ID : MRU_ 429589 | Date : Nov, 2025 | Pages : 257 | Region : Global | Publisher : MRU

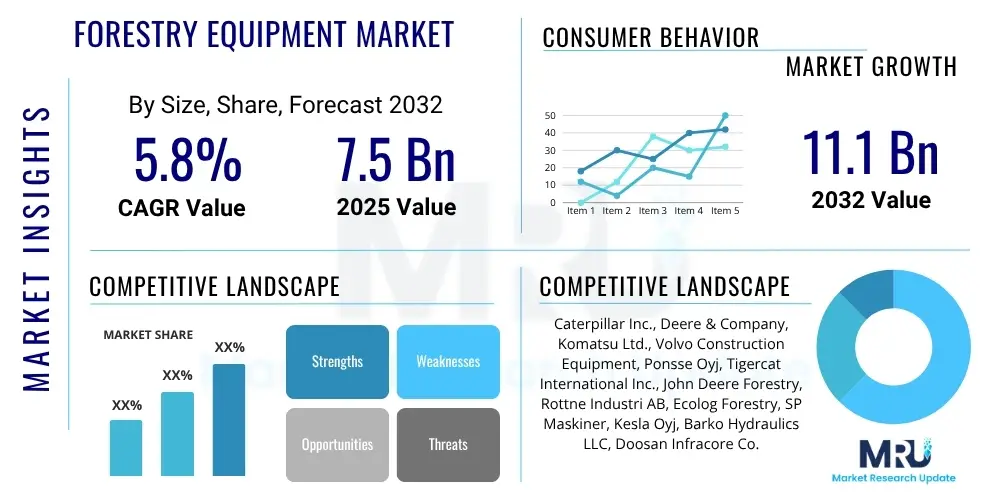

The Forestry Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2032. The market is estimated at $7.5 billion in 2025 and is projected to reach $11.1 billion by the end of the forecast period in 2032.

The global forestry equipment market stands as a cornerstone of the modern timber industry, providing essential machinery for the sustainable harvesting, processing, and transportation of forest resources. This vital sector supports not only traditional lumber production but also burgeoning industries such as pulp and paper, bioenergy, and even specialized construction. The equipment range is designed to address diverse operational requirements, from dense boreal forests to scattered plantations, ensuring efficiency, safety, and adherence to environmental stewardship principles. As global demand for wood products continues to escalate, alongside a heightened focus on ecological balance and forest health, the role of advanced forestry machinery becomes increasingly indispensable for both commercial and conservation efforts.

Modern forestry equipment encompasses a sophisticated suite of machines, each engineered for specific tasks within the logging and forestry management lifecycle. Key product categories include harvesters, which are multi-functional machines capable of felling, delimbing, and bucking trees; forwarders, designed for transporting processed logs from the stump to a roadside landing; and skidders, used to drag whole trees or large sections to processing sites. Other critical equipment includes feller bunchers for rapid tree felling, loaders for efficient material handling, chippers and grinders for converting wood waste into biomass, and mulchers for site preparation or forest fire prevention. These machines are increasingly integrated with advanced technologies, optimizing their performance, reducing fuel consumption, and minimizing their ecological footprint through precision operations.

The primary applications of this equipment span commercial timber harvesting, selective logging for forest thinning and health improvement, and significant contributions to reforestation and afforestation projects. The benefits derived from employing modern forestry equipment are multi-faceted, notably including substantial increases in operational efficiency and productivity, directly translating into reduced labor costs and faster project completion times. Furthermore, the robust design and advanced controls of these machines significantly enhance worker safety by automating hazardous manual tasks. A critical driving factor for market expansion is the global push towards sustainable forest management, where mechanized equipment, often equipped with GPS and telematics, allows for precise, low-impact operations. This, coupled with the rising demand for wood-based products and continuous technological innovations, positions the forestry equipment market for sustained growth, adapting to both economic pressures and environmental responsibilities.

The global Forestry Equipment Market is currently navigating a period of dynamic transformation, propelled by a confluence of evolving business trends, significant regional shifts, and specialized segmental demands. At a macro level, the industry is witnessing an accelerated adoption of automation, digitalization, and electrification, which are becoming central to manufacturers' strategies for enhancing machine capabilities. Companies are heavily investing in research and development to integrate sophisticated telematics, real-time data analytics, and predictive maintenance solutions, all aimed at boosting operational uptime, optimizing resource allocation, and providing unparalleled insights into fleet performance. This focus on smart forestry solutions is redefining traditional logging practices, emphasizing efficiency, cost-effectiveness, and environmental compliance, fundamentally reshaping the competitive landscape and driving innovation across the entire value chain.

From a regional perspective, the market presents a diverse mosaic of growth patterns and technological maturity. North America and Europe continue to represent cornerstone markets, characterized by high levels of mechanization, strict environmental regulations, and a robust demand for advanced, high-performance equipment. These regions are often at the forefront of adopting innovative solutions like electric and hybrid machinery, and autonomous systems, driven by sustainability targets and labor cost pressures. Conversely, the Asia Pacific region is rapidly emerging as a pivotal growth engine. Fueled by burgeoning populations, rapid industrialization, and extensive infrastructure development, countries like China, India, and Indonesia are experiencing a significant shift from traditional manual logging to mechanized operations, consequently driving substantial demand for both new and refurbished forestry equipment. Latin America and the Middle East & Africa also demonstrate considerable potential, albeit with varying paces of modernization and specific needs related to their unique forest types and economic development stages.

Segmental trends within the market underscore the evolving priorities of end-users. Harvesters and forwarders remain the foundational pillars, essential for efficient felling, processing, and transportation of timber, and continue to account for the largest share of market revenue. However, the biomass harvesting equipment segment is experiencing particularly vigorous growth, reflecting the global pivot towards renewable energy sources and the increasing utilization of forest residues for bioenergy production. Furthermore, there is a distinct upward trend in the demand for specialized equipment catering to precision forestry, which leverages technologies like drones and advanced GIS to optimize forest management. The ongoing development of compact and versatile machinery also addresses the needs of smaller forest owners and selective logging operations, indicating a market responsive to both large-scale industrial requirements and niche, sustainable practices.

Common user questions regarding AI's influence on the Forestry Equipment Market often center on its capacity to dramatically improve operational efficiency, minimize costs through optimized resource utilization, and significantly enhance worker safety by reducing human exposure to hazardous tasks. Users frequently inquire about the practical implementation of autonomous forestry vehicles, the efficacy of AI-driven predictive maintenance systems, and the ability of AI algorithms to optimize logging routes and timber processing. There is also considerable interest in how AI can contribute to more sustainable forest management practices, such as precise tree identification and health monitoring. However, alongside this enthusiasm, concerns are frequently raised regarding the substantial initial capital investment required for AI integration, the technical challenges associated with deploying AI in rugged and unpredictable forest environments, and the critical need for upskilling the workforce to manage these sophisticated systems. The potential impact on employment due to automation and the imperative for robust cybersecurity measures for connected machinery are also key points of discussion.

Based on this analysis, the key themes, concerns, and expectations users have about AI's influence in this domain revolve around transformative improvements in productivity and safety, balanced against the practicalities of adoption and workforce adaptation. Users expect AI to move forestry operations towards a more data-driven, precise, and environmentally conscious paradigm. The integration of AI is seen as an opportunity to overcome long-standing industry challenges, such as labor shortages and the need for higher yields, while simultaneously promoting sustainable practices. Yet, a clear apprehension exists regarding the accessibility of these advanced technologies for smaller operators and the broader societal implications of increased automation. Bridging the gap between technological potential and practical, equitable implementation remains a central challenge and expectation for the market.

The Forestry Equipment Market is profoundly influenced by a complex interplay of Drivers, Restraints, Opportunities, and broader Impact Forces that shape its trajectory and competitive landscape. A significant driver is the persistent and growing global demand for wood and wood products across various sectors, including construction, furniture manufacturing, pulp and paper, and increasingly, bioenergy production. This demand necessitates efficient and large-scale timber harvesting operations, which are increasingly reliant on mechanized solutions. Concurrently, the global shift towards sustainable forest management practices, mandated by environmental regulations and consumer preferences, pushes for the adoption of precision forestry equipment that minimizes waste and ecological footprint. Technological advancements, such as enhanced automation, improved fuel efficiency, and digital integration (telematics, GPS), further act as powerful drivers by increasing productivity, reducing operational costs, and improving safety for workers in hazardous forest environments.

Despite these strong tailwinds, the market faces notable restraints. The high initial capital investment required to acquire modern, technologically advanced forestry equipment can be prohibitive for smaller logging companies or those operating in developing economies, limiting market penetration. Furthermore, the industry is grappling with a persistent shortage of skilled operators and maintenance technicians capable of handling sophisticated machinery, which can lead to underutilization of assets and increased operational overheads. Environmental regulations, while driving sustainable practices, can also impose stringent operational restrictions, higher compliance costs, and limitations on harvesting areas, thereby acting as a restraint on market expansion. Economic volatility, including fluctuations in commodity prices for timber and macroeconomic slowdowns, can directly impact investment decisions for new equipment, presenting a cyclical challenge to market stability and growth.

Significant opportunities, however, exist for stakeholders within the forestry equipment market. The burgeoning global bioenergy sector presents a substantial opportunity for specialized biomass harvesting and processing equipment, converting forest residues into renewable energy. Emerging markets in Asia Pacific, Latin America, and Africa, characterized by vast untapped forest resources and a growing need for modern infrastructure, offer fertile ground for market expansion as these regions transition from manual to mechanized logging. The advancement of precision forestry techniques, leveraging IoT, AI, and remote sensing, opens new avenues for highly specialized, data-driven equipment that promises optimized yields and enhanced environmental performance. The ongoing trend towards electrification and the development of hybrid forestry machines further present opportunities for innovation and market differentiation, aligning with global sustainability goals. Beyond these, external impact forces such as the increasing frequency and intensity of forest fires due to climate change create demand for fire prevention and recovery equipment, while evolving government policies regarding land use, carbon sequestration, and international timber trade agreements continuously reshape market dynamics and investment priorities, requiring manufacturers and operators to remain agile and adaptive to a changing global landscape.

The Forestry Equipment Market is intricately segmented across several critical dimensions, providing a granular understanding of its structure, demand patterns, and growth drivers. This comprehensive segmentation allows for a detailed analysis of market dynamics, enabling manufacturers to strategically align their product portfolios with specific end-user requirements and regional nuances. The classification by equipment type highlights the diverse machinery employed throughout the forestry value chain, from initial felling to final processing and transportation. Further segmentation by application illuminates the primary uses of this equipment, reflecting the varying operational needs of commercial logging, forest management, and specialized biomass harvesting. Additionally, categorizing by power source reveals the industry's progression towards more sustainable energy solutions, while operational modes distinguish between traditional manual controls and advanced automated systems. This multi-faceted approach to segmentation is essential for dissecting market trends, identifying niche opportunities, and formulating targeted business strategies in a competitive global landscape.

The value chain of the Forestry Equipment Market is an intricate network of activities and participants, beginning from the conceptualization and manufacturing of specialized machinery to its eventual deployment and ongoing support in diverse forest environments. At the upstream end, the chain is heavily reliant on a sophisticated supplier ecosystem that provides critical raw materials and complex components. This includes manufacturers of high-strength steels, advanced composite materials for lighter yet durable structures, and precision engineering firms specializing in hydraulic systems, powertrains, and robust internal combustion engines or electric motors. Additionally, suppliers of cutting-edge electronics, sensors, GPS modules, and telematics systems are fundamental, as these components enable the smart functionalities and connectivity that define modern forestry equipment. Strategic partnerships between OEMs and these component suppliers are crucial for ensuring quality, innovation, and a resilient supply chain, particularly given the specialized nature and demanding operating conditions of forestry machinery.

Moving through the midstream, the core manufacturing and assembly processes transform these raw materials and components into finished forestry machines. This phase involves intricate design, engineering, and rigorous testing to ensure durability, performance, and compliance with safety and environmental standards. OEMs invest substantially in R&D to continuously innovate, integrating features that enhance efficiency, operator comfort, and sustainability. Post-manufacturing, the downstream segment of the value chain focuses on distribution, sales, and comprehensive aftermarket services. Distribution channels are varied and strategically chosen to reach a broad customer base. Large-scale logging corporations and governmental forestry agencies often engage in direct procurement from OEMs, facilitating customized solutions and direct technical support. This direct model allows manufacturers to maintain close relationships with their largest clients, understanding their evolving needs firsthand and providing bespoke equipment configurations.

Conversely, an extensive network of independent dealers and distributors forms a vital indirect channel, particularly for serving small to medium-sized logging contractors, private forest owners, and regional operators. These dealers play a pivotal role by providing localized sales expertise, financing options, demonstration units, and critical aftermarket services such as parts inventory, routine maintenance, emergency repairs, and technical training. The effectiveness of this dealer network is paramount for customer satisfaction and brand loyalty, as equipment uptime is crucial in time-sensitive logging operations. Furthermore, rental companies represent another significant component of the downstream value chain, offering flexible equipment access for short-term projects, seasonal work, or for businesses looking to mitigate large capital expenditures. The entire value chain is characterized by a strong emphasis on reliability, robust support systems, and the ability to adapt to demanding environmental conditions, ensuring that high-value forestry assets remain productive throughout their operational lifespan and contributing to the overall sustainability of the timber industry.

The Forestry Equipment Market caters to a diverse range of potential customers, all of whom share a common objective: efficient and sustainable management or harvesting of forest resources. At the forefront are commercial logging companies, which represent the largest segment of end-users. These enterprises vary significantly in scale, from vast multinational timber corporations managing extensive forest tracts to smaller, family-owned businesses operating within specific regions. Their demand encompasses a full spectrum of heavy machinery, including feller bunchers, harvesters, forwarders, and skidders, essential for high-volume, cost-effective timber extraction. The choice of equipment often depends on the type of forest, terrain, timber size, and environmental regulations, leading to a highly customized demand profile for manufacturers.

Beyond traditional logging, a substantial customer base exists within the broader wood products industry. Sawmills, pulp and paper manufacturers, and composite board producers require specialized forestry equipment for processing raw timber into usable forms. This includes industrial-grade debarkers, chippers, grinders, and material handlers that are integrated into their mill operations. These customers prioritize efficiency, reliability, and the ability to process large volumes of wood consistently to maintain their production lines. Their purchasing decisions are often influenced by the total cost of ownership, including fuel efficiency, maintenance requirements, and the availability of spare parts and service support.

Furthermore, governmental forestry departments and public land management agencies constitute another significant segment of potential customers. These entities acquire forestry equipment for a variety of purposes, including sustainable forest management, reforestation initiatives, wildfire prevention and suppression, pest and disease control, and the maintenance of forest infrastructure like roads and trails. Their purchasing criteria often include strict environmental compliance, long-term durability, and versatility for diverse tasks. Private forest owners, ranging from individual landowners managing small woodlots to large investment funds overseeing thousands of acres of timberland, also represent a growing customer segment. They typically seek versatile, often smaller-scale equipment for thinning, selective harvesting, and general forest maintenance, valuing ease of use and economic efficiency. Lastly, the burgeoning bioenergy sector is creating a new demand for specialized biomass harvesting and processing equipment, as forest residues and dedicated energy crops are increasingly utilized for renewable energy generation, expanding the customer landscape for relevant machinery.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $7.5 billion |

| Market Forecast in 2032 | $11.1 billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., Deere & Company, Komatsu Ltd., Volvo Construction Equipment, Ponsse Oyj, Tigercat International Inc., John Deere Forestry, Rottne Industri AB, Ecolog Forestry, SP Maskiner, Kesla Oyj, Barko Hydraulics LLC, Doosan Infracore Co. Ltd., Guangxi Liugong Machinery Co. Ltd., Weifang Taihong Tractor Co. Ltd., FAE Group S.p.A., Waratah Forestry Equipment, Hyundai Construction Equipment Co. Ltd., Liebherr Group, Log Max AB, Sandvik AB, Stihl AG Co KG, Husqvarna AB, ASV Holdings Inc., Sennebogen Maschinenfabrik GmbH, Kleemann GmbH, Bandit Industries Inc., Peterson Pacific Corp., Vermeer Corporation. |

| Regions Covered | North America (United States, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Nordic Countries, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Southeast Asia, Australia, Rest of APAC), Latin America (Brazil, Argentina, Rest of Latin America), Middle East, and Africa (MEA) (GCC Countries, South Africa, Rest of MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Forestry Equipment Market is currently undergoing a profound technological transformation, driven by a convergence of advancements aimed at optimizing operational efficiency, enhancing worker safety, and promoting environmental stewardship. Central to this evolution is the pervasive integration of Global Positioning Systems (GPS) and telematics systems. GPS provides precise location data for machines and facilitates accurate mapping of forest areas, enabling optimized logging plans and compliance with environmental boundaries. Telematics systems, on the other hand, transmit real-time operational data, including fuel consumption, engine diagnostics, and machine performance metrics, directly to operators and fleet managers. This connectivity allows for proactive maintenance scheduling, remote troubleshooting, and continuous performance monitoring, significantly reducing unplanned downtime and enhancing overall fleet management. The ability to collect and analyze this rich data is instrumental in making informed decisions that improve productivity and profitability.

Further reshaping the landscape is the widespread adoption of the Internet of Things (IoT) and advanced sensor technologies. IoT connectivity enables various components within a forestry machine, or even multiple machines across a site, to communicate seamlessly, creating a networked ecosystem. Sensors detect everything from tree diameter and species to soil conditions and obstacles, feeding crucial information into the machine's control systems. This data empowers features such as automated cutting heads, precise log bucking, and dynamic adjustments to machine operations based on real-time environmental inputs. Remote sensing, including the use of drones equipped with LiDAR and multispectral cameras, is revolutionizing forest inventory and health monitoring. Drones can rapidly survey vast areas, providing highly detailed topographical maps and tree-level data, which is invaluable for pre-harvest planning, post-harvest assessment, and early detection of forest diseases or pests, contributing significantly to sustainable forest management.

Looking to the future, the technology landscape is increasingly defined by automation, Artificial Intelligence (AI), and electrification. Automation is progressing from semi-autonomous functions, where machines assist operators with complex tasks, to fully autonomous systems capable of performing specific operations without direct human intervention in controlled environments. AI and Machine Learning (ML) algorithms are being deployed for tasks such as optimizing harvesting patterns, predictive maintenance, and even advanced visual recognition for timber sorting and quality grading, thereby maximizing resource value. Furthermore, the imperative for reduced emissions and lower operational noise is driving significant innovation in electric and hybrid forestry machines. These advancements, while representing substantial R&D investment, promise a future where forestry operations are not only more productive and safer but also significantly more environmentally friendly, aligning with global sustainability goals and expanding the possibilities for sustainable timber supply chains.

The global forestry equipment market is distinctly shaped by unique regional characteristics, encompassing varying forest management practices, economic development stages, and regulatory environments. These regional disparities create diverse market dynamics, presenting both strategic opportunities and specific challenges for manufacturers and stakeholders. A nuanced understanding of these localized conditions is crucial for effective market penetration, product development, and the establishment of robust distribution and service networks. The demand for specific equipment types, the adoption rate of advanced technologies, and the competitive intensity can vary significantly from one geographical area to another, necessitating tailored approaches for success in this global industry.

The Forestry Equipment Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2032. It is estimated to reach a market value of $11.1 billion by the end of the forecast period in 2032, driven by increased mechanization, global timber demand, and a focus on sustainable forest management.

Key drivers include the escalating global demand for timber and wood-derived products, the increasing adoption of mechanized logging for improved efficiency and enhanced worker safety, a growing worldwide emphasis on sustainable forest management practices, and continuous technological advancements in equipment design and functionality, such as automation and digital integration.

Major technological trends involve the extensive integration of AI, IoT, GPS, and telematics for enhanced automation, real-time data monitoring, and predictive maintenance. Furthermore, there is a significant shift towards electric and hybrid power sources to reduce emissions and operational noise, alongside the use of drones and remote sensing for precise forest inventory and management.

The Asia Pacific (APAC) region is anticipated to be the fastest-growing market. This growth is attributed to rapid industrialization, urbanization, substantial infrastructure development, and a surging demand for wood products, leading to a significant transition from manual to mechanized logging operations in countries such as China, India, and Southeast Asia.

The integration of AI and automation significantly enhances worker safety by enabling autonomous or semi-autonomous machine operations, thereby reducing human exposure to inherently hazardous tasks like felling and processing. Additionally, advanced operator assistance systems, powered by AI, minimize operator fatigue, provide critical real-time hazard warnings, and can prevent accidents by automating complex maneuvers or detecting unsafe conditions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.