ID : MRU_ 427888 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

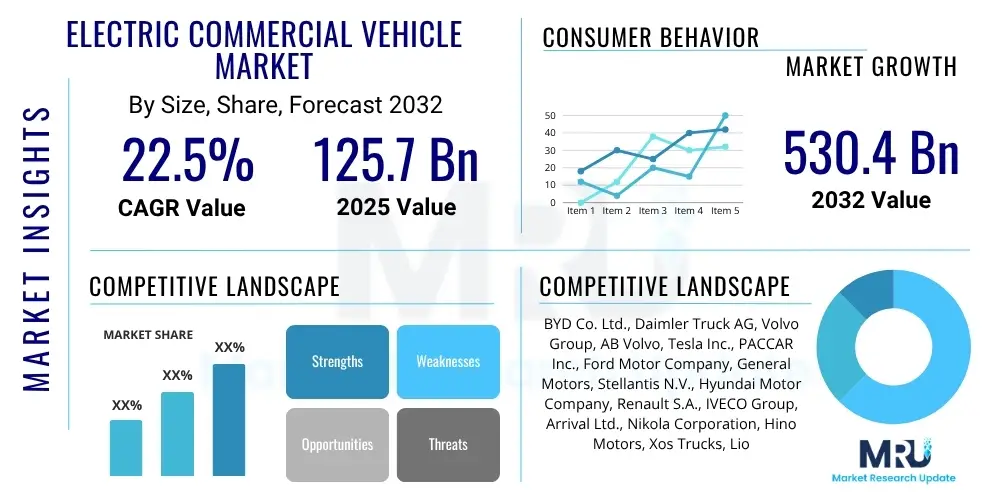

The Electric Commercial Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2032, reflecting a significant transition towards sustainable transportation solutions driven by global decarbonization efforts and technological advancements. The market is estimated at USD 125.7 billion in 2025 and is projected to reach USD 530.4 billion by the end of the forecast period in 2032. This robust growth trajectory is underpinned by increasing demand from logistics, public transportation, and last-mile delivery sectors, alongside supportive government policies and incentives aimed at accelerating EV adoption. The economic viability of electric commercial vehicles is also improving due to declining battery costs and enhanced performance metrics, making them increasingly competitive with traditional internal combustion engine (ICE) vehicles.

The expansion of the electric commercial vehicle market is further fueled by growing environmental consciousness among businesses and consumers, stringent emissions regulations, and the rising cost of fossil fuels, all contributing to a compelling business case for electrification. Innovations in battery technology, charging infrastructure, and vehicle design are pivotal in overcoming historical barriers such as range anxiety and charging times, thereby broadening the operational scope and appeal of electric commercial vehicles across various industries. This market evolution signifies a fundamental shift in commercial fleet management strategies, prioritizing operational efficiency, reduced environmental footprint, and long-term cost savings through electrification.

The Electric Commercial Vehicle (ECV) market encompasses a wide array of vehicles, including vans, trucks, and buses, designed for commercial purposes and powered by electricity, primarily through battery electric vehicle (BEV) technology, but also including fuel cell electric vehicles (FCEV) and plug-in hybrid electric vehicles (PHEV). These vehicles are characterized by their zero tailpipe emissions, reduced noise pollution, and lower operating costs compared to their traditional internal combustion engine (ICE) counterparts, making them an increasingly attractive solution for urban logistics, public transport, and various industrial applications. Product descriptions emphasize their advanced powertrain systems, regenerative braking capabilities, and often sophisticated telematics for fleet management, aimed at optimizing performance, efficiency, and safety. Major applications span last-mile delivery services, inter-city logistics, waste management, construction, and passenger transport, where their environmental benefits and operational efficiencies are particularly impactful. The core benefits include significant reductions in carbon footprint, lower fuel and maintenance costs due to fewer moving parts, enhanced driver comfort from quieter operation, and compliance with escalating environmental regulations in urban centers. Driving factors for market growth are multifaceted, incorporating stringent government emission standards, attractive purchase subsidies and tax incentives, corporate sustainability goals, advancements in battery energy density and charging infrastructure, and the growing demand for efficient, clean, and quiet delivery solutions, particularly in rapidly urbanizing regions. This collective impetus is propelling the ECV market into a phase of rapid expansion and technological innovation, transforming the landscape of commercial transportation.

The Electric Commercial Vehicle (ECV) market is currently experiencing unprecedented growth, propelled by a confluence of evolving business trends, significant regional initiatives, and dynamic segment shifts across the industry. Business trends are largely characterized by a pronounced corporate focus on Environmental, Social, and Governance (ESG) principles, compelling major logistics and transportation companies to electrify their fleets to meet sustainability targets and improve brand image. Furthermore, the increasing adoption of e-commerce and the resultant surge in last-mile delivery services are driving demand for agile, efficient, and emission-free light commercial electric vehicles. Companies are increasingly investing in proprietary charging infrastructure and smart fleet management systems to maximize operational efficiencies and reduce total cost of ownership (TCO). Regional trends reveal Europe and Asia-Pacific leading the charge, driven by aggressive regulatory frameworks, substantial government incentives, and robust public charging networks; countries like China and those within the European Union are at the forefront of ECV adoption, with North America rapidly catching up due to increasing corporate commitments and federal support. In contrast, emerging markets in Latin America, the Middle East, and Africa are showing nascent but accelerating growth, spurred by similar environmental concerns and the potential for leapfrogging traditional fossil fuel infrastructure. Segment trends indicate a strong initial focus on light commercial vehicles (LCVs) for urban delivery, but significant advancements are now observed in medium and heavy-duty electric trucks and buses, as battery technology improves and operational challenges related to range and payload are systematically addressed. Public transportation is undergoing a substantial transformation with electric buses becoming commonplace in major cities worldwide, while the development of long-haul electric trucks, including those powered by hydrogen fuel cells, is gaining momentum, signaling a comprehensive electrification across all commercial vehicle categories. These overarching trends collectively underscore a vibrant and rapidly maturing market poised for sustained expansion and innovation.

The integration of Artificial Intelligence (AI) is fundamentally transforming the Electric Commercial Vehicle (ECV) market by enhancing operational efficiency, optimizing vehicle performance, and revolutionizing fleet management. Common user questions related to AI's impact often revolve around how AI can improve battery life, reduce maintenance costs, optimize delivery routes, and enable autonomous driving capabilities. Users are keen to understand the tangible benefits AI brings to fleet owners in terms of cost savings, increased safety, and environmental sustainability, as well as the challenges associated with data management, system integration, and cybersecurity. The key themes emerging from this analysis include AI's role in predictive maintenance, smart energy management, route optimization, and the eventual realization of autonomous commercial transport, all geared towards making ECVs more reliable, efficient, and economically viable, while addressing concerns about job displacement and the complexity of adoption within existing logistical frameworks.

The Electric Commercial Vehicle (ECV) market is profoundly shaped by a dynamic interplay of drivers, restraints, opportunities, and various impact forces that collectively dictate its growth trajectory and adoption rate. Key drivers propelling the market forward include increasingly stringent government emission regulations, such as those implemented in Europe and California, which necessitate a shift away from fossil fuel-powered vehicles, coupled with substantial government incentives, subsidies, and tax benefits designed to reduce the high upfront cost of ECVs for fleet operators. Furthermore, growing corporate sustainability initiatives, consumer demand for eco-friendly logistics, and the significant operational cost savings derived from lower fuel prices (electricity vs. diesel) and reduced maintenance requirements due to simpler electric powertrains are powerful motivators. However, several significant restraints challenge rapid market expansion, primarily the high initial purchase price of ECVs compared to their ICE counterparts, which can be a barrier for smaller businesses. Limited charging infrastructure, especially for heavy-duty vehicles requiring high-power fast chargers, and range anxiety among fleet managers, particularly for long-haul operations, present considerable operational hurdles. Moreover, the weight of battery packs can sometimes reduce payload capacity, and the availability of specialized technicians for ECV maintenance is still developing. Despite these challenges, the market is rife with opportunities stemming from continuous advancements in battery technology, leading to higher energy density, faster charging capabilities, and decreasing costs, alongside the expansion of dedicated charging networks facilitated by public and private investments. The burgeoning last-mile delivery sector, the electrification of public transport fleets, and the emergence of innovative business models like battery-as-a-service (BaaS) and vehicle-to-grid (V2G) solutions offer significant avenues for growth. Impact forces, such as fluctuating raw material prices for batteries (e.g., lithium, cobalt), geopolitical tensions affecting supply chains, and evolving energy policies, exert considerable influence on market dynamics, necessitating adaptive strategies from manufacturers and operators alike. Additionally, the development of robust regulatory frameworks for autonomous electric commercial vehicles and data privacy concerns associated with connected vehicle technologies represent critical impact forces that will shape the future landscape of the ECV market. This complex interplay of forces ensures a continuously evolving and highly competitive market environment for electric commercial vehicles.

The Electric Commercial Vehicle market is meticulously segmented to provide a granular understanding of its diverse components, applications, and technological underpinnings, enabling stakeholders to identify specific growth areas and tailor strategies effectively. This comprehensive segmentation allows for an in-depth analysis of market dynamics, revealing varying adoption rates and preferences across different vehicle types, propulsion technologies, and end-use industries. Understanding these segments is crucial for manufacturers to optimize product development, for policymakers to design targeted incentives, and for fleet operators to make informed investment decisions, ultimately accelerating the overall transition to electric mobility in the commercial sector.

A comprehensive value chain analysis for the Electric Commercial Vehicle (ECV) market reveals a complex network of interconnected activities, starting from raw material extraction to end-user deployment and after-sales service, highlighting critical stages where value is added and competitive advantages are forged. The upstream analysis focuses on the sourcing and processing of essential raw materials, particularly for batteries, including lithium, cobalt, nickel, and graphite, alongside the production of electric motors, power electronics, and specialized chassis components. This stage involves mining companies, chemical processing plants, and component manufacturers, where innovation in material science and efficient sourcing strategies are paramount for cost control and supply chain resilience. Moving downstream, the value chain progresses through the manufacturing and assembly of ECVs, encompassing traditional automotive OEMs, specialized EV manufacturers, and emerging technology firms. This stage integrates components from upstream suppliers, involves sophisticated manufacturing processes, and emphasizes modular design for efficiency and scalability. Distribution channels play a crucial role in bringing ECVs to market, comprising both direct and indirect models; direct channels involve manufacturers selling directly to large fleet operators or through online platforms, offering greater control over customer experience and pricing, while indirect channels leverage established dealerships, distributors, and leasing companies that provide widespread market access, financing options, and localized support. The after-sales segment, including maintenance, repair, spare parts supply, and battery recycling or second-life applications, completes the value chain, ensuring sustained operational efficiency and maximizing the lifecycle value of ECVs. Understanding the intricate relationships and dependencies across these stages is critical for identifying areas for cost optimization, fostering innovation, and building robust, sustainable supply networks within the rapidly evolving ECV market.

The Electric Commercial Vehicle (ECV) market targets a diverse and expanding base of end-users and buyers, spanning various industries and operational scales, all seeking to leverage the environmental, operational, and financial benefits of electrification. Potential customers primarily include large logistics and parcel delivery companies, which are increasingly under pressure to reduce their carbon footprint and optimize last-mile delivery operations, finding ECV vans and light trucks ideal for urban environments due to lower operating costs and quiet operation. Public transportation authorities and municipal governments represent another significant customer segment, driven by mandates to electrify their bus fleets to improve air quality and achieve sustainability targets within city limits. Waste management and utility companies are progressively adopting electric refuse trucks and service vehicles, benefiting from reduced noise pollution in residential areas and significant fuel savings, despite higher upfront costs. Construction and mining sectors are emerging as strong potential customers, with a growing interest in heavy-duty electric and fuel cell vehicles that offer high torque, reduced emissions at job sites, and lower operational expenses in demanding environments. Additionally, port and airport operators are increasingly investing in electric tugs, forklifts, and ground support equipment to enhance operational efficiency and comply with strict emissions regulations in controlled areas. Smaller businesses and independent contractors engaged in local delivery, mobile services, and short-haul logistics also constitute a growing customer base, often attracted by government incentives and the long-term economic advantages of electric vehicles. This broad spectrum of buyers, united by a common drive for efficiency, sustainability, and compliance, underscores the immense and multifaceted potential for growth within the Electric Commercial Vehicle market, necessitating tailored product offerings and supportive ecosystem development to meet their varied operational requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 125.7 Billion |

| Market Forecast in 2032 | USD 530.4 Billion |

| Growth Rate | 22.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BYD Co. Ltd., Daimler Truck AG, Volvo Group, AB Volvo, Tesla Inc., PACCAR Inc., Ford Motor Company, General Motors, Stellantis N.V., Hyundai Motor Company, Renault S.A., IVECO Group, Arrival Ltd., Nikola Corporation, Hino Motors, Xos Trucks, Lion Electric Company, Rivian Automotive, Scania AB, Workhorse Group Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Electric Commercial Vehicle (ECV) market is continually reshaped by a rapidly evolving technological landscape, with innovations focused on enhancing vehicle performance, extending range, reducing charging times, and improving overall operational efficiency and safety. At the forefront are advancements in battery technology, primarily lithium-ion batteries, which are seeing significant improvements in energy density, power output, and lifespan, alongside reductions in cost and weight, crucial for enabling longer ranges and heavier payloads for commercial applications. Emerging battery chemistries, such as solid-state batteries and lithium-iron phosphate (LFP) variants, promise further breakthroughs in safety, thermal stability, and cycle life. Electric motor technology is also advancing, with the development of more efficient, compact, and powerful permanent magnet synchronous motors (PMSM) and asynchronous induction motors, optimized for the rigorous demands of commercial operations. Power electronics, including inverters, converters, and onboard chargers, are becoming more sophisticated, improving energy management, thermal efficiency, and overall system integration. Significant strides are also being made in fast-charging infrastructure, with higher power DC fast chargers (e.g., 350 kW and beyond) and innovative charging solutions like pantograph charging for buses and wireless charging systems gaining traction, addressing the critical challenge of vehicle downtime. Beyond core powertrain components, vehicle-to-grid (V2G) technology is gaining importance, allowing ECVs to return surplus energy to the grid during peak demand, providing revenue opportunities for fleet operators and supporting grid stability. Telematics and fleet management systems, heavily leveraging IoT and AI, are integral, offering real-time data on vehicle performance, driver behavior, energy consumption, and predictive maintenance, thereby optimizing routes and operational costs. Furthermore, the development of advanced driver-assistance systems (ADAS) and autonomous driving technologies specifically tailored for commercial vehicles is progressing, promising enhanced safety, reduced driver fatigue, and the potential for fully autonomous logistics in the future. Fuel cell technology, particularly for heavy-duty long-haul trucks, represents a key alternative propulsion avenue, with ongoing research focused on improving fuel cell stack efficiency, hydrogen storage solutions, and establishing a robust hydrogen refueling infrastructure. These interconnected technological developments collectively drive the evolution of the ECV market, making electric commercial vehicles more competitive, functional, and economically viable across a broader spectrum of applications.

The primary advantage of electric commercial vehicles (ECVs) is their significantly lower operating costs, driven by cheaper electricity compared to diesel and substantially reduced maintenance requirements due to fewer moving parts in electric powertrains. Additionally, ECVs offer zero tailpipe emissions, contributing to cleaner air and meeting stringent environmental regulations, particularly beneficial for urban operations.

The availability and accessibility of robust charging infrastructure are critical for widespread ECV adoption. Inadequate charging options, especially for heavy-duty vehicles requiring high-power fast chargers, can lead to range anxiety and operational disruptions. Development of public, private, and dedicated fleet charging solutions is essential to support the growing demand and ensure seamless operations for electric fleets.

Government incentives play a crucial role in promoting the ECV market by addressing the higher upfront costs. These include purchase subsidies, tax credits, preferential vehicle registration, exemptions from road tolls, and dedicated funding for charging infrastructure development. Local and national governments also introduce emission regulations and mandates for fleet electrification, indirectly incentivizing ECV adoption.

Battery technology is pivotal for the future of ECVs, directly influencing range, payload capacity, charging speed, and overall vehicle cost. Ongoing advancements in energy density, power output, durability, and cost reduction of battery cells (e.g., solid-state, LFP) are essential for making ECVs more competitive, expanding their application scope, and addressing performance limitations for heavy-duty and long-haul operations.

Asia Pacific, particularly China, and Europe are leading in ECV adoption due to stringent emission regulations, substantial government support and incentives, rapid deployment of charging infrastructure, and a strong focus on urban air quality and sustainability. These regions have actively fostered an ecosystem conducive to the manufacturing, deployment, and operation of electric commercial fleets across various segments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.