ID : MRU_ 429827 | Date : Nov, 2025 | Pages : 257 | Region : Global | Publisher : MRU

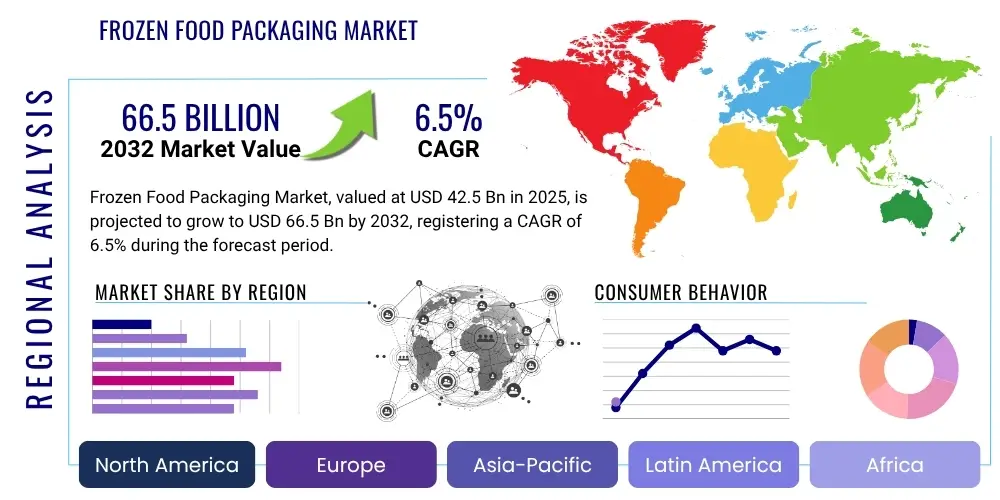

The Frozen Food Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at USD 42.5 Billion in 2025 and is projected to reach USD 66.5 Billion by the end of the forecast period in 2032.

The Frozen Food Packaging Market encompasses a diverse range of materials, innovative formats, and advanced technological solutions specifically engineered to meticulously preserve and robustly protect frozen food products throughout their entire complex lifecycle. This critical function includes safeguarding goods during rigorous cold storage conditions, navigating intricate global transportation logistics, and ensuring appealing presentation in vibrant retail display environments. The paramount objective of this specialized packaging is to ensure the inherent safety, maintain the superior quality, and provide a significantly extended shelf life for a vast and ever-expanding array of frozen commodities, spanning from nutrient-rich individually quick-frozen (IQF) vegetables and wholesome fruits to convenient ready meals and various processed meats. Effective packaging in this sector is critically designed to withstand the extreme low temperatures characteristic of commercial freezing, meticulously prevent the detrimental effects of freezer burn, which can degrade food quality, and provide robust barrier properties against external elements such as moisture, ambient oxygen, and potential microbial contaminants. By adeptly performing these functions, it plays a pivotal role in meticulously preserving the product's essential nutritional value, desirable texture, and overall sensory attributes right up until the moment of consumer consumption, thereby maintaining optimal product integrity and appeal.

The comprehensive product offerings within this dynamic market are extensive and remarkably varied, encompassing highly versatile flexible pouches, stable stand-up bags, durable rigid cartons, practical thermoformed trays, and protective multi-layer film wraps. These essential packaging formats are predominantly constructed from a carefully selected range of materials, such as various advanced types of plastics (including polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET)), sustainable and often recycled paperboard, lightweight yet strong aluminum, and sophisticated multi-layered laminates that synergistically combine diverse barrier functionalities. Major applications of these packaging solutions are widespread and continually expanding, catering comprehensively to both household retail frozen foods readily available on supermarket shelves, large-scale institutional food service operations for bulk supply to entities like schools and hospitals, and the extensive needs of industrial sectors requiring frozen ingredients for further processing. The intrinsic benefits derived from high-quality frozen food packaging are manifold and strategically impactful: they include vastly enhanced food preservation capabilities that minimize spoilage, significantly extended product usability that contributes to reduced food waste, and unparalleled convenience for modern consumers through easy storage and straightforward preparation. Furthermore, these solutions provide an effective platform for compelling branding and essential product information display in competitive retail settings, influencing purchasing decisions. These compelling advantages, intrinsically linked with the global shift towards increasingly demanding consumer lifestyles that prioritize convenience, health, and readily available meal options, serve as powerful and enduring driving forces propelling the substantial expansion and continuous innovation within the global frozen food packaging market, making it a critical component of the modern food industry infrastructure.

The global Frozen Food Packaging Market is currently experiencing a period of robust and sustained growth, fundamentally propelled by significant shifts in contemporary consumer preferences, which increasingly favor convenience and efficiency in daily living. This prominent trend is clearly reflected in the escalating proliferation of ready-to-eat and ready-to-cook frozen meals, designed for quick preparation, alongside the accelerating pace of urbanization across numerous developing economies worldwide, leading to smaller living spaces and less time for cooking. In terms of overarching business trends, there is an emphatic strategic focus on the development and widespread adoption of sustainable and environmentally friendly packaging solutions. This critical pivot is driven concurrently by growing consumer demand for eco-conscious products and by increasingly stringent global environmental regulations, such as single-use plastic bans and extended producer responsibility schemes. Consequently, leading companies within this sector are heavily investing in rigorous research and development to create and implement innovative recyclable, biodegradable, and compostable packaging materials, exploring options like bioplastics and advanced paperboard. Concurrently, efforts are concentrated on designing lightweight and highly efficient packaging structures aimed at significantly reducing their carbon footprint, minimizing logistics costs, and appealing directly to the expanding segment of environmentally aware consumers. Furthermore, the sophisticated integration of advanced printing technologies, offering greater customization, vivid graphics, and visual appeal, along with the incorporation of smart packaging features for enhanced product traceability, real-time freshness monitoring, and direct consumer engagement through QR codes or NFC tags, is rapidly emerging as a prominent industry trend. These innovations collectively represent the industry's proactive and adaptive response to the complexities of modern supply chain management and the evolving expectations of today's discerning, digitally-connected consumers.

Analyzing regional trends, the Asia Pacific region stands out as a particularly dynamic and rapidly expanding market segment, poised for continued leadership in growth. This accelerated expansion is primarily attributable to several intertwined socio-economic factors, including consistently rising disposable incomes that enable greater expenditure on convenience foods, the substantial proliferation of modern retail infrastructure, and the increasing adoption of westernized dietary habits among its vast and growing population. North America and Europe, while representing more mature and established markets, continue to demonstrate significant innovation, particularly in the premium frozen food sectors and in the relentless pursuit of more sustainable packaging alternatives, often driven by ambitious corporate sustainability goals and strong consumer advocacy. These regions frequently lead in the early adoption of cutting-edge packaging technologies and advanced materials, such as active packaging and intelligent film structures. Conversely, burgeoning markets situated in Latin America, the Middle East, and Africa are concurrently witnessing an accelerated pace of growth. This expansion is largely supported by continuous improvements in crucial cold chain logistics networks, which are essential for distributing frozen products, and the strategic expansion of modern retail formats into previously underserved urban and peri-urban areas. Within the segment analysis, flexible plastic-based packaging continues to hold a dominant market share, primarily due to its inherent cost-effectiveness, exceptional versatility, and proven performance characteristics in preserving frozen foods. However, there is a distinct and growing traction observed for paperboard and innovative bio-based alternatives, indicative of a broader industry shift towards more environmentally responsible options. The ready meals and meat & seafood categories are identified as particularly significant application segments and potent drivers of market growth, as contemporary busy lifestyles increasingly necessitate convenient, quick, and nutritious meal solutions, thereby stimulating further innovation and investment in sophisticated packaging designs that not only ensure robust product integrity but also maximize consumer appeal on crowded retail shelves and optimize supply chain efficiency.

User inquiries regarding the pervasive influence of Artificial Intelligence (AI) on the Frozen Food Packaging Market predominantly center around its potential to revolutionize operational efficiencies, dramatically enhance supply chain transparency, and facilitate the development of smarter, inherently more responsive packaging solutions. A recurrent key theme emerging from these inquiries is the transformative capacity of AI to meticulously optimize complex production lines through predictive maintenance and process control, enabling far more accurate demand forecasting by analyzing vast datasets, and significantly contributing to a substantial reduction in waste generation throughout the entire packaging process, from raw material sourcing to final product delivery. Consumers and industry stakeholders are also intensely interested in understanding precisely how AI can be leveraged to advance sustainable practices within the sector. This includes, but is not limited to, optimizing material usage to minimize excess through smart design, improving the precision and efficacy of recycling sorting mechanisms through AI-powered vision, and enabling highly personalized packaging experiences through data analytics. Furthermore, there is a strong expectation that AI will play a critical role in developing robust quality control systems capable of detecting even subtle defects with unprecedented precision and consistency. The overarching sentiment points towards a clear anticipation that AI integration will ultimately lead to the establishment of more intelligent, highly adaptive, and resource-efficient packaging ecosystems that are better equipped to meet the multifaceted challenges and dynamic demands of the modern food industry, enhancing both profitability and environmental responsibility.

The Frozen Food Packaging Market is dynamically shaped by a complex interplay of influential drivers, inherent challenges acting as restraints, and compelling opportunities that collectively dictate its growth trajectory, strategic investments, and overall directional evolution. A primary and increasingly potent driver is the consistently rising global consumer demand for convenience foods. This demand is significantly propelled by accelerating urbanization rates worldwide, the growing prevalence of dual-income households with limited time, and the pervasive shift towards busier, more demanding lifestyles, all of which make readily available and easy-to-prepare frozen meals an exceptionally attractive and often indispensable dietary option for a broad consumer base. Furthermore, the extensive global expansion of organized retail sectors, including supermarkets, hypermarkets, and specialized frozen food stores, coupled with substantial improvements and technological advancements in cold chain infrastructure—such as advanced refrigeration technologies and efficient logistics networks—particularly across burgeoning developing economies, dramatically boosts both the accessibility and consumption volumes of a wide array of frozen products. Concurrently, continuous innovations and technological breakthroughs in packaging materials and designs, offering superior barrier properties, enhanced structural integrity, and critically extended shelf life, play an absolutely crucial role in meticulously maintaining food quality, significantly reducing product spoilage, and minimizing food waste across the entire supply chain, thereby robustly driving market demand and fostering heightened consumer confidence.

However, the market is simultaneously confronted by several notable restraints that pose significant challenges to its unbridled growth and operational fluidity. Foremost among these is the escalating global concern regarding environmental sustainability, particularly the pervasive issue of plastic waste and the growing imperative for genuinely sustainable alternatives. This societal pressure and increasing regulatory scrutiny, including bans on certain plastic types and mandates for recycled content, compel packaging manufacturers to make substantial investments in often costly research and development initiatives focused on eco-friendly and circular economy-aligned materials, which can inherently impact profitability and necessitate complex retooling of production lines. Another significant hurdle is the substantial initial capital investment required for acquiring and implementing state-of-the-art, high-speed packaging machinery, such as advanced form-fill-seal systems, and developing robust, efficient recycling infrastructure capable of processing diverse, multi-material packaging types. Additionally, the proliferation of stringent food safety regulations, coupled with widely varying regional and national packaging standards (e.g., EU regulations vs. FDA guidelines), mandates rigorous compliance and complex testing, adding intricate layers of complexity, operational costs, and potential legal liabilities to the entire production and distribution process. Moreover, the inherent volatility in the prices of key raw materials, most notably various plastic resins, paper pulp, and aluminum, can lead to unpredictable fluctuations in production costs, thereby impacting market stability, profit margins, and long-term strategic planning for packaging providers, often forcing them to absorb or pass on increased costs.

Despite these significant restraints, the Frozen Food Packaging Market abounds with numerous opportunities for profound innovation, strategic diversification, and substantial market expansion. The continuous development and commercialization of truly biodegradable, industrially compostable, and highly recyclable packaging materials represents a monumental growth avenue, perfectly aligning with ambitious global sustainability objectives and rapidly evolving consumer preferences for environmentally responsible products. The explosive growth of e-commerce platforms for groceries and prepared meals creates a distinct and increasing demand for specialized packaging solutions that are robust enough to withstand the unique rigors of direct-to-consumer delivery, including multiple handling points, variable climatic conditions, and extended transit times, while impeccably maintaining product integrity and thermal stability throughout the critical last-mile delivery process. Moreover, the burgeoning demand for premium, specialized, and often niche frozen food categories—such as organic, gluten-free, plant-based, and gourmet ready-meals—offers discerning manufacturers an exceptional chance to significantly differentiate their products through innovative, high-quality, and aesthetically appealing packaging designs that communicate value, specialty, and brand identity effectively. The strategic adoption and integration of advanced smart packaging technologies, including quick response (QR) codes for enhanced product traceability, sophisticated NFC tags for interactive consumer engagement, and highly responsive freshness indicators that visually signal product condition, further elevate consumer trust, provide verifiable transparency, and unlock entirely new value propositions within this dynamic and competitive market, promising future avenues for growth, enhanced brand loyalty, and improved supply chain management.

The Frozen Food Packaging Market is meticulously analyzed through a comprehensive segmentation based on core attributes such as material composition, structural type, and specific application categories, providing a granular and multi-dimensional view of market dynamics. This detailed approach is invaluable for discerning specific growth opportunities, identifying inherent challenges within each distinct segment, and understanding the intricate interplay between evolving consumer preferences, rapid technological advancements, and the nuanced impacts of regional and global regulatory frameworks across a diverse spectrum of product types and end-use scenarios. The material segment rigorously differentiates between the various primary components utilized in packaging construction, encompassing both traditional fossil-fuel-derived plastics and emerging sustainable options. The type segment systematically categorizes packaging based on its fundamental physical structure and flexibility, distinguishing between highly versatile flexible solutions and structurally robust rigid options. Lastly, the application segment precisely identifies the myriad frozen food categories that extensively utilize these specialized packaging solutions, thereby offering critical insights into prevailing consumption patterns, evolving dietary trends, and broader industry demands, allowing for targeted product development and market strategies.

The intricate value chain underpinning the Frozen Food Packaging Market commences with critical upstream activities, primarily involving a sophisticated network of raw material suppliers. These fundamental players are responsible for sourcing and providing essential inputs such as various polymer resins (e.g., polyethylene, polypropylene, PET), sustainably harvested paper pulp, high-grade aluminum, and a spectrum of specialty additives, including barrier coatings, printing inks, and adhesives. These foundational raw materials undergo initial, rigorous processing and meticulous conversion into intermediate packaging components like films, sheets, granules, or paperboard stock. Key participants at this initial stage strategically focus on securing cost-effective, consistently high-quality, and, increasingly, environmentally sustainable raw materials to proactively meet the evolving demands of the market and adhere to tightening global regulatory standards. Collaborative partnerships with leading chemical companies, innovative material science research institutions, and specialized additive manufacturers are absolutely crucial for the continuous development of advanced barrier properties, enhanced structural integrity, and novel eco-friendly alternatives. This upstream segment forms the indispensable foundational input upon which all subsequent packaging production and value addition processes are built, directly impacting the quality, performance, and sustainability profile of the final product.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2032 | USD 66.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Inc., Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, Sonoco Products Company, Ardagh Group S.A., Smurfit Kappa Group plc, WestRock Company, Constantia Flexibles GmbH, ProAmpac LLC, TC Transcontinental Inc., Pactiv Evergreen Inc., Winpak Ltd., Printpack Inc., RPC Group (now part of Berry Global), Schur Flexibles Group, DS Smith Plc, Coveris Holdings SA, Graham Packaging Company. |

| Regions Covered | North America (U.S., Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC), Latin America (Brazil, Argentina, Rest of Latin America), Middle East, and Africa (MEA) (UAE, Saudi Arabia, South Africa, Rest of MEA). |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Frozen Food Packaging Market is characterized by a relentless pursuit of innovation, driven by significant technological advancements aimed at optimizing food preservation, bolstering sustainability efforts, and enhancing overall manufacturing efficiency. One of the paramount areas of ongoing innovation resides within material science, where intense focus is directed towards developing cutting-edge barrier films. These films are meticulously engineered to offer genuinely superior protection against the ingress of oxygen and moisture, thereby critically extending the shelf life of highly sensitive frozen products and meticulously preventing the detrimental effects of freezer burn, which can severely compromise taste, texture, and nutritional value. Such advanced solutions frequently incorporate multi-layer co-extruded films and sophisticated coating technologies, often integrating specialized high-barrier polymers like EVOH (ethylene vinyl alcohol) or implementing metallization processes to impart exceptionally robust barrier properties, crucial for delicate frozen seafood and meats. In parallel with the continuous refinement of traditional plastic materials, there is a powerful and accelerating momentum towards the research, development, and widespread implementation of truly sustainable alternatives. This includes innovative bioplastics (such as PLA – Polylactic Acid, derived from renewable resources like corn starch, and PHA – Polyhydroxyalkanoates, produced by microbial fermentation), plastics containing high percentages of post-consumer recycled (PCR) content, and advanced compostable films designed to break down in industrial composting facilities. All these options represent a concerted effort to address pervasive environmental concerns while rigorously maintaining the essential performance characteristics demanded by the frozen food sector.

The market is primarily driven by the escalating global consumer demand for convenience foods, influenced by increasingly busy lifestyles, global urbanization trends, and the expansion of modern retail. Significant growth factors also include robust advancements and improvements in crucial cold chain infrastructure, particularly in developing economies, and continuous material science innovation leading to extended shelf life and enhanced product protection for a diverse range of frozen items.

The Frozen Food Packaging Market confronts several significant challenges, most notably the growing global environmental concerns over plastic waste, which necessitates substantial investment in developing and adopting genuinely sustainable alternatives like bioplastics and recycled content. Other key hurdles include the inherently high costs associated with implementing advanced packaging technologies, the unpredictable volatility in raw material prices impacting production costs, and the complex landscape of adhering to increasingly stringent food safety and diverse regional packaging regulations.

Plastics, particularly widely used variants such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET), continue to be predominantly utilized due to their exceptional versatility, superior barrier properties against moisture and oxygen essential for preventing freezer burn, and overall cost-effectiveness. Additionally, paperboard is extensively employed for rigid cartons and boxes due to its printability and sustainability appeal, and aluminum is frequently used for trays and foil wraps, both providing excellent protective and thermal characteristics for various frozen applications requiring oven-readiness.

Sustainability has emerged as a paramount and transformative trend, vigorously driving demand for packaging solutions manufactured from recycled content, those that are inherently recyclable, biodegradable, or industrially compostable materials. Manufacturers are strategically investing in lightweight designs, pursuing responsible sourcing practices, and innovating in material science to significantly reduce their environmental footprint and proactively meet the evolving expectations of both environmentally conscious consumers and increasingly strict regulatory bodies worldwide, fostering a shift towards a circular economy for packaging.

Technology plays a pivotal and transformative role in shaping the future of frozen food packaging. It is instrumental in developing highly advanced smart packaging with integrated features such as real-time temperature indicators, robust anti-tamper devices, and comprehensive traceability codes (e.g., QR, RFID), significantly enhancing existing barrier properties of materials through multi-layer structures, enabling sophisticated automation of production lines, and facilitating flexible digital printing for greater customization. These innovations collectively aim to drastically improve food safety, maximize operational efficiency, and profoundly enhance consumer engagement across the entire frozen food supply chain, from production to consumption.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.