ID : MRU_ 430522 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

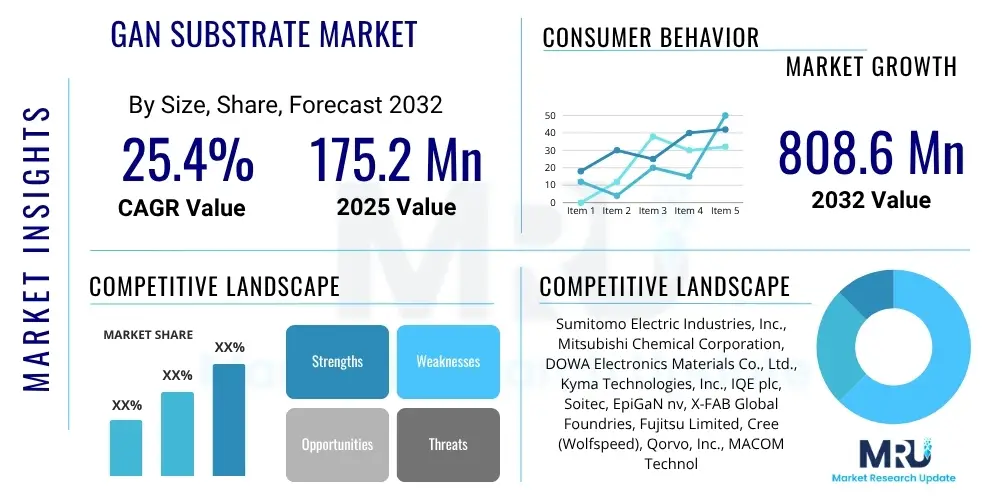

The GaN Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.4% between 2025 and 2032. The market is estimated at $175.2 Million in 2025 and is projected to reach $808.6 Million by the end of the forecast period in 2032.

The Gallium Nitride (GaN) Substrate Market encompasses the production and utilization of GaN wafers and epitaxy for advanced semiconductor devices. GaN is a wide bandgap semiconductor material renowned for its superior electronic properties, including high breakdown voltage, fast switching speed, high thermal conductivity, and radiation hardness, which surpass those of traditional silicon. This unique combination makes GaN ideal for high-power, high-frequency, and high-temperature applications, driving its adoption across various industries.

GaN substrates serve as the foundational material for manufacturing a wide range of devices such as power transistors, radio frequency (RF) amplifiers, light-emitting diodes (LEDs), and lasers. These products are critical components in modern technology, enabling enhanced efficiency, reduced size, and improved performance in end-user applications. The primary applications for GaN substrates include power electronics for efficient energy conversion, RF devices for telecommunications, and optoelectronics for lighting and display technologies. The inherent benefits of GaN, such as higher power density and lower energy losses, are crucial for advancing technological capabilities.

Key driving factors for the GaN Substrate Market include the escalating demand for high-efficiency power electronics in electric vehicles (EVs) and charging infrastructure, the global rollout of 5G networks requiring advanced RF components, and the continuous expansion of data centers necessitating more energy-efficient power supplies. Additionally, the increasing focus on energy conservation and the need for compact, lightweight electronic solutions are significant market accelerators, positioning GaN as a pivotal material in the next generation of semiconductor innovation.

The GaN Substrate Market is experiencing robust growth, primarily fueled by technological advancements and increasing adoption in high-performance applications. Business trends indicate a significant shift towards wide bandgap semiconductors, with GaN emerging as a preferred material due to its superior power handling and high-frequency capabilities. Key market players are investing heavily in research and development to improve manufacturing processes, reduce costs, and develop larger diameter substrates, thereby expanding the commercial viability and application scope of GaN technology. Strategic collaborations and partnerships are also becoming prevalent as companies seek to consolidate their positions and accelerate innovation within the competitive landscape.

Regional trends reveal Asia Pacific as the dominant market, driven by its extensive manufacturing infrastructure, rapid deployment of 5G, and robust growth in consumer electronics and automotive industries, particularly in countries like China, Japan, and South Korea. North America and Europe are also significant contributors, characterized by strong R&D activities, early adoption in defense and aerospace sectors, and increasing investments in electric vehicle technologies and renewable energy systems. These regions are focused on developing advanced GaN-based solutions to enhance energy efficiency and reduce carbon footprints, aligning with global sustainability initiatives.

Segmentation trends highlight power electronics and RF devices as the leading application segments, experiencing substantial growth due to their critical roles in electric vehicles, fast chargers, 5G infrastructure, and data centers. The optoelectronics segment, while mature, continues to innovate, especially in advanced LED and laser applications. Substrate types are evolving, with ongoing efforts to improve the quality and availability of bulk GaN substrates, which offer superior performance compared to heteroepitaxial GaN on silicon or sapphire, albeit at a higher cost. These dynamic trends underscore a vibrant market poised for continued expansion and diversification.

User inquiries regarding AI's influence on the GaN Substrate Market frequently center on how artificial intelligence-driven technologies necessitate more efficient and high-performance power and RF components, thereby directly impacting the demand for GaN. Users are keen to understand if AI's massive computational and data processing requirements, particularly in data centers and edge computing, will accelerate GaN adoption due to its energy efficiency and ability to handle high power densities. Concerns often revolve around the scalability of GaN production to meet future AI demands, the integration challenges with existing AI hardware ecosystems, and whether AI itself can optimize GaN manufacturing processes or design. There is a clear expectation that AI will be a significant long-term driver for GaN, pushing the boundaries of power management and communication within next-generation AI infrastructure.

The GaN Substrate Market is propelled by a confluence of strong drivers, balanced by notable restraints, while presenting significant opportunities for growth and innovation. The increasing global demand for high-efficiency power conversion across various sectors, including electric vehicles and renewable energy, acts as a primary market driver. Concurrently, the extensive deployment of 5G telecommunication networks necessitates advanced RF devices that leverage GaN's high-frequency capabilities. However, the market faces hurdles such as the high manufacturing cost of GaN substrates and devices compared to traditional silicon, alongside the technical complexities associated with scaling up substrate production to larger diameters. These challenges highlight the need for continuous research and development to achieve cost efficiencies and manufacturing maturity.

Opportunities for the GaN market are vast and diversified, extending into emerging applications like satellite communication, industrial IoT, and advanced medical devices, where GaN's robust performance characteristics offer distinct advantages. Furthermore, ongoing innovations in bulk GaN growth techniques and the development of hybrid GaN-on-silicon solutions are expanding the material's accessibility and reducing cost barriers. The overall impact forces shaping this market are characterized by intense competition from alternative materials like SiC in specific power applications, the growing bargaining power of key customers seeking customized solutions, and the critical role of intellectual property and technological leadership in differentiating market players. Regulatory push for energy efficiency globally also exerts a positive influence, favoring the adoption of GaN-based solutions.

The GaN Substrate Market is comprehensively segmented based on substrate type, application, end-use industry, and region, reflecting the diverse characteristics and strategic importance of this advanced material. This segmentation allows for a detailed understanding of market dynamics, specific growth drivers within each category, and the varying technological requirements of different sectors. By analyzing these segments, stakeholders can identify niche opportunities, assess competitive landscapes, and formulate targeted strategies for market penetration and expansion. The intricate interplay between these segments defines the market's current structure and future trajectory, emphasizing the versatility and critical role of GaN across numerous high-tech domains.

The value chain for the GaN Substrate Market is a multi-layered ecosystem involving several critical stages, from the procurement of raw materials to the distribution of finished GaN-based devices. Upstream activities involve the sourcing and purification of gallium and nitrogen, along with the manufacturing of support substrates like sapphire, silicon, or silicon carbide, which are crucial for heteroepitaxial growth. This stage also includes the development and provision of specialized equipment for crystal growth and epitaxy. The quality and cost-effectiveness of these initial components significantly influence the final product's performance and market price, with a few specialized suppliers dominating the supply of high-purity raw materials and advanced growth equipment.

Midstream activities primarily focus on the manufacturing of GaN substrates, either through bulk (homoepitaxial) growth for pure GaN wafers or through epitaxial deposition of GaN layers onto foreign substrates (heteroepitaxial). This segment involves advanced chemical vapor deposition (CVD) techniques, such as Metalorganic Chemical Vapor Deposition (MOCVD) or Hydride Vapor Phase Epitaxy (HVPE), which require significant capital investment and specialized expertise. Following substrate preparation, device fabricators process these wafers into integrated circuits, transistors, and diodes. Downstream activities encompass the assembly of these GaN devices into modules and their integration into final products by original equipment manufacturers (OEMs) across various end-use industries.

Distribution channels for GaN substrates and devices typically involve a mix of direct and indirect approaches. Direct sales are common for large-volume customers, particularly major semiconductor manufacturers and integrated device manufacturers (IDMs), allowing for closer technical collaboration and customized solutions. Indirect channels involve a network of distributors and value-added resellers who provide broader market reach, technical support, and logistical services to smaller and mid-sized enterprises. The complexity of GaN technology often necessitates strong technical partnerships throughout the distribution network to ensure proper application and integration, thus reinforcing the importance of expert knowledge at every stage of the value chain.

Potential customers for GaN substrates and devices span a wide array of industries, primarily comprising manufacturers and integrators developing advanced electronic systems that demand high efficiency, power density, and operational reliability. These end-users are driven by the need to meet stringent performance requirements, reduce energy consumption, and enable smaller form factors in their products. Key buyers often include companies at the forefront of technological innovation, seeking to leverage GaN's superior properties to gain a competitive edge in rapidly evolving markets. Their purchasing decisions are influenced by factors such as device performance, cost-effectiveness over the product lifecycle, and the ability of GaN solutions to address specific application challenges that silicon-based technologies cannot efficiently overcome.

The automotive industry represents a significant and growing customer base, especially manufacturers of electric vehicles (EVs) and hybrid vehicles. These companies utilize GaN for on-board chargers, DC-DC converters, and traction inverters, aiming to improve vehicle range, reduce battery size, and enhance overall power management efficiency. Similarly, the telecommunications sector, particularly those involved in the rollout of 5G infrastructure, are crucial buyers. They procure GaN RF devices for base station amplifiers, active antenna systems, and satellite communication modules, where GaN's high-frequency performance and power output are indispensable for robust and high-speed networks. The shift to higher frequencies and wider bandwidths in 5G makes GaN a vital enabling technology for network operators and equipment providers globally.

Beyond automotive and telecom, the consumer electronics market is a strong customer segment, with rapid adoption of GaN in fast chargers for smartphones, laptops, and other portable devices, driven by the demand for smaller, lighter, and more efficient power adapters. Industrial and data center operators also represent substantial potential customers, as they increasingly seek GaN-based power supplies to improve the energy efficiency of servers, industrial motor drives, and renewable energy inverters, thereby reducing operational costs and environmental impact. The aerospace and defense sector, requiring high-reliability and radiation-hardened components for radar, avionics, and electronic warfare, further underscores the diverse and critical customer landscape for GaN technology.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $175.2 Million |

| Market Forecast in 2032 | $808.6 Million |

| Growth Rate | 25.4% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sumitomo Electric Industries, Inc., Mitsubishi Chemical Corporation, DOWA Electronics Materials Co., Ltd., Kyma Technologies, Inc., IQE plc, Soitec, EpiGaN nv, X-FAB Global Foundries, Fujitsu Limited, Cree (Wolfspeed), Qorvo, Inc., MACOM Technology Solutions Holdings, Inc., Infineon Technologies AG, STMicroelectronics N.V., ON Semiconductor Corporation, GaN Systems Inc., Navitas Semiconductor Corporation, Nexperia B.V., Toshiba Corporation, Broadcom Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The GaN Substrate Market is characterized by a dynamic and evolving technology landscape, primarily driven by advancements in crystal growth methods and epitaxial techniques aimed at improving material quality, increasing wafer size, and reducing manufacturing costs. One foundational technology is Hydride Vapor Phase Epitaxy (HVPE), widely used for growing thick GaN layers and bulk GaN substrates, offering high growth rates and good material quality. However, HVPE still faces challenges in achieving truly free-standing, large-diameter GaN wafers with low defect densities at commercial scales. Another critical method is Metalorganic Chemical Vapor Deposition (MOCVD), essential for growing thin, high-quality GaN epitaxial layers on various foreign substrates like sapphire, silicon carbide, and silicon, particularly for LED and power device applications. MOCVD enables precise control over layer thickness and doping profiles, critical for device performance.

The choice of substrate for GaN epitaxy is a significant technological consideration. While homoepitaxial GaN (GaN grown on GaN substrates) offers superior material quality with minimal lattice mismatch, leading to fewer defects and better device performance, its high cost and limited availability of large-diameter wafers remain a challenge. Therefore, heteroepitaxial growth on readily available and cost-effective substrates like silicon (GaN-on-Si) and silicon carbide (GaN-on-SiC) has gained considerable traction. GaN-on-Si is favored for power electronics due to its potential for integration with established silicon fabrication processes and larger wafer sizes, while GaN-on-SiC is preferred for high-frequency RF applications due to silicon carbide's excellent thermal conductivity and higher cost. Developments in buffer layer technologies are crucial for mitigating lattice and thermal mismatch when growing GaN on foreign substrates, enabling higher quality epilayers.

Emerging technologies include advanced bulk GaN growth techniques like high-pressure solution growth and ammonothermal methods, which promise larger, higher-quality, and more cost-effective native GaN substrates in the long term. Furthermore, innovations in device architectures, such as High Electron Mobility Transistors (HEMTs) and advanced vertical GaN devices, are continuously leveraging these substrate advancements. The focus is also on developing GaN-on-AlN substrates for extreme high-frequency and high-power applications, offering an alternative to SiC. Miniaturization, enhanced thermal management solutions, and the integration of GaN with other wide bandgap materials are key areas of ongoing research, all contributing to a vibrant technological ecosystem that continues to push the boundaries of semiconductor performance.

North America is a significant market for GaN substrates, driven by robust investments in research and development, particularly in the aerospace and defense sectors. The region benefits from strong government funding for advanced material science and semiconductor technology, leading to innovation in high-power RF applications such as radar systems and electronic warfare. Additionally, the growing electric vehicle market and expansion of data centers contribute to the increasing demand for high-efficiency GaN power devices. The presence of leading semiconductor companies and academic institutions actively engaged in GaN research further solidifies its market position, focusing on both bulk GaN and advanced GaN-on-SiC solutions for demanding applications.

The United States leads the regional market, characterized by a mature semiconductor industry and significant adoption of GaN in telecom infrastructure upgrades, including 5G deployments. There is also a strong emphasis on developing GaN-based solutions for renewable energy systems, such as solar inverters and grid infrastructure, aligning with national energy efficiency goals. Canadian innovation in GaN is steadily progressing, particularly in niche high-frequency communication technologies. The regional market is marked by strategic collaborations between industry players and government agencies to accelerate the commercialization of new GaN technologies.

Europe demonstrates substantial growth in the GaN Substrate Market, primarily fueled by the burgeoning automotive industry's pivot towards electric mobility and the strong industrial sector's demand for efficient power management. Countries like Germany, France, and the UK are at the forefront of EV manufacturing and research, integrating GaN power semiconductors into on-board chargers, inverters, and DC-DC converters to enhance vehicle performance and range. This drive for energy efficiency also extends to industrial power supplies, motor drives, and automation systems, where GaN's superior properties offer considerable advantages over traditional silicon-based solutions. European environmental regulations and targets for carbon reduction further incentivize the adoption of energy-efficient GaN technology.

The region is also a key hub for advanced research in wide bandgap semiconductors, with numerous universities and research institutes contributing to advancements in GaN material science and device fabrication. Collaborative projects funded by the European Union aim to strengthen the domestic supply chain and foster innovation across the value chain, from substrate manufacturing to final device integration. While less dominant than APAC in overall semiconductor production, Europe excels in high-value, niche applications requiring custom GaN solutions. The telecommunications sector also contributes to demand, particularly for high-frequency GaN RF devices used in regional 5G deployments and satellite communication systems.

The Asia Pacific region stands as the largest and fastest-growing market for GaN substrates, driven by its unparalleled manufacturing capabilities, rapid industrialization, and extensive consumer electronics market. Countries such as China, Japan, South Korea, and Taiwan are at the epicenter of GaN production and consumption, benefiting from vast investments in semiconductor foundries and a robust supply chain. The aggressive rollout of 5G networks across the region is a primary catalyst, propelling demand for GaN RF devices in base stations and related communication infrastructure. The massive consumer electronics industry further fuels growth, with GaN being widely adopted in compact, fast chargers for smartphones, laptops, and other portable devices.

Beyond consumer electronics and telecom, the APAC automotive market, particularly the rapid growth of electric vehicles in China and South Korea, significantly contributes to GaN demand for power electronics. Government initiatives and strategic national plans in several APAC countries prioritize the development of advanced semiconductor materials, including GaN, to enhance technological independence and global competitiveness. This region is not only a major consumer but also a key innovator, with significant R&D efforts aimed at improving GaN material quality, increasing wafer sizes, and reducing production costs to cater to its massive and diverse market needs. The sheer scale of industrial and technological expansion in APAC ensures its continued dominance in the GaN Substrate Market.

The Latin American GaN Substrate Market is in its nascent stages but is experiencing steady growth, driven primarily by increasing infrastructure development and expanding digitalization efforts. The region's growing adoption of 5G technology, albeit slower than other major regions, is gradually stimulating demand for GaN RF components in telecommunication base stations. Additionally, the nascent electric vehicle market and investments in renewable energy projects, particularly solar power, are creating opportunities for GaN-based power electronics. Countries like Brazil and Mexico are leading regional adoption, supported by foreign investments and local initiatives aimed at modernizing infrastructure and improving energy efficiency.

The Middle East and Africa (MEA) GaN Substrate Market is emerging, propelled by significant government investments in diversifying economies away from oil, focusing on technological advancement and sustainable energy. Countries in the Gulf Cooperation Council (GCC) are investing heavily in smart city initiatives and advanced communication networks, including 5G, which drives demand for GaN RF devices. Furthermore, the region's abundant solar resources are encouraging the adoption of solar power, creating a market for efficient GaN power electronics in inverters. While the market is smaller compared to other regions, a growing emphasis on industrial modernization and defense spending also contributes to the increased interest and adoption of GaN technology for high-performance applications.

Gallium Nitride (GaN) is a wide bandgap semiconductor material known for its superior electronic properties, including high breakdown voltage, fast switching speed, and high thermal conductivity. It is important because it enables the creation of more efficient, powerful, and compact electronic devices compared to traditional silicon, addressing the growing demand for energy efficiency and higher performance in modern electronics.

The GaN Substrate Market growth is primarily driven by three key application areas: power electronics (e.g., electric vehicles, fast chargers, data center power supplies), RF devices (e.g., 5G base stations, radar systems), and optoelectronics (e.g., LEDs, laser diodes). These sectors leverage GaN's high efficiency and performance advantages.

The primary challenges include the relatively high manufacturing cost of GaN substrates and devices compared to silicon, technical complexities in scaling up production to larger wafer diameters, and intense competition from other wide bandgap materials like Silicon Carbide (SiC) in certain high-power applications. Overcoming these requires significant R&D and process optimization.

GaN-on-Silicon (GaN-on-Si) technology offers cost advantages and larger wafer sizes by leveraging mature silicon manufacturing infrastructure. However, it suffers from lattice and thermal mismatch, requiring buffer layers that can impact device performance. Bulk GaN substrates, or homoepitaxial GaN, provide superior material quality with fewer defects and better thermal properties, leading to higher performance devices, but are currently more expensive and available in smaller diameters.

Asia Pacific is the largest and fastest-growing market for GaN substrates, primarily due to extensive manufacturing capabilities, rapid deployment of 5G networks, and a thriving consumer electronics industry. Countries like China, Japan, and South Korea are major producers and consumers, driving significant innovation and adoption across various GaN applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.