ID : MRU_ 428260 | Date : Oct, 2025 | Pages : 253 | Region : Global | Publisher : MRU

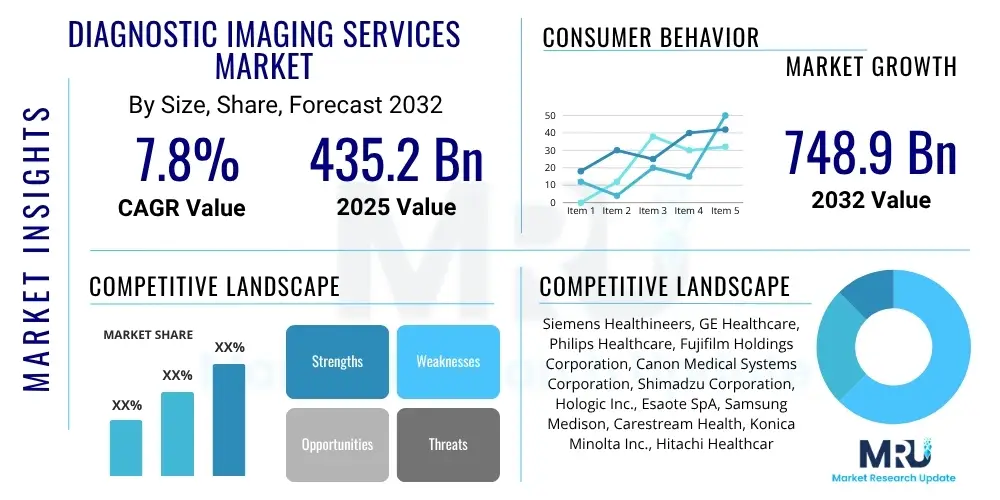

The Diagnostic Imaging Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 435.2 Billion in 2025 and is projected to reach USD 748.9 Billion by the end of the forecast period in 2032.

The Diagnostic Imaging Services Market encompasses a broad spectrum of medical technologies and procedures used to visualize the internal structures of the human body without invasive surgery. These services are paramount in modern medicine, providing invaluable insights for disease detection, accurate diagnosis, precise monitoring of disease progression, and meticulous planning of treatment strategies. The ultimate goal is to empower healthcare professionals with comprehensive visual data that allows for informed clinical decisions, thereby improving patient care outcomes. The market offers a diverse array of imaging modalities, each operating on distinct physical principles to generate detailed images, including X-ray, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, Nuclear Medicine (such as PET and SPECT scans), and Mammography. These technologies are continually advancing, offering higher resolution, faster acquisition times, and enhanced safety profiles to meet the evolving demands of clinical practice.

The applications of diagnostic imaging are extensive and span nearly every medical specialty. In cardiology, imaging helps identify structural heart defects, assess blood flow, and diagnose conditions like coronary artery disease. Oncology relies heavily on imaging for cancer screening, staging, monitoring treatment response, and guiding biopsies. Neurology utilizes advanced scans to detect brain tumors, strokes, and neurodegenerative disorders. Orthopedics benefits from imaging for diagnosing bone fractures, joint injuries, and degenerative conditions. Furthermore, diagnostic imaging is crucial in gastroenterology, urology, and gynecology for evaluating organ health and identifying pathologies. The tangible benefits for patients and healthcare systems include earlier and more accurate disease diagnosis, often leading to less invasive treatment options, a significant reduction in the need for exploratory surgeries, and ultimately, improved patient prognosis and quality of life. These services also contribute to enhanced treatment efficacy by allowing clinicians to precisely target affected areas and monitor therapeutic interventions effectively.

Driving factors for the sustained growth of this market are multifaceted. A significant contributor is the global rise in the prevalence of chronic and lifestyle-related diseases, such as various forms of cancer, cardiovascular ailments, and neurological conditions, which necessitate frequent and precise diagnostic evaluations throughout a patient's care continuum. Concurrent technological advancements, including the development of AI-powered imaging solutions, hybrid modalities, and more patient-friendly equipment, continue to enhance the capabilities and accessibility of these services. Additionally, the increasing global geriatric population, which is inherently more susceptible to a range of age-related health issues requiring diagnostic assessment, fuels demand. Growing public and professional awareness regarding the importance of preventive healthcare and early disease detection further stimulates market expansion, supported by increasing healthcare expenditures globally.

The Diagnostic Imaging Services Market is currently experiencing robust and dynamic expansion, underpinned by a confluence of evolving business models and significant technological advancements. Healthcare providers globally are strategically increasing their investments in state-of-the-art imaging modalities, driven by the imperative to enhance diagnostic accuracy, optimize operational efficiency, and deliver superior patient care. This trend is fostering a strong demand for innovative equipment and sophisticated software solutions that can integrate seamlessly into existing healthcare infrastructures. A palpable shift is observed towards integrated imaging systems, which promise streamlined data management, improved interoperability across different platforms, and more efficient clinical workflows, aligning with the growing emphasis on value-based care models that prioritize patient outcomes while simultaneously managing costs effectively. Collaborative strategic partnerships between pioneering technology developers and established healthcare facilities are becoming increasingly prevalent, serving as catalysts for accelerated innovation and significantly expanding access to advanced diagnostic services across diverse populations.

Regionally, North America and Europe continue to exert a dominant influence over the global market share, largely attributable to their highly developed and technologically advanced healthcare infrastructures, substantial healthcare expenditure, and a proactive approach to the early adoption of cutting-edge imaging technologies. These regions benefit from a high concentration of key market players and a robust regulatory environment that fosters innovation. Conversely, the Asia Pacific region is rapidly emerging as a formidable growth engine, poised for exponential market expansion. This growth is predominantly fueled by rapid improvements in healthcare awareness, ascending economic prosperity leading to increased disposable income for healthcare services, and a plethora of government initiatives strategically aimed at modernizing and upgrading healthcare facilities and services. Emerging economies within Latin America, the Middle East, and Africa are also demonstrating promising growth trajectories, propelled by expanding healthcare access, a burgeoning patient population, and increasing investments directed towards developing more robust medical infrastructures.

From a segmentation perspective, the market's growth is notably influenced by specific modalities and applications. Advanced modalities such as Magnetic Resonance Imaging (MRI) and Computed Tomography (CT) are experiencing particularly high adoption rates, primarily due to their superior imaging capabilities, non-invasive nature, and versatility in diagnosing a wide array of complex conditions. These technologies offer detailed anatomical and functional insights that are critical for complex diagnoses. In terms of clinical applications, oncology and cardiology consistently remain primary drivers of demand, reflecting the persistently high global incidence and prevalence of cancers and cardiovascular diseases, which necessitate frequent, precise, and advanced diagnostic evaluations for effective management. The end-user landscape is predominantly shaped by hospitals, which serve as comprehensive hubs for diverse imaging needs, and specialized diagnostic centers, which often focus on delivering high-volume, specialized imaging services efficiently. Both these end-user segments continue to be pivotal in the delivery and expansion of advanced diagnostic imaging services globally.

The integration of Artificial Intelligence (AI) into the Diagnostic Imaging Services Market is unequivocally transforming how medical images are acquired, processed, interpreted, and ultimately utilized in clinical practice. A predominant set of user questions and concerns centers on AI's potential to significantly enhance diagnostic accuracy, alleviate the escalating workload faced by radiologists, effectively address global staffing shortages in imaging departments, and drastically expedite overall patient care pathways. Users are particularly interested in understanding how AI can discern subtle anomalies that might be imperceptible to the human eye, thereby facilitating earlier and more precise diagnoses. Conversely, significant concerns frequently arise regarding critical issues such as data privacy and security, the potential for job displacement among radiologists, the profound ethical implications associated with increasingly autonomous AI-driven decision-making processes, and the rigorous validation and regulatory approval frameworks essential for ensuring the safety and efficacy of sophisticated AI algorithms in clinical use.

There are substantial expectations for AI to serve as a powerful augmentative tool, significantly enhancing human capabilities rather than entirely supplanting them. AI is envisioned as an intelligent assistant capable of identifying intricate patterns, precisely quantifying various biomarkers, and intelligently prioritizing critical cases for immediate radiologist review, thereby optimizing workflow and improving diagnostic throughput. A strong demand exists for AI-powered solutions that can integrate seamlessly and efficiently into existing Picture Archiving and Communication Systems (PACS) and Radiology Information Systems (RIS) workflows. These integrated AI tools are expected to offer advanced predictive analytics for anticipating disease progression and evaluating treatment response, providing clinicians with proactive insights. Moreover, the discourse around AI frequently highlights its promise to democratize diagnostic imaging, making it more accessible and potentially more affordable, particularly in underserved and remote regions, through automated preliminary readings and dramatically streamlined operational workflows. This could significantly bridge current gaps in global healthcare access.

Further exploration into AI's impact reveals its capacity to revolutionize several operational and clinical aspects within diagnostic imaging. AI algorithms are being developed and refined to optimize radiation dose protocols across modalities like CT and X-ray, minimizing patient exposure while maintaining diagnostic image quality. They are also instrumental in noise reduction and artifact suppression, leading to superior image clarity and interpretability. The sheer volume of medical imaging data generated globally presents a significant challenge, which AI is adept at managing and analyzing, converting raw data into actionable insights at an unprecedented scale. Beyond technical improvements, AI is expected to play a crucial role in enhancing patient engagement through more personalized explanations of imaging findings and guiding patients through complex diagnostic journeys. The continuous development and application of AI in imaging are poised to foster a new era of precision medicine, where diagnostic pathways are tailored, efficient, and ultimately lead to superior patient outcomes.

The Diagnostic Imaging Services Market is robustly propelled by an intricate interplay of dynamic drivers. Chief among these is the escalating global burden of chronic and acute diseases, including various forms of cancer, cardiovascular disorders, neurological conditions, and musculoskeletal ailments, all of which necessitate advanced, timely, and precise diagnostic interventions for effective patient management. The relentless pace of technological advancements in imaging modalities represents another powerful catalyst, with continuous innovations leading to higher resolution images, significantly faster acquisition times, reduced patient discomfort, and the development of multi-functional capabilities that broaden clinical utility. Furthermore, the demographic shift towards an increasingly aging global population, a segment inherently more susceptible to a wide spectrum of age-related health issues requiring frequent diagnostic assessments, fuels a sustained demand. Concurrently, a surge in healthcare expenditure worldwide, coupled with growing public and professional awareness regarding the critical importance of preventive healthcare and early disease detection, collectively provides substantial momentum for continued market growth.

Despite the pervasive growth drivers, the market navigates several notable restraints. The substantial capital investment required for the acquisition, installation, and ongoing maintenance of sophisticated diagnostic imaging equipment presents a formidable barrier to entry, particularly for smaller healthcare facilities, private practices, and healthcare systems in developing economies with constrained budgets. Furthermore, the diagnostic imaging sector is subject to stringent regulatory frameworks and often protracted approval processes for new technologies and services, which can significantly delay market entry and stifle innovation. A persistent global shortage of highly skilled radiologists, radiographers, and medical physicists, essential for operating advanced equipment and accurately interpreting complex imaging results, poses another significant operational challenge. These human resource constraints can impact service delivery capacity and quality, particularly in underserved regions. The rapid technological evolution also necessitates continuous training and upgrades, adding to operational costs and complexity for healthcare providers.

The market is replete with significant opportunities that promise to reshape its future trajectory. The burgeoning integration of Artificial Intelligence (AI) and big data analytics is poised to revolutionize image interpretation, diagnostic accuracy, and workflow efficiency, offering unparalleled potential for growth and innovation. The expansion of teleradiology services, which enable remote image interpretation and expert consultation, is creating avenues for extending diagnostic reach to remote and underserved populations, simultaneously addressing geographical disparities and staffing shortages. Moreover, the growth in emerging economies, characterized by rapidly developing healthcare infrastructures and increasing healthcare access, presents vast untapped markets for diagnostic imaging services. The ongoing shift towards personalized medicine, where diagnostic insights are tailored to individual patient profiles, further enhances the value proposition of advanced imaging. The overall impact forces, including relentless technological innovations, evolving global healthcare reforms, significant macroeconomic shifts, and changing demographic landscapes, constantly redefine the competitive dynamics and necessitate agile strategic adaptations among all market participants to capitalize on new growth frontiers and mitigate emerging risks.

The Diagnostic Imaging Services Market is intricately segmented to provide a granular and comprehensive understanding of its diverse components, offering stakeholders invaluable insights into market dynamics and growth trajectories. This methodical segmentation allows for a detailed analysis across various critical dimensions, including the specific type of imaging technology utilized, the prevalent medical application for which these services are sought, and the distinct end-user facilities that procure and deliver these essential services. Such a nuanced understanding is absolutely crucial for manufacturers, service providers, and investors to accurately identify key areas of growth, effectively tailor their strategic initiatives, and optimally allocate precious resources to maximize impact and return on investment. Each defined segment reflects unique operational characteristics, specific technological requirements, and often distinct patient demographics, all of which profoundly influence demand patterns, pricing strategies, and the competitive landscape across the entire market spectrum.

The primary segmentation framework commonly employed in this market typically involves categorizing services by modality, application, and end-user, with a subsequent overlay of geographical analysis to provide a regional perspective. Modality-based segmentation meticulously differentiates between the diverse array of imaging techniques available, each possessing its own unique capabilities, limitations, and specific diagnostic strengths, thereby catering to a wide range of specialized diagnostic needs. Application-based segmentation strategically highlights the most prevalent and impactful clinical areas that derive the greatest benefit from diagnostic imaging, often showing a direct correlation with global disease prevalence and incidence rates. End-user segmentation further refines this view by categorizing the various types of healthcare providers offering these services, thereby illuminating variations in infrastructure investment, patient volume capacity, and specific service delivery models. This multi-faceted and detailed approach to segmentation ensures a holistic and exhaustive view of the market, which is indispensable for precise market forecasting, robust strategic planning, and successful market navigation for all engaged entities.

Further refinements within these segments are often necessary to capture the full complexity and diversity of the market. For instance, within the X-ray modality, distinctions between analog, digital radiography, and computed radiography highlight technological evolution and adoption trends. Similarly, MRI can be sub-segmented by field strength (e.g., 1.5T, 3T, 7T) or by type (open vs. closed, functional MRI), reflecting variations in diagnostic capabilities and applications. Within applications, specific sub-indications like cardiac MRI for specific heart conditions or breast MRI for high-risk screening offer even finer detail. The end-user segment also considers the growing role of ambulatory surgical centers and mobile imaging units, which are expanding access and convenience. Such detailed segmentation facilitates a more targeted market analysis, enabling businesses to identify niche opportunities, understand competitive positioning, and develop products and services that precisely meet the evolving needs of specific market sub-segments, driving innovation and market penetration.

The value chain within the Diagnostic Imaging Services Market is a sophisticated and multi-tiered ecosystem, involving a diverse array of stakeholders who collaboratively contribute to the research, development, manufacturing, distribution, and ultimate delivery of critical diagnostic information to patients. Upstream activities constitute the foundational layers, commencing with intensive research and development efforts aimed at pioneering novel imaging technologies and refining existing ones. This phase involves scientific breakthroughs in physics, materials science, and software engineering. Following R&D, the manufacturing segment focuses on producing highly sophisticated medical imaging equipment, which includes intricate components such as advanced X-ray tubes, high-precision detectors, powerful magnets for MRI systems, and sensitive transducers for ultrasound devices. Key upstream suppliers are crucial, encompassing manufacturers of medical-grade electronic components, specialized software developers for imaging platforms and AI algorithms, and providers of essential consumables like contrast agents and radiopharmaceuticals. This initial phase of the value chain places paramount importance on innovation, precision engineering, and rigorous adherence to stringent quality and safety standards, as the fundamental technology directly dictates the diagnostic efficacy and clinical reliability of the subsequent services.

Midstream activities primarily revolve around the robust logistical framework for distributing these complex imaging systems and associated products. This typically involves a combination of direct sales forces employed by major manufacturers, a network of specialized distributors, and value-added resellers who provide installation, training, and ongoing technical support. These entities are responsible for ensuring that state-of-the-art equipment reaches diverse healthcare facilities, including large academic hospitals, community clinics, and specialized diagnostic centers globally. Simultaneously, the development and integration of Picture Archiving and Communication Systems (PACS) and Radiology Information Systems (RIS) are crucial midstream components, providing the digital infrastructure for efficient image acquisition, secure storage, rapid retrieval, and comprehensive management of patient imaging data. These systems streamline workflows, improve data accessibility, and ensure compliance with healthcare information standards, forming the backbone of modern diagnostic imaging operations.

Downstream analysis elucidates the final stages of service delivery and utilization, where the core diagnostic services are rendered directly to patients. This critical phase involves highly trained and specialized personnel, including board-certified radiologists who interpret images and provide diagnoses, skilled radiographers and technologists who operate the advanced equipment and acquire high-quality images, and medical physicists who ensure equipment calibration and radiation safety. Direct channels predominantly involve patients accessing services at established healthcare facilities through physician referrals or emergency admissions. Indirect channels might include teleradiology services, where images are transmitted securely for remote interpretation by radiologists, thereby extending expertise and capacity, particularly to remote or underserved areas. Beyond direct image interpretation, ancillary services such as advanced visualization software, cloud-based data storage, cybersecurity solutions, and comprehensive equipment maintenance services are integral to optimizing workflow, enhancing data security, ensuring operational uptime, and facilitating the effective communication of vital diagnostic insights to referring clinicians for precise patient management and treatment planning.

The potential customer base for Diagnostic Imaging Services is exceptionally broad and integral to the entire spectrum of the global healthcare ecosystem. It primarily encompasses various entities and individual practitioners who require sophisticated internal body visualization capabilities for a multitude of medical purposes, ranging from routine screenings to complex disease diagnosis and treatment monitoring. The largest and most significant segment of end-users are hospitals, which vary in scale from expansive academic medical centers with cutting-edge research capabilities to smaller community hospitals providing essential local care. These institutions cater to an immensely diverse patient population across virtually all medical specialties and typically house a comprehensive suite of advanced imaging modalities. Hospitals are profoundly reliant on diagnostic imaging for critical emergency care, comprehensive inpatient diagnostics, meticulous surgical planning, and long-term management of chronic diseases, positioning them as the undisputed epicenter of demand within this market.

Beyond the extensive hospital network, dedicated diagnostic centers represent another crucially substantial customer segment. These specialized centers primarily focus on delivering a wide array of imaging services, often prioritizing operational efficiency, enhancing patient comfort, and cultivating specialized expertise in specific imaging modalities or clinical areas. Such centers are frequently the preferred choice for patients referred by primary care physicians and various specialists seeking focused and high-quality diagnostic evaluations. In addition to these, specialty clinics, encompassing cardiology clinics focused on heart health, orthopedic centers addressing bone and joint issues, oncology clinics specializing in cancer care, and women's health centers providing gynecological and obstetrical imaging, also constitute significant buyers. These clinics procure imaging services that are precisely tailored to the specific needs of their unique patient populations and prevalent disease areas, ensuring targeted and effective diagnostic support for their specialized services.

Furthermore, academic and research institutes play an increasingly pivotal role as discerning customers for advanced diagnostic imaging services and equipment. These institutions frequently leverage state-of-the-art imaging technologies for rigorous clinical trials, groundbreaking biomedical research, and vital educational purposes, contributing significantly to medical advancements and the training of future healthcare professionals. The burgeoning field of telemedicine and teleradiology has also created a new class of customers, including remote clinics and healthcare providers seeking outsourced imaging interpretations, expanding access to expert diagnostics in underserved regions. The overall trend points towards a continued diversification of the customer base, driven by technological innovations, evolving healthcare delivery models, and an increasing recognition of the indispensable role of timely and accurate diagnostic imaging in improving global health outcomes. This diversification underscores the market's resilience and adaptability to changing healthcare landscapes and patient needs.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 435.2 Billion |

| Market Forecast in 2032 | USD 748.9 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Healthineers, GE Healthcare, Philips Healthcare, Fujifilm Holdings Corporation, Canon Medical Systems Corporation, Shimadzu Corporation, Hologic Inc., Esaote SpA, Samsung Medison, Carestream Health, Konica Minolta Inc., Hitachi Healthcare, Mindray Medical International Limited, Analogic Corporation, Trivitron Healthcare, Varex Imaging Corporation, Agfa-Gevaert Group, Bracco Imaging S.p.A., Guerbet, Sectra AB. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Diagnostic Imaging Services Market is perpetually reshaped by a relentlessly dynamic and rapidly evolving technology landscape, with continuous innovations focused on multifaceted objectives: profoundly enhancing image quality, significantly reducing patient radiation exposure and discomfort, substantially improving workflow efficiency, and dramatically expanding the overall diagnostic capabilities available to clinicians. At the core of this technological evolution are breakthroughs in fundamental components and engineering. For modalities such as Computed Tomography (CT) and X-ray, advancements include sophisticated detector designs, ultra-fast reconstruction algorithms, and dose-optimization techniques that collectively lead to significantly sharper images acquired with remarkably lower radiation doses. In Magnetic Resonance Imaging (MRI), innovations encompass higher field strengths (e.g., 3T, 7T) for superior signal-to-noise ratios, more compact and patient-friendly magnet designs, and accelerated scanning sequences (such as compressed sensing), enabling clearer visualization of soft tissues, detailed functional imaging, and reduced scan times. Ultrasound technology has progressed remarkably with capabilities like real-time 3D/4D imaging, elastography for tissue stiffness assessment, and contrast-enhanced ultrasound, collectively offering enhanced diagnostic utility for a much wider and more complex range of medical conditions.

Beyond the fundamental imaging equipment, the current technology landscape is profoundly influenced and driven by the pervasive integration of digital solutions and cutting-edge artificial intelligence. Picture Archiving and Communication Systems (PACS) and Radiology Information Systems (RIS) remain absolutely foundational, serving as the indispensable digital infrastructure for efficient image storage, rapid retrieval, seamless data management, and streamlined reporting workflows. These systems ensure that digital images and patient data are accessible to authorized personnel across a healthcare network. The revolutionary integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is fundamentally transforming image interpretation by automating lesion detection, precisely quantifying disease progression, and intelligently guiding radiologists through complex cases, promising to significantly augment human capabilities and dramatically improve diagnostic accuracy, consistency, and speed. Cloud computing is another pivotal technology, facilitating secure, scalable, and cost-effective data storage and sharing, which is essential for the expansion of teleradiology and collaborative diagnostics across geographical boundaries. Furthermore, advanced visualization tools provide sophisticated 3D rendering, virtual reality (VR) interfaces, and augmented reality (AR) overlays for intricate case analysis, pre-surgical planning, and educational purposes, allowing for deeper insights into complex anatomical structures and pathologies.

The innovation extends to the development of sophisticated hybrid imaging systems, representing a significant leap forward in multimodal diagnostics. Examples include PET/CT and PET/MRI, which combine the anatomical precision of CT or MRI with the functional and metabolic insights of Positron Emission Tomography (PET). These hybrid systems offer a more comprehensive and holistic diagnostic view by simultaneously capturing both structural and biological information, leading to more accurate staging of cancers, better assessment of neurological disorders, and improved characterization of cardiac conditions. Furthermore, molecular imaging techniques, which aim to visualize biological processes at the cellular and molecular level, are also gaining prominence, providing even earlier disease detection and more personalized treatment strategies. The increasing focus on interoperability standards (such as DICOM and HL7) ensures seamless communication between different devices and systems, fostering a truly integrated diagnostic environment. These ongoing technological advancements, coupled with an emphasis on patient comfort, safety, and efficiency, underscore the dynamic and innovative trajectory of the diagnostic imaging services market, continuously pushing the boundaries of what is medically possible.

The primary modalities include X-ray, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, Nuclear Medicine (SPECT, PET), and Mammography. Each modality offers unique advantages for visualizing different body structures and conditions, aiding in comprehensive diagnostic evaluations.

AI is significantly impacting diagnostic imaging by enhancing image analysis, improving diagnostic accuracy, reducing radiologist workload, and streamlining workflows. AI algorithms assist in lesion detection, disease quantification, and prioritizing urgent cases, leading to faster and more precise diagnoses.

Key drivers include the rising prevalence of chronic diseases, continuous technological advancements in imaging equipment, an increasing global geriatric population, growing awareness about early disease diagnosis, and expanding healthcare infrastructure, particularly in emerging economies.

The market faces challenges such as the high cost of advanced imaging equipment, stringent regulatory requirements for new technologies, and a persistent shortage of skilled radiologists and technicians. Data privacy and cybersecurity concerns also present ongoing challenges for digital imaging services.

North America and Europe currently lead in the adoption of diagnostic imaging services due to well-established healthcare systems and high technology penetration. However, the Asia Pacific region is expected to show the fastest growth, driven by healthcare infrastructure development and increasing patient demand.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.