ID : MRU_ 429279 | Date : Oct, 2025 | Pages : 257 | Region : Global | Publisher : MRU

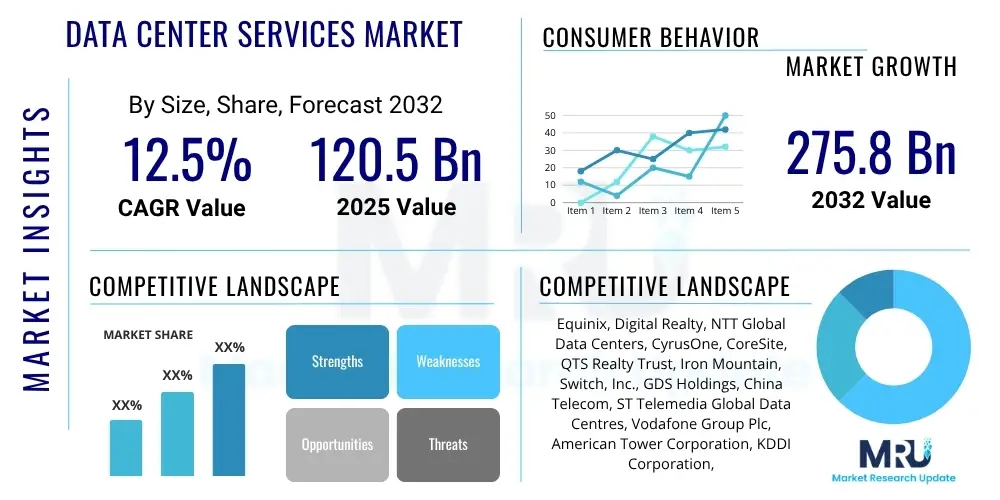

The Data Center Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2032. The market is estimated at USD 120.5 billion in 2025 and is projected to reach USD 275.8 billion by the end of the forecast period in 2032.

The Data Center Services Market encompasses a wide array of offerings designed to support the operational and strategic needs of modern businesses, ranging from colocation and managed hosting to cloud and hyperscale solutions. These services provide essential infrastructure, connectivity, and technical expertise, allowing organizations to store, process, and manage vast amounts of data efficiently and securely. With the escalating demands of digital transformation, cloud adoption, and the proliferation of data-intensive applications, data center services have become indispensable for maintaining business continuity and fostering innovation across nearly every industry sector.

Major applications for data center services span across diverse industries, including Banking, Financial Services, and Insurance (BFSI), IT and Telecommunications, Healthcare, Government, Retail, and Energy. Benefits derived from these services are multifaceted, encompassing enhanced scalability, improved disaster recovery capabilities, reduced operational expenditures, and access to advanced security protocols and compliance frameworks. These advantages allow businesses to focus on their core competencies while relying on specialized providers for critical infrastructure management. The market's growth is primarily driven by the exponential increase in data generation, the pervasive trend of digitalization across enterprises, and the continuous migration of workloads to cloud environments, necessitating robust and agile data center infrastructure.

The Data Center Services Market is experiencing robust expansion, characterized by significant business trends such as the increasing demand for hybrid cloud solutions and the strategic investments in edge computing infrastructure. Enterprises are increasingly seeking flexible and scalable data center models that can accommodate fluctuating data demands and support geographically dispersed operations. This shift is driving innovation in service offerings, pushing providers to deliver more specialized and value-added services beyond basic infrastructure. The emphasis on sustainability and energy efficiency within data center operations is also becoming a critical business imperative, influencing design, technology adoption, and operational practices across the industry.

Regionally, North America and Europe continue to dominate the market due to early adoption of advanced technologies, presence of major cloud providers, and substantial enterprise digitalization efforts. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by rapid industrialization, burgeoning digital economies, and increasing investments in IT infrastructure across countries like China, India, and Southeast Asia. Latin America, the Middle East, and Africa (MEA) are also emerging as significant markets, driven by improving internet penetration, government initiatives for digital transformation, and the expansion of local and international businesses requiring robust data infrastructure. Each region presents unique opportunities and challenges, influencing deployment strategies and partnership models among market players.

In terms of segment trends, colocation services remain a foundational component, offering cost-effective and secure environments for enterprises to house their own IT equipment. Managed services are witnessing accelerated growth as businesses increasingly outsource complex data center operations to specialized providers, seeking expertise in areas such as network management, security, and disaster recovery. The hyperscale segment, driven by the massive infrastructure demands of cloud giants and large-scale digital platforms, continues its rapid expansion. Furthermore, the rising adoption of Artificial Intelligence (AI) and Machine Learning (ML) technologies is profoundly impacting demand, necessitating higher power densities and specialized cooling solutions within data centers to support intensive computational workloads.

Common user questions regarding AI's impact on the Data Center Services Market frequently revolve around how AI will reshape infrastructure requirements, operational efficiency, and security protocols. Users are keen to understand the implications of AI's immense computational demands on existing data center capacities, including power consumption, cooling solutions, and network bandwidth. Concerns also extend to how AI can be leveraged to automate data center operations, predict maintenance needs, and enhance overall efficiency. Furthermore, there is considerable interest in the security implications, specifically how AI can both bolster defenses against cyber threats and potentially introduce new vulnerabilities within highly complex data center environments. The overarching theme is a desire to comprehend AI's dual role as a driver of demand for more sophisticated data center services and as a tool for optimizing their delivery.

AI's influence on the Data Center Services Market is profound and multi-faceted, acting as a catalyst for significant advancements and increased demand. The need for specialized hardware such as GPUs and high-performance computing (HPC) clusters to train and deploy AI models is driving the adoption of high-density racks and advanced cooling technologies like liquid cooling. This shift necessitates data centers that are not only larger but also more adaptable and energy-efficient to manage the unprecedented heat generation and power consumption associated with AI workloads. Furthermore, AI is being integrated into data center management systems to optimize energy usage, predict potential hardware failures, and automate routine operational tasks, leading to substantial improvements in efficiency and reliability.

Moreover, the integration of AI is fostering the development of new service offerings tailored to machine learning workloads, including AI-as-a-Service and specialized colocation facilities for AI research and development. This creates new revenue streams for data center providers and allows enterprises to access cutting-performance infrastructure without the prohibitive capital expenditure. The increased reliance on AI also escalates the importance of robust cybersecurity measures, as AI models and the vast datasets they process become attractive targets for malicious actors. Data center operators are consequently investing in AI-driven security tools and advanced threat detection systems to safeguard critical assets, positioning data security as a paramount concern in the evolving AI landscape.

The Data Center Services Market is propelled by several key drivers, primarily the exponential growth in global data generation, driven by the proliferation of IoT devices, social media, and digital content. Concurrently, the accelerating pace of digital transformation across industries mandates robust and scalable IT infrastructure, pushing enterprises towards data center service providers. The widespread adoption of cloud computing models, encompassing public, private, and hybrid clouds, further fuels demand as businesses increasingly offload their computing and storage needs to external providers. These factors collectively create a strong impetus for market expansion, requiring continuous innovation in service offerings and infrastructure capabilities.

Despite significant growth, the market faces notable restraints. The substantial capital expenditure required for building and maintaining state-of-the-art data centers, including land acquisition, power infrastructure, and advanced cooling systems, presents a significant barrier to entry and expansion. Data security concerns, particularly regarding sensitive enterprise and customer information, remain a critical challenge, demanding continuous investment in advanced cybersecurity measures and compliance with evolving data protection regulations. Regulatory compliance, such as GDPR and regional data residency laws, adds complexity and cost, forcing providers to adapt their services and geographical footprint to meet stringent requirements.

Opportunities within the market are abundant, particularly with the rise of edge computing, which brings data processing closer to the source, reducing latency and enabling real-time applications. The integration of Artificial Intelligence (AI) and Machine Learning (ML) workloads is creating a demand for specialized high-performance data center facilities capable of handling intensive computational tasks. Furthermore, the increasing preference for hybrid cloud solutions allows businesses to leverage the flexibility of public clouds while maintaining control over critical data on-premises or in private cloud environments, presenting a nuanced opportunity for service providers to offer integrated solutions. These opportunities are shaping the future trajectory of the market, encouraging innovation and strategic partnerships.

The Data Center Services Market is comprehensively segmented to cater to the diverse needs of enterprises across various operational and technological requirements. These segments allow for a detailed analysis of market dynamics, consumer preferences, and competitive landscapes, providing valuable insights into specific growth areas and strategic opportunities. The segmentation covers different types of services, organizational sizes, deployment models, and the broad range of end-user industries that utilize data center capabilities.

The value chain for the Data Center Services Market is intricate, beginning with upstream suppliers of critical components such as hardware manufacturers (servers, storage, networking equipment), power infrastructure providers (UPS, generators), and cooling system developers. These foundational elements are essential for constructing and maintaining the physical data center facilities. Software vendors providing operating systems, virtualization platforms, and data center infrastructure management (DCIM) tools also form a crucial part of the upstream segment, enabling the efficient operation and orchestration of the underlying infrastructure. The quality and innovation from these upstream suppliers directly impact the capabilities and reliability of the data center services offered downstream.

Midstream activities involve the data center service providers themselves, who design, build, operate, and market their facilities and services. This includes site selection, architectural design, procurement of hardware and software, network connectivity provisioning, and the establishment of robust security and compliance frameworks. These providers offer various services like colocation, managed hosting, cloud services (IaaS, PaaS, SaaS), and specialized solutions for AI/ML workloads or edge computing. Their role is to integrate the diverse upstream components into a cohesive, reliable, and scalable service offering that meets the complex demands of their clientele.

Downstream, the value chain extends to the end-users and their distribution channels. Data center services are primarily distributed through direct sales channels, where service providers engage directly with large enterprises and hyperscale clients to tailor solutions. Indirect channels include partnerships with system integrators, value-added resellers (VARs), and managed service providers (MSPs) who bundle data center services with their own offerings, catering to SMEs and specific industry verticals. These channels are crucial for reaching a broader market and providing integrated solutions that encompass not just infrastructure but also applications and business process optimization. The effectiveness of these channels directly influences market penetration and customer acquisition.

The potential customer base for Data Center Services is remarkably broad and continues to expand across virtually all sectors of the modern economy. At the core, any organization that generates, processes, or stores significant amounts of digital data is a prime candidate. This includes small and medium-sized enterprises (SMEs) seeking to reduce IT overheads and leverage professional infrastructure without large capital investments, as well as large enterprises that require scalable, resilient, and geographically dispersed data center capabilities to support their global operations and digital transformation initiatives. The rapid acceleration of cloud adoption and the increasing complexity of IT environments mean that even companies with existing on-premises infrastructure are increasingly looking to hybrid models, driving demand for external data center services.

Key industries represent substantial segments of potential customers. The Banking, Financial Services, and Insurance (BFSI) sector, for instance, requires highly secure, compliant, and reliable data centers for transaction processing, data analytics, and regulatory reporting. IT and Telecommunications companies are both providers and major consumers of data center services, utilizing them for network infrastructure, cloud platforms, and supporting various digital communication channels. The Healthcare industry relies on data centers for electronic health records (EHR), medical imaging, and research data, prioritizing data privacy and regulatory adherence. Government and public sector entities also leverage these services for citizen data, national security, and various e-governance initiatives, emphasizing data sovereignty and robust security.

Furthermore, emerging and rapidly growing sectors contribute significantly to the customer landscape. The Retail and E-commerce industry depends on data centers for online transaction processing, inventory management, customer relationship management, and sophisticated analytics to personalize consumer experiences. Manufacturing companies are increasingly adopting Industry 4.0 initiatives, requiring data centers for IoT data processing, predictive maintenance, and operational technology (OT) integration. Media and Entertainment companies utilize data centers for content delivery, streaming services, and large-scale digital asset management. Essentially, any entity facing challenges in managing escalating data volumes, ensuring business continuity, enhancing cybersecurity, or seeking cost-effective scalability will find value in leveraging external data center services, making the market highly diversified in its clientele.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 120.5 billion |

| Market Forecast in 2032 | USD 275.8 billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Equinix, Digital Realty, NTT Global Data Centers, CyrusOne, CoreSite, QTS Realty Trust, Iron Mountain, Switch, Inc., GDS Holdings, China Telecom, ST Telemedia Global Data Centres, Vodafone Group Plc, American Tower Corporation, KDDI Corporation, Telefonica S.A., Tata Communications, OVHcloud, Alibaba Cloud, Amazon Web Services, Microsoft Azure |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Data Center Services Market is continuously evolving, driven by advancements in core technologies that enhance efficiency, scalability, and security. Critical infrastructure technologies include high-performance servers, storage solutions (flash, hybrid, object storage), and advanced networking equipment (Software-Defined Networking - SDN, Network Function Virtualization - NFV) that enable flexible and agile resource allocation. Power and cooling innovations, such as liquid cooling systems, free cooling, and intelligent power distribution units (PDUs), are crucial for managing the increasing heat density from high-performance computing (HPC) and AI workloads, while simultaneously improving energy efficiency and reducing operational costs. These foundational elements ensure the physical and virtual resilience of data center environments.

Software and automation platforms play an equally vital role in modern data centers. Data Center Infrastructure Management (DCIM) software provides comprehensive monitoring and management of IT and facility assets, power, and cooling systems, offering real-time insights for optimization. Cloud management platforms facilitate the orchestration of resources across hybrid and multi-cloud environments, ensuring seamless integration and workload mobility. Automation tools, often augmented by Artificial Intelligence (AI) and Machine Learning (ML), are increasingly deployed for predictive maintenance, resource provisioning, and security incident response, significantly reducing human intervention and improving reliability. These technologies are instrumental in enabling the highly automated, self-healing, and intelligent data centers of the future.

Security and connectivity technologies are paramount for protecting critical data and ensuring uninterrupted access. Advanced cybersecurity solutions, including next-generation firewalls, intrusion detection/prevention systems (IDPS), data encryption, and identity and access management (IAM), are integral to defending against sophisticated cyber threats. Connectivity relies on high-speed, low-latency fiber optic networks, often incorporating direct cloud interconnects and content delivery networks (CDNs) to ensure robust and efficient data transfer. Furthermore, emerging technologies like edge computing architectures are extending data center capabilities closer to data sources, utilizing micro data centers and specialized hardware to process information locally, thereby reducing latency and bandwidth requirements for time-sensitive applications. These technological advancements collectively underpin the enhanced performance, reliability, and security expected from contemporary data center services.

The primary types of data center services include colocation, which provides physical space for client equipment; managed hosting, where providers manage servers and hardware; and cloud services (IaaS, PaaS, SaaS) offering scalable virtualized resources. Hyperscale services cater to extremely large-scale demands from major cloud providers.

AI significantly impacts infrastructure by driving demand for high-density compute, specialized hardware like GPUs, and advanced cooling solutions. It also increases power consumption and network bandwidth needs, pushing data centers towards more efficient and resilient designs.

Key growth drivers include the exponential increase in data generation, accelerated digital transformation initiatives, widespread adoption of cloud computing, and the rising demand for robust, scalable, and secure IT infrastructure across industries.

Major challenges include high capital expenditure for infrastructure, growing concerns over data security and privacy, complex regulatory compliance requirements, and the increasing demand for energy efficiency and sustainable operations.

The Asia Pacific (APAC) region is projected to exhibit the highest growth, driven by rapid digitalization, economic expansion, and increasing investments in IT infrastructure across countries like China, India, and Southeast Asia.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.