ID : MRU_ 427925 | Date : Oct, 2025 | Pages : 245 | Region : Global | Publisher : MRU

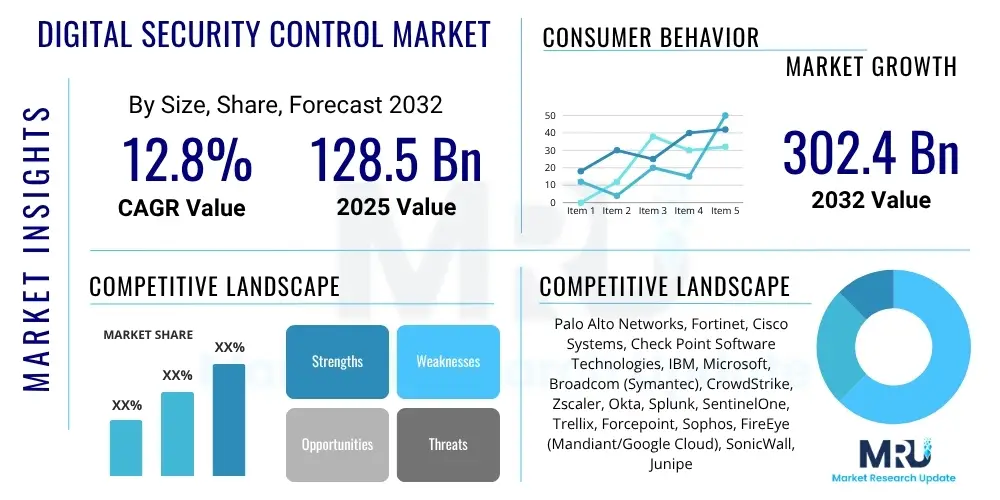

The Digital Security Control Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2032. The market is estimated at USD 128.5 billion in 2025 and is projected to reach USD 302.4 billion by the end of the forecast period in 2032.

The Digital Security Control Market encompasses a broad spectrum of technologies, solutions, and services designed to protect digital assets, networks, and systems from unauthorized access, cyberattacks, and data breaches. It addresses the critical need for organizations to safeguard sensitive information, maintain operational continuity, and comply with an increasingly stringent regulatory landscape in an interconnected world. The market is defined by its continuous evolution in response to emerging threats and technological advancements, providing comprehensive defense mechanisms against a dynamic threat environment.

Products within this market range from identity and access management (IAM) systems, data loss prevention (DLP) tools, encryption technologies, intrusion detection and prevention systems (IDPS), security information and event management (SIEM) platforms, to cloud security and endpoint protection solutions. Major applications span across virtually all industries, including banking, financial services, and insurance (BFSI), IT and telecommunications, healthcare, government, retail, manufacturing, and energy, each with unique security requirements. The inherent benefits of robust digital security control include enhanced data privacy, reduced financial losses from cyber incidents, improved operational resilience, increased customer trust, and compliance with global data protection regulations.

Key driving factors for market expansion include the accelerating pace of digital transformation across enterprises, the pervasive adoption of cloud computing and the Internet of Things (IoT), and the exponential increase in the volume and sophistication of cyber threats. Furthermore, the growing awareness among businesses about the financial and reputational ramifications of security breaches, coupled with stricter regulatory mandates like GDPR, HIPAA, and CCPA, compel organizations to invest heavily in advanced digital security control measures. The shift towards remote and hybrid work models has also expanded attack surfaces, making comprehensive digital security control an indispensable component of modern business operations.

The Digital Security Control Market is experiencing robust growth driven by the escalating cyber threat landscape, rapid digital transformation initiatives, and increasing regulatory pressures worldwide. Business trends indicate a strong move towards integrated, AI-powered security solutions and managed security services, as organizations seek to consolidate their security posture and address the pervasive cybersecurity skills gap. Enterprises are prioritizing proactive threat intelligence, automated response capabilities, and a layered security approach to protect their expanding digital footprints, encompassing cloud environments, remote endpoints, and critical infrastructure. The emphasis on zero-trust architectures and identity-centric security is also shaping investment priorities, reflecting a shift from perimeter-based defenses to more granular access control and continuous verification.

Regional trends reveal North America and Europe as dominant markets, primarily due to advanced technological infrastructure, high rates of digital adoption, and stringent regulatory frameworks. However, the Asia Pacific region is emerging as the fastest-growing market, propelled by rapid industrialization, increasing internet penetration, and a burgeoning digital economy that demands sophisticated security solutions. Latin America, the Middle East, and Africa are also witnessing significant growth, driven by government initiatives to enhance cybersecurity and the increasing digital presence of businesses. Each region presents unique challenges and opportunities, influencing localized security strategies and technology adoption patterns.

Segmentation trends highlight the increasing demand for cloud security solutions as organizations migrate workloads to public and private clouds, alongside continued investment in identity and access management to control who accesses what resources. Services, particularly managed security services, are gaining traction as businesses opt to outsource complex security operations to specialized providers. The large enterprise segment remains a primary consumer of advanced security controls, but small and medium-sized enterprises (SMEs) are increasingly recognizing the necessity of robust security, leading to a growing demand for cost-effective, scalable solutions. The BFSI and IT & Telecom sectors continue to be major adopters due to their high-value data assets and strict compliance requirements, while healthcare and manufacturing are rapidly expanding their security expenditures to combat industry-specific threats.

Users frequently inquire about AI's capacity to revolutionize threat detection, automate response mechanisms, and enhance predictive analytics within digital security. Common concerns include the potential for AI-powered attacks, the ethical implications of AI in surveillance, and the challenge of managing false positives and ensuring explainability in AI-driven security systems. There's significant interest in how AI can help address the cybersecurity skills gap and process the overwhelming volume of security data, alongside expectations for AI to deliver more intelligent, adaptive, and proactive security measures.

The Digital Security Control Market is primarily driven by the relentless increase in the volume, sophistication, and diversity of cyberattacks, which necessitate advanced defense mechanisms. The pervasive digital transformation across all industry sectors, involving cloud adoption, IoT proliferation, and remote work, continuously expands the attack surface, creating an urgent demand for comprehensive security solutions. Furthermore, the growing global push for stringent data privacy and protection regulations, such as GDPR, CCPA, and various industry-specific mandates, compels organizations to invest in robust digital security controls to avoid severe penalties and maintain compliance. These drivers collectively underpin the sustained growth trajectory of the market, making digital security an indispensable component of modern business strategy.

However, the market faces significant restraints that can impede its full potential. High implementation costs associated with advanced security technologies, particularly for small and medium-sized enterprises (SMEs), can be a barrier to adoption. The inherent complexity of integrating diverse security solutions into existing IT infrastructures, coupled with the persistent global shortage of skilled cybersecurity professionals, poses substantial operational challenges. Additionally, the constant evolution of threats requires continuous investment in updates and training, which can strain IT budgets and resources, particularly for organizations with limited financial capacity or technical expertise. The challenge of balancing security needs with user convenience also presents a hurdle, as overly restrictive controls can hinder productivity.

Despite these challenges, significant opportunities abound for innovation and market expansion. The integration of artificial intelligence (AI) and machine learning (ML) into security solutions offers vast potential for predictive threat intelligence, automated response, and enhanced anomaly detection, transforming reactive security into proactive defense. The rise of managed security services (MSS) provides an avenue for organizations to outsource their security operations, bridging the skills gap and leveraging expert capabilities without extensive in-house investment. Furthermore, the convergence of operational technology (OT) and information technology (IT) security, the increasing adoption of zero-trust security models, and the expanding market for specialized cloud security and IoT security solutions present lucrative growth areas. The continuous need for cybersecurity awareness and training also creates opportunities for service providers.

The impact forces influencing this market are multifaceted and dynamic. Technological advancements, particularly in areas like quantum computing and advanced encryption, will continuously reshape the security landscape, demanding constant adaptation from solution providers. The evolving threat landscape, characterized by state-sponsored attacks, ransomware-as-a-service models, and supply chain compromises, necessitates agile and resilient security strategies. Regulatory pressures from governments and international bodies will continue to dictate compliance requirements, influencing product development and market demand. Economic conditions can impact IT spending, while geopolitical stability can lead to shifts in national cybersecurity priorities and investment. Collectively, these impact forces create a complex environment that drives innovation and strategic decision-making within the Digital Security Control Market.

The Digital Security Control Market is comprehensively segmented across various dimensions to provide a granular understanding of its dynamics and emerging trends. These segmentations help analyze different facets of the market, including the types of solutions and services offered, the methods of deployment, the organizational sizes they cater to, and the diverse industry verticals that utilize these security measures. Understanding these segments is crucial for identifying key growth drivers, competitive landscapes, and unmet needs across different market niches. The market’s segmentation reflects the diverse and evolving requirements of modern enterprises in securing their digital assets and operations.

The value chain for the Digital Security Control Market commences with upstream activities focused on foundational research and development (R&D), where innovative security technologies, algorithms, and threat intelligence capabilities are conceptualized and engineered. This phase involves extensive investment in cybersecurity expertise, data science, and advanced computing to create the core intellectual property that underpins security solutions. Semiconductor manufacturers, software developers, and academic research institutions play a crucial role in providing the essential building blocks and underlying infrastructure, often specializing in areas like cryptographic techniques, AI/ML for threat detection, and secure hardware design. These upstream activities are critical for driving future advancements and maintaining a competitive edge in a rapidly evolving threat landscape.

Further along the value chain, downstream activities involve the development, integration, and deployment of these security solutions into comprehensive products and services. This includes software and hardware vendors who build specific security products such as firewalls, IAM systems, endpoint protection suites, and cloud security platforms. System integrators then play a pivotal role in customizing, deploying, and integrating these diverse solutions into clients' complex IT environments, ensuring seamless operation and optimal security posture. Managed security service providers (MSSPs) offer ongoing monitoring, threat detection, incident response, and security management as a service, allowing organizations to outsource their cybersecurity operations and leverage specialized expertise, thereby significantly extending the reach and impact of security controls to end-users.

Distribution channels in the Digital Security Control Market are multi-faceted, encompassing both direct and indirect models. Direct channels involve security vendors selling their products and services directly to large enterprise clients, often through dedicated sales teams, professional services, and direct support. This approach allows for closer client relationships, custom solutions, and direct feedback. Indirect channels, on the other hand, leverage a network of partners, including value-added resellers (VARs), system integrators, managed service providers (MSPs), and distributors. These partners extend market reach, provide localized support, and bundle security solutions with other IT services, making them accessible to a wider range of customers, including SMEs, who might not have direct engagement with top-tier vendors. The choice of channel often depends on the product's complexity, the target customer segment, and the vendor's overall market strategy, with many opting for a hybrid approach to maximize market penetration and service delivery.

The potential customers for the Digital Security Control Market are incredibly diverse, spanning virtually every sector that relies on digital infrastructure and handles sensitive information. These end-users, or buyers of the product, encompass a broad range from government entities and large multinational corporations to small and medium-sized enterprises (SMEs) and even individual consumers in some specialized contexts. Organizations across all verticals are increasingly becoming targets of cyberattacks and are subject to stringent regulatory compliance, making robust digital security an imperative rather than an option. The escalating digital transformation initiatives, including cloud adoption, remote work, and IoT integration, universally expand the attack surface, driving a fundamental need for comprehensive security controls across the entire business ecosystem.

Specifically, the Banking, Financial Services, and Insurance (BFSI) sector represents a critical customer segment, given the high value of financial data and the strict regulatory environment it operates within. Similarly, the IT and Telecommunications sector, being the backbone of digital communication and data processing, requires advanced security to protect its vast networks and customer information. Healthcare organizations are increasingly targeted for their highly sensitive patient data, necessitating strong data privacy and breach prevention solutions. Government and Defense agencies demand state-of-the-art security to safeguard national infrastructure and classified information from state-sponsored attacks and espionage. Retail and E-commerce businesses need to protect customer payment information and maintain trust in their online platforms. Manufacturing and Energy & Utilities sectors are also rapidly adopting digital security controls to secure their operational technology (OT) and industrial control systems (ICS) from cyber-physical threats, recognizing the potential for significant disruption.

Furthermore, educational institutions, media and entertainment companies, and various other emerging sectors are becoming significant end-users as their digital presence and data dependency grow. The shift towards remote and hybrid work models has expanded the need for endpoint security, cloud access security brokers (CASB), and secure collaboration tools, making any organization with a distributed workforce a potential customer. SMEs, while often operating with limited IT budgets and expertise, are increasingly recognizing their vulnerability and the catastrophic impact of a breach, leading to a rising demand for scalable, easy-to-manage security solutions, including managed security services. Essentially, any entity that creates, processes, stores, or transmits digital data is a potential customer for digital security control solutions, making the market exceptionally broad and ever-expanding.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 128.5 billion |

| Market Forecast in 2032 | USD 302.4 billion |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Palo Alto Networks, Fortinet, Cisco Systems, Check Point Software Technologies, IBM, Microsoft, Broadcom (Symantec), CrowdStrike, Zscaler, Okta, Splunk, SentinelOne, Trellix, Forcepoint, Sophos, FireEye (Mandiant/Google Cloud), SonicWall, Juniper Networks, Huawei, CyberArk |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Digital Security Control Market is characterized by a dynamic and continuously evolving technology landscape, driven by the need to counter increasingly sophisticated cyber threats and adapt to new digital paradigms. At its core, the market leverages a blend of established and emerging technologies to provide multi-layered defense. Core technologies include advanced encryption standards (AES, RSA) for data protection, sophisticated firewalls and intrusion prevention systems (IPS) for network perimeter defense, and robust identity and access management (IAM) solutions utilizing multi-factor authentication (MFA) and single sign-on (SSO) to control user access. Data loss prevention (DLP) technologies employ content inspection and contextual analysis to prevent sensitive data exfiltration. Endpoint detection and response (EDR) and extended detection and response (XDR) platforms integrate various security tools to provide comprehensive visibility and automate threat response across endpoints, networks, and cloud environments, marking a significant evolution from traditional antivirus solutions.

Recent advancements have seen artificial intelligence (AI) and machine learning (ML) become foundational elements, revolutionizing threat detection, anomaly behavior analysis, and predictive analytics. AI/ML algorithms are employed in security information and event management (SIEM) systems to process vast amounts of log data, identify patterns indicative of attacks, and reduce false positives. Behavioral analytics for users and entities (UEBA) leverage AI to establish baselines of normal behavior and flag deviations, indicating potential insider threats or compromised accounts. Cloud security technologies, including Cloud Access Security Brokers (CASB), Cloud Security Posture Management (CSPM), and Serverless security, are paramount as organizations increasingly migrate their workloads to various cloud platforms, ensuring data protection, compliance, and threat prevention in distributed cloud environments. These technologies are crucial for managing the unique security challenges posed by shared responsibility models and dynamic cloud infrastructures.

Furthermore, the market is witnessing the growing importance of zero-trust network access (ZTNA), which operates on the principle of "never trust, always verify," implementing strict access controls regardless of network location. Security orchestration, automation, and response (SOAR) platforms are gaining traction, allowing organizations to automate routine security tasks, integrate disparate security tools, and accelerate incident response times, thereby improving operational efficiency and reducing the burden on security teams. Blockchain technology is also being explored for its potential in enhancing identity verification, secure data sharing, and immutable logging. Container security and DevSecOps practices are becoming critical for securing modern application development and deployment pipelines. These emerging technologies collectively contribute to a more resilient, intelligent, and adaptive digital security control ecosystem, enabling organizations to stay ahead of evolving cyber threats and safeguard their digital assets more effectively.

Digital Security Control refers to the technologies and processes used to protect digital assets, networks, and data from cyber threats. It is crucial for preventing data breaches, ensuring operational continuity, maintaining compliance with regulations, and safeguarding an organization's reputation and financial stability in the digital age.

The market is typically segmented by component (solutions like IAM, DLP, encryption; and services like managed security, consulting), deployment model (on-premise, cloud, hybrid), organization size (SMEs, large enterprises), and industry vertical (BFSI, IT & Telecom, Healthcare, Government, etc.) to address diverse security needs.

Key growth drivers include the escalating volume and sophistication of cyberattacks, accelerating digital transformation and cloud adoption, stricter data privacy regulations (e.g., GDPR), the rise of remote work, and the expanding attack surface due to IoT proliferation and interconnected systems.

AI significantly enhances digital security by improving threat detection through advanced machine learning, automating incident response, enabling predictive analytics for emerging threats, and reducing false positives. It helps security systems become more intelligent, adaptive, and efficient in countering complex cyber threats.

The primary challenges include high implementation and maintenance costs for advanced security solutions, the complexity of integrating diverse security tools, a persistent global shortage of skilled cybersecurity professionals, and the continuous need to adapt to an evolving and sophisticated cyber threat landscape.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.