ID : MRU_ 430850 | Date : Nov, 2025 | Pages : 242 | Region : Global | Publisher : MRU

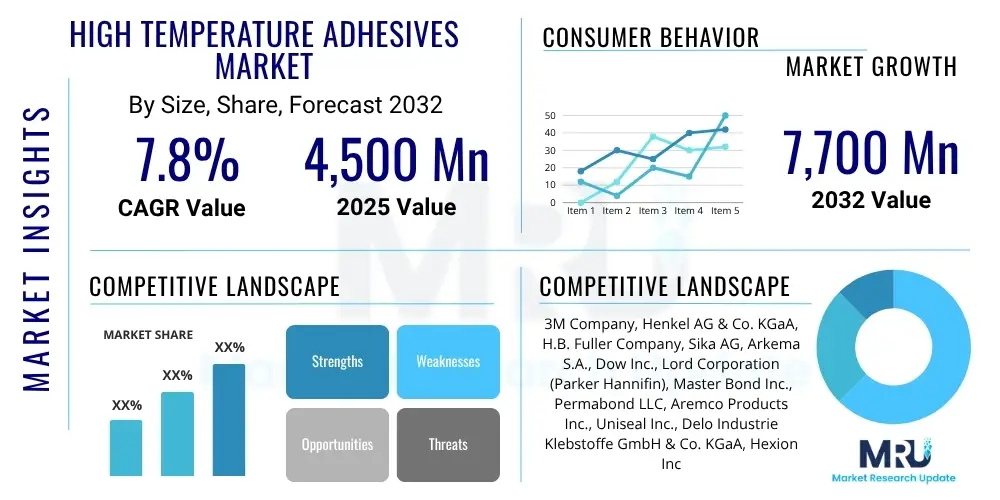

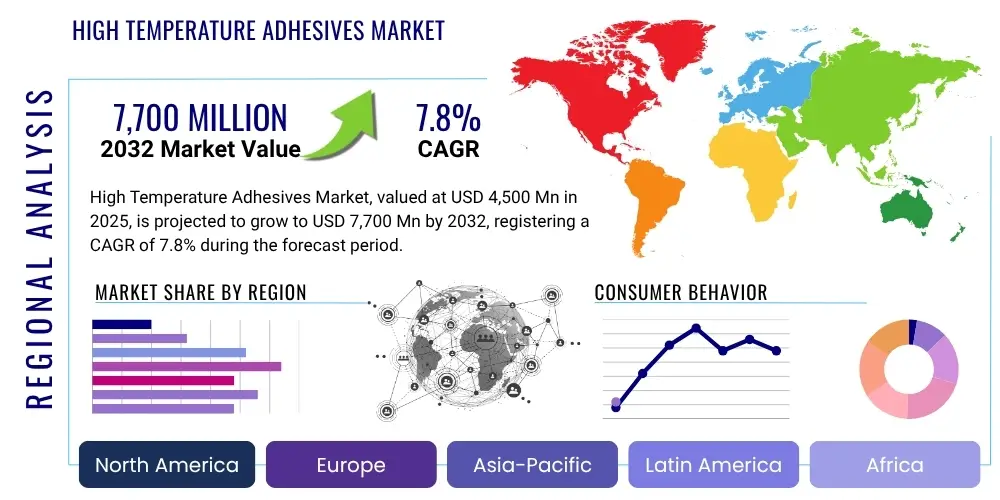

The High Temperature Adhesives Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at $4,500 Million in 2025 and is projected to reach $7,700 Million by the end of the forecast period in 2032.

The High Temperature Adhesives Market encompasses specialized bonding agents designed to maintain structural integrity and performance under extreme thermal conditions, typically exceeding 150°C. These advanced materials are crucial for applications where conventional adhesives would fail, offering superior thermal stability, chemical resistance, and mechanical strength. Key product types include epoxies, silicones, polyimides, ceramics, and phenolics, each formulated to meet specific operational requirements across diverse industries. The primary benefits of these adhesives include enhanced durability, reduced weight through material substitution, improved safety in critical components, and extended product lifecycles in harsh environments.

Major applications for high temperature adhesives span critical sectors such as automotive, aerospace and defense, electronics, and various industrial manufacturing processes. In automotive, they are used in engine compartments, exhaust systems, and brake components. The aerospace industry relies on them for structural bonding in aircraft, spacecraft, and missiles, where high strength-to-weight ratios are paramount. Electronics benefit from their use in semiconductor packaging, circuit board assembly, and heat sinks, ensuring reliability of devices operating at elevated temperatures. Industrial applications range from furnace linings to power generation equipment, demanding robust solutions for extreme heat and corrosive conditions.

The market's growth is predominantly driven by the increasing demand for high-performance materials in these end-use industries, coupled with a global push for lightweight and fuel-efficient designs. Rapid industrialization, particularly in emerging economies, and the continuous technological advancements in product development further fuel market expansion. Additionally, the rising complexity and miniaturization of electronic devices necessitate advanced bonding solutions capable of withstanding operational heat. Stricter regulatory standards regarding safety and emissions in sectors like automotive and aerospace also compel manufacturers to adopt more durable and temperature-resistant adhesive technologies.

The High Temperature Adhesives Market is characterized by robust growth, driven by escalating demand from critical end-use industries and continuous innovation in material science. Business trends indicate a strong focus on research and development to create advanced formulations that offer enhanced performance, sustainability, and ease of application. Companies are increasingly investing in expanding their product portfolios to cater to niche applications, and strategic collaborations, mergers, and acquisitions are common as firms seek to consolidate market share and leverage specialized expertise. There is a notable shift towards developing eco-friendly and solvent-free high temperature adhesive solutions in response to environmental regulations and consumer preferences, alongside advancements in automation for adhesive application.

Regionally, Asia Pacific is poised to exhibit the fastest growth, largely due to its burgeoning manufacturing sector, particularly in automotive, electronics, and industrial machinery, coupled with significant investments in infrastructure development. North America and Europe, while mature markets, continue to demonstrate steady demand, driven by stringent performance standards in aerospace and defense, and the ongoing modernization of industrial infrastructure. These regions also lead in technological innovation and the adoption of advanced adhesive systems. Latin America and the Middle East & Africa are emerging markets, showing potential with increasing industrialization and investments in oil & gas, automotive, and construction sectors, fostering a gradual yet consistent uptake of high temperature adhesives.

Segmentation trends highlight the dominance of epoxy-based adhesives due to their versatility and excellent mechanical properties, though silicone-based adhesives are experiencing significant growth, particularly in automotive electronics and medical applications, owing to their flexibility and wide temperature range. The aerospace and defense industry remains a critical segment, demanding custom formulations for extreme operating conditions. However, the automotive sector, driven by the shift towards electric vehicles (EVs) and lightweighting initiatives, is rapidly expanding its consumption of high temperature adhesives for battery components, structural bonding, and powertrain applications. The electronics industry's relentless pursuit of miniaturization and higher power density also ensures sustained demand for specialized encapsulants and bonding agents that can dissipate heat efficiently and maintain electrical insulation.

Users frequently inquire about how Artificial Intelligence (AI) can revolutionize the High Temperature Adhesives Market, with primary themes centering on optimizing material discovery, enhancing manufacturing processes, improving quality control, and streamlining supply chains. There is keen interest in AI's potential to accelerate the development of novel adhesive formulations with superior thermal resistance and bonding capabilities, reducing the traditional trial-and-error approach in R&D. Concerns also arise regarding the practical implementation costs, data privacy, and the need for specialized AI expertise within the chemicals industry. Expectations are high for AI to lead to more sustainable and cost-effective adhesive solutions, addressing both performance and environmental challenges through predictive modeling and advanced analytics.

The High Temperature Adhesives Market is propelled by several robust drivers, including the increasing global demand for lightweight and fuel-efficient materials across the automotive and aerospace sectors. The relentless miniaturization and enhanced performance requirements within the electronics industry, particularly for devices operating under high thermal loads, further stimulate market growth. Furthermore, the expansion of industrial manufacturing, renewable energy infrastructure, and advancements in additive manufacturing necessitate adhesives capable of withstanding extreme conditions, thus creating a fertile ground for market expansion. The continuous innovation in material science also introduces new adhesive chemistries with superior properties, broadening their application scope and accelerating adoption.

However, the market also faces significant restraints. The high research and development costs associated with developing new high temperature adhesive formulations, particularly those meeting stringent performance and safety standards, can be a barrier to entry for smaller players. Additionally, the volatility in raw material prices, such as specialized resins and fillers, directly impacts production costs and profit margins. Stringent regulatory approvals and environmental compliance, especially for adhesives used in critical applications like aerospace and healthcare, add complexity and time to market. The technical challenges associated with processing and applying certain high-temperature formulations also limit their widespread adoption, requiring specialized equipment and skilled labor.

Opportunities for growth are abundant within the market, particularly with the global shift towards electric vehicles (EVs) and battery technologies, which require specialized high temperature adhesives for battery pack assembly, thermal management, and structural bonding. The advancements in additive manufacturing (3D printing) also present new avenues for customized adhesive solutions capable of bonding complex geometries and diverse materials at elevated temperatures. The increasing focus on sustainability and green chemistry is fostering the development of bio-based and solvent-free high temperature adhesives, opening new market segments. Moreover, expanding applications in extreme environments such as deep-sea exploration, space technology, and high-performance industrial machinery continue to drive innovation and demand for more robust adhesive solutions. These drivers, restraints, and opportunities collectively shape the market's trajectory, influenced by underlying impact forces that dictate the pace and direction of technological evolution and market dynamics.

The High Temperature Adhesives Market is extensively segmented to reflect the diverse applications and product types within the industry. This segmentation helps in understanding the specific demands and growth drivers across various sectors and material categories. Key segments include classifications by resin type, end-use industry, and application, each revealing distinct market dynamics and competitive landscapes. Analyzing these segments provides a comprehensive view of market trends, allowing stakeholders to identify high-growth areas and tailor product development strategies to specific market needs. The intricate interplay between material properties, performance requirements, and industrial applications defines the structure of this specialized market.

The value chain for the High Temperature Adhesives Market begins with the upstream segment, which primarily involves the sourcing and production of raw materials. This includes specialty chemicals like various types of resins (epoxy, silicone, polyimide, acrylic), hardeners, catalysts, fillers (e.g., ceramic particles, metal oxides), and performance additives. Key players in this stage are chemical manufacturers who supply these raw ingredients to adhesive formulators. The quality, consistency, and availability of these upstream materials significantly influence the final performance and cost of high temperature adhesives. Innovation in raw material synthesis, focusing on sustainability and enhanced properties, is critical at this stage.

Moving downstream, the value chain encompasses the adhesive manufacturers who formulate these raw materials into finished high temperature adhesive products. This stage involves complex research and development, blending, and compounding processes to create adhesives with specific thermal resistance, mechanical strength, and application characteristics. After manufacturing, these adhesives are distributed to end-users through various channels. Direct distribution involves sales teams engaging directly with large industrial customers, such as automotive OEMs or aerospace manufacturers, often providing technical support and customized solutions. Indirect distribution channels include a network of third-party distributors, wholesalers, and retailers who make products accessible to a broader range of smaller and medium-sized enterprises (SMEs) across diverse geographical locations.

The choice between direct and indirect distribution often depends on the scale of the customer, the complexity of the product, and the geographic reach desired. Direct channels allow for greater control over customer relationships and technical service, which is crucial for highly specialized high temperature applications. Indirect channels offer wider market penetration and logistical efficiency for standardized products. The end-users, forming the final link in the value chain, apply these adhesives in their manufacturing processes across industries like automotive, aerospace, electronics, and industrial sectors. Their feedback drives innovation and product improvement throughout the entire value chain, emphasizing the importance of a well-integrated and responsive supply network to meet evolving market demands effectively.

The primary potential customers for high temperature adhesives are diverse industrial entities that require robust bonding solutions capable of withstanding extreme heat and harsh operating conditions. This includes Original Equipment Manufacturers (OEMs) in the automotive sector, where these adhesives are critical for engine components, exhaust systems, brake assemblies, and increasingly, in battery packs and power electronics for electric vehicles. The demand is driven by the need for lightweight materials, enhanced durability, and improved safety standards in modern vehicle designs. Manufacturers of internal combustion engines and electric powertrains are constantly seeking advanced adhesive solutions to manage thermal stress and ensure long-term reliability of components operating at elevated temperatures.

Another significant customer segment comprises aerospace and defense manufacturers. These industries utilize high temperature adhesives for structural bonding in aircraft, spacecraft, missiles, and drones, where performance at high altitudes and varying temperatures is non-negotiable. Applications include bonding composite structures, attaching heat shields, securing electrical components, and sealing fuel tanks, requiring adhesives with exceptional strength-to-weight ratios and thermal stability. The stringent safety regulations and the mission-critical nature of aerospace applications necessitate the highest quality and most reliable high temperature adhesive solutions, making these customers a premium segment within the market.

Furthermore, the electronics industry, encompassing manufacturers of semiconductors, circuit boards, and electronic devices, represents a rapidly growing customer base. As electronic components become smaller and more powerful, generating significant heat, high temperature adhesives are essential for die attach, encapsulation, thermal management, and structural bonding to prevent thermal degradation and ensure device longevity. Industrial machinery and equipment manufacturers also constitute a substantial customer segment, using these adhesives in applications like furnace construction, power generation equipment, industrial ovens, and HVAC systems. The construction sector, particularly for high-performance facades and specialized infrastructure, and the healthcare industry for certain sterilization-resistant medical devices, further expand the potential customer landscape for advanced high temperature adhesives, each demanding specific characteristics tailored to their operational environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $4,500 Million |

| Market Forecast in 2032 | $7,700 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema S.A., Dow Inc., Lord Corporation (Parker Hannifin), Master Bond Inc., Permabond LLC, Aremco Products Inc., Uniseal Inc., Delo Industrie Klebstoffe GmbH & Co. KGaA, Hexion Inc., Parson Adhesives Inc., Saint-Gobain S.A., Ashland Global Holdings Inc., DIC Corporation, Franklin International, ITW Performance Polymers, Momentive Performance Materials Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Temperature Adhesives Market is continually evolving, driven by advancements in material science and engineering, leading to a sophisticated technological landscape. A critical area of development involves the synthesis of advanced polymer chemistries, such as specialized polyimides, polybenzimidazoles (PBIs), and silicone-epoxy hybrids, designed to offer superior thermal oxidative stability, mechanical strength at elevated temperatures, and chemical resistance. Nanotechnology plays a pivotal role, with the incorporation of nanoparticles (e.g., silica, alumina, carbon nanotubes) into adhesive formulations to enhance thermal conductivity, mechanical properties, and barrier performance without compromising high-temperature integrity. These innovations enable the creation of adhesives that can operate reliably under even more extreme thermal cycling and aggressive chemical exposures, crucial for demanding applications.

Another significant technological advancement is in the processing and curing mechanisms of these adhesives. UV-curing and dual-cure systems are gaining traction for applications requiring rapid processing and improved efficiency, particularly in electronics manufacturing and assembly lines. Reactive hot melts, which combine the benefits of hot melt application with subsequent chemical curing, offer excellent green strength and high ultimate performance, including temperature resistance. Sol-gel processes are also being explored to create inorganic-organic hybrid adhesives that exhibit exceptional thermal stability and strong adhesion to various substrates, often at lower processing temperatures compared to traditional ceramic adhesives. These processing innovations address the challenges of integrating high-performance adhesives into automated and high-volume production environments, enhancing both efficiency and reliability.

Furthermore, advancements in simulation and modeling software are transforming the design and testing phases of high temperature adhesives. Computational fluid dynamics (CFD) and finite element analysis (FEA) allow for predictive analysis of adhesive behavior under thermal stress, mechanical loads, and chemical exposure, significantly reducing the need for extensive physical prototyping and testing. This digital approach accelerates product development cycles and optimizes material selection. The integration of smart adhesive technologies, featuring self-healing properties or integrated sensors for performance monitoring, represents a future frontier. These technological strides are collectively pushing the boundaries of what high temperature adhesives can achieve, enabling new applications and driving market expansion across various industries requiring robust thermal performance.

High temperature adhesives are specialized bonding agents designed to maintain structural integrity, adhesion, and performance when exposed to extreme heat, typically exceeding 150°C, and often under various environmental stresses. They are formulated to prevent degradation and delamination at elevated temperatures.

High temperature adhesives are critically utilized in the automotive sector for engine parts and exhaust systems, in aerospace for structural bonding and heat shields, in electronics for semiconductor packaging and thermal management, and across industrial applications like furnaces and power generation equipment.

The primary industries driving demand for high temperature adhesives include automotive (especially for lightweighting and electric vehicles), aerospace and defense (for high-performance aircraft and spacecraft), and electronics (for miniaturized and high-power devices that generate significant heat).

Key types of high temperature adhesives include epoxy-based, silicone-based, polyimide-based, ceramic-based, and acrylic-based formulations. Each type offers distinct advantages in terms of temperature range, flexibility, strength, and chemical resistance, catering to specific application requirements.

Future trends in the high temperature adhesives market include a growing focus on sustainable and bio-based formulations, increasing adoption in electric vehicle battery technology, advancements in nanotechnology for enhanced properties, and the integration of AI for accelerated material discovery and process optimization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.