ID : MRU_ 429292 | Date : Oct, 2025 | Pages : 249 | Region : Global | Publisher : MRU

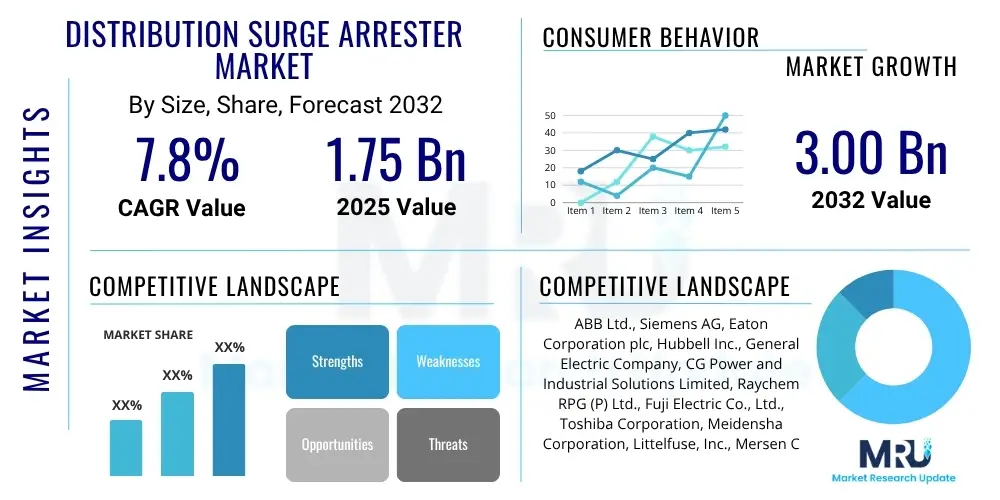

The Distribution Surge Arrester Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 1.75 Billion in 2025 and is projected to reach USD 3.00 Billion by the end of the forecast period in 2032.

The Distribution Surge Arrester Market is a critical segment within the electrical infrastructure industry, driven by the escalating need to protect sensitive electrical equipment from transient overvoltages caused by lightning strikes, switching operations, and other electrical disturbances. These vital devices ensure the reliability and longevity of power distribution networks, which are increasingly complex due to the integration of renewable energy sources and the expansion of smart grid technologies. The core function of a surge arrester is to divert excessive voltage surges to the ground, thereby preventing damage to transformers, circuit breakers, and other essential components, which in turn minimizes power outages and operational costs for utilities and industrial consumers alike.

Product descriptions typically focus on various types, including polymer-housed and porcelain-housed metal oxide varistor (MOV) arresters, differentiated by their voltage ratings, energy absorption capabilities, and environmental resilience. Major applications span across utility substations, industrial facilities, commercial buildings, and infrastructure projects like railways and telecommunications. Their deployment is indispensable in regions prone to severe weather conditions or where grid stability is a paramount concern. The continuous demand for reliable power supply across urban and rural landscapes further cements the indispensable role of distribution surge arresters in maintaining robust electrical grids and protecting capital-intensive assets.

The primary benefits derived from the widespread adoption of distribution surge arresters include enhanced system reliability, reduced equipment downtime, improved safety for personnel, and significant cost savings over the operational lifespan of electrical assets. Key driving factors propelling market expansion encompass global grid modernization initiatives, the rapid expansion of renewable energy generation capacity, increasing industrialization and urbanization leading to higher electricity demand, and the urgent need to replace aging electrical infrastructure in developed economies. These factors collectively underscore the market's robust growth trajectory, as stakeholders prioritize resilient and efficient power distribution systems.

The Distribution Surge Arrester Market is experiencing dynamic shifts, characterized by several key business trends, regional growth patterns, and distinct segment developments. Business trends are largely influenced by technological advancements, such as the introduction of smart surge arresters equipped with monitoring capabilities for predictive maintenance and enhanced grid intelligence. There is a discernible focus on developing environmentally friendly materials and designs, including silicone-based polymer housings, which offer superior performance and reduced weight compared to traditional porcelain. Furthermore, market players are actively pursuing mergers, acquisitions, and strategic partnerships to expand their product portfolios, geographic reach, and technological expertise, catering to diverse customer needs and market specificities.

Regionally, the market exhibits a robust growth trajectory, particularly in the Asia Pacific due to rapid industrialization, urbanization, and substantial investments in expanding and modernizing power grids in countries like China and India. North America and Europe are witnessing steady demand driven by extensive grid renovation projects, the integration of distributed energy resources, and stringent regulatory frameworks mandating reliable power protection. Latin America, the Middle East, and Africa are emerging as significant markets, propelled by increasing electrification rates, infrastructure development initiatives, and the establishment of new industrial corridors. Each region presents unique opportunities and challenges, shaping the competitive landscape and strategic priorities of market participants.

Segment trends highlight a preference for medium voltage distribution surge arresters, which constitute a significant share of the market due to their widespread application in primary and secondary distribution networks. In terms of product type, polymer-housed arresters are gaining traction over porcelain due to their lightweight nature, superior hydrophobicity, explosion-proof characteristics, and improved resistance to vandalism. The utility sector remains the largest end-user segment, consistently investing in advanced surge protection solutions to ensure grid stability and minimize economic losses from outages. The industrial sector, including heavy manufacturing, oil and gas, and mining, also contributes substantially, emphasizing protection for critical machinery and operational continuity.

The integration of Artificial Intelligence (AI) and machine learning capabilities is poised to significantly transform the Distribution Surge Arrester Market, addressing common user questions about enhancing grid reliability, optimizing operational efficiency, and enabling proactive maintenance strategies. Users are increasingly concerned with how AI can move surge protection beyond reactive measures to predictive and intelligent systems. They seek to understand AI's role in diagnosing potential issues before they lead to failures, minimizing downtime, and extending the lifespan of critical infrastructure. The primary expectation revolves around leveraging AI for smarter grid management, where surge arresters contribute data that, when analyzed, provides actionable insights for an overall more resilient and efficient power distribution system, ultimately reducing human intervention and operational costs while improving safety and service continuity.

The Distribution Surge Arrester Market is significantly influenced by a complex interplay of drivers, restraints, opportunities, and various impact forces that collectively shape its growth trajectory and competitive landscape. Drivers for market expansion are primarily rooted in the increasing global demand for reliable electricity, necessitating robust protection for power infrastructure. The continuous upgrade and expansion of smart grids, coupled with the rapid integration of renewable energy sources such such as solar and wind, inherently expose grids to greater transient overvoltage risks, driving the adoption of advanced surge arresters. Additionally, aging electrical infrastructure in developed economies requires frequent replacement and modernization, providing a sustained demand for new and improved surge protection devices. Urbanization and industrial growth further amplify electricity consumption, making reliable grid operation paramount.

Despite these strong drivers, the market faces several restraints that could impede its growth. High initial investment costs associated with advanced surge arresters, particularly for high-voltage applications and smart variants, can be a significant barrier for smaller utilities or developing regions with budget constraints. The presence of alternative protection methods, such as grounding systems and transient voltage suppressors, though often less comprehensive, can also pose competitive challenges. Furthermore, a lack of standardized regulations or enforcement across all regions regarding surge protection requirements can lead to varied adoption rates and market fragmentation. The complexity of integrating smart arresters into existing legacy grid systems also presents a technical and financial hurdle, requiring substantial infrastructure upgrades and skilled personnel.

However, the market is rich with opportunities that promise future growth and innovation. The burgeoning smart grid market worldwide offers a fertile ground for sophisticated surge arresters equipped with communication and monitoring capabilities, enabling predictive maintenance and enhanced grid analytics. Developing economies, with their ambitious electrification programs and infrastructure expansion projects, represent untapped potential for market penetration. Ongoing research and development into novel materials, such as advanced composites and environmentally friendly polymers, along with innovations in Metal Oxide Varistor (MOV) technology, are creating opportunities for more efficient, durable, and cost-effective products. The increasing focus on remote monitoring and control systems for grid assets also opens new avenues for integrating surge arresters into comprehensive smart infrastructure solutions.

The Distribution Surge Arrester Market is meticulously segmented based on various critical parameters including type, voltage level, and application, allowing for a granular understanding of market dynamics and targeted strategic approaches. This segmentation provides stakeholders with insights into specific product demands, end-user preferences, and technological advancements across different operational environments. Analyzing these segments is essential for manufacturers to tailor their product offerings, for distributors to optimize their supply chains, and for investors to identify high-growth areas within the broader market landscape. Each segment is characterized by unique technical requirements, deployment challenges, and competitive pressures, contributing to the overall complexity and diversity of the market.

The value chain for the Distribution Surge Arrester Market is a complex and interconnected network, beginning with the sourcing of specialized raw materials and extending through manufacturing, assembly, distribution, and ultimately to the end-user applications. Upstream activities involve the procurement of critical components such as metal oxide varistors (MOVs), typically made from zinc oxide, which form the core active element for surge protection. Other essential raw materials include silicone rubber for polymer housings, porcelain for ceramic housings, various metallic components for electrodes and terminals, and insulation materials. The quality and availability of these raw materials, along with their associated pricing, significantly impact the final product cost and performance, driving manufacturers to establish robust supply chain relationships and often engage in vertical integration or long-term supplier contracts.

Midstream activities primarily encompass the sophisticated manufacturing processes involved in producing surge arresters. This includes the precise fabrication of MOV discs with specific electrical characteristics, the molding and curing of polymer housings, the intricate assembly of internal components, and rigorous testing procedures to ensure compliance with international standards such as IEC and ANSI. Companies invest heavily in research and development to innovate in materials science, manufacturing techniques, and smart technologies to enhance arrester performance, durability, and cost-effectiveness. Downstream activities focus on the distribution and installation of these products. Distribution channels are typically a mix of direct sales to large utility clients, indirect sales through a network of specialized distributors and system integrators, and sometimes through electrical contractors who serve smaller industrial and commercial customers. Effective logistics and a strong sales network are crucial for market penetration and customer reach, particularly in geographically diverse regions.

The distribution channels, encompassing both direct and indirect approaches, play a pivotal role in bringing distribution surge arresters to their end-users. Direct sales involve manufacturers engaging directly with major utility companies, large industrial complexes, and governmental infrastructure projects, often requiring customized solutions, technical support, and long-term service agreements. This approach allows for direct feedback and stronger customer relationships. Indirect channels involve collaboration with a network of authorized distributors, wholesalers, and electrical equipment suppliers who cater to a broader range of smaller utilities, industrial buyers, commercial clients, and electrical contractors. These intermediaries provide localized inventory, sales support, and installation services, significantly expanding market reach and ensuring timely product availability. The selection of appropriate distribution channels is vital for optimizing market presence, ensuring efficient delivery, and maintaining competitive pricing strategies across different market segments.

The primary potential customers and end-users of distribution surge arresters are diverse, spanning across critical sectors that rely heavily on stable and uninterrupted electrical power. The most significant customer base comprises public and private utility companies involved in the transmission and distribution of electricity. These entities are consistently investing in surge arresters to protect their extensive network infrastructure, including power lines, transformers, substations, and switchgear, from atmospheric overvoltages and switching surges. Their overarching objective is to ensure grid stability, minimize power outages, protect substantial capital investments, and maintain high service reliability for their vast consumer base, making them perpetual buyers of these essential protection devices as grids expand and age.

Beyond utilities, a substantial segment of potential customers includes industrial enterprises that operate complex machinery and sensitive electronic control systems. Industries such as manufacturing, oil and gas, mining, chemical processing, automotive, and data centers are highly susceptible to economic losses from equipment damage and production downtime caused by transient overvoltages. For these end-users, surge arresters are critical for safeguarding expensive automation equipment, motors, Variable Frequency Drives (VFDs), Programmable Logic Controllers (PLCs), and critical data infrastructure. The cost of downtime in these sectors can be astronomical, thus justifying investments in advanced surge protection solutions to ensure continuous operation and protect valuable assets from electrical disturbances.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.75 Billion |

| Market Forecast in 2032 | USD 3.00 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, Eaton Corporation plc, Hubbell Inc., General Electric Company, CG Power and Industrial Solutions Limited, Raychem RPG (P) Ltd., Fuji Electric Co., Ltd., Toshiba Corporation, Meidensha Corporation, Littelfuse, Inc., Mersen Corporate, N.V. (Novagard), DEHN + S脰HNE GmbH + Co KG, Schneider Electric SE, Zotup S.p.A., Winsted Group, Emico, Inc., TE Connectivity, Streamer Electric. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Distribution Surge Arrester Market is characterized by a dynamic and evolving technology landscape, driven by continuous innovation aimed at enhancing performance, reliability, and smart grid compatibility. At the core of modern surge arrester technology lies the Metal Oxide Varistor (MOV), which is primarily composed of zinc oxide grains with specific additives. The advanced fabrication techniques for MOV blocks are crucial, focusing on improving their energy absorption capability, stability under repetitive surges, and very low residual voltage characteristics. Research is continuously directed towards refining the composition and sintering processes of MOVs to achieve even higher performance metrics, enabling arresters to handle increasingly severe overvoltage events while maintaining a longer operational life. The quality and consistency of these MOV blocks are paramount to the arrester's effectiveness and reliability in diverse electrical environments.

Beyond the core MOV technology, significant advancements are observed in housing materials and overall arrester design. Polymer-housed arresters, predominantly utilizing silicone rubber, represent a key technological shift from traditional porcelain. These composite housings offer superior tracking and erosion resistance, excellent hydrophobicity, light weight, and a significantly lower risk of explosive failure, enhancing safety for both personnel and equipment. Manufacturers are also integrating smart features into surge arresters, incorporating sensors for real-time monitoring of leakage current, temperature, and surge events. These smart arresters can communicate data wirelessly to central control systems, enabling predictive maintenance, fault localization, and comprehensive grid health monitoring, aligning with the broader objectives of smart grid infrastructure development and operational efficiency improvements for utilities.

Further technological advancements include the development of gapless surge arresters, which offer continuous protection without the need for series gaps, thereby improving response time and energy handling capabilities. The integration of fiber optic sensors for enhanced insulation monitoring and advanced diagnostic tools for assessing arrester health in-situ are also gaining traction. Furthermore, there is a growing emphasis on modular designs and compact form factors to facilitate easier installation and replacement, especially in space-constrained applications. The confluence of these innovations, from material science to digital integration, is shaping a new generation of distribution surge arresters that are not only more protective but also intelligent, environmentally resilient, and integral components of future-proof electrical distribution networks, contributing significantly to grid stability and operational excellence.

A distribution surge arrester is a critical protective device designed to safeguard electrical equipment and distribution networks from damaging overvoltages. These overvoltages, often caused by lightning strikes, switching operations within the grid, or faults, can severely damage transformers, circuit breakers, cables, and other sensitive components, leading to extensive power outages and significant repair costs. The arrester works by diverting the excess current from a surge safely to the ground, thus limiting the voltage to a safe level and ensuring the continued integrity and operational reliability of the entire power distribution system. Its essentiality stems from its role in preventing equipment failure, minimizing downtime, and enhancing the overall resilience and safety of electrical infrastructure, making it an indispensable component for maintaining a stable and uninterrupted power supply in both urban and rural settings.

Polymer-housed surge arresters, typically made with silicone rubber composites, offer several distinct advantages over traditional porcelain-housed arresters. Firstly, they are significantly lighter, making them easier and safer to handle and install, which reduces labor costs and logistical challenges. Secondly, polymer housings possess superior hydrophobicity, meaning they repel water effectively, which prevents flashovers and ensures better performance in polluted or humid environments where porcelain can suffer from surface contamination and degradation. Thirdly, polymer arresters are inherently explosion-proof and less prone to shattering under internal faults or external impacts, enhancing safety for utility personnel and preventing secondary damage. While porcelain arresters have a long history of proven reliability and mechanical strength, the flexibility, durability, and enhanced safety features of polymer-housed arresters make them the preferred choice for modern distribution networks, contributing to improved grid resilience and lower lifecycle costs for utilities and industrial users.

The voltage level is a primary determinant in the selection and application of distribution surge arresters, as it directly relates to the energy handling capacity and insulation coordination required for effective protection. Surge arresters are specifically designed and rated for different voltage ranges: low voltage (up to 1 kV), medium voltage (1 kV to 72.5 kV), and high voltage (above 72.5 kV). Low voltage arresters protect end-user equipment and service entrances, while medium voltage arresters are crucial for primary and secondary distribution lines, transformers, and switchgear in utility and industrial settings, representing the largest market segment due to their widespread application. High voltage arresters are utilized in transmission substations to safeguard critical EHV assets. Selecting an arrester with an appropriate voltage rating is paramount; an under-rated arrester may fail to provide adequate protection, while an over-rated one could be uneconomical and potentially less effective. Proper selection ensures optimal protection, system reliability, and cost-efficiency across various segments of the electrical grid infrastructure.

The increasing integration of renewable energy sources, such as solar and wind power, significantly influences and drives the demand for distribution surge arresters. Renewable energy installations often introduce new complexities and potential vulnerabilities into the electrical grid. For instance, solar farms and wind turbines are frequently located in remote, exposed areas, making them highly susceptible to lightning strikes and other atmospheric overvoltages. Furthermore, the intermittent nature of renewables, combined with power electronic converters used for grid interconnection, can generate switching surges and harmonics, increasing the risk of transient overvoltages within the distribution network. To protect the sensitive and costly equipment associated with these installations, including inverters, converters, and transformers, a robust surge protection strategy is essential. Consequently, the global shift towards green energy mandates greater deployment of advanced distribution surge arresters, ensuring the reliability, longevity, and safe operation of these vital renewable energy assets and their seamless integration into the existing grid infrastructure.

The market for smart distribution surge arresters is primarily driven by the overarching need for enhanced grid reliability, operational efficiency, and the broader push towards intelligent, self-healing smart grids. Key driving factors include the escalating demand for predictive maintenance capabilities, which allow grid operators to monitor the real-time health and performance of arresters, anticipating failures before they occur and minimizing unplanned outages. The integration of communication modules enables these smart devices to transmit data wirelessly, providing valuable insights into surge events, leakage currents, and operational temperatures. Benefits to grid operators are substantial: they gain real-time visibility into grid conditions, enabling faster fault identification and isolation, optimized maintenance schedules, and improved asset management. This leads to significant reductions in operational costs, prolonged equipment lifespan, enhanced safety for personnel, and ultimately, a more stable, resilient, and responsive power distribution system that can adapt to modern challenges and higher reliability expectations from consumers. The data collected from smart arresters also feeds into AI-driven analytics for long-term grid optimization strategies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.