, reduce human error, improve response times, and optimize resource utilization within increasingly complex and geographically dispersed data center infrastructures. As digital transformation accelerates globally, the demand for robust, scalable, and autonomous data center operations has become paramount, driving the adoption of specialized robotic solutions.

Products within this market include various types of robots such as Autonomous Mobile Robots (AMRs) for navigation and transport, robotic arms for precise manipulation of hardware, and drone-based systems for aerial inspection and monitoring. Major applications span inventory management, where robots track and locate assets; security, providing continuous surveillance and threat detection; and facilities management, involving tasks like power and cooling system checks or server rack integrity assessments. The benefits are multifold, including significant reductions in operational expenditure, minimized downtime through proactive maintenance, enhanced physical security protocols, and the ability to operate in challenging or hazardous conditions without human intervention, ensuring business continuity and data integrity.

Driving factors for the market's robust growth are directly tied to the exponential increase in data generation and consumption, necessitating larger, more efficient, and resilient data centers. The escalating costs of manual labor, coupled with the scarcity of skilled technicians in remote or specialized data center locations, further propel the need for automation. Additionally, the continuous push for greater energy efficiency, higher uptime SLAs, and enhanced security measures across cloud, edge, and on-premise data center deployments are key contributors to the expanding adoption of robotic solutions, transforming traditional data center management paradigms into highly automated, intelligent operations.

The Data Center Robotics Market is experiencing rapid expansion, driven by an urgent need for operational efficiency and automation across the global digital infrastructure landscape. Key business trends indicate a strong shift towards intelligent automation solutions that integrate seamlessly with existing data center management platforms, leveraging AI and machine learning for predictive capabilities and autonomous decision-making. Companies are increasingly investing in robotics to overcome challenges such as escalating operational costs, the complexity of managing vast server farms, and the persistent shortage of specialized IT personnel. This strategic shift is not just about replacing human tasks but augmenting human capabilities, allowing skilled professionals to focus on higher-value activities while routine and repetitive tasks are handled by autonomous systems, leading to more resilient and agile data center operations.

Regionally, North America and Europe are leading the adoption curve, characterized by early investments in advanced data center technologies and a strong presence of hyperscale cloud providers and large enterprises. However, the Asia Pacific region, particularly China, India, and Japan, is emerging as a significant growth engine, fueled by massive digital transformation initiatives, expanding internet penetration, and substantial government and private sector investments in new data center construction. Latin America, the Middle East, and Africa are also showing promising growth, albeit from a smaller base, as these regions modernize their IT infrastructures and embrace cloud computing, necessitating more efficient and scalable data center operations that robotics can provide.

Segmentation trends within the market highlight the growing prominence of Autonomous Mobile Robots (AMRs) for logistics and surveillance, alongside specialized robotic arms for intricate hardware handling and maintenance. End-user segments such as hyperscale data centers and colocation facilities are primary beneficiaries, given their sheer scale and need for continuous, uninterrupted operation. Enterprises are also increasingly exploring modular and smaller-scale robotic deployments to manage their on-premise or edge data center facilities. This diversification across robot types and end-user applications underscores the market's maturity and its ability to offer tailored solutions for diverse operational requirements, indicating a broad and sustained growth trajectory across all key segments as the digital economy continues its rapid expansion.

Common user questions regarding the impact of Artificial Intelligence on the Data Center Robotics Market frequently revolve around how AI can enhance the autonomy, intelligence, and efficiency of these robotic systems. Users are keenly interested in the extent to which AI can enable robots to perform more complex tasks, adapt to dynamic environments, and make autonomous decisions without human intervention. Concerns often include the reliability and safety of AI-driven robots, the potential for job displacement, and the integration challenges with existing data center infrastructure. There's also a strong curiosity about AI's role in predictive maintenance, anomaly detection, and optimizing energy consumption, signaling a desire for smarter, self-optimizing data center operations. The overarching expectation is that AI will transform robots from mere automated tools into intelligent, adaptive co-workers capable of profoundly impacting data center performance and operational resilience.

The integration of AI is expected to significantly elevate the capabilities of data center robotics, moving them beyond predefined programmed tasks to intelligent, adaptive operations. AI algorithms provide robots with the ability to learn from their environment, recognize patterns, and anticipate potential issues, thereby transforming reactive maintenance into proactive interventions. This shift is crucial for maintaining the high availability and performance standards demanded by modern data centers. Furthermore, AI-powered computer vision and sensor fusion allow robots to navigate complex data center layouts more efficiently, identify misplaced or faulty equipment with greater accuracy, and even manage inventory dynamically, adapting to real-time changes in server racks and facility conditions. The ability of AI to process vast amounts of operational data enables robots to contribute to a more holistic understanding of data center health and performance.

Moreover, AI plays a pivotal role in optimizing energy consumption within data centers. By analyzing temperature, airflow, and power usage patterns, AI-enabled robots can identify inefficiencies and suggest or even execute adjustments to cooling systems or server loads, contributing significantly to sustainability goals. The predictive analytics capabilities of AI are instrumental in foreseeing equipment failures, allowing robots to perform preventive maintenance or alert human operators, thereby minimizing downtime. As data centers continue to grow in scale and complexity, the symbiotic relationship between AI and robotics becomes increasingly vital for achieving autonomous, resilient, and energy-efficient operations. This synergy not only addresses current operational challenges but also paves the way for future innovations in automated data center management, ensuring that data centers can meet the escalating demands of the digital era.

The Data Center Robotics Market is profoundly influenced by a complex interplay of drivers, restraints, and opportunities that shape its growth trajectory. Key drivers include the exponential growth in global data traffic and the increasing demand for data storage and processing, which necessitate more efficient, scalable, and automated data center operations. The rising operational costs associated with traditional manual management, coupled with the critical need for 24/7 uptime and enhanced security, further compel data center operators to invest in robotic solutions. Moreover, the scarcity of skilled labor in remote data center locations and the inherent risks of human error in complex environments are significant factors pushing for greater automation. The quest for higher energy efficiency and sustainability also acts as a powerful driver, as robots can optimize cooling and power distribution with precision, reducing the carbon footprint of data centers.

However, the market faces notable restraints that could temper its expansion. The high initial capital investment required for purchasing and integrating advanced robotic systems is a primary barrier for many organizations, especially small to medium-sized data centers. The complexity of integrating these new robotic solutions with existing legacy infrastructure and diverse software platforms poses significant technical challenges. Concerns regarding data security and potential vulnerabilities introduced by automated systems, alongside the psychological and social impacts of job displacement among data center personnel, also represent considerable hurdles. Furthermore, regulatory complexities and the absence of standardized protocols for robotic operations within highly sensitive data environments can delay adoption and increase compliance costs, creating friction in the deployment process.

Despite these challenges, substantial opportunities exist for market participants. The rapid growth of edge computing and 5G networks, which require distributed and highly automated micro-data centers, presents a fertile ground for specialized robotic applications. The development of more collaborative robots (cobots) that can work safely alongside humans offers a pathway for gradual integration and addresses some job displacement concerns. Advancements in artificial intelligence, machine learning, and sensor technologies are continuously improving robot capabilities, making them more versatile and cost-effective. Furthermore, the increasing demand for specialized services such as robotic-as-a-service (RaaS) models, which lower upfront investment and operational burden, are opening new avenues for market penetration. The ongoing emphasis on disaster recovery and business continuity planning also underscores the value of autonomous robotic systems in maintaining critical infrastructure operations, especially in challenging situations, solidifying their long-term market potential.

The Data Center Robotics Market is meticulously segmented to provide a comprehensive understanding of its diverse components and growth avenues. This segmentation allows for targeted analysis of different robotic technologies, their specific applications, and the various end-user profiles that benefit from these advanced solutions. The market can be broadly categorized by robot type, offering insights into the adoption rates of mobile robots versus stationary manipulators; by application, detailing the operational areas where robots provide the most significant value; and by end-user, differentiating between the needs of hyperscale facilities, colocation centers, and enterprise data environments. Each segment represents a unique demand landscape influenced by distinct operational requirements, technological advancements, and investment capacities, providing a granular view of market dynamics and potential for innovation.

Further granularity in segmentation often includes parameters such as component type, distinguishing between hardware (robot platforms, sensors, actuators) and software (AI/ML algorithms, control systems, integration platforms); deployment model, differentiating between on-premise solutions and cloud-based robotic management; and the level of autonomy, categorizing robots from semi-autonomous to fully autonomous systems. This detailed breakdown aids market players in developing tailored products and services that address specific needs within the data center ecosystem, from enhancing physical security through patrol robots to optimizing server management with robotic arms. Understanding these segmentations is critical for strategic planning, product development, and identifying untapped market niches, driving the overall growth and maturation of the data center robotics industry as it responds to evolving technological landscapes and operational demands across the globe.

The value chain for the Data Center Robotics Market is a multi-faceted ecosystem that begins with upstream activities involving research, development, and the manufacturing of core robotic components. This initial stage includes suppliers of specialized sensors, advanced actuators, high-performance processors, AI chips, and robotic operating system (ROS) software developers. These upstream providers are critical for driving innovation in areas such as precision navigation, object recognition, and human-robot interaction. Further upstream are raw material suppliers and specialized electronic component manufacturers, whose quality and cost efficiency directly impact the final product. The robust intellectual property developed at this stage, particularly in AI and advanced materials, is a key differentiator and a source of competitive advantage for robot manufacturers.

Moving through the value chain, the core activities involve the design, assembly, and integration of these components into complete robotic systems. This midstream segment includes robot manufacturers who specialize in building robots specifically tailored for data center environments, ensuring they meet stringent requirements for electromagnetic compatibility, temperature resilience, and operational precision. These manufacturers often collaborate with software developers to embed sophisticated AI and machine learning algorithms, enabling autonomous decision-making and real-time data analysis. Downstream activities focus on the distribution, deployment, and ongoing support of these robotic solutions. Distribution channels include direct sales teams for large-scale enterprise deployments, as well as indirect channels through system integrators, value-added resellers (VARs), and technology partners who provide localized expertise and support. These partners are crucial for customizing solutions to specific data center architectures and ensuring seamless integration with existing IT infrastructure, including Data Center Infrastructure Management (DCIM) systems.

The final stages of the value chain encompass post-sales services, which are paramount for ensuring customer satisfaction and long-term market penetration. This includes installation, configuration, maintenance, training, and continuous software updates. The direct channel offers a direct line of communication between the manufacturer and the end-user, facilitating immediate feedback and faster resolution of issues. However, the indirect channel, through a network of service providers, can offer broader market reach and specialized support, particularly for complex deployments or in geographically diverse regions. The emergence of Robotics-as-a-Service (RaaS) models further diversifies the distribution and consumption patterns, allowing data center operators to access robotic capabilities on a subscription basis, reducing upfront capital expenditure and shifting towards operational expenditure. This entire value chain emphasizes collaboration, technological innovation, and robust service delivery to maximize the efficiency and impact of robotics within the data center ecosystem, ultimately delivering value to the end-users by enhancing data center performance and reliability.

Potential customers for the Data Center Robotics Market are primarily organizations that own, operate, or manage large-scale digital infrastructures, where efficiency, uptime, and security are paramount. This includes a broad spectrum of entities, starting with hyperscale cloud service providers such as Amazon Web Services, Google Cloud, Microsoft Azure, and Meta. These companies manage vast global networks of data centers, often requiring thousands of servers and complex cooling systems, making them ideal candidates for automated solutions that can optimize resource allocation, perform predictive maintenance, and enhance physical security across their expansive facilities. The sheer volume of assets and the continuous need for expansion and upgrades within these environments create a compelling business case for robotic integration, significantly reducing operational expenditure and manual intervention.

Another significant segment of potential customers includes colocation data center providers, who host IT infrastructure for multiple clients. Companies like Equinix, Digital Realty, and CyrusOne can leverage robotics to offer enhanced services to their tenants, including faster hardware deployments, more accurate asset tracking, and improved security surveillance, thereby differentiating their offerings in a highly competitive market. Robotics can help these providers manage their diverse client requirements more efficiently, ensuring compliance with strict service level agreements (SLAs) and providing better transparency in asset management. The ability to automate routine tasks frees up their human staff to focus on higher-value client interactions and complex problem-solving, leading to improved customer satisfaction and operational scalability without commensurate increases in human labor costs.

Furthermore, large enterprises with their own on-premise data centers, particularly those in sectors like finance, telecommunications, manufacturing, and healthcare, represent a growing customer base. These organizations often have mission-critical data and applications that demand the highest levels of reliability and security. Robotic solutions can assist in maintaining compliance, conducting automated audits, and performing environmental monitoring to ensure optimal operating conditions. As edge computing proliferates, smaller, distributed data centers requiring autonomous management will also become key customers. Government agencies, research institutions, and defense organizations with secure data facilities also stand to benefit from the enhanced security and operational resilience offered by data center robotics, making them a diverse and expanding market for these advanced automation solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2032 | USD 25.4 Billion |

| Growth Rate | 22.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Boston Dynamics (Hyundai Motor Group), Bright Machines, Exoskel (formerly known as i-ROBOTICS), GXO Logistics, Inc., IAM Robotics, Locus Robotics, Mobile Industrial Robots A/S (Teradyne), NVIDIA Corporation, Oracle Corporation, Pensa Systems, Rocos (acquired by Robot Operating System), Sarcos Technology and Robotics Corporation, Schneider Electric SE, Supermicro Computer, Inc., Symbio Robotics, The FANUC Corporation, Tompkins Robotics, Vecna Robotics, Yaskawa Electric Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Data Center Robotics Market is underpinned by a sophisticated array of technologies that enable autonomous operation, intelligent decision-making, and seamless integration within complex data center environments. At the core, advanced robotics hardware forms the foundation, including highly precise actuators, motors, and robust chassis designed to navigate challenging industrial settings. Lidar sensors, depth cameras (e.g., Intel RealSense, Microsoft Azure Kinect), ultrasonic sensors, and Inertial Measurement Units (IMUs) are crucial for perception, allowing robots to accurately map their surroundings, detect obstacles, and localize themselves within the data center. Furthermore, specialized end-effectors and grippers are engineered to safely handle sensitive IT equipment, from server blades to network cables, without causing damage, demanding high levels of dexterity and force control.

Software and artificial intelligence (AI) constitute the brain of data center robots. Robotics Operating System (ROS) and its commercial variants provide a flexible framework for developing and deploying robotic applications, facilitating communication between different hardware and software components. AI and machine learning algorithms are indispensable for enabling autonomous navigation, object recognition, predictive maintenance, and complex task execution. Computer vision systems, powered by deep learning, allow robots to identify specific server models, read asset tags, and detect visual anomalies such as overheating components or cable disarray. Reinforcement learning is increasingly used to train robots for optimal task sequences and adaptive behaviors, ensuring they can operate efficiently in dynamic and evolving data center layouts, learning from experience and continuous data streams.

Connectivity and integration technologies are also pivotal. High-speed, low-latency wireless communication protocols like Wi-Fi 6, 5G, and dedicated mesh networks ensure reliable data exchange between robots, central control systems, and human operators. Integration with Data Center Infrastructure Management (DCIM) software, Building Management Systems (BMS), and IT Service Management (ITSM) platforms is essential for robots to receive tasks, report status, and contribute to a holistic view of data center operations. Cloud computing infrastructure often supports the processing of vast amounts of sensor data and the execution of complex AI models, particularly for fleet management and analytical insights. Furthermore, advanced cybersecurity measures are embedded into these systems to protect against unauthorized access and ensure the integrity of robotic operations, reflecting the critical nature of data center security.

Data centers primarily employ Autonomous Mobile Robots (AMRs) for navigation, surveillance, and transport, and robotic arms for precise manipulation of hardware. Tasks include physical security patrols, environmental monitoring, asset tracking, server installation, maintenance, and logistics, aiming to enhance efficiency and reduce human intervention in routine or hazardous operations.

Robots enhance efficiency by automating repetitive tasks, reducing human error, and operating 24/7 without fatigue. They offer cost savings through optimized labor allocation, decreased downtime via predictive maintenance, improved energy efficiency from precise environmental controls, and reduced operational expenditures compared to manual processes in large-scale facilities.

Key challenges include the high initial capital investment, the complexity of integrating new robotic systems with legacy infrastructure and diverse DCIM software, ensuring data security and network integrity, addressing potential job displacement concerns, and navigating the absence of standardized protocols for robotic operations in sensitive environments.

AI significantly enhances robotic capabilities by enabling autonomous navigation, predictive maintenance through data analysis, optimized resource management, intelligent security monitoring (e.g., facial recognition, anomaly detection), and adaptive task execution. This allows robots to learn, make informed decisions, and operate more efficiently and flexibly without constant human oversight.

The future outlook for human-robot collaboration in data centers is highly positive, with increasing development of collaborative robots (cobots) designed to work safely alongside human technicians. This synergy will allow robots to handle routine, dangerous, or physically demanding tasks, while humans focus on complex problem-solving, strategic planning, and critical decision-making, leading to a more productive, safer, and efficient workforce.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.