ID : MRU_ 428482 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

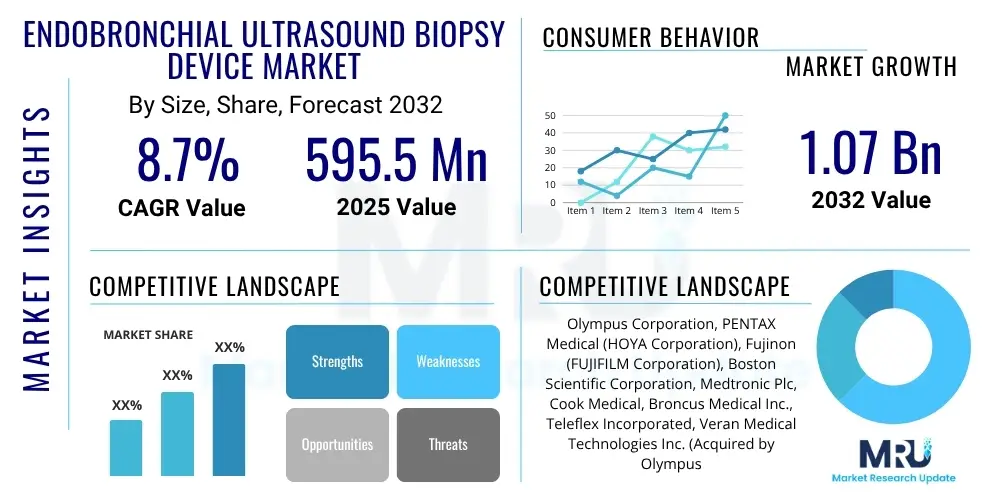

The Endobronchial Ultrasound Biopsy Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2032. The market is estimated at USD 595.5 million in 2025 and is projected to reach USD 1.07 billion by the end of the forecast period in 2032.

The Endobronchial Ultrasound (EBUS) Biopsy Device Market encompasses sophisticated medical instruments designed for the precise, minimally invasive diagnosis and staging of various intrathoracic conditions, primarily lung cancer. These advanced devices ingeniously integrate real-time ultrasound imaging capabilities with the flexibility of a bronchoscope, enabling clinicians to visualize and meticulously assess anatomical structures, such as lymph nodes, masses, and other lesions, situated adjacent to the tracheobronchial tree that are otherwise inaccessible or indistinct through conventional bronchoscopic visualization. This innovative fusion of technologies facilitates highly targeted and accurate tissue sampling, which is paramount for achieving a definitive diagnosis and subsequently formulating an effective and personalized treatment plan. The core product offerings within this market segment typically include EBUS bronchoscopes, specialized biopsy needles (such as transbronchial needle aspiration or TBNA needles), and a range of associated accessories like ultrasound processors, high-intensity light sources, and advanced video processors, which collectively form a complete and integrated diagnostic system.

Major applications for EBUS biopsy devices extend across critical domains of pulmonary medicine and oncology. Foremost among these is the accurate staging of lung cancer, where EBUS-TBNA plays an indispensable role by allowing for the efficient and precise assessment of mediastinal and hilar lymph nodes. This assessment is crucial for determining the extent of disease progression, guiding appropriate therapeutic interventions, and establishing prognosis. Beyond oncological applications, these devices are equally invaluable in the diagnosis of various non-malignant conditions, including sarcoidosis, where histological confirmation of granulomatous inflammation in lymph nodes is often required, and for the evaluation and diagnosis of different types of lymphoma affecting the thoracic region. The benefits derived from employing EBUS-guided biopsies are considerable and far-reaching, encompassing significantly enhanced diagnostic accuracy due to real-time visual guidance, substantially reduced invasiveness compared to traditional surgical procedures like mediastinoscopy, which translates into less patient discomfort, shorter hospital stays, and quicker recovery periods. These manifold advantages collectively contribute to markedly improved patient outcomes, optimize the utilization of healthcare resources, and firmly establish EBUS as a gold standard in modern thoracic diagnostics.

The burgeoning growth trajectory of the EBUS Biopsy Device Market is fundamentally propelled by a combination of potent and interconnected driving factors. A primary catalyst is the escalating global incidence and prevalence of lung cancer, which continues to stand as a leading cause of cancer-related mortality worldwide, thereby creating an urgent and persistent demand for early and highly precise diagnostic tools. Concurrently, there is a widespread and increasing preference within the medical community and among patients alike for minimally invasive diagnostic and therapeutic procedures, a preference driven by superior safety profiles, reduced post-procedural complications, and an improved quality of life. Furthermore, continuous and rapid technological advancements in medical imaging, device miniaturization, and sophisticated software integration are consistently enhancing the capabilities, maneuverability, and overall accessibility of EBUS systems. These innovations are leading to improved image resolution, superior scope flexibility, and facilitating easier adoption by practitioners. Additionally, a growing awareness among medical professionals regarding the superior diagnostic yield, accuracy, and safety profile of EBUS-guided biopsies, coupled with increasingly favorable reimbursement policies in key developed healthcare markets, further stimulates market expansion and device adoption on a global scale. These elements collectively foster an environment conducive to sustained market growth.

The Endobronchial Ultrasound Biopsy Device Market is experiencing robust and sustained growth, predominantly fueled by the increasing global burden of lung cancer and the accelerating adoption of minimally invasive diagnostic techniques across healthcare systems. Current business trends within this market indicate a strong and pervasive focus on intensive research and development initiatives undertaken by leading market players. These efforts are aimed at introducing more advanced, ergonomically designed, and flexible devices, often incorporating cutting-edge features such as enhanced imaging resolution, real-time navigation capabilities, and greater integration with digital platforms. There is also a noticeable trend towards market consolidation, evidenced by strategic acquisitions and partnerships among major companies, enabling them to expand their product portfolios, leverage synergistic technologies, and significantly broaden their geographical reach, thereby securing larger market shares and fostering innovation through collaborative efforts. This strategic maneuvering is crucial for maintaining a competitive edge in a rapidly evolving technological landscape and for addressing diverse market demands more comprehensively.

Regional trends reveal a heterogeneous but overall positive market landscape. North America and Europe are positioned as mature markets, characterized by high adoption rates of EBUS devices due to their well-established healthcare infrastructure, high prevalence of lung cancer, advanced diagnostic capabilities, and favorable reimbursement scenarios that encourage the use of sophisticated medical technologies. Conversely, the Asia Pacific region is emerging as the fastest-growing market segment, propelled by a confluence of factors including rapidly increasing healthcare expenditure, a substantial and growing patient population, increasing public and professional awareness regarding advanced diagnostic methods, and significant improvements in healthcare infrastructure and accessibility to modern medical technologies. Latin America and the Middle East and Africa regions are also showing promising growth, albeit from a lower base, driven by improving economic conditions, expanding healthcare services, and increasing investments in medical facilities. These regional dynamics highlight significant opportunities for market penetration and expansion, particularly in developing economies.

In terms of segmentation trends, the market is witnessing a notable surge in demand for disposable EBUS needles. This trend is primarily driven by heightened concerns regarding infection control, the desire for streamlined operational efficiency, and the reduction of complex reprocessing protocols associated with reusable instruments. The application segment for lung cancer diagnosis and staging continues to dominate the market, reflecting the critical role of EBUS in managing this prevalent and severe disease. However, the utilization of EBUS in other important indications such as sarcoidosis, various types of lymphoma, and the evaluation of other mediastinal pathologies is steadily expanding, driven by increasing clinical evidence supporting its efficacy and cost-effectiveness in these areas. The market is also progressively witnessing the integration of advanced digital health solutions, including artificial intelligence (AI)-powered image analysis, automated reporting, and sophisticated procedural guidance systems. These integrations are set to further enhance diagnostic precision, improve workflow efficiency, and bolster overall patient safety, representing a pivotal shift towards more intelligent and assisted diagnostic procedures.

User inquiries about Artificial Intelligence's (AI) evolving role in the Endobronchial Ultrasound Biopsy Device Market frequently center on its potential to significantly enhance diagnostic accuracy, streamline procedural workflows, and overcome inherent limitations associated with human interpretation and manual dexterity. Users are keen to understand precisely how AI can assist in real-time lesion detection, improve the precision of needle placement during biopsy, and provide advanced prognostic insights derived from complex imaging and pathological data. There is also considerable interest regarding AI's capability to automate repetitive or time-consuming tasks, potentially reducing overall procedure times, and its utility as an objective and standardized training tool for new pulmonologists and endoscopists. While the transformative potential is acknowledged, concerns often include the reliability and validation of AI algorithms across diverse patient populations, the critical need for extensive and high-quality data sets for robust model training, regulatory approval hurdles for AI-driven medical devices, and the ethical implications surrounding AI-driven diagnostics, particularly concerning accountability and patient data privacy. The overarching expectation is that AI will function as a powerful augmentative tool, significantly enhancing rather than replacing human expertise, ultimately leading to more consistent, efficient, and superior patient care outcomes in the complex diagnosis of thoracic pathologies.

The Endobronchial Ultrasound Biopsy Device Market is dynamically shaped by a complex interplay of driving forces, inherent restraining factors, and emerging opportunities, all collectively influencing its current growth trajectory and future potential. Key drivers exerting significant upward pressure on the market include the alarming and escalating global prevalence of lung cancer and other thoracic malignancies, which creates an urgent and persistent need for highly accurate, early diagnostic tools. Complementing this is the continuously increasing demand within the medical community and among patients for minimally invasive diagnostic procedures. These procedures offer distinct advantages such as reduced patient discomfort, significantly shorter hospital stays, and quicker recovery times, making them highly desirable alternatives to more invasive surgical options. Furthermore, persistent and rapid technological advancements, encompassing improvements in imaging quality, enhanced maneuverability of EBUS scopes, and the seamless integration of complementary technologies like advanced navigation systems, are consistently contributing to the broader adoption and efficacy of these devices. Favorable reimbursement policies across developed healthcare economies and a growing awareness among healthcare professionals regarding the superior diagnostic yield and safety profile of EBUS also act as strong catalysts for market expansion.

However, the market also faces several notable restraints that temper its growth. A significant barrier is the high initial capital investment required for EBUS equipment, which can be prohibitive for smaller healthcare facilities, those with budget constraints, or institutions in developing economies, thereby limiting widespread adoption. Another substantial restraint is the steep learning curve associated with mastering EBUS procedures, demanding specialized training and considerable clinical experience. This, coupled with a persistent shortage of adequately trained pulmonologists and endoscopists, particularly in underserved regions, restricts the availability and accessibility of EBUS services. Additionally, stringent and often protracted regulatory approval processes for new medical devices, particularly those incorporating advanced technologies, can extend the time-to-market for innovative products, delaying their commercial availability and hindering rapid technological dissemination. These factors collectively pose challenges to market penetration and expansion, requiring strategic solutions from manufacturers and policymakers.

Despite these restraints, the Endobronchial Ultrasound Biopsy Device Market presents numerous lucrative opportunities that are poised to drive future growth and innovation. Significant potential lies in emerging economies across Asia Pacific, Latin America, and the Middle East and Africa, where healthcare infrastructure is rapidly developing, and access to advanced diagnostic technologies is steadily improving. These regions represent untapped markets with large patient populations and increasing healthcare expenditures. The profound integration of artificial intelligence (AI) and robotics is set to revolutionize the precision, efficiency, and safety of EBUS procedures, offering new avenues for product development and clinical application. Moreover, expanding the application scope of EBUS beyond its primary focus on lung cancer to encompass a wider range of indications, such as infectious diseases, interstitial lung diseases, and further applications in oncology, presents considerable market expansion opportunities. The development of more affordable, portable, and user-friendly devices, potentially incorporating disposable components, also offers a pathway to increase accessibility and reduce the economic burden on healthcare systems, thereby catering to a broader segment of the market and accelerating global adoption rates.

The Endobronchial Ultrasound Biopsy Device Market is meticulously segmented across various crucial parameters to provide a comprehensive, granular understanding of its intricate dynamics, evolving adoption patterns, and underlying growth potential. This detailed market segmentation allows for a precise and in-depth analysis of prevailing market trends, the competitive landscape, and strategic opportunities, catering to the diverse healthcare needs and technological preferences observed globally. By disaggregating the market into distinct categories, stakeholders can identify niche markets, understand specific consumer demands, and tailor product development and marketing strategies more effectively. This analytical approach is vital for companies aiming to optimize their market positioning, anticipate future shifts, and allocate resources efficiently within this highly specialized medical device sector.

The primary segmentation criteria employed within this market include categorization by product type, application, end-user, and usability, with each category offering unique insights into the overall market's evolution and specific growth drivers. Understanding these segments is critical for manufacturers to align their research and development efforts with market demands, for healthcare providers to make informed purchasing decisions, and for investors to identify high-growth areas. For instance, the distinction between reusable and disposable devices impacts hospital procurement strategies and infection control protocols, while application-specific demands drive innovation in biopsy needle design and imaging capabilities. This multi-faceted segmentation framework ensures that all aspects of the market, from technological innovation to clinical adoption and economic viability, are thoroughly scrutinized, providing a holistic view of the Endobronchial Ultrasound Biopsy Device ecosystem and its future trajectory.

The value chain for the Endobronchial Ultrasound Biopsy Device Market is a highly intricate and interconnected network, encompassing a series of specialized activities from the very initial stages of raw material sourcing to the final deployment and utilization of these advanced medical devices by end-users. This complex chain highlights the multifaceted processes and strategic collaborations required to successfully develop, manufacture, and bring these sophisticated instruments to market. The upstream segment of the value chain is characterized by the meticulous procurement of highly specialized raw materials and precision components. This includes biocompatible polymers for flexible scope sheaths, advanced metals for robust needle construction, high-grade optical fibers for imaging, and cutting-edge ultrasound transducer components. Manufacturers in this initial phase heavily rely on a specialized supply chain of highly reputable component providers who adhere to stringent quality, safety, and regulatory standards, ensuring the foundational integrity and performance of the final product. Innovation in these raw materials and components, such as smaller, more efficient transducers or more durable yet flexible materials, significantly impacts the capabilities and cost-effectiveness of the end device.

Following the sourcing stage, the manufacturing segment involves the complex and precision-driven assembly of EBUS bronchoscope systems, various types of biopsy needles, and their associated accessories. This stage is marked by intricate engineering processes, cleanroom manufacturing environments, rigorous quality control measures, and extensive testing to ensure product reliability, safety, and compliance with global medical device regulations. Given the high technological complexity and precision required, manufacturing often involves automated processes alongside skilled manual assembly to ensure the functionality and sterile integrity of each component. Downstream activities in the value chain are primarily concentrated on efficient distribution and sales, where finished products move from the manufacturing facilities to diverse healthcare providers. This involves a carefully managed network of direct sales forces employed by major multinational manufacturers, as well as a robust ecosystem of third-party distributors and specialized medical device suppliers. These entities manage critical aspects such as inventory, logistics, regional sales strategies, and often provide essential technical support and comprehensive training to end-users to ensure proper device operation and optimal clinical outcomes.

Distribution channels for EBUS biopsy devices are predominantly bifurcated into direct and indirect routes. Major manufacturers often employ direct sales forces to engage with large hospital networks, university medical centers, and specialized cancer treatment centers. This direct approach facilitates stronger manufacturer-to-customer relationships, enables specialized product demonstrations, and ensures dedicated post-sales support and service for complex and high-value equipment. Conversely, indirect channels, leveraging a network of third-party medical distributors, are utilized to reach a wider array of smaller clinics, ambulatory surgical centers, and regional hospitals that may benefit from the distributors' localized market knowledge and extensive customer reach. The efficiency and reliability of these distribution channels are paramount for effective market penetration and maintaining high levels of customer satisfaction. Factors such as efficient logistics, strict adherence to regional regulatory compliance for medical device distribution, and the provision of continuous, high-quality post-sales technical support and training are critical elements that underpin the success and sustainability of the entire EBUS biopsy device value chain. Strategic partnerships within the value chain, particularly with key opinion leaders and clinical experts, also play a vital role in product development, clinical validation, and market adoption.

The primary potential customers and end-users of Endobronchial Ultrasound Biopsy Devices are a diverse group of healthcare institutions and medical professionals who specialize in pulmonology, oncology, and thoracic surgery. Hospitals, particularly those equipped with comprehensive cancer centers, advanced diagnostic imaging departments, and robust pulmonology and thoracic surgery divisions, represent the largest and most significant segment of buyers. These multi-specialty facilities require EBUS devices for their critical role in the diagnosis and accurate staging of lung cancer, the thorough evaluation of mediastinal lymphadenopathy (enlarged lymph nodes in the chest), and the assessment of various other complex thoracic pathologies. The demand from hospitals is consistently high due to the prevalence of these conditions and the imperative for precise diagnostic capabilities to inform patient care pathways and treatment decisions.

In addition to large hospital systems, ambulatory surgical centers (ASCs) are increasingly adopting EBUS technology. This trend is driven by the growing shift towards outpatient procedures, where EBUS's minimally invasive nature allows for efficient, safe, and often same-day diagnostic interventions, reducing the need for costly inpatient stays. This makes ASCs an attractive and growing customer segment, as they seek to expand their service offerings and provide advanced, cost-effective care. Furthermore, specialized diagnostic centers focusing on respiratory health and pulmonology clinics that prioritize state-of-the-art respiratory diagnostics also constitute a significant and expanding customer base. These centers leverage EBUS technology to offer specialized diagnostic services, attracting patients who require advanced, non-surgical methods for evaluating thoracic conditions, thereby enhancing their diagnostic capabilities and competitive positioning in the healthcare market.

The key decision-makers within these customer organizations typically include heads of pulmonology departments, lead oncologists, chief thoracic surgeons, interventional pulmonologists, and hospital procurement committees. These stakeholders prioritize a range of critical factors when making purchasing decisions, including the diagnostic accuracy and reliability of the device, paramount patient safety features, the overall usability and ergonomic design for clinicians, device durability, and crucially, its cost-effectiveness over the product's lifecycle. The ability of an EBUS device to integrate seamlessly into existing clinical workflows, coupled with comprehensive training and ongoing technical support from the manufacturer, also significantly influences procurement choices. The ongoing expansion of these devices into a broader spectrum of clinical settings signifies a growing recognition and demand from institutions seeking to enhance their diagnostic capabilities, streamline patient care pathways, and ultimately offer the most advanced and effective care to patients grappling with complex thoracic diseases.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 595.5 Million |

| Market Forecast in 2032 | USD 1.07 Billion |

| Growth Rate | 8.7% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Olympus Corporation, PENTAX Medical (HOYA Corporation), Fujinon (FUJIFILM Corporation), Boston Scientific Corporation, Medtronic Plc, Cook Medical, Broncus Medical Inc., Teleflex Incorporated, Veran Medical Technologies Inc. (Acquired by Olympus), ConMed Corporation, Ambu A/S, Karl Storz SE & Co. KG, Richard Wolf GmbH, Argon Medical Devices, Inc., Angiotech Pharmaceuticals, Inc., Stryker Corporation, Becton, Dickinson and Company (BD), Cardinal Health Inc., Ethicon (Johnson & Johnson), ENDODOC GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Endobronchial Ultrasound Biopsy Device market is characterized by a highly dynamic and continuously evolving technology landscape, driven by an unceasing pursuit of enhanced diagnostic accuracy, improved procedural safety, and greater user-friendliness for clinicians. A pivotal techno

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.