ID : MRU_ 429488 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

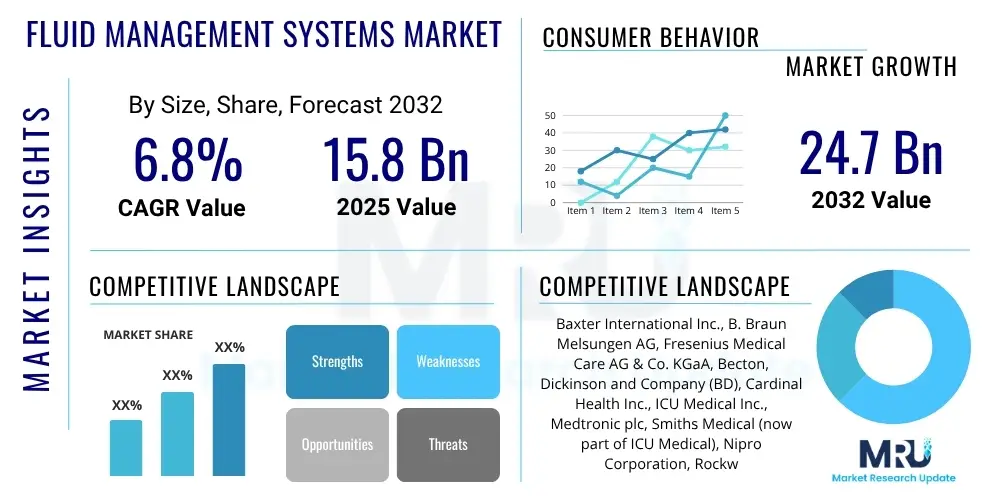

The Fluid Management Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at $15.8 Billion in 2025 and is projected to reach $24.7 Billion by the end of the forecast period in 2032.

The Fluid Management Systems Market encompasses a broad range of devices, equipment, and consumables used for controlling, monitoring, and delivering fluids within medical, industrial, and research settings. These systems are critical for maintaining fluid balance, administering medications, managing waste fluids, and conducting various diagnostic and therapeutic procedures. The increasing prevalence of chronic diseases, an aging global population, and the growing demand for accurate and efficient fluid delivery solutions are key factors driving market expansion.

Products within this market range from sophisticated smart infusion pumps and dialysis machines to simpler disposables like catheters, connectors, and fluid bags. Major applications span across critical care, oncology, nephrology, gastroenterology, and surgical procedures. The core benefits include enhanced patient safety through precise fluid administration, improved operational efficiency in healthcare facilities, and reduced risk of complications associated with manual fluid management processes. These systems also play a vital role in research and laboratory environments for controlled liquid handling.

Driving factors propelling the fluid management systems market include the continuous advancements in medical technology, the rising adoption of minimally invasive surgeries, and the expansion of home healthcare settings. Furthermore, a heightened focus on infection control and the need for standardized clinical practices contribute significantly to the demand for advanced fluid management solutions. The push for automation and integration of these systems within broader healthcare IT infrastructure also serves as a strong market impetus.

The Fluid Management Systems Market is characterized by robust business trends focusing on technological innovation, strategic partnerships, and a strong emphasis on product differentiation. Companies are investing heavily in research and development to introduce smart, connected, and highly accurate devices that integrate seamlessly into existing healthcare workflows. Regional trends indicate significant growth opportunities in emerging economies, particularly across Asia Pacific, driven by improving healthcare infrastructure and increasing access to advanced medical treatments. Meanwhile, mature markets in North America and Europe continue to adopt next-generation systems, prioritizing safety features and data analytics capabilities. Segment trends highlight a sustained demand for dialysis equipment and infusion pumps, alongside a growing market for standalone fluid management systems and consumables.

Key business trends shaping the market include an observable shift towards automation and digitalization, enabling better patient monitoring and reduced clinical burden. Consolidation activities through mergers and acquisitions are also prevalent as companies seek to expand their product portfolios and geographical reach. Furthermore, there is an increasing focus on developing cost-effective solutions and improving supply chain resilience to meet global demands. Manufacturers are also prioritizing the development of user-friendly interfaces and interoperable systems to enhance clinical efficiency and reduce training requirements.

From a regional perspective, North America and Europe maintain their leading positions due to high healthcare expenditure, advanced technological adoption, and a strong presence of key market players. However, the Asia Pacific region is expected to exhibit the fastest growth rate, fueled by a large patient pool, rising disposable incomes, and government initiatives aimed at modernizing healthcare facilities. Segment-wise, the consumables segment is projected to hold a substantial market share due to the recurring need for disposables in various fluid management procedures, while product advancements in standalone fluid management systems and integrated workstations are driving innovation across the device segment.

User inquiries regarding AI's influence on Fluid Management Systems often revolve around improving precision, enabling predictive maintenance, personalizing patient care, and enhancing data analytics capabilities. Key themes include the potential for AI to reduce medical errors associated with fluid administration, optimize resource allocation, and provide deeper insights into patient physiology for better therapeutic outcomes. There are also concerns about data security, the ethical implications of autonomous systems, and the need for robust validation processes to ensure reliability in critical medical applications.

The Fluid Management Systems Market is influenced by a complex interplay of drivers, restraints, opportunities, and broader impact forces that shape its growth trajectory. Key drivers include the escalating global burden of chronic diseases, such as kidney failure and cardiovascular conditions, which necessitate advanced fluid management solutions. Technological advancements, particularly in smart pump technology and integrated systems, are continuously expanding the market's capabilities and appeal. However, significant restraints exist, including the high cost of advanced equipment, stringent regulatory approval processes that can delay market entry, and the inherent risk of infections associated with invasive fluid management procedures. Opportunities lie in the burgeoning potential of emerging markets, the integration of fluid management into home healthcare, and the ongoing shift towards personalized medicine. The market's competitive landscape is also shaped by factors such as the bargaining power of both buyers and suppliers, the threat of new market entrants, the availability of substitute products, and the intensity of existing competitive rivalry.

Drivers such as the increasing geriatric population, which is more prone to various chronic ailments requiring fluid therapy, significantly contribute to market expansion. The growing number of surgical procedures performed globally also fuels demand for intraoperative and postoperative fluid management. Furthermore, the rising awareness about patient safety and the push for standardized healthcare practices globally incentivize the adoption of advanced and automated fluid management systems that minimize human error. Investments in healthcare infrastructure, especially in developing countries, further open avenues for market penetration.

Conversely, significant restraints hinder market growth. The substantial capital investment required for purchasing and maintaining sophisticated fluid management systems can be a barrier for smaller healthcare facilities. Regulatory complexities and the need for extensive clinical validation for new products add to development costs and time-to-market. Additionally, the potential for complications such as catheter-related bloodstream infections remains a concern, prompting continuous innovation in antimicrobial technologies and aseptic techniques. The scarcity of skilled professionals trained to operate and maintain advanced fluid management systems also poses a challenge in some regions.

The Fluid Management Systems Market is extensively segmented across various dimensions to provide a comprehensive view of its intricate structure and growth dynamics. These segmentations typically include classifications by product type, application area, and end-user, each revealing distinct market behaviors and opportunities. Understanding these segments is crucial for stakeholders to identify lucrative niches, tailor product development strategies, and optimize market penetration efforts.

The product segment, for instance, encompasses a wide array of devices and consumables, reflecting the diverse needs of fluid management across different medical and industrial contexts. This includes critical components like dedicated pumps, sophisticated workstations, and a variety of disposable sets that are essential for system functionality and patient safety. Analyzing growth trends within each product category helps in assessing the adoption rates of innovative technologies and the recurring revenue potential from consumables. The application segment, on the other hand, illustrates where these systems are predominantly utilized, from life-sustaining therapies like dialysis to intricate surgical procedures and drug discovery processes, highlighting areas of high demand and specialized requirements.

Furthermore, segmentation by end-user provides insight into the primary consumers of these systems, whether they are large hospital networks, specialized diagnostic centers, or increasingly, home care settings. This granular view allows for a targeted marketing approach and the development of solutions specifically designed to meet the operational and clinical needs of different healthcare providers. Geographical segmentation, while a regional highlight, also plays a crucial role in understanding market maturity, regulatory environments, and economic factors influencing adoption rates worldwide.

A comprehensive value chain analysis for the Fluid Management Systems Market highlights the intricate network of activities involved from raw material sourcing to end-user delivery. The upstream segment involves the procurement and processing of essential components and materials. This includes specialized plastics for disposables, sophisticated electronics for pumps, and precision engineering for mechanical components. Key players in this stage are raw material suppliers, component manufacturers, and technology providers who develop proprietary sensors and software. Ensuring quality and compliance at this stage is paramount, as it directly impacts the reliability and safety of the final fluid management systems.

Moving downstream, the value chain encompasses manufacturing, assembly, and quality control processes where components are integrated into finished products like infusion pumps, dialysis machines, and fluid warmer units. Following manufacturing, the distribution channel plays a critical role in connecting these products with end-users. Distribution can occur through direct sales channels, where manufacturers engage directly with large hospitals or healthcare networks, offering specialized support and training. Alternatively, indirect sales leverage a network of distributors, wholesalers, and medical device representatives who facilitate broader market reach, particularly to smaller clinics and ambulatory surgical centers.

Both direct and indirect distribution channels are vital for market penetration. Direct sales allow for tighter control over customer relationships, product customization, and specialized technical support, often preferred for high-value or complex integrated systems. Indirect channels, through established distributors, offer extensive logistical capabilities, local market knowledge, and access to a wider customer base without the need for manufacturers to build vast sales infrastructures in every region. The efficiency of these channels significantly influences product accessibility, pricing strategies, and overall market share for fluid management system providers.

The potential customers for Fluid Management Systems are diverse and span across various healthcare and research sectors, reflecting the broad applicability of these crucial devices. Hospitals and clinics represent the largest segment of end-users, utilizing these systems across multiple departments including intensive care units, operating rooms, emergency departments, and general wards for a wide range of patient care needs. These institutions rely heavily on fluid management systems for medication delivery, hydration, blood transfusion, and waste fluid collection, making them primary purchasers.

Beyond traditional hospital settings, ambulatory surgical centers (ASCs) and specialized diagnostic centers are increasingly becoming significant buyers. ASCs require efficient and precise fluid management for outpatient procedures, while diagnostic centers may use these systems for various analytical processes and patient preparation. The growing trend of home care also expands the customer base to individual patients and their caregivers who require portable and user-friendly fluid management solutions for long-term therapies like home dialysis or intravenous medication administration.

Furthermore, pharmaceutical and biotechnology companies, along with academic and research institutes, constitute another vital customer segment. These entities leverage fluid management systems in their laboratories for drug discovery, clinical trials, and basic scientific research, where precise liquid handling and control are essential. The need for high accuracy, sterility, and automation in these environments drives demand for specialized and advanced fluid management technologies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $15.8 Billion |

| Market Forecast in 2032 | $24.7 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Baxter International Inc., B. Braun Melsungen AG, Fresenius Medical Care AG & Co. KGaA, Becton, Dickinson and Company (BD), Cardinal Health Inc., ICU Medical Inc., Medtronic plc, Smiths Medical (now part of ICU Medical), Nipro Corporation, Rockwell Medical Inc., AngioDynamics Inc., Zimmer Biomet Holdings Inc., Stryker Corporation, Terumo Corporation, Argos Therapeutics Inc., Siemens Healthineers AG, GE Healthcare, Mindray Medical International Limited, Avanos Medical Inc., Moog Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Fluid Management Systems Market is rapidly evolving, driven by the demand for greater precision, patient safety, and operational efficiency. Advanced pump technologies form the core, with smart infusion pumps leading the innovation. These pumps incorporate features like dose error reduction systems (DERS), wireless connectivity for data integration with electronic health records (EHR), and advanced algorithms for precise medication delivery, significantly reducing the risk of medication errors. Peristaltic and volumetric pumps also continue to see advancements in their design for improved accuracy and reliability across various applications.

Beyond pumps, the integration of microfluidics is revolutionizing fluid handling in diagnostic and research settings, enabling high-throughput screening and miniaturized assays with minimal sample volumes. Sensor technologies are becoming increasingly sophisticated, allowing for real-time monitoring of fluid levels, pressure, and flow rates within the systems, providing critical feedback for automated adjustments and early detection of potential issues. Connectivity through IoT (Internet of Things) platforms is transforming fluid management by enabling remote monitoring, predictive maintenance, and seamless data exchange across different medical devices and IT infrastructure.

Furthermore, advancements in materials science contribute to the development of safer and more biocompatible consumables, such as anti-microbial coated catheters and advanced filtration membranes, reducing the risk of infections. The use of robotics and automation in fluid handling systems for laboratory and pharmaceutical applications is also gaining traction, enhancing throughput and reproducibility. These technological innovations collectively aim to deliver more intuitive, integrated, and reliable fluid management solutions that address complex clinical needs and optimize healthcare delivery.

The market's growth is primarily driven by the increasing global prevalence of chronic diseases such as kidney failure and cardiovascular conditions, an aging population, and continuous technological advancements leading to more precise and safer fluid management solutions. The rising demand for minimally invasive procedures and home healthcare also contributes significantly.

The consumables segment typically holds a substantial market share due to the recurring need for single-use items like catheters, tubing sets, and fluid bags across all fluid management procedures. However, infusion pumps and dialysis equipment also represent significant and growing product segments.

AI is set to revolutionize fluid management by enhancing precision in fluid delivery, enabling predictive maintenance for devices, personalizing patient treatment plans based on real-time data, and improving overall operational efficiency through advanced analytics and automation. It aims to reduce errors and optimize clinical workflows.

Key challenges include the high initial cost of advanced fluid management systems, stringent regulatory approval processes that can impede market entry, the potential risk of healthcare-associated infections, and the scarcity of skilled professionals required to operate and maintain sophisticated equipment.

The Asia Pacific (APAC) region is projected to offer the most significant growth opportunities due to its large and growing patient population, improving healthcare infrastructure, increasing healthcare expenditure, and rising adoption of advanced medical technologies across countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.