ID : MRU_ 430032 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

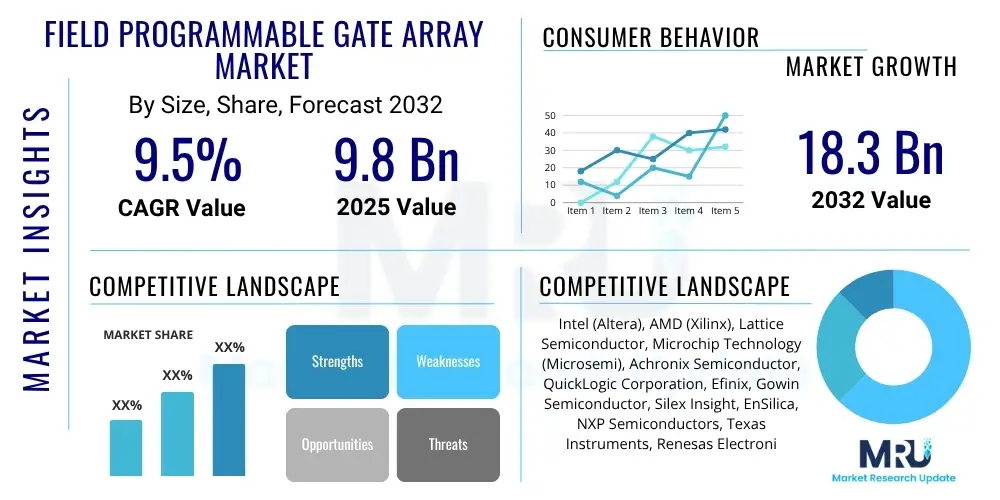

The Field Programmable Gate Array Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at $9.8 billion in 2025 and is projected to reach $18.3 billion by the end of the forecast period in 2032.

The Field Programmable Gate Array (FPGA) market encompasses integrated circuits designed to be configured by a customer or a designer after manufacturing. These highly versatile semiconductor devices offer significant advantages in terms of flexibility, allowing for hardware reconfiguration to suit evolving application requirements, and accelerating time-to-market. Unlike Application Specific Integrated Circuits (ASICs), FPGAs can be reprogrammed, making them ideal for prototyping, low-volume production, and applications where standards are still developing or algorithms may change frequently. Their parallel processing capabilities and low latency performance position them as crucial components in a diverse range of high-performance computing environments.

Major applications for FPGAs span across telecommunications, automotive systems, data centers, industrial automation, and aerospace and defense. In telecommunications, FPGAs are vital for 5G infrastructure, base stations, and network acceleration due to their ability to handle complex signal processing and dynamic network loads. The automotive sector leverages FPGAs for Advanced Driver-Assistance Systems (ADAS), infotainment, and autonomous driving due to their real-time processing and reconfigurability. Data centers utilize FPGAs for workload acceleration, especially for artificial intelligence (AI) and machine learning (ML) inference, database processing, and network function virtualization (NFV).

The primary benefits of FPGAs include their superior performance for parallel tasks, reduced non-recurring engineering (NRE) costs compared to ASICs, and accelerated development cycles. Key driving factors propelling market growth include the escalating demand for high-performance computing solutions, the proliferation of AI and ML applications requiring specialized hardware acceleration, the global rollout of 5G networks, the expansion of the Internet of Things (IoT) ecosystem, and the increasing adoption of FPGAs in critical safety systems within industrial and automotive domains. These factors collectively underscore the strategic importance of FPGAs in the modern technological landscape, fostering continuous innovation and expanding their market footprint.

The Field Programmable Gate Array market is experiencing robust growth, driven by key business trends such as increasing investments in data center infrastructure, the rapid expansion of 5G networks globally, and the growing integration of AI and machine learning technologies across various industries. Semiconductor companies are heavily investing in advanced process technologies (e.g., 7nm, 5nm) to enhance FPGA performance, power efficiency, and logic density, pushing the boundaries of what these devices can achieve. Consolidation among major players, such as AMD's acquisition of Xilinx, reflects a strategic move to offer more comprehensive solutions and strengthen competitive positions in the evolving semiconductor landscape, aiming to capture synergy across CPU, GPU, and FPGA ecosystems.

Regionally, Asia Pacific stands out as the dominant and fastest-growing market for FPGAs, primarily due to its robust manufacturing base, massive investments in 5G deployment, and the burgeoning consumer electronics and automotive industries in countries like China, Japan, and South Korea. North America continues to be a hub for innovation and early adoption, particularly in aerospace and defense, high-performance computing, and advanced AI research. Europe maintains a significant presence, driven by its strong automotive, industrial automation, and telecommunications sectors, with a growing focus on edge computing applications. Emerging markets in Latin America and the Middle East & Africa are also showing increasing adoption as their digital infrastructure and industrial capabilities mature.

In terms of segment trends, the market is witnessing a shift towards high-end and mid-range FPGAs, fueled by demanding applications requiring higher logic densities, embedded processors (SoC FPGAs), and integrated high-speed transceivers. The technology segmentation highlights the continued dominance of SRAM-based FPGAs due to their reconfigurability and performance, while flash-based FPGAs are gaining traction for instant-on capabilities and lower power consumption. Application-wise, data processing and telecommunications remain leading segments, with automotive and industrial applications showing accelerated growth as FPGAs become indispensable for safety-critical and real-time processing tasks. The convergence of these trends underlines a dynamic and expanding market with significant opportunities for innovation and strategic development across the entire value chain.

Common user inquiries regarding the intersection of AI and FPGAs often revolve around the practical utility of FPGAs for AI workloads, their competitive standing against GPUs and ASICs, and their role in facilitating edge AI deployments. Users frequently question the performance-per-watt efficiency of FPGAs for AI inference, the ease of programming compared to more established AI accelerators, and the scenarios where FPGAs offer a distinct advantage. There is also considerable interest in how FPGAs contribute to the development of custom AI hardware and whether their reconfigurability truly provides a future-proof solution for rapidly evolving AI algorithms. Concerns sometimes surface about the software ecosystem maturity and the learning curve associated with FPGA development for AI applications, contrasting it with the more widely adopted frameworks for GPUs.

Based on this analysis, the key themes indicate that users seek clarity on the specific niches where FPGAs excel in AI, particularly regarding flexibility, latency, and power consumption, especially outside of large-scale data center training. They anticipate FPGAs to enable highly optimized and specialized AI solutions that might not be feasible or cost-effective with general-purpose processors or fixed-function ASICs. The expectation is that FPGAs will bridge the gap between fixed hardware and purely software-based solutions, offering a customizable and adaptable platform for emerging AI requirements, particularly at the edge where resources are constrained and real-time responsiveness is paramount. Users are looking for evidence of FPGAs delivering tangible benefits in real-world AI deployments.

The consensus suggests that FPGAs are becoming increasingly vital for flexible, low-latency AI inference, especially at the edge and for specialized data center workloads. While GPUs dominate AI training, FPGAs offer a compelling balance between ASIC-like efficiency and GPU-like programmability for inference, addressing specific needs for customization and power efficiency. The main concerns for users often center on the perceived complexity of FPGA development and the availability of mature software tools and frameworks that simplify AI application deployment on these devices. However, advancements in high-level synthesis (HLS) tools and specialized AI IP cores are steadily addressing these challenges, making FPGAs more accessible to a broader range of AI developers and data scientists.

The Field Programmable Gate Array market is primarily driven by the escalating demand for high-performance computing and the widespread adoption of AI and machine learning across diverse sectors, necessitating specialized and reconfigurable hardware for efficient inference. The global rollout of 5G infrastructure, which relies heavily on FPGAs for flexible base station and network equipment, along with the continuous expansion of the Internet of Things (IoT) ecosystem, further fuels market growth by requiring low-latency and customisable processing at the edge. However, the market faces restraints such as the inherent design complexity associated with FPGA development, which can increase time-to-market and demand specialized engineering expertise. Additionally, for very high-volume production, the per-unit cost of FPGAs can be higher than that of custom ASICs, posing a competitive challenge.

Opportunities for market expansion are significant, particularly in the burgeoning edge computing segment, where FPGAs offer unparalleled advantages in terms of low power consumption and real-time processing capabilities for AI and sensory data. The increasing need for customizable hardware solutions that can adapt to rapidly evolving AI algorithms and new communication standards presents a fertile ground for FPGA innovation. Furthermore, critical sectors like aerospace and defense, and medical imaging, continue to expand their reliance on FPGAs for their reliability, long product lifecycles, and ability to meet stringent performance requirements. The ongoing development of advanced high-level synthesis tools is also making FPGA design more accessible, potentially expanding the user base.

Impact forces influencing the market include rapid technological advancements, especially in smaller process nodes (e.g., 7nm, 5nm), which enable higher logic density, increased performance, and reduced power consumption, making FPGAs more attractive for demanding applications. Supply chain dynamics, including raw material availability and geopolitical factors affecting manufacturing and trade, can significantly impact production and delivery schedules. The competitive landscape, characterized by intense rivalry from GPU and ASIC manufacturers, pushes FPGA vendors to continuously innovate and differentiate their offerings, particularly in software ecosystems and specialized IP cores. Lastly, regulatory landscapes, particularly those pertaining to semiconductor tariffs and export controls, can influence market access and competitive positioning, creating both challenges and opportunities for regional players.

The Field Programmable Gate Array market is comprehensively segmented to provide a granular understanding of its diverse landscape and growth trajectories. This segmentation allows for targeted analysis based on various product attributes, underlying technologies, the specific applications FPGAs serve, and the broad end-user industries that adopt these highly versatile devices. Understanding these distinct segments is crucial for identifying key growth drivers, competitive dynamics, and emerging opportunities within the overall FPGA ecosystem. Each category reflects different performance requirements, cost sensitivities, and market adoption patterns, contributing to the complex market structure.

The value chain for the Field Programmable Gate Array market commences with upstream activities, involving critical suppliers such as intellectual property (IP) core providers who offer pre-verified design blocks, Electronic Design Automation (EDA) tool vendors providing sophisticated software for design, verification, and synthesis, and wafer fabrication facilities (foundries) responsible for the actual manufacturing of semiconductor wafers. These upstream partners are fundamental as they dictate the technological capabilities, design complexity, and manufacturing costs of the FPGAs. Innovation in process technology by foundries, alongside advanced IP and robust EDA tools, directly influences the performance and features of the final FPGA product, enabling smaller geometries, higher logic densities, and better power efficiency. Strategic alliances and partnerships at this stage are common to ensure access to leading-edge technologies and specialized expertise.

Moving downstream, the value chain involves FPGA vendors themselves, who integrate the IP cores, utilize EDA tools to design the FPGA architecture, and then send the designs for fabrication. After fabrication, these vendors conduct rigorous testing, packaging, and branding of the FPGAs. The finished FPGA chips are then supplied to module integrators and system manufacturers, who incorporate them into their final products, such as networking equipment, ADAS units, industrial control systems, or specialized servers. This stage often involves extensive collaboration between FPGA vendors and their customers to optimize design implementations and ensure seamless integration. Software developers also play a crucial role downstream by creating libraries, development kits, and higher-level programming abstractions that simplify FPGA utilization for specific applications, thereby expanding the potential customer base.

Distribution channels for FPGAs are typically bifurcated into direct and indirect routes. Direct sales involve FPGA manufacturers engaging directly with large original equipment manufacturers (OEMs) and key accounts, often offering customized solutions, technical support, and long-term supply agreements. This direct approach allows for closer collaboration and a deeper understanding of customer-specific needs. Indirect channels predominantly rely on a network of authorized distributors, who serve smaller to mid-sized customers, providing broader market reach, localized support, and inventory management services. Online platforms and specialized component retailers also contribute to the distribution, particularly for evaluation boards, development kits, and standard off-the-shelf FPGA components. The choice of distribution channel often depends on customer size, geographic location, and the complexity of the required solution, with a hybrid approach being common to maximize market penetration and customer satisfaction.

The Field Programmable Gate Array market targets a diverse array of potential customers across multiple high-growth industries, each leveraging FPGAs for distinct, performance-critical applications. Original Equipment Manufacturers (OEMs) in the telecommunications sector represent a significant customer base, procuring FPGAs for their 5G base stations, network routers, switches, and other infrastructure equipment, valuing the devices' reconfigurability for evolving communication standards and high-speed data processing capabilities. Automotive manufacturers and Tier 1 suppliers are increasingly adopting FPGAs for Advanced Driver-Assistance Systems (ADAS), autonomous driving platforms, in-vehicle infotainment systems, and powertrain control, where real-time processing, functional safety, and adaptability are paramount.

Data center operators and cloud service providers constitute another crucial segment of buyers, utilizing FPGAs for workload acceleration in areas such as artificial intelligence (AI) inference, database query acceleration, network function virtualization (NFV), and video transcoding. These customers seek FPGAs for their ability to provide custom hardware acceleration, optimize power efficiency, and reduce latency for specific computational tasks that may not be efficiently handled by general-purpose CPUs or GPUs. Furthermore, industrial automation companies purchase FPGAs for motor control, robotic systems, machine vision, and real-time process control, benefiting from their deterministic performance and long product lifecycles, which are critical in factory environments.

Other significant end-users include aerospace and defense contractors, who integrate FPGAs into radar systems, avionics, secure communication devices, and electronic warfare applications, valuing their high reliability, radiation tolerance, and long-term availability for mission-critical systems. Medical device manufacturers use FPGAs for imaging equipment, diagnostic tools, and surgical robots, where high-speed data acquisition, parallel processing, and stringent regulatory compliance are essential. Consumer electronics companies, particularly those developing high-end audio/video processing equipment and advanced gaming consoles, also leverage FPGAs for custom signal processing and feature differentiation. Research institutions and academic bodies further serve as potential customers, utilizing FPGAs for advanced scientific computing, prototyping new technologies, and educational purposes, driving future innovation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $9.8 billion |

| Market Forecast in 2032 | $18.3 billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Intel (Altera), AMD (Xilinx), Lattice Semiconductor, Microchip Technology (Microsemi), Achronix Semiconductor, QuickLogic Corporation, Efinix, Gowin Semiconductor, Silex Insight, EnSilica, NXP Semiconductors, Texas Instruments, Renesas Electronics, Samsung Foundry, TSMC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Field Programmable Gate Array market's technological landscape is characterized by continuous innovation aimed at enhancing performance, power efficiency, and design flexibility. One of the most significant advancements is the migration to smaller process nodes, such as 7nm, 5nm, and increasingly 3nm, which allows for a dramatic increase in logic density, higher operating frequencies, and reduced power consumption. This enables FPGAs to integrate more complex functionalities and support increasingly demanding applications in AI, 5G, and high-performance computing. Alongside this, heterogeneous integration is gaining prominence, with System-on-Chip (SoC) FPGAs embedding ARM processors and other dedicated hard IP blocks alongside programmable logic, offering a powerful combination of flexibility and processing power for complete system solutions.

Another critical area of technological development involves high-bandwidth memory (HBM) integration and advanced packaging techniques. Integrating HBM directly with FPGAs significantly boosts memory bandwidth, which is crucial for data-intensive applications like AI inference and high-speed data processing, overcoming traditional memory bottlenecks. Advanced packaging technologies, such as 2.5D and 3D stacking, enable the integration of multiple dice (e.g., FPGA logic, HBM, optical transceivers) into a single package, further enhancing performance, reducing form factor, and improving power efficiency. These advancements allow FPGAs to serve as highly integrated, adaptive computing platforms capable of addressing a wide range of specialized workloads.

Furthermore, the evolution of software-defined hardware and adaptive computing architectures is reshaping how FPGAs are utilized. High-Level Synthesis (HLS) tools are becoming more sophisticated, allowing designers to program FPGAs using higher-level languages like C, C++, and OpenCL, thereby abstracting much of the traditional hardware description language (HDL) complexity. This democratization of FPGA programming is making these devices more accessible to software developers, accelerating design cycles, and enabling faster deployment of applications. Specialized IP cores for AI acceleration, networking protocols, and digital signal processing are also continuously being developed, providing ready-to-use, optimized building blocks that significantly reduce design effort and time-to-market for complex FPGA-based systems, solidifying FPGAs' role in the adaptive computing paradigm.

The global Field Programmable Gate Array market exhibits distinct regional dynamics, influenced by technological adoption rates, industrial infrastructure, and strategic investments. North America continues to be a pivotal market, driven by its robust defense and aerospace industries, a strong presence of data center operators, and significant investments in research and development for advanced AI and high-performance computing. The region is characterized by early adoption of cutting-edge FPGA technologies and a high demand for custom, secure, and high-reliability solutions, particularly from government and technology giants. Innovation in software tools and design methodologies also frequently originates from this region, supporting the broader global FPGA ecosystem and fostering a competitive environment among leading vendors.

Asia Pacific (APAC) stands out as the largest and most rapidly growing market for FPGAs, primarily fueled by the region's expansive manufacturing capabilities, aggressive deployment of 5G infrastructure, and burgeoning consumer electronics sector. Countries like China, Japan, South Korea, and Taiwan are at the forefront of semiconductor manufacturing and technological innovation, driving high demand for FPGAs in telecommunications equipment, automotive systems, and a rapidly expanding network of data centers. Government initiatives supporting local semiconductor industries and significant foreign investments in digital infrastructure further accelerate market growth across the region. The sheer volume of electronics production and the increasing complexity of devices in APAC make it a critical market for FPGA vendors.

Europe represents another substantial market, characterized by its strong automotive, industrial automation, and telecommunications sectors. European manufacturers are increasingly integrating FPGAs into their advanced driver-assistance systems, industrial IoT solutions, and sophisticated robotics, driven by the need for real-time processing, functional safety, and adaptability. The region also benefits from significant research initiatives in advanced computing and edge intelligence, fostering demand for FPGAs in scientific instruments and niche industrial applications. Latin America and the Middle East & Africa (MEA) are emerging markets, demonstrating steady growth driven by increasing digitalization, infrastructure development projects, and a growing emphasis on industrial modernization. These regions are gradually adopting FPGAs for telecommunications expansion, energy management systems, and nascent automotive manufacturing, indicating future growth potential as their technological capabilities mature and industrial bases expand.

A Field Programmable Gate Array (FPGA) is an integrated circuit designed to be configured or reprogrammed by a customer or designer after manufacturing. It comprises an array of configurable logic blocks (CLBs) connected by programmable interconnects, offering flexibility to implement various digital circuits and systems.

FPGAs are primarily used in applications requiring high performance, low latency, and reconfigurability. Key areas include telecommunications (5G, network acceleration), automotive (ADAS, autonomous driving), data centers (AI/ML acceleration, workload offloading), industrial automation, aerospace and defense, and medical imaging.

FPGAs offer post-manufacturing reconfigurability, unlike fixed-function ASICs, providing design flexibility and lower NRE costs for smaller volumes. Compared to GPUs, FPGAs excel in customizability, lower latency, and power efficiency for specialized parallel workloads like AI inference, whereas GPUs are optimized for massive parallel processing in AI training and graphics.

In AI/ML, FPGAs are critical for accelerating inference tasks, especially at the edge and in data centers, due to their ability to provide highly customized hardware architectures for specific neural networks and algorithms. They offer a balance of performance, power efficiency, and flexibility that is ideal for evolving AI models and real-time processing needs.

The primary industries driving FPGA market growth are telecommunications (due to 5G rollout), automotive (for ADAS and autonomous vehicles), data centers (for AI/ML acceleration and cloud computing), and industrial automation (for real-time control and IoT). The aerospace and defense sector also contributes significantly due to demand for high-reliability systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.