ID : MRU_ 427419 | Date : Oct, 2025 | Pages : 254 | Region : Global | Publisher : MRU

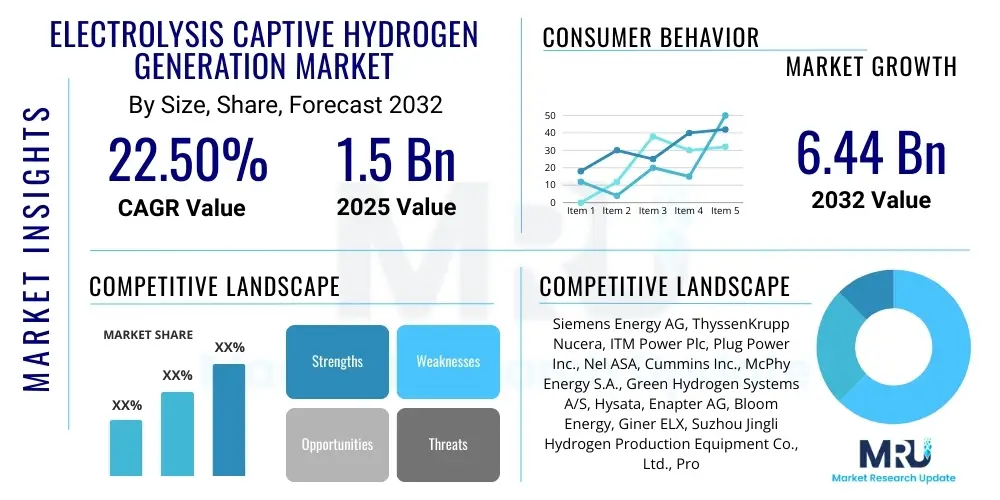

The Electrolysis Captive Hydrogen Generation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2032. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 6.44 Billion by the end of the forecast period in 2032.

The Electrolysis Captive Hydrogen Generation Market signifies a pivotal shift in industrial hydrogen sourcing, moving from centralized production and complex logistical supply chains to on-site, demand-driven generation. This market primarily involves the deployment of electrolyzer technologies, such as Alkaline, Proton Exchange Membrane (PEM), and Solid Oxide Electrolyzer Cells (SOEC), which leverage electricity to split water into pure hydrogen and oxygen. The hydrogen produced is then immediately consumed by the host industrial facility, serving critical roles as a chemical feedstock, a reducing agent, or a fuel. This approach is gaining immense traction due to its inherent advantages in efficiency, security of supply, and environmental sustainability, particularly when the electricity source is renewable.

Major applications for captive hydrogen generation span across a diverse range of heavy industries. Petroleum refining relies on hydrogen for hydrotreating and hydrocracking processes to remove impurities and upgrade fuels. The chemical sector, including the production of ammonia for fertilizers and methanol for various industrial chemicals, represents another substantial application area. Furthermore, the burgeoning green steel industry is increasingly adopting on-site hydrogen production to replace coal-based reducing agents, aligning with global decarbonization efforts. The electronics sector, demanding ultra-high purity hydrogen for semiconductor manufacturing, also benefits significantly from controlled, on-site generation.

The benefits of this localized production model are manifold. Industries achieve enhanced energy independence by reducing reliance on external hydrogen suppliers, mitigating supply chain risks and price volatility. Environmentally, when coupled with renewable energy sources like solar or wind power, captive electrolysis enables the production of "green hydrogen," drastically cutting carbon emissions associated with traditional hydrogen production methods. Key driving factors for market expansion include the global imperative for decarbonization, stringent environmental regulations pushing for cleaner industrial processes, rapidly declining costs of renewable energy, and supportive government policies and incentives promoting hydrogen economies. These elements collectively foster a robust growth trajectory for the electrolysis captive hydrogen generation sector.

The Electrolysis Captive Hydrogen Generation Market is undergoing a transformative phase, propelled by the urgent global agenda for decarbonization and the increasing emphasis on energy sovereignty. Current business trends indicate a strong move towards strategic alliances and joint ventures between electrolyzer manufacturers, renewable energy developers, and large industrial consumers. This collaborative ecosystem facilitates integrated solutions, from renewable power generation to on-site hydrogen utilization, streamlining project deployment and de-risking investments. Furthermore, there is a clear trend towards modular and scalable electrolyzer systems, enabling industries to tailor their hydrogen production capacities precisely to operational demands, thereby optimizing capital expenditure and operational flexibility. Digitalization and automation are also key, with integrated control systems enhancing efficiency and ensuring seamless operation within complex industrial environments.

Regional trends reveal distinct patterns of market leadership and emerging growth. Europe and North America are at the forefront, driven by comprehensive government support mechanisms, such as the European Green Deal and the U.S. Inflation Reduction Act, which provide substantial funding and tax credits for green hydrogen projects. These regions boast mature industrial infrastructures and ambitious climate targets, accelerating the adoption of captive hydrogen solutions in sectors like refining, chemicals, and steel. Asia-Pacific is rapidly emerging as a significant growth engine, with countries like China, Japan, South Korea, and India investing heavily in hydrogen technology and infrastructure, spurred by massive industrial expansion and increasing energy demand, coupled with evolving national hydrogen strategies aimed at reducing reliance on fossil fuels.

Segmentation trends highlight the increasing preference for advanced electrolyzer technologies that can efficiently integrate with intermittent renewable energy sources. Proton Exchange Membrane (PEM) electrolyzers are experiencing rapid growth due to their dynamic response capabilities and compact footprint, making them ideal for fluctuating power inputs. Alkaline electrolyzers continue to hold a substantial market share owing to their proven reliability and lower initial investment costs for steady-state applications. Solid Oxide Electrolyzer Cells (SOEC) are garnering attention for their high-efficiency potential when coupled with industrial waste heat or high-temperature steam, promising significant energy savings in specific industrial contexts. The application landscape is broadening beyond traditional refining and ammonia production to include green steel, synthetic fuels, and advanced manufacturing, underscoring the versatility and growing importance of captive hydrogen generation in the future industrial landscape.

User inquiries regarding AIs impact on captive hydrogen generation frequently center on optimizing operational efficiency, enhancing predictive maintenance, and integrating intelligent energy management systems. Users are keen to understand how AI can reduce energy consumption in electrolysis, improve electrolyzer lifespan through proactive fault detection, and optimize hydrogen production schedules based on real-time energy prices and demand fluctuations. Expectations also include AIs role in accelerating R&D for novel materials and designs, streamlining regulatory compliance, and facilitating the seamless integration of intermittent renewable energy sources, thereby making on-site hydrogen production more reliable, cost-effective, and sustainable.

The Electrolysis Captive Hydrogen Generation Market is predominantly driven by the global imperative to achieve net-zero carbon emissions, compelling industries to seek cleaner alternatives to fossil fuel-derived hydrogen. A significant driver is the dramatic decline in the cost of renewable energy, making green hydrogen production increasingly economically viable. Government policies worldwide, including subsidies, tax incentives, and mandates for green hydrogen adoption, play a crucial role in accelerating investment and deployment. Furthermore, the inherent benefits of on-site production, such as enhanced energy security, reduced logistical complexities, and greater control over hydrogen supply, resonate strongly with industrial end-users seeking operational resilience and independence from fluctuating external market prices. The growing demand for green products, like green steel and sustainable chemicals, further fuels this market as industries strive to meet consumer and regulatory expectations for environmental responsibility.

Despite the strong tailwinds, several restraints temper the markets growth trajectory. The most prominent is the high initial capital expenditure (CAPEX) associated with installing electrolyzer systems and integrating them into existing industrial infrastructure. While operational costs are decreasing, green hydrogen can still be more expensive than traditional grey hydrogen in some regions, creating an economic barrier to widespread adoption, especially for facilities without access to abundant, low-cost renewable electricity. Technical challenges also exist, particularly in managing the intermittency of renewable energy sources and integrating them seamlessly with continuous industrial processes, requiring advanced control systems and potentially energy storage solutions. Supply chain bottlenecks for critical materials and components, along with a shortage of skilled personnel for design, installation, and maintenance, pose additional hurdles that need to be addressed for sustained market expansion.

Opportunities within the Electrolysis Captive Hydrogen Generation Market are vast and rapidly evolving. Continuous technological advancements are leading to more efficient, durable, and cost-effective electrolyzer designs, including innovations in catalysts, membranes, and balance of plant components. The development of advanced energy management systems and grid integration solutions will further enhance the economic viability of pairing electrolysis with variable renewable energy. Expanding applications into new sectors such as maritime fuels (e-ammonia, e-methanol), aviation (sustainable aviation fuels), and district heating presents significant growth avenues. The strategic impact forces shaping this market include stringent environmental regulations and carbon pricing mechanisms that increasingly penalize fossil-fuel-based production, thereby incentivizing green alternatives. Technological innovation is constantly pushing the boundaries of what is possible, driving down costs and improving performance. Geopolitical shifts are also influential, as nations prioritize energy independence and secure domestic hydrogen supply chains, reducing reliance on volatile international energy markets. These powerful forces are collectively transforming the industrial hydrogen landscape, positioning captive electrolysis as a cornerstone of future sustainable economies.

The Electrolysis Captive Hydrogen Generation Market is meticulously segmented to offer a granular understanding of its diverse components and drivers. This comprehensive analysis considers various dimensions, including the specific technology employed, the end-use application of the generated hydrogen, and the particular industrial sector serving as the end-user. Each segmentation category provides unique insights into market dynamics, enabling stakeholders to identify niches, assess competitive landscapes, and formulate targeted strategic initiatives. Understanding these distinct segments is crucial for forecasting growth trends and pinpointing areas of significant investment and innovation within the broader hydrogen economy.

Within the technology segment, distinctions are made based on the underlying electrochemical principles and operational characteristics of different electrolyzer types, which directly influence their suitability for various applications and integration with power sources. The application segment delineates the myriad uses of on-site generated hydrogen, from foundational chemical processes to emerging green manufacturing techniques. Meanwhile, the end-user industry segmentation categorizes the diverse sectors that consume captive hydrogen, recognizing that each industry possesses unique hydrogen purity requirements, consumption patterns, and decarbonization pathways, thereby impacting their adoption rates and technological preferences. This layered approach ensures a holistic view of the markets structure and potential.

The value chain for the Electrolysis Captive Hydrogen Generation Market commences with the crucial upstream segment, which involves the research, development, and manufacturing of core components essential for electrolyzer systems. This includes specialized electrodes, ion-exchange membranes (for PEM and AEM), catalysts (often involving platinum group metals for PEM), power electronics, and various balance of plant (BoP) equipment such as purifiers, compressors, and control systems. Key players in this stage are material scientists, chemical companies, and specialized component manufacturers. The quality and cost-effectiveness of these upstream components directly impact the overall efficiency and economic viability of the entire hydrogen production system. Furthermore, the sourcing of critical raw materials, often with complex global supply chains, is a vital consideration in this initial phase.

The midstream segment of the value chain focuses on the integration and assembly of these components into complete, operational electrolyzer modules and systems. This involves engineering, procurement, and construction (EPC) firms that design, build, and commission the on-site hydrogen generation facilities. System integrators play a critical role here, ensuring seamless compatibility between various components and optimal performance. This stage also encompasses the development of sophisticated control systems that manage the electrolysis process, integrate with renewable energy inputs, and ensure safety standards are met. Given the customized nature of captive generation, tailored engineering solutions are often required to fit specific industrial site requirements and operational demands, ranging from megawatt-scale to multi-gigawatt installations.

The downstream segment primarily centers on the direct and immediate utilization of the generated hydrogen by the industrial end-user, which is the defining characteristic of "captive" generation. This produced hydrogen is channeled directly into the customers manufacturing processes, such as petrochemical refining, ammonia synthesis, or steel reduction, eliminating the need for external distribution logistics like trucking or pipelines. Distribution channels are thus predominantly direct, with manufacturers or EPC companies delivering and installing systems directly for the end-user. However, indirect channels involve technology licensors, consultancy firms, and energy service providers who facilitate the adoption and operation of these systems. The value chains emphasis is squarely on local, just-in-time supply, maximizing operational efficiency and minimizing the environmental footprint associated with hydrogen transportation and storage, thereby reinforcing the economic and ecological benefits of the captive model.

The primary and most significant potential customers for Electrolysis Captive Hydrogen Generation solutions are large industrial enterprises characterized by substantial, continuous demand for hydrogen and a strategic imperative to decarbonize their operations. This category prominently includes the petroleum refining sector, which utilizes vast quantities of hydrogen for hydrotreating and hydrocracking processes to remove impurities from crude oil and upgrade fuel products. These facilities are often major emitters of carbon dioxide, and on-site green hydrogen offers a direct pathway to significantly reduce their environmental footprint and comply with increasingly stringent environmental regulations. The scale of their hydrogen consumption makes captive generation an economically attractive and strategically sound investment.

Another crucial customer segment is the chemical manufacturing industry, particularly producers of ammonia, methanol, and other specialty chemicals. Hydrogen serves as a fundamental feedstock in these processes. As global demand for fertilizers (ammonia) and various industrial chemicals (methanol) continues to grow, and pressure mounts to produce these substances sustainably, captive green hydrogen becomes an indispensable solution. Beyond these established sectors, the burgeoning green steel industry represents an enormous emerging market. Traditional steelmaking is highly carbon-intensive, and the transition to hydrogen-based direct reduced iron (DRI) processes requires massive, continuous supplies of hydrogen, making on-site generation a critical enabler for sustainable steel production.

Furthermore, niche but high-value customer segments include the electronics industry, specifically semiconductor manufacturers, which require ultra-high purity hydrogen for various fabrication steps, benefiting from the controlled and consistent supply of captive generation. The food and beverage sector utilizes hydrogen for hydrogenation processes, and the pharmaceutical industry employs it in various synthesis routes, both seeking reliable and pure sources. Essentially, any industrial operation that consumes hydrogen as a critical input, aims to enhance its energy independence, mitigate supply chain risks, and aggressively pursue sustainability targets, is a prime candidate for adopting on-site electrolytic hydrogen generation. The appeal is particularly strong for industries located in regions with abundant and affordable renewable energy resources, where the economic case for green hydrogen is most compelling.

The technology landscape for Electrolysis Captive Hydrogen Generation is characterized by a rapidly evolving array of electrochemical systems, each with distinct advantages and operational profiles. The market is primarily underpinned by three main electrolyzer technologies: Alkaline, Proton Exchange Membrane (PEM), and Solid Oxide Electrolyzer Cells (SOEC). Alkaline electrolyzers, a mature technology, are known for their robustness, longevity, and lower capital costs, making them suitable for large-scale, steady-state hydrogen production where stable power inputs are available. They typically operate with a liquid electrolyte (e.g., potassium hydroxide) and can achieve high efficiencies, making them a foundational choice for many industrial applications. Continued innovation in alkaline systems focuses on increasing current density and improving material durability to further enhance their cost-effectiveness and performance.

Proton Exchange Membrane (PEM) electrolyzers represent a rapidly growing segment, distinguished by their compact design, high current densities, and exceptional ability to respond quickly to dynamic power inputs, making them ideal for integration with intermittent renewable energy sources like solar and wind. PEM systems use a solid polymer electrolyte membrane and require expensive platinum group metal catalysts, which contribute to higher capital costs compared to alkaline systems. However, their operational flexibility, ability to produce high-purity hydrogen directly, and smaller footprint are significant advantages that are driving widespread adoption in various industrial and mobility applications. Ongoing research aims to reduce the reliance on precious metals and improve the overall efficiency and lifespan of PEM stacks.

Solid Oxide Electrolyzer Cells (SOEC) are an advanced, high-temperature electrolysis technology that operates at temperatures between 500-1000°C. This high operating temperature allows for highly efficient conversion of steam (water vapor) into hydrogen, often leveraging waste heat from industrial processes or nuclear power plants. SOECs demonstrate the highest potential for electrical efficiency among current technologies, particularly when co-electrolyzing CO2 to produce syngas, opening avenues for power-to-X applications. While still largely in the development and demonstration phase for large-scale industrial deployment, SOECs hold immense promise for the future of low-cost, high-efficiency green hydrogen production. Additionally, Anion Exchange Membrane (AEM) electrolyzers are emerging as a promising hybrid technology, aiming to combine the benefits of alkaline systems (low-cost materials, no precious metals) with the dynamic operation and compact design of PEM systems, making them a significant area of research and development for future market disruption.

Electrolysis captive hydrogen generation refers to the on-site production of hydrogen gas through the process of electrolysis, where water is split into hydrogen and oxygen using electricity. This hydrogen is then immediately utilized by an adjacent industrial facility for its operational needs, eliminating the need for external transportation and storage, thereby improving efficiency and reducing logistics.

On-site hydrogen generation offers industries enhanced energy security by providing a localized, controlled supply, reducing dependence on external markets and mitigating supply chain risks. It also enables significant carbon footprint reduction when powered by renewable electricity, aligning with global decarbonization goals and increasingly stringent environmental regulations, while also providing greater operational flexibility and cost stability.

The main technologies in use are Alkaline Electrolyzers, known for their mature design and cost-effectiveness; Proton Exchange Membrane (PEM) Electrolyzers, prized for their rapid response and suitability for intermittent renewable power; and Solid Oxide Electrolyzer Cells (SOEC), which offer high efficiency when integrated with industrial waste heat at elevated temperatures, advancing the potential for green hydrogen production.

Leading adopting industries include petroleum refining, which uses hydrogen for critical hydrotreating processes; chemical manufacturing, particularly for producing ammonia and methanol; and the rapidly expanding green steel sector, where hydrogen serves as a clean reducing agent. The electronics industry also relies on captive generation for ultra-high purity hydrogen in semiconductor fabrication.

AI significantly enhances efficiency by enabling real-time operational optimization of electrolyzers, leading to reduced energy consumption. It facilitates predictive maintenance, extending equipment lifespan and minimizing downtime. Moreover, AI intelligently integrates variable renewable energy sources, optimizes hydrogen production schedules based on energy prices, and improves safety protocols, making the entire process more sustainable and cost-effective.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.