ID : MRU_ 430714 | Date : Nov, 2025 | Pages : 241 | Region : Global | Publisher : MRU

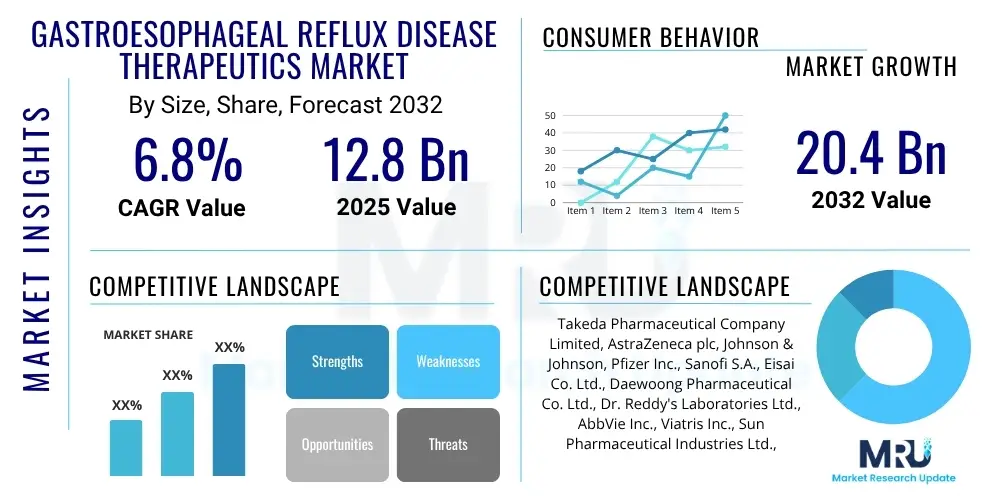

The Gastroesophageal Reflux Disease Therapeutics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at $12.8 Billion in 2025 and is projected to reach $20.4 Billion by the end of the forecast period in 2032.

The Gastroesophageal Reflux Disease (GERD) Therapeutics market encompasses pharmaceutical and non-pharmacological interventions aimed at managing and treating the symptoms and complications associated with GERD, a chronic digestive disorder characterized by the reflux of stomach acid into the esophagus. GERD affects a substantial portion of the global population, leading to discomfort and potentially severe health issues if left untreated. Therapeutic products for GERD include a diverse range of medications such as proton pump inhibitors (PPIs), H2 receptor antagonists, antacids, and prokinetic agents, along with emerging novel therapies targeting different mechanisms of action. The primary goal of these therapeutics is to alleviate symptoms like heartburn and acid regurgitation, heal esophageal damage, and prevent long-term complications such as esophagitis, strictures, and Barrett's esophagus, ultimately enhancing the patient's quality of life.

Major applications of GERD therapeutics span across various patient populations, from those experiencing mild, intermittent symptoms to individuals with severe erosive esophagitis or precancerous conditions. The benefits of effective GERD management are profound, including significant symptom relief, improved sleep patterns, reduction in esophageal inflammation, and a decreased risk of surgical intervention. The market is driven by several critical factors, including the increasing global prevalence of GERD, largely attributed to evolving dietary habits, sedentary lifestyles, rising obesity rates, and an aging population more susceptible to digestive disorders. Furthermore, heightened awareness among patients and healthcare providers regarding the chronic nature of GERD and the importance of early intervention continues to fuel market expansion. Ongoing research and development activities aimed at discovering more potent, safer, and longer-acting therapeutic options, along with advancements in diagnostic tools that enable earlier and more accurate diagnosis, also contribute significantly to market growth.

The Gastroesophageal Reflux Disease Therapeutics Market is experiencing dynamic shifts driven by evolving business trends, regional growth patterns, and distinct segment transformations. Business trends indicate a strong focus on innovation, with pharmaceutical companies investing heavily in the development of novel drug classes, such as potassium-competitive acid blockers (P-CABs) and neuromodulators, to address the unmet needs of patients unresponsive to conventional therapies like PPIs. Concurrently, the market faces intense generic competition as patents for several blockbuster drugs expire, necessitating strategies focused on product differentiation and value-added services. Strategic collaborations and mergers and acquisitions are also prominent, allowing companies to expand their product portfolios and geographical reach, consolidating market positions in a competitive landscape. Furthermore, the rising adoption of digital health solutions and telemedicine is influencing how GERD patients are monitored and managed, presenting new avenues for growth and patient engagement.

Regionally, North America and Europe continue to dominate the GERD therapeutics market due to high disease prevalence, well-established healthcare infrastructures, significant healthcare expenditure, and robust R&D activities. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by increasing awareness, improving healthcare access, a growing middle class with changing lifestyles, and a large patient pool. Latin America, the Middle East, and Africa are also showing considerable potential, with rising disposable incomes and expanding healthcare facilities contributing to market expansion. Segment trends highlight the enduring dominance of proton pump inhibitors (PPIs) as the first-line treatment due to their efficacy in acid suppression. Nonetheless, there is a gradual shift towards advanced therapies offering faster onset of action, improved side effect profiles, and solutions for refractory GERD. The market also sees growth in over-the-counter (OTC) options, catering to consumers seeking immediate and accessible relief for mild symptoms. Additionally, the development of combination therapies and personalized medicine approaches is gaining traction, promising more tailored and effective treatment outcomes for diverse patient needs.

User inquiries concerning AI's influence on the Gastroesophageal Reflux Disease Therapeutics Market frequently revolve around its potential to revolutionize diagnosis, personalize treatment strategies, accelerate drug discovery, and enhance patient management. Key themes include the ability of AI to interpret complex diagnostic data more accurately, identify patient phenotypes for targeted therapies, streamline preclinical and clinical trials, and develop predictive models for treatment response and disease progression. Concerns often relate to data privacy, the ethical implications of AI-driven healthcare decisions, and the need for robust validation of AI algorithms. Overall, there is a clear expectation that AI will significantly improve efficiency, precision, and innovation within the GERD therapeutic landscape, moving towards more effective and patient-centric care.

The Gastroesophageal Reflux Disease Therapeutics Market is shaped by a complex interplay of drivers, restraints, opportunities, and various impact forces that collectively dictate its growth trajectory and competitive dynamics. Key drivers propelling market expansion include the escalating global prevalence of GERD, significantly influenced by dietary changes, increasing obesity rates, and the aging population which is more susceptible to digestive disorders. Enhanced public awareness regarding GERD symptoms and available treatments, coupled with improved diagnostic capabilities, leads to earlier disease detection and a greater demand for therapeutic interventions. Furthermore, continuous advancements in pharmaceutical research and development, particularly the introduction of novel drug classes with improved efficacy and safety profiles, are vital in sustaining market momentum. These factors collectively create a fertile ground for market growth by expanding the patient base and improving treatment accessibility.

However, the market also faces substantial restraints that temper its growth. The expiration of patents for several blockbuster GERD medications, especially PPIs, has led to a surge in generic alternatives, intensifying price competition and eroding the profit margins of branded drug manufacturers. Concerns regarding the long-term safety and potential side effects associated with prolonged use of certain GERD medications, particularly PPIs, such as increased risk of kidney disease, bone fractures, and infections, prompt caution among healthcare providers and patients. Moreover, stringent regulatory approval processes for new drugs and high R&D costs can delay market entry for innovative therapies, limiting the pace of market evolution. These restraints compel market players to innovate beyond traditional drug development and focus on differentiation.

Opportunities within the GERD therapeutics market are abundant, particularly in emerging economies where improving healthcare infrastructure, increasing disposable incomes, and a rising awareness of health issues are driving greater access to treatment. The development of novel drug targets and therapeutic approaches, including potassium-competitive acid blockers (P-CABs) and therapies addressing esophageal hypersensitivity or motility disorders, represents significant growth avenues. Furthermore, the integration of combination therapies, personalized medicine strategies based on genetic markers, and non-pharmacological interventions like dietary modifications and lifestyle management programs, offer diversified treatment pathways. The market is also subject to various impact forces, including the bargaining power of buyers (healthcare providers, insurance companies) demanding cost-effective treatments and the bargaining power of suppliers (raw material manufacturers) influencing production costs. The threat of new entrants, while mitigated by high R&D costs and regulatory hurdles, keeps established players focused on innovation, while the threat of substitute products, such as surgical interventions or lifestyle changes, encourages pharmaceutical companies to demonstrate superior efficacy and patient convenience. Intense competitive rivalry among existing players, driven by product differentiation and market share acquisition, further defines the market's dynamic landscape.

The Gastroesophageal Reflux Disease Therapeutics Market is comprehensively segmented to provide a detailed understanding of its diverse components, allowing for targeted analysis of market dynamics and growth opportunities. This segmentation typically categorizes the market based on drug class, distribution channel, and application, each reflecting distinct aspects of demand, supply, and patient needs. Analyzing these segments is crucial for stakeholders to identify lucrative niches, develop precise marketing strategies, and anticipate future market shifts. The prevalence of different drug classes, the accessibility through various distribution channels, and the varying requirements across different GERD applications collectively shape the overall market landscape, driving innovation and competition.

The segmentation by drug class is particularly important as it highlights the types of pharmacological interventions available and their market share. Proton pump inhibitors (PPIs) currently dominate this segment due to their high efficacy in acid suppression, but other classes like H2 receptor antagonists and antacids remain significant for milder symptoms or specific patient profiles. The distribution channel segmentation illustrates how these therapeutics reach the end-user, differentiating between hospital pharmacies, retail pharmacies, and the growing online pharmacy sector. This distribution landscape reflects evolving consumer preferences for convenience and accessibility. Finally, segmentation by application delineates the specific GERD conditions being treated, such as erosive esophagitis, non-erosive reflux disease (NERD), and Barrett's esophagus, indicating areas of high unmet medical need and therapeutic focus.

The value chain for the Gastroesophageal Reflux Disease Therapeutics Market is a complex and multi-stage process, beginning with extensive upstream activities such as research and development, active pharmaceutical ingredient (API) manufacturing, and the sourcing of raw materials. The upstream segment involves significant investment in scientific discovery to identify new drug targets, synthesize novel compounds, and conduct preclinical studies to establish efficacy and safety. This phase is capital-intensive and requires specialized expertise. Raw material suppliers play a crucial role, providing high-quality chemicals and ingredients essential for API synthesis. Ensuring a robust and compliant supply chain for these critical components is paramount for pharmaceutical manufacturers to maintain product quality and regulatory standards.

Moving downstream, the value chain encompasses drug formulation, clinical trials, large-scale manufacturing, packaging, and regulatory approval processes. After successful clinical trials demonstrating safety and efficacy, the drug enters commercial production where APIs are formulated into final dosage forms like tablets, capsules, or liquids, followed by stringent quality control. Packaging and labeling are critical steps to ensure product integrity and compliance with diverse regional regulations. The distribution channel then takes over, facilitating the movement of finished products from manufacturers to end-users. This involves a network of wholesalers, distributors, and logistics providers who ensure efficient storage, transport, and delivery to various points of sale.

The market primarily utilizes both direct and indirect distribution channels. Direct channels involve pharmaceutical companies selling their products directly to large hospital systems, government health programs, or major integrated healthcare networks. This approach often allows for better control over pricing and marketing messages. Conversely, indirect channels, which are more common, rely on a network of third-party distributors and wholesalers who then supply to retail pharmacies, hospital pharmacies, and increasingly, online pharmacies. Online pharmacies represent a rapidly growing segment, offering convenience and broader accessibility for patients. Both direct and indirect models are essential for comprehensive market penetration, each presenting distinct advantages and challenges in terms of reach, cost-efficiency, and stakeholder engagement within the GERD therapeutics market.

Potential customers for Gastroesophageal Reflux Disease Therapeutics are diverse and span across various segments of the healthcare ecosystem, ranging from individual patients to large institutional buyers. The primary end-users are individuals suffering from GERD, whether diagnosed with mild symptoms like occasional heartburn or more severe conditions such as erosive esophagitis, Barrett's esophagus, or related complications requiring long-term pharmacological management. These patients seek relief from symptoms, healing of esophageal damage, and prevention of disease progression, often purchasing medications through retail pharmacies or receiving them via hospital prescriptions. The growing global prevalence of GERD, driven by lifestyle factors, diet, and an aging population, ensures a continuously expanding patient base seeking effective therapeutic solutions.

Beyond individual patients, healthcare providers constitute a significant segment of potential customers. This includes gastroenterologists, general practitioners, family physicians, and other specialists who diagnose GERD and prescribe appropriate therapeutic regimens. Hospitals, clinics, and outpatient care centers are institutional buyers that procure GERD medications in bulk to serve their patient populations, often relying on formularies and preferred drug lists. The decision-making process for these entities is influenced by drug efficacy, safety profiles, cost-effectiveness, and inclusion in national or regional treatment guidelines. Moreover, pharmacists, both in retail and hospital settings, play a crucial role in recommending over-the-counter (OTC) options and dispensing prescription medications, acting as key intermediaries and influencers for patient purchasing decisions.

Furthermore, entities such as government healthcare programs, private health insurance providers, and managed care organizations are critical indirect customers. These organizations heavily influence market dynamics through their formulary decisions, reimbursement policies, and cost-containment strategies, which directly impact drug accessibility and affordability for patients. Their purchasing decisions are often based on health economic outcomes, clinical guidelines, and population health management objectives. Therefore, pharmaceutical companies targeting the GERD therapeutics market must engage with a broad spectrum of stakeholders, understanding the varied needs and purchasing drivers across individual patients, healthcare professionals, and institutional payers to achieve comprehensive market penetration and sustained growth.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $12.8 Billion |

| Market Forecast in 2032 | $20.4 Billion |

| Growth Rate | CAGR 6.8% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Takeda Pharmaceutical Company Limited, AstraZeneca plc, Johnson & Johnson, Pfizer Inc., Sanofi S.A., Eisai Co. Ltd., Daewoong Pharmaceutical Co. Ltd., Dr. Reddy's Laboratories Ltd., AbbVie Inc., Viatris Inc., Sun Pharmaceutical Industries Ltd., Alfasigma S.p.A., Sebela Pharmaceuticals, Inc., Reata Pharmaceuticals, Inc., CinRx Pharma, Inc., Ironwood Pharmaceuticals, Inc., Ardelyx, Inc., Otsuka Pharmaceutical Co. Ltd., Teva Pharmaceutical Industries Ltd., Endo International plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Gastroesophageal Reflux Disease Therapeutics Market is continually evolving, driven by significant advancements in medical technology and pharmaceutical research aimed at improving diagnostic accuracy, enhancing treatment efficacy, and reducing side effects. One prominent technological area involves the development of novel drug delivery systems designed to optimize medication absorption, prolong therapeutic effects, and minimize systemic exposure. This includes extended-release formulations, targeted delivery systems that release active pharmaceutical ingredients directly at the site of action, and innovative oral dosage forms that improve patient adherence and convenience. These advancements represent a crucial step towards personalized and more effective patient management, especially for chronic conditions like GERD that require long-term treatment.

Another critical aspect of the technology landscape is the emergence of new drug classes that operate through distinct mechanisms of action, offering alternatives to traditional proton pump inhibitors (PPIs) and H2 receptor antagonists. Potassium-competitive acid blockers (P-CABs), for instance, have gained traction due to their faster onset of action and superior acid suppression compared to PPIs, particularly in patients with severe or refractory GERD. Furthermore, research into neuromodulators, therapies targeting transient receptor potential (TRP) channels, and agents focused on improving esophageal motility or barrier function are indicative of a shift towards more targeted and comprehensive management strategies that address the multifaceted pathophysiology of GERD. These innovative therapeutic approaches aim to overcome the limitations of existing treatments and cater to diverse patient needs.

Beyond pharmacological interventions, diagnostic technologies play a pivotal role in the GERD therapeutics market. Advanced endoscopic techniques, such as high-resolution manometry and multichannel intraluminal impedance-pH monitoring, provide more precise assessments of esophageal motility and acid reflux patterns, facilitating accurate diagnosis and guiding treatment decisions. Imaging technologies with enhanced capabilities, including narrow-band imaging and confocal laser endomicroscopy, assist in detecting subtle mucosal changes and identifying pre-cancerous conditions like Barrett's esophagus at earlier stages. Moreover, the integration of digital health solutions, wearable devices, and telehealth platforms is transforming patient monitoring and engagement. These technologies allow for continuous tracking of symptoms, medication adherence, and lifestyle factors, enabling healthcare providers to deliver more personalized care and allowing patients to actively manage their condition, thereby creating a more holistic approach to GERD management.

Primary treatments for GERD include proton pump inhibitors (PPIs) and H2 receptor antagonists for acid suppression, antacids for immediate symptom relief, prokinetic agents to improve gastric motility, and newer therapies like potassium-competitive acid blockers (P-CABs). Lifestyle modifications, such as dietary changes and elevation of the head during sleep, are also crucial components of GERD management.

The GERD therapeutics market is projected to grow significantly, estimated to reach $20.4 Billion by 2032 from $12.8 Billion in 2025, at a Compound Annual Growth Rate (CAGR) of 6.8%. This growth is driven by increasing disease prevalence, lifestyle changes, an aging population, and continuous advancements in therapeutic solutions.

Recent innovations in GERD treatment include the development of Potassium-Competitive Acid Blockers (P-CABs) offering faster onset and more potent acid suppression, novel neuromodulators targeting esophageal hypersensitivity, and advancements in drug delivery systems for improved patient adherence and efficacy. Research into therapies for specific GERD phenotypes and personalized medicine approaches is also gaining traction.

Yes, non-pharmacological approaches are essential for managing GERD. These include lifestyle modifications such as avoiding trigger foods (e.g., fatty foods, caffeine, acidic foods), eating smaller and more frequent meals, not lying down immediately after eating, elevating the head of the bed, weight management, and quitting smoking. These strategies can significantly reduce symptoms and complement medication therapy.

The GERD therapeutics market faces challenges such as intense generic competition due to patent expirations of blockbuster drugs, concerns regarding the long-term side effects of certain medications (like PPIs), stringent regulatory approval processes for new drugs, and the need for more effective treatments for refractory GERD. These factors necessitate continuous innovation and differentiation strategies from market players.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.