ID : MRU_ 430815 | Date : Nov, 2025 | Pages : 243 | Region : Global | Publisher : MRU

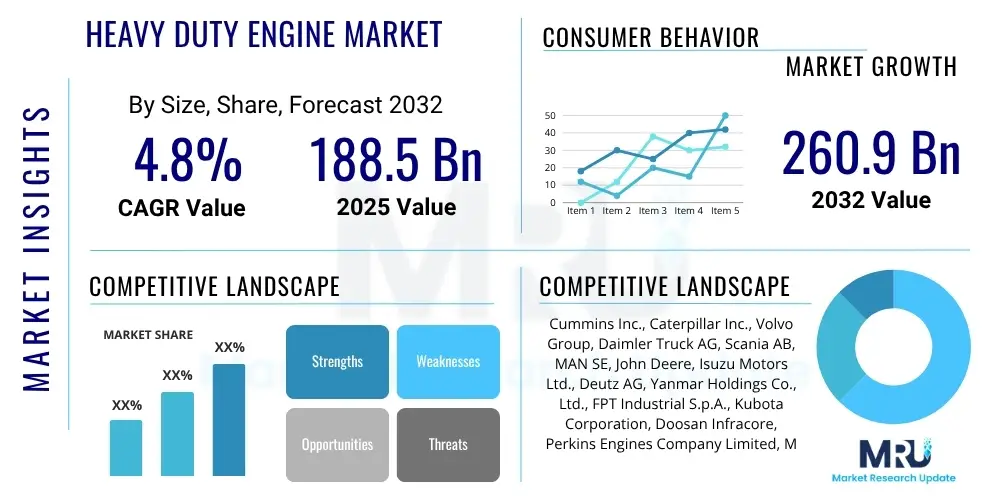

The Heavy Duty Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2032. The market is estimated at USD 188.5 billion in 2025 and is projected to reach USD 260.9 billion by the end of the forecast period in 2032.

The Heavy Duty Engine market encompasses power units specifically designed for demanding applications requiring substantial power, torque, and durability over extended operational periods. These engines are engineered to withstand rigorous conditions, high load factors, and continuous operation, making them indispensable across various industrial sectors. Their robust construction and advanced technological features ensure reliability and performance in environments where failure is not an option. The market is primarily driven by the expanding global economy, which fuels demand for transportation, infrastructure development, resource extraction, and agricultural productivity.

Products within this market range from traditional internal combustion engines, predominantly diesel, to increasingly prevalent natural gas, hybrid, and electric powertrains. Key applications include commercial vehicles such as heavy trucks and buses, construction and mining equipment, marine vessels, agricultural machinery, and power generation units. The benefits of modern heavy duty engines include improved fuel efficiency, reduced emissions through advanced aftertreatment systems, enhanced power density, and extended service intervals. These advancements not only contribute to operational cost savings but also help meet increasingly stringent environmental regulations worldwide.

Major driving factors for the heavy duty engine market include significant global infrastructure projects, the expansion of e-commerce necessitating larger logistics fleets, and the continuous modernization of industrial equipment. Technological advancements focusing on efficiency gains, emissions reduction, and digitalization are also pivotal in shaping market growth. Furthermore, the rising adoption of alternative fuels and electrification initiatives presents new opportunities for manufacturers to innovate and diversify their product portfolios, aligning with global sustainability goals while meeting evolving performance demands.

The Heavy Duty Engine Market is currently undergoing a transformative phase, characterized by significant business trends towards sustainable power solutions and digital integration. Manufacturers are heavily investing in research and development to offer engines that comply with stringent emission regulations, leading to a surge in hybrid, electric, and alternative fuel options. This shift is accompanied by a growing emphasis on smart engines equipped with IoT and AI capabilities for predictive maintenance, remote diagnostics, and optimized performance, thereby enhancing operational efficiency and reducing downtime for end-users. Globalization of manufacturing and supply chains continues, though recent disruptions have highlighted the need for greater resilience and localization in critical component production.

Regional trends indicate varied growth trajectories and technological adoption rates. Asia Pacific, particularly China and India, remains a dominant growth engine due to rapid industrialization, urbanization, and massive infrastructure spending. North America and Europe are at the forefront of adopting advanced emission standards and exploring electrification, driven by environmental mandates and strong consumer demand for greener transportation and industrial solutions. Latin America and the Middle East & Africa regions are experiencing steady growth, fueled by resource extraction industries, agricultural expansion, and ongoing infrastructure development, with a gradual uptake of more efficient and compliant engine technologies.

Segmentation trends highlight the enduring dominance of diesel engines, particularly in high-power and long-haul applications, albeit with continuous technological improvements for lower emissions. However, natural gas engines are gaining traction, especially in urban transport and specific industrial applications, owing to their lower carbon footprint and stable fuel prices in certain regions. The most significant shift is observed in the burgeoning hybrid and electric engine segments, which are projected to exhibit the highest growth rates over the forecast period. This growth is propelled by supportive government policies, advancements in battery technology, and increasing corporate sustainability commitments, fundamentally reshaping the future landscape of heavy duty power solutions across all application areas.

Users frequently inquire about how Artificial Intelligence will revolutionize the operational efficiency, maintenance strategies, and design paradigms within the heavy duty engine market. Key concerns revolve around AI's capacity to enhance fuel economy, predict potential mechanical failures before they occur, and optimize engine performance in real-time. There is also considerable interest in AI's role in developing next-generation engines that are more adaptable, environmentally friendly, and seamlessly integrated into smart ecosystems. Expectations include significant reductions in operational costs, prolonged engine lifespan, and a transition towards more autonomous and data-driven fleet management.

The Heavy Duty Engine Market is significantly influenced by a confluence of driving forces, restraining factors, and emerging opportunities. Key drivers include robust global infrastructure spending, particularly in developing economies, which stimulates demand for construction and mining equipment. The burgeoning e-commerce sector is also fueling the expansion of logistics and commercial vehicle fleets, directly increasing the need for powerful and efficient heavy duty engines. Furthermore, increasingly stringent global emission regulations compel manufacturers to invest in advanced engine technologies that reduce pollutants, thereby driving innovation and product upgrades across the market. Technological advancements focused on enhancing fuel efficiency, improving power density, and integrating digital solutions are continuously reshaping market offerings and driving adoption.

Conversely, several restraints impede the market's growth trajectory. The high initial capital expenditure associated with purchasing heavy duty engines, especially those incorporating advanced technologies or alternative fuels, can be a barrier for smaller businesses. Volatility and disruptions in global supply chains for critical components and raw materials pose significant manufacturing challenges, impacting production schedules and costs. The rising prominence of alternative powertrain solutions, such as full-electric and fuel cell engines, presents a long-term competitive threat to conventional heavy duty engines. Moreover, fluctuating global fuel prices and raw material costs introduce economic uncertainties, while macroeconomic slowdowns can temper demand for new equipment and vehicles across key end-use sectors, thereby restraining market expansion.

Despite these challenges, substantial opportunities exist for market participants. The ongoing trend towards electrification and hybridization of heavy duty vehicles and equipment opens new avenues for technological development and market penetration. Research into and adoption of hydrogen as a viable fuel source for heavy duty applications represents a promising long-term opportunity. The integration of advanced telematics, Internet of Things (IoT), and big data analytics offers opportunities for improved engine performance monitoring, predictive maintenance, and optimized fleet management. Furthermore, the expansion into emerging markets with growing industrial bases and the increasing demand for retrofitting and upgrading existing engine fleets to meet newer emission standards present considerable growth prospects for manufacturers and service providers alike. Government incentives and supportive policies for clean energy technologies also play a crucial role in creating favorable market conditions for these opportunities.

The Heavy Duty Engine Market is broadly segmented based on several critical attributes including fuel type, application, power output, and technology. This comprehensive segmentation allows for a detailed analysis of market dynamics, competitive landscapes, and growth prospects within specific niches. Understanding these segments is crucial for manufacturers to tailor their product development strategies, for suppliers to optimize their offerings, and for end-users to make informed purchasing decisions based on their operational requirements and sustainability goals. Each segment is influenced by unique drivers, regulations, and technological advancements, leading to varying growth rates and market shares across the forecast period.

The value chain for the heavy duty engine market is complex and involves multiple stages, from raw material sourcing to end-user deployment and aftermarket services. At the upstream stage, it begins with the extraction and processing of essential raw materials such as steel, aluminum, copper, and various specialized alloys, which are then supplied to component manufacturers. These component manufacturers specialize in producing critical engine parts like cylinder blocks, crankshafts, pistons, turbochargers, fuel injection systems, and electronic control units. The quality and availability of these components are paramount to the final engine product's performance and reliability. Strong relationships with reliable upstream suppliers are critical for engine manufacturers to ensure a steady supply of high-quality materials and components, managing costs and production timelines effectively.

Further along the chain, these components are assembled by heavy duty engine manufacturers, who design, produce, and test the complete engine units. These manufacturers often engage in extensive research and development to innovate new engine technologies, improve fuel efficiency, reduce emissions, and enhance power output. Once manufactured, the engines are distributed through various channels to downstream entities. The primary distribution channel involves direct sales to Original Equipment Manufacturers (OEMs) who integrate these engines into their final products, such as heavy trucks, construction machinery, agricultural equipment, or marine vessels. These OEMs then distribute their complete vehicles or equipment to end-users through their established dealer networks.

Indirect distribution channels also play a significant role, particularly in the aftermarket for replacement engines and components, or for specific industrial applications where engines are sold directly to integrators or independent distributors. These distributors often cater to smaller fleet operators, industrial clients, or provide specialized service and parts support. Aftermarket services, including maintenance, repairs, and spare parts supply, form a crucial part of the downstream value chain, ensuring the longevity and optimal performance of heavy duty engines throughout their operational life. The efficiency and effectiveness of both direct and indirect distribution channels are vital for market penetration, customer satisfaction, and maintaining competitive advantage, with digital platforms increasingly facilitating parts sales and service scheduling.

The heavy duty engine market serves a diverse array of end-users and buyers, all of whom require robust, reliable, and powerful engines for their critical operations. These customers operate across various industrial sectors, with their purchasing decisions often driven by factors such as total cost of ownership, regulatory compliance, fuel efficiency, durability, and the availability of comprehensive aftermarket support. Understanding the specific needs and operational environments of these diverse customer segments is essential for engine manufacturers to develop targeted products and marketing strategies, ensuring their offerings align with customer expectations for performance and value.

Primary end-users include commercial fleet operators, ranging from large logistics companies managing extensive truck fleets for freight transportation to public and private entities operating bus services for passenger transport. Construction companies, involved in infrastructure projects, real estate development, and civil engineering, represent another major customer group, requiring engines for excavators, loaders, graders, and other heavy machinery. Similarly, mining corporations depend on heavy duty engines for their haul trucks, drilling equipment, and other specialized mining vehicles, where engine reliability under extreme conditions is paramount to operational continuity.

Agricultural businesses, from large-scale farming enterprises to smaller family farms, rely on heavy duty engines for tractors, combines, and irrigation systems to maximize productivity and efficiency in crop cultivation and livestock management. Furthermore, marine vessel owners, including commercial shipping companies, fishing fleets, and offshore support vessel operators, require engines for propulsion and auxiliary power in demanding maritime environments. Power generation utilities and various industrial facilities also serve as crucial customers, utilizing heavy duty engines for prime power, standby generators, and other industrial applications where uninterrupted and substantial power supply is critical for their operations. Each of these customer groups exhibits unique purchasing behaviors and operational requirements, which heavy duty engine manufacturers must address effectively.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 188.5 Billion |

| Market Forecast in 2032 | USD 260.9 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cummins Inc., Caterpillar Inc., Volvo Group, Daimler Truck AG, Scania AB, MAN SE, John Deere, Isuzu Motors Ltd., Deutz AG, Yanmar Holdings Co., Ltd., FPT Industrial S.p.A., Kubota Corporation, Doosan Infracore, Perkins Engines Company Limited, Mitsubishi Heavy Industries, Ltd., Hyundai Heavy Industries Co., Ltd., Weichai Power Co., Ltd., Power Solutions International (PSI), Rolls-Royce Holdings plc (Power Systems), Hino Motors, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Heavy Duty Engine market is characterized by a dynamic and evolving technology landscape, driven by the dual imperatives of enhanced performance and environmental sustainability. Traditional internal combustion engines have seen significant advancements, incorporating sophisticated fuel injection systems like common rail technology, which precisely controls fuel delivery for optimal combustion and reduced emissions. Advanced turbocharging and supercharging systems are now standard, improving power density and fuel efficiency by forcing more air into the engine. Exhaust gas recirculation (EGR) and selective catalytic reduction (SCR) systems are crucial aftertreatment technologies that significantly reduce nitrogen oxides (NOx) and particulate matter, ensuring compliance with stringent global emission regulations such as EPA Tier standards and Euro norms.

Beyond traditional combustion improvements, the market is rapidly integrating digital and smart technologies. Engine Control Units (ECUs) have become highly sophisticated, leveraging advanced algorithms to manage engine operations in real-time, optimizing everything from fuel consumption to power output. Telematics and IoT integration enable remote monitoring, predictive diagnostics, and data analytics, allowing operators to track engine performance, predict maintenance needs, and manage fleets more efficiently. These technologies provide valuable insights into engine health and operational patterns, thereby minimizing downtime and extending the lifespan of critical components. The development of advanced materials, offering greater strength-to-weight ratios and improved heat resistance, further contributes to engine durability and performance while potentially reducing overall engine weight.

Looking ahead, the technological landscape is increasingly dominated by alternative powertrain solutions. Hybrid electric powertrains, combining internal combustion engines with electric motors and battery packs, offer improved fuel economy and reduced emissions, especially in stop-and-go applications. Full electric heavy duty engines are gaining traction, driven by advancements in battery technology, charging infrastructure, and zero-emission mandates, particularly for urban delivery and short-haul operations. Furthermore, research and development into hydrogen combustion engines and hydrogen fuel cell electric powertrains represent a significant frontier, aiming to provide zero-emission solutions with long-range capabilities, positioning these technologies as critical future developments in the heavy duty engine market. This continuous innovation across fuel types, control systems, and material science defines the cutting-edge of heavy duty engine technology.

The heavy-duty engine market is primarily driven by global infrastructure development, the expansion of the e-commerce sector increasing demand for commercial vehicles, and stringent emission regulations pushing for technological advancements. Additionally, continuous innovation in fuel efficiency and power density also acts as a significant market driver.

Emission regulations are profoundly impacting heavy-duty engine design by necessitating advanced technologies such as selective catalytic reduction (SCR), exhaust gas recirculation (EGR), and diesel particulate filters (DPF). These regulations encourage the development of cleaner combustion systems, alternative fuel compatibility, and a shift towards hybrid and electric powertrains to reduce pollutants.

Alternative fuels like natural gas, hydrogen, and biofuels are playing an increasingly important role in the heavy-duty engine market by offering pathways to reduce carbon emissions and operational costs. While diesel remains dominant, a growing focus on sustainability and energy security is driving the adoption and development of engines capable of running on these cleaner alternatives.

Digitalization is transforming heavy-duty engines through the integration of advanced electronics, IoT connectivity, and artificial intelligence. This enables features such as real-time performance monitoring, predictive maintenance, remote diagnostics, and optimized fuel management, leading to improved operational efficiency, reduced downtime, and enhanced fleet management capabilities.

The Asia Pacific region, particularly countries like China and India, is exhibiting the most significant growth in the heavy-duty engine market due to rapid industrialization, extensive infrastructure projects, and increasing demand across commercial and construction sectors. North America and Europe also show steady growth, driven by technological advancements and stringent environmental compliance.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.