ID : MRU_ 428875 | Date : Oct, 2025 | Pages : 248 | Region : Global | Publisher : MRU

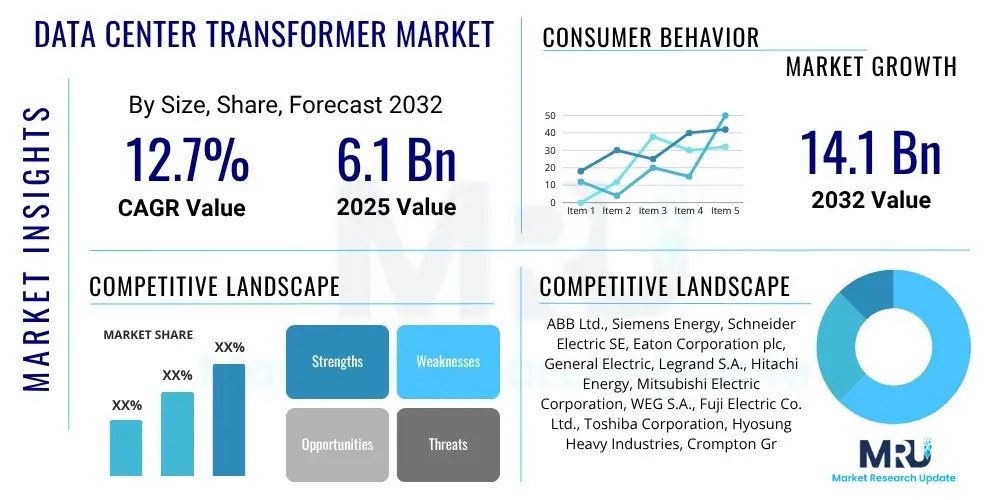

The Data Center Transformer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.7% between 2025 and 2032. The market is estimated at USD 6.1 Billion in 2025 and is projected to reach USD 14.1 Billion by the end of the forecast period in 2032.

The Data Center Transformer Market encompasses the design, manufacturing, and deployment of specialized electrical transformers critical for efficient and reliable power distribution within data center infrastructures. These transformers are essential components that step down or step up voltage levels to meet the specific requirements of various data center equipment, ranging from servers and storage units to cooling systems and networking hardware. The intricate power demands of modern data centers necessitate robust, highly efficient, and reliable transformers that can operate continuously under heavy loads, ensuring uninterrupted service and optimal performance.

Data center transformers are specifically engineered to handle the unique operating conditions of mission-critical facilities, which include high heat loads, constant operational demands, and the need for superior energy efficiency to minimize operational costs and environmental impact. Product descriptions often highlight features such as low loss designs, advanced cooling methods, compact footprints, and smart monitoring capabilities. Major applications span across hyperscale, colocation, and enterprise data centers, each requiring customized power solutions tailored to their scale and specific operational needs. Benefits include enhanced power quality, improved energy efficiency, reduced operational expenditure, increased system reliability, and better adherence to environmental standards.

The primary driving factors propelling the growth of this market include the exponential increase in data generation and consumption, the pervasive adoption of cloud computing services, the rapid expansion of digital transformation initiatives across industries, and the escalating demand for high-performance computing necessary for AI and machine learning workloads. These factors collectively necessitate continuous investment in data center infrastructure, where transformers play a foundational role in managing the complex power requirements of an ever-evolving digital landscape.

The Data Center Transformer Market is experiencing robust growth, driven by an unprecedented surge in global data traffic, the widespread adoption of cloud-based services, and the continuous expansion of digital infrastructure. Business trends indicate a strong focus on energy efficiency, sustainability, and modularity in transformer design, as data center operators strive to reduce operational costs and environmental footprints. Consolidation among smaller players and strategic partnerships between manufacturers and data center builders are also notable business trends, aiming to offer integrated and optimized power solutions. The competitive landscape is characterized by a mix of established electrical equipment manufacturers and specialized power solution providers, all vying to innovate with advanced materials, smart monitoring systems, and environmentally friendly dielectric fluids.

Regional trends reveal North America and Asia Pacific as the leading markets, largely due to the presence of hyperscale data centers, early adoption of advanced technologies, and significant investments in digital infrastructure expansion. North America continues its dominance with a high concentration of tech giants and colocation facilities, while Asia Pacific, particularly countries like China, India, and Japan, demonstrates the fastest growth rates fueled by rapid digitalization, expanding internet penetration, and government initiatives promoting data localization. Europe is also a key region, driven by strict energy efficiency regulations and increasing demand for sustainable data center solutions, with a growing emphasis on integrating renewable energy sources into data center power grids. Latin America and the Middle East & Africa are emerging markets, showing considerable potential due to increasing internet penetration and nascent digital transformation efforts.

Segment trends highlight the growing preference for dry-type transformers over traditional oil-immersed units, primarily due to enhanced safety, reduced maintenance, and environmental benefits. Within the dry-type segment, cast resin transformers are gaining traction for their durability and high performance. There is also an increasing demand for higher kVA ratings to support power-dense racks and modular data center designs. The integration of smart features, such as remote monitoring, predictive maintenance capabilities, and digital control systems, is becoming standard, transforming transformers from mere passive components into intelligent assets within the data center power ecosystem. The shift towards edge computing further accentuates the need for compact, efficient, and robust transformers capable of deployment in diverse environments.

The advent and widespread adoption of Artificial Intelligence (AI) and Machine Learning (ML) workloads are profoundly impacting the Data Center Transformer Market. Users frequently inquire about how AI increases power density demands, the specific transformer characteristics required for AI clusters, and the implications for cooling systems. These inquiries reflect a collective concern regarding the ability of existing power infrastructure to support the exponentially growing energy requirements of AI-driven computing. The consensus indicates that AI processing units, particularly GPUs, consume significantly more power than traditional CPUs, leading to much higher power densities per rack. This necessitates transformers that can deliver more power efficiently, handle transient loads, and often operate closer to their thermal limits, demanding advanced cooling and robust design for reliability. Furthermore, the need for uninterrupted power for critical AI training models emphasizes the importance of fault tolerance and intelligent power management at the transformer level.

The Data Center Transformer Market is primarily driven by the relentless expansion of digital infrastructure globally, fueled by soaring data volumes, ubiquitous cloud adoption, and the emergence of advanced technologies such as Artificial Intelligence and the Internet of Things. These factors necessitate continuous investment in building new data centers and upgrading existing facilities, all of which require reliable, high-capacity transformers. Furthermore, government initiatives promoting digital economies and data localization mandates in various regions are providing a significant impetus for market growth. The increasing focus on energy efficiency and sustainability within data centers also acts as a driver, pushing manufacturers to develop more efficient and environmentally friendly transformer solutions, including those with amorphous cores and eco-friendly dielectric fluids.

However, the market faces several restraints that could impede its growth. High upfront capital expenditure associated with purchasing and installing advanced transformers can be a barrier for smaller data center operators. Volatility in raw material prices, such as copper and steel, directly impacts manufacturing costs and can lead to price fluctuations for the end-products. Additionally, the complexity of supply chains, particularly for specialized components, can cause delays and increase lead times. Stringent regulatory requirements concerning electrical safety, energy efficiency standards, and environmental compliance, while beneficial in the long run, can present initial hurdles for market players needing to adapt their product portfolios and manufacturing processes. The skilled labor shortage for installation and maintenance of complex power infrastructure also poses a challenge.

Despite these restraints, significant opportunities abound. The proliferation of edge computing is creating demand for smaller, more rugged, and highly efficient transformers suitable for decentralized deployments closer to data sources. The integration of renewable energy sources into data center power grids opens avenues for specialized transformers capable of handling variable power inputs and smart grid functionalities. Furthermore, the development of smart transformers equipped with advanced sensors, IoT connectivity, and predictive analytics offers substantial growth potential, allowing for optimized performance, proactive maintenance, and enhanced energy management. Impact forces such as rapid technological advancements in power electronics, increasing focus on grid modernization, and the global push for decarbonization will continue to shape the market landscape, favoring innovative and sustainable transformer solutions.

The Data Center Transformer Market is meticulously segmented to provide a granular understanding of its various facets, allowing for precise market analysis and strategic planning. These segmentations typically involve categorizing transformers based on their design type, power rating, cooling method, insulation type, and the specific application within a data center. Each segment reflects distinct technological characteristics, operational benefits, and suitability for different scales and operational environments of data center facilities, from hyperscale to edge deployments.

Understanding these segments is crucial for stakeholders to identify niche markets, assess competitive landscapes, and tailor product offerings to specific customer needs. For instance, dry-type transformers are often preferred in indoor data center environments due to safety concerns, while oil-immersed transformers might be considered for outdoor substations feeding large data center campuses. The choice of transformer also depends heavily on the required power capacity, the level of efficiency demanded, and the overall budget and regulatory compliance. The continuous evolution of data center architecture, particularly with the rise of AI and modular designs, further drives the need for diverse transformer solutions across these segmented categories.

The value chain for the Data Center Transformer Market begins with the sourcing of raw materials, which includes specialized steel for cores, copper or aluminum for windings, insulating materials like cellulose or resin, and dielectric fluids. These raw materials are processed by upstream suppliers to create components such as core laminations, winding wires, and transformer tanks. This stage is critical as the quality and cost of these basic components significantly influence the final product's performance and price. Innovation in material science, such as amorphous metals for ultra-low loss cores, continuously impacts this initial segment of the value chain, driving efficiency improvements and cost reductions.

Further along the value chain, component manufacturers assemble these raw materials into semi-finished products and specialized parts, such as tap changers, bushings, and cooling systems, which are then supplied to transformer manufacturers. These manufacturers, who form the core of the value chain, design, assemble, test, and certify the final data center transformers according to stringent industry standards and client specifications. Their expertise in electrical engineering, manufacturing processes, and quality control is paramount to producing reliable and high-performance transformers tailored for demanding data center environments. Advanced manufacturing techniques, including automation and precision engineering, are increasingly adopted to enhance production efficiency and product quality.

The distribution channel for data center transformers is multifaceted, involving both direct and indirect sales. For large-scale projects, such as hyperscale data centers or new colocation facilities, manufacturers often engage in direct sales, collaborating closely with data center developers, engineering firms, and electrical contractors from the design phase through commissioning. This direct approach ensures customized solutions and seamless integration. For smaller enterprise data centers or specific upgrade projects, indirect channels like electrical distributors, value-added resellers, and system integrators play a crucial role. These intermediaries provide wider market reach, local support, and often bundled solutions including installation and maintenance services, extending the manufacturers' presence and providing greater accessibility to a diverse customer base.

The primary potential customers and end-users of data center transformers are organizations that own, operate, or develop data centers of various scales and purposes. These entities require robust, efficient, and reliable power distribution infrastructure to support their continuous and intensive computing operations. The increasing reliance on digital services across all sectors means that the customer base is constantly expanding, encompassing both traditional IT infrastructure providers and new entrants in specialized computing domains.

Hyperscale data center operators represent a significant segment of potential customers. These include global technology giants such as Amazon Web Services (AWS), Google Cloud, Microsoft Azure, and Meta, which build and manage massive data center campuses to support their vast cloud services and online platforms. Their demand is characterized by extremely high power requirements, a need for economies of scale, and an emphasis on modularity, energy efficiency, and advanced monitoring capabilities to manage thousands of megawatts of power across multiple facilities. These customers often drive innovation in transformer design and efficiency due to their sheer scale and technical sophistication.

Another crucial customer segment consists of colocation service providers like Equinix, Digital Realty, and CyrusOne. These companies offer data center space, power, and cooling to multiple tenants, catering to businesses that prefer not to build or manage their own data centers. Colocation providers demand highly reliable and flexible transformer solutions that can scale to accommodate diverse tenant requirements and ensure high availability for their mission-critical infrastructure. Enterprise data centers, belonging to large corporations in sectors such as finance, healthcare, telecommunications, and government, also constitute a substantial customer base, focusing on security, uptime, and efficiency for their internal IT operations. Finally, the emerging market for edge computing facilities, which deploy smaller data centers closer to end-users for reduced latency, is creating demand for compact, durable, and highly efficient transformers suitable for diverse and often remote deployment environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.1 Billion |

| Market Forecast in 2032 | USD 14.1 Billion |

| Growth Rate | 12.7% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens Energy, Schneider Electric SE, Eaton Corporation plc, General Electric, Legrand S.A., Hitachi Energy, Mitsubishi Electric Corporation, WEG S.A., Fuji Electric Co. Ltd., Toshiba Corporation, Hyosung Heavy Industries, Crompton Greaves Power and Industrial Solutions Ltd., Voltamp Transformers Ltd., TECO Electric & Machinery Co., Ltd., Hammond Power Solutions, Inc., SGB-SMIT Group, Wilson Power Solutions, Jinpan International Ltd., Efacec |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Data Center Transformer Market is undergoing significant technological advancements aimed at improving efficiency, reliability, and sustainability to meet the evolving demands of modern data centers. A key area of innovation is the development of ultra-high-efficiency transformers, often utilizing amorphous metal cores or advanced grain-oriented electrical steel. These materials significantly reduce no-load losses, contributing to lower operational costs and reduced carbon footprint, which is paramount for energy-intensive data centers. Manufacturers are also exploring advanced winding techniques and improved insulation materials to enhance performance and extend the lifespan of transformers, even under continuous heavy loads and high operating temperatures.

Another crucial technological trend is the integration of smart capabilities into data center transformers. This involves embedding sensors for real-time monitoring of critical parameters such as temperature, voltage, current, and vibration. These sensors, combined with IoT connectivity, enable predictive maintenance, remote diagnostics, and proactive fault detection, ensuring maximum uptime and preventing costly outages. Digital twin technology is also gaining traction, allowing operators to create virtual models of their transformers to simulate performance, optimize operations, and test maintenance strategies without impacting physical assets. This level of intelligence transforms transformers from passive components into active, data-generating assets within the data center's power infrastructure.

Furthermore, there is a growing emphasis on environmentally friendly and space-saving transformer designs. This includes the increasing adoption of dry-type transformers, particularly cast-resin and vacuum pressure impregnated (VPI) types, which eliminate the fire risk and environmental concerns associated with traditional oil-filled units, making them ideal for indoor data center installations. For oil-filled transformers, the use of biodegradable and non-toxic ester fluids is becoming more common as a safer and greener alternative to mineral oil. Modular transformer designs are also gaining popularity, offering greater flexibility and scalability for data center expansion, allowing operators to add or replace units easily without significant disruption to ongoing operations. These technological innovations collectively aim to address the twin challenges of power density and energy efficiency while enhancing the overall resilience of data center power systems.

A data center transformer is a specialized electrical transformer designed to step down or step up voltage within a data center's power distribution system, ensuring reliable and efficient delivery of electricity to servers, cooling systems, and other critical infrastructure components.

Energy-efficient transformers are crucial for data centers to minimize power losses, reduce operational costs, lower carbon emissions, and meet increasingly stringent environmental regulations, thereby improving the overall sustainability and profitability of the facility.

The most common types are dry-type transformers, particularly cast resin and vacuum pressure impregnated (VPI) units, due to their safety, low maintenance, and environmental benefits. Oil-immersed transformers may also be used in outdoor substations or specific applications.

AI significantly increases power density and overall power consumption in data centers, driving demand for higher kVA rated transformers with enhanced efficiency, advanced cooling capabilities, and intelligent monitoring systems to support intensive AI workloads.

Key factors include the data center's power requirements (kVA rating), desired energy efficiency, safety regulations, environmental considerations, physical space constraints, cooling method, initial capital cost, and ongoing maintenance requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.