ID : MRU_ 429529 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

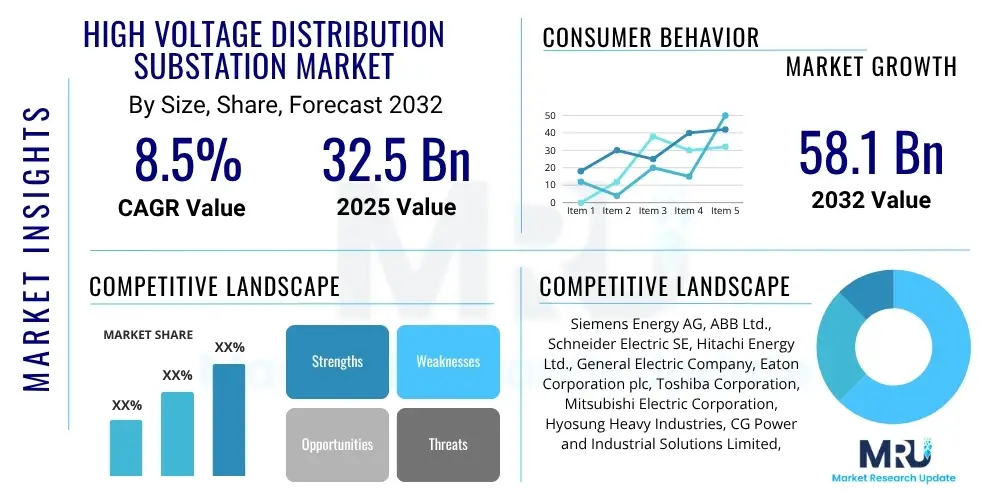

The High Voltage Distribution Substation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at $32.5 Billion in 2025 and is projected to reach $58.1 Billion by the end of the forecast period in 2032.

High Voltage Distribution Substation Market products are indispensable elements within modern electrical grids, serving as critical intermediaries in the power delivery infrastructure. These complex installations are engineered to efficiently step down high-voltage electricity, typically received from transmission lines, to lower voltages suitable for safe and effective distribution to end-users. A typical substation comprises a sophisticated array of components including power transformers for voltage conversion, switchgear for circuit protection and control, circuit breakers for fault isolation, and comprehensive control and monitoring systems that ensure stable and reliable operation, making them fundamental for energy security and economic functionality.

The primary applications of high voltage distribution substations span across a wide spectrum of energy consumers, from large-scale industrial complexes and sprawling commercial centers to residential neighborhoods and critical public services. Their fundamental role involves ensuring power quality, managing grid stability, and protecting the network from overloads and short circuits. The essential benefits derived from these substations include enhanced power grid reliability, substantial reduction in transmission and distribution losses, and improved overall efficiency of electricity delivery, which are crucial for meeting consistent demand and fostering economic growth across various sectors requiring uninterrupted power supply.

The market for high voltage distribution substations is currently being propelled by several powerful driving factors. Chief among these are the accelerating global electrification initiatives aimed at providing access to reliable electricity in underserved regions, coupled with the relentlessly increasing energy demand driven by industrial expansion, rapid urbanization, and the widespread adoption of electric vehicles and smart home technologies across developing economies. Furthermore, significant governmental and private sector investments in the modernization and expansion of aging grid infrastructure, along with the imperative to integrate burgeoning renewable energy sources into the national power grids, are creating substantial and sustained demand for new and upgraded substation technologies capable of handling dynamic power flows.

The High Voltage Distribution Substation Market is poised for substantial expansion, underpinned by a confluence of evolving business strategies, dynamic regional growth patterns, and distinct segment-specific trends that are reshaping the global energy landscape. Business trends highlight a significant industry shift towards the adoption of more compact, modular, and environmentally sustainable substation designs, which are particularly desirable in urban areas where space is at a premium and environmental regulations are increasingly stringent. There is also a pronounced emphasis on incorporating advanced automation, digitalization, and predictive analytics into substation operations, aiming to boost operational efficiency, minimize human intervention, and significantly reduce long-term maintenance expenditures through data-driven insights.

Regional trends reveal a diverse yet robust market landscape with varying growth catalysts. The Asia Pacific region is unequivocally at the forefront of market growth, primarily fueled by extensive and ongoing investments in power infrastructure development across populous and rapidly industrializing nations such as China, India, and various Southeast Asian countries, driven by escalating energy demand and vast rural electrification programs. In contrast, mature markets like North America and Europe are primarily focused on the critical tasks of replacing their aging grid assets, modernizing existing infrastructure, and integrating smart grid technologies to enhance resilience, accommodate increasing renewable energy penetration, and comply with strict emission reduction targets. Latin America and the Middle East and Africa regions are also exhibiting strong growth due to increasing electrification and industrial development initiatives, supported by investments in new energy projects.

From a segmentation perspective, several key trends are shaping the market's trajectory and influencing investment patterns. The Gas Insulated Switchgear (GIS) technology segment is witnessing particularly strong growth, driven by its inherent advantages of compact design, enhanced safety, reduced environmental footprint, and minimal maintenance requirements, making it an ideal solution for urban installations and critical infrastructure. Furthermore, the utility-scale application segment continues to dominate, given the foundational role of substations in national power grids for bulk power transmission and distribution. There is also an observable trend towards hybrid substation configurations, which cleverly combine the benefits of both Air Insulated Switchgear (AIS) and GIS technologies to offer flexible, cost-effective, and optimized solutions for diverse site conditions and operational requirements, balancing space efficiency with traditional reliability.

Common user questions regarding the impact of Artificial Intelligence (AI) on the High Voltage Distribution Substation Market frequently center on how these advanced technologies can revolutionize operational efficiency, enhance predictive maintenance capabilities, and fortify the cybersecurity posture of critical grid infrastructure. Users are keenly interested in understanding AI's transformative potential in optimizing complex power flows, enabling real-time fault detection and isolation, and intelligently managing the increasing integration of intermittent renewable energy sources into the grid. The expectations are high for AI to provide unprecedented levels of grid resilience, adaptability, and responsiveness to dynamic energy demands, thereby creating a more robust and future-proof power delivery system.

Furthermore, stakeholder concerns often revolve around practical implementation challenges associated with AI adoption in critical infrastructure. These include the imperative for robust data security protocols to protect sensitive operational data from cyber threats, ensuring the reliability, explainability, and transparency of AI algorithms in mission-critical applications where failure is not an option, and addressing the significant need for upskilling and reskilling the existing workforce to effectively deploy, manage, and maintain AI-powered substation systems. Despite these challenges, there is a prevailing consensus that AI will be instrumental in drastically improving the uptime of assets, reducing operational expenditures through optimized maintenance cycles, and enhancing the overall economic viability and environmental sustainability of electricity distribution networks worldwide by minimizing losses and improving resource allocation.

The High Voltage Distribution Substation Market is primarily driven by a surging global demand for electricity, which is an inevitable consequence of rapid industrialization, burgeoning urbanization, and the widespread adoption of electric vehicles and other electrified technologies across various sectors. Complementing this demand is a substantial wave of investments from both public and private sectors aimed at modernizing and expanding existing grid infrastructure, especially in rapidly developing economies where new power generation capacity requires robust distribution networks capable of handling increased loads. The critical imperative to integrate a growing portfolio of renewable energy sources, such as large-scale solar and wind farms, into the national grids also necessitates significant upgrades and new installations of high voltage substations to handle intermittent power flows efficiently, reliably, and with enhanced stability.

Despite these powerful tailwinds, the market faces notable restraints that can impede its growth trajectory. The exceptionally high capital expenditure required for designing, procuring, and constructing new high voltage substation projects presents a significant barrier to entry and expansion, particularly for smaller utility companies or in regions with limited financial resources. Furthermore, navigating complex and often protracted regulatory approval processes, coupled with the inherent challenges of acquiring suitable land, particularly in densely populated urban or environmentally sensitive areas, can substantially delay projects, inflate overall costs, and lead to public opposition. The need for highly specialized technical expertise for both complex construction and ongoing sophisticated maintenance also adds to operational complexities and cost burdens.

Opportunities within this dynamic market are abundant, primarily stemming from continuous technological advancements that promise greater efficiency and sustainability. The ongoing shift towards smart grid integration, which leverages digital communication and control technologies for enhanced grid management and automation, presents a vast area for growth. The increasing digitalization of substation components, leading to "digital substations" with fiber optics and intelligent electronic devices (IEDs), offers improved real-time monitoring, precise control, and advanced data analytics capabilities. Additionally, the development and adoption of compact, modular, and environmentally friendly substations, including those utilizing eco-friendly insulation gases to replace SF6, are creating new market niches by addressing space constraints and environmental concerns, thereby opening new avenues for innovation, market penetration, and sustainable grid development. These impact forces collectively underscore a market experiencing robust essential demand, tempered by significant investment hurdles, yet strongly propelled by technological evolution.

The High Voltage Distribution Substation Market is extensively segmented to provide a comprehensive and granular understanding of its diverse operational landscape, revealing distinct growth drivers and competitive dynamics within each category. This intricate market structure allows stakeholders to identify specific areas of demand, technological preferences, and regional concentrations, thereby informing strategic investment decisions, targeted product development, and effective market penetration strategies. The various segmentation criteria reflect the multifaceted nature of electricity distribution infrastructure, from the highly technical specifications of voltage and insulation to the practical considerations of end-user applications and the overall operational scale, providing a holistic view of market dynamics.

Understanding these granular segments is crucial for market participants, as it highlights how different types of substations and their components cater to unique requirements across the power sector. For instance, the choice of voltage level significantly impacts the complexity of design and the specific equipment specifications, directly influencing the technological sophistication and cost of a substation. Similarly, the insulation type deployed determines not only the physical footprint of the installation but also its environmental characteristics and safety profile. Distinguishing between end-users such as utilities, industrial complexes, or railways, underscores the varied operational demands, regulatory environments, and procurement processes that influence purchasing patterns and adoption rates, offering clear insights into where market growth is concentrated and what specific technological attributes are most valued by particular customer groups, allowing for tailored solutions and strategic positioning.

The value chain for the High Voltage Distribution Substation Market is a complex and highly integrated ecosystem that commences with a robust upstream segment, primarily focused on the sourcing and manufacturing of critical raw materials and highly specialized components. This initial stage involves a diverse array of suppliers providing high-grade steel for structural elements, refined copper and aluminum for conductors, and advanced polymeric and ceramic insulation materials crucial for safe and efficient operation. Additionally, specialized manufacturers producing intricate components like high-voltage bushings, surge arresters, on-load tap changers, and advanced circuit breaker mechanisms form a vital part of this foundational phase, providing the essential building blocks that ensure the long-term performance and durability of substation equipment.

The midstream segment of the value chain is dominated by Original Equipment Manufacturers (OEMs) and specialized engineering firms that undertake the intricate processes of design, engineering, manufacturing, assembly, and rigorous factory acceptance testing of complete substation systems. This phase involves sophisticated technical expertise to integrate diverse components into a cohesive and operational unit, ensuring compliance with stringent international standards, local regulations, and specific project requirements. Engineering, Procurement, and Construction (EPC) contractors often play a pivotal role here, managing the entire project lifecycle from initial concept to final commissioning, coordinating multiple suppliers, mitigating risks, and ensuring seamless execution within defined timelines and budgets, thereby transforming blueprints into functional infrastructure.

Downstream activities encompass the critical stages of installation, precise commissioning, long-term operation, and ongoing maintenance of high voltage distribution substations throughout their extensive service life. This segment primarily involves large utility companies, significant industrial enterprises, independent power producers, and specialized service providers who ensure the continuous, reliable, and efficient functioning of these vital assets. Distribution channels are predominantly direct, characterized by close and often long-term collaboration between OEMs, EPC contractors, and end-users, typically facilitated through competitive bidding processes for large-scale infrastructure projects. However, indirect channels involving local distributors or authorized agents may be strategically utilized for supplying spare parts, smaller ancillary components, or providing regionalized support and routine maintenance services, thereby extending market reach and enhancing responsiveness to localized operational needs.

The primary potential customers and key buyers within the High Voltage Distribution Substation Market represent a diverse yet interconnected group of organizations, all united by their fundamental and increasing need for robust, reliable, and efficient electrical infrastructure to support their operations. Utility companies, encompassing national grid operators, regional power distributors, and municipal electricity providers, collectively constitute the largest and most significant customer segment. These entities are directly responsible for the generation, transmission, and distribution of electricity to a broad consumer base, necessitating continuous investment in new substations to meet growing demand and the critical modernization or replacement of existing ones to enhance grid resilience, reduce losses, and integrate new technologies.

Beyond traditional utilities, the industrial sector stands as a substantial and expanding end-user base for high voltage distribution substations. Large-scale manufacturing plants, heavy industries such as metallurgy, chemical production, and mining operations, along with burgeoning data centers, require dedicated, high-capacity power supplies with stringent reliability and power quality standards to prevent costly production interruptions. These industrial facilities often invest in their own high voltage distribution substations to ensure stable power delivery, protect sensitive equipment from voltage fluctuations, and effectively manage their substantial energy consumption, frequently integrating with the main grid at high voltage levels for direct supply and control.

Furthermore, the market's customer base extends significantly to the commercial sector and vital public infrastructure projects. Major commercial complexes, expansive business parks, large institutional campuses, airports, and modern healthcare facilities demand robust power infrastructure capable of sustaining continuous operations and accommodating high energy loads. Additionally, the rapidly expanding global railway networks, particularly electrified metropolitan and intercity lines, are significant buyers of specialized traction substations that convert and supply appropriate power to overhead lines or third rails for railway operations. These diverse end-users collectively drive substantial demand for the design, construction, installation, and ongoing maintenance of high voltage distribution substations, highlighting the market's broad applicability across critical economic and social domains globally.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $32.5 Billion |

| Market Forecast in 2032 | $58.1 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Energy AG, ABB Ltd., Schneider Electric SE, Hitachi Energy Ltd., General Electric Company, Eaton Corporation plc, Toshiba Corporation, Mitsubishi Electric Corporation, Hyosung Heavy Industries, CG Power and Industrial Solutions Limited, KEC International Ltd., TBEA Co. Ltd., Shandong Electrical Engineering & Equipment Group Co. Ltd., Bharat Heavy Electricals Limited (BHEL), LS Electric Co. Ltd., Arteche Group, Xylem Inc., Fuji Electric Co. Ltd., EMCO Limited, MEIDENSHA Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Voltage Distribution Substation Market is undergoing a profound technological transformation, driven by the dual imperatives of enhancing grid efficiency, ensuring long-term reliability, and achieving sustainable operations. A cornerstone of this ongoing evolution is the increasing adoption of Gas Insulated Switchgear (GIS) and Hybrid Switchgear, which offer significant advantages over traditional Air Insulated Switchgear (AIS). GIS technology, in particular, allows for ultra-compact substation designs, reducing the physical footprint by up to 90% compared to AIS, making it an ideal solution for deployment in urban environments and areas with limited space constraints where traditional expansion is not feasible. Furthermore, the sealed environment of GIS enhances operational safety, significantly reduces maintenance requirements, and protects internal components from environmental contaminants, contributing to an extended equipment lifespan and superior performance.

The advent and accelerating implementation of digital substations represent another pivotal advancement, fundamentally transforming how substations are operated and managed. This paradigm shift leverages fiber optic communication networks and intelligent electronic devices (IEDs) to replace cumbersome traditional copper wiring for control and protection functionalities. This comprehensive digitalization enables real-time data exchange, advanced remote monitoring, and sophisticated automation capabilities, drastically improving operational visibility, responsiveness, and control. Digital substations facilitate precise fault location, rapid isolation of affected sections, and quicker restoration times, all of which are crucial for maintaining grid stability, minimizing power outages, and enhancing overall grid resilience. The ability to collect and analyze vast amounts of operational data also robustly supports predictive maintenance strategies, optimizes asset utilization, and informs strategic infrastructure planning.

Further innovations are concentrated on smart grid integration, enhanced cybersecurity measures, and critical environmental sustainability initiatives. The deployment of advanced sensors, high-speed communication infrastructure, and sophisticated substation automation systems (SAS) is crucial for efficiently integrating increasingly intermittent renewable energy sources into the grid and enabling dynamic demand-side management programs. Additionally, the industry is actively pursuing viable alternatives to sulfur hexafluoride (SF6) gas, a potent greenhouse gas traditionally used in GIS, by vigorously developing and deploying eco-friendly insulation gases such as g3 gas and various mixtures of nitrogen and carbon dioxide. These concerted technological shifts are collectively moving the market towards the establishment of more resilient, efficient, secure, and ecologically responsible power distribution networks, thereby ensuring robust grid reliability for the complex energy landscapes of the future.

A high voltage distribution substation is a critical node in an electrical grid that efficiently converts high-voltage electricity from transmission lines to a lower voltage suitable for distribution to local consumers, including homes, businesses, and industries. Its core functions are to ensure reliable power supply, manage voltage levels, control power flow, and protect the grid from faults and overloads, thereby maintaining grid stability and safety.

The market's substantial growth is primarily driven by the increasing global electricity demand stemming from rapid industrialization and urbanization, massive ongoing investments in grid modernization and expansion projects worldwide, and the critical imperative to integrate a growing share of intermittent renewable energy sources into existing power networks. Additionally, the electrification of transportation and industries also contributes significantly.

Technological advancements, especially in Artificial Intelligence (AI) and digitalization, are profoundly transforming substation operations. They significantly enhance efficiency through predictive maintenance, optimize real-time grid management, strengthen cybersecurity defenses, and automate fault detection and isolation processes. These innovations lead to greater operational reliability, reduced downtime, lower maintenance costs, and improved integration of complex power sources.

The Asia Pacific region, particularly rapidly developing economies like China, India, and various Southeast Asian countries, is anticipated to show the most substantial market growth. This is due to extensive infrastructure development, rapid urbanization, and ambitious electrification initiatives. North America and Europe also contribute significantly, driven by grid modernization, asset replacement cycles, and large-scale renewable energy integration projects.

Modern high voltage distribution substations predominantly employ three main types of insulation technologies: Air Insulated Substations (AIS), which are traditional, cost-effective, but require larger land footprints; Gas Insulated Substations (GIS), known for their compact design, enhanced safety, and reduced environmental exposure; and Hybrid Substations, which strategically combine features of both AIS and GIS to offer optimized solutions balancing space, cost, and operational flexibility for diverse applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.