ID : MRU_ 430502 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

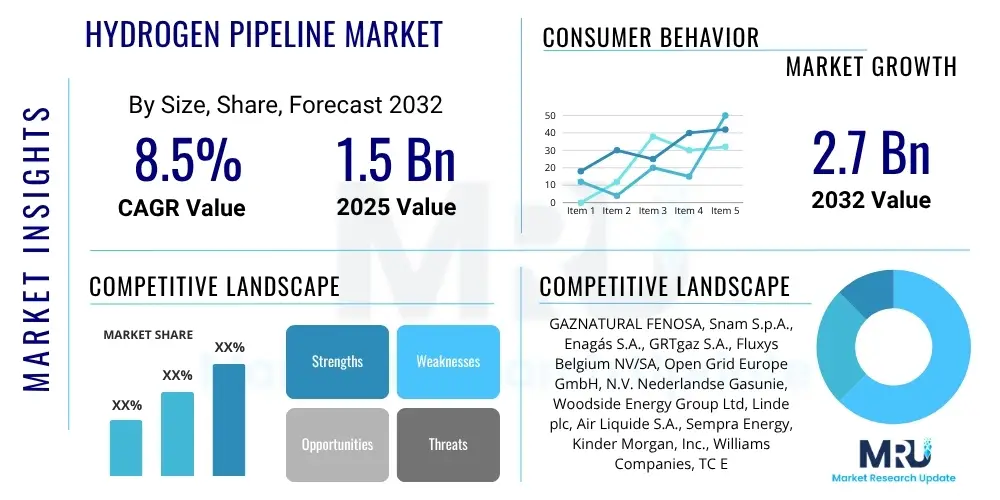

The Hydrogen Pipeline Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at $1.5 Billion in 2025 and is projected to reach $2.7 Billion by the end of the forecast period in 2032.

The Hydrogen Pipeline Market is emerging as a critical component of the global energy transition, facilitating the efficient and safe transportation of hydrogen from production sites to end-use applications. This infrastructure is vital for establishing a robust hydrogen economy, supporting decarbonization efforts across various sectors including industrial, transportation, and power generation. Hydrogen pipelines are specialized conduits designed to withstand the unique properties of hydrogen, such as its small molecular size and propensity for embrittlement in certain materials, ensuring secure delivery over long distances.

The core product in this market encompasses both newly constructed pipelines specifically engineered for hydrogen and the repurposing of existing natural gas pipeline infrastructure, which requires significant modifications and safety protocols. Major applications include supplying hydrogen as a feedstock for chemical processes like ammonia and methanol production, enabling fuel cell vehicles and hydrogen-powered transportation, and integrating hydrogen into power grids for energy storage or direct power generation. The inherent benefits of these pipelines extend to enabling large-scale hydrogen deployment, enhancing energy security, reducing carbon emissions by replacing fossil fuels, and fostering industrial growth through new supply chains.

Several key factors are driving the expansion of the hydrogen pipeline market. Global decarbonization targets and ambitious national hydrogen strategies are creating a strong policy-driven demand for hydrogen infrastructure. Significant government incentives and funding for green hydrogen production and infrastructure development are accelerating investment. Furthermore, advancements in materials science, compression technologies, and operational safety are making hydrogen pipeline construction and operation increasingly viable and cost-effective, thus reinforcing the market's growth trajectory.

The Hydrogen Pipeline Market is undergoing significant transformation, driven by global commitments to achieve net-zero emissions and the accelerating development of a hydrogen economy. Business trends indicate a surge in public and private investment into hydrogen infrastructure projects, with a strong focus on large-scale cross-border pipeline initiatives aimed at connecting hydrogen production hubs with major consumption centers. There is a growing trend towards the formation of consortia and partnerships between gas transmission system operators, energy companies, and industrial players to share risks and leverage expertise in developing integrated hydrogen networks. Furthermore, technological innovation in pipeline materials, monitoring systems, and compression technologies is enhancing the feasibility and safety of hydrogen transport.

Regionally, Europe is a frontrunner, supported by the European Hydrogen Strategy and initiatives like the European Hydrogen Backbone, which aims to repurpose and build thousands of kilometers of pipelines by 2030 and beyond. North America is also seeing robust growth, primarily fueled by the Inflation Reduction Act (IRA) in the United States, offering significant tax credits for clean hydrogen production, thereby spurring demand for associated transport infrastructure. Asia-Pacific, particularly Japan, South Korea, and Australia, is investing heavily in developing export-oriented hydrogen supply chains, necessitating extensive pipeline networks for domestic distribution and port connections. The Middle East and Africa are emerging as significant hydrogen production regions, planning extensive pipeline networks to facilitate export to energy-importing regions.

From a segmentation perspective, the market is primarily bifurcated into new hydrogen-dedicated pipelines and the repurposing of existing natural gas pipelines. The latter represents a cost-effective and faster deployment strategy, albeit with technical challenges related to material compatibility and operational adjustments. Demand for high-pressure pipelines is increasing to efficiently transport larger volumes of hydrogen, while application segments such as industrial feedstock and power generation are currently the dominant users, with the mobility sector expected to grow substantially. The overarching market trend emphasizes scalability, safety, and economic viability as paramount considerations for future development.

Common user questions regarding the impact of AI on the Hydrogen Pipeline Market frequently center on how artificial intelligence can enhance operational efficiency, ensure safety, and optimize the design and maintenance of these critical infrastructures. Users are keenly interested in AI's potential to address the unique challenges of hydrogen transport, such as leak detection, material degradation, and dynamic flow management. There are also queries about the role of AI in predictive maintenance, real-time monitoring, and integrating hydrogen pipelines into broader energy grids, alongside concerns about data security, system reliability, and the upfront investment required for AI implementation.

The Hydrogen Pipeline Market is propelled by significant drivers including global decarbonization mandates and government incentives aimed at reducing carbon emissions across industrial, transportation, and energy sectors. The increasing demand for clean energy and industrial feedstocks, coupled with growing geopolitical emphasis on energy independence and security, further strengthens the market. Supportive regulatory frameworks and substantial public-private investments in hydrogen infrastructure projects are instrumental in accelerating pipeline development. These factors collectively create a robust environment for market expansion, pushing for the rapid establishment of interconnected hydrogen networks to facilitate large-scale deployment.

However, the market faces notable restraints, primarily the high upfront capital expenditure required for building new, dedicated hydrogen pipelines or repurposing existing natural gas infrastructure. Safety concerns associated with hydrogen, such as its flammability and potential for embrittlement in pipeline materials, necessitate stringent safety protocols and advanced engineering, adding to complexity and cost. Technical challenges, including the need for high compression and ensuring gas purity during transport, pose additional hurdles. Public perception and the need for greater awareness regarding hydrogen’s safe handling and environmental benefits also present a barrier to widespread acceptance and project approval.

Despite these challenges, significant opportunities abound. The repurposing of existing natural gas pipelines offers a more cost-effective and time-efficient pathway to build out hydrogen networks, reducing the need for entirely new construction. The development of hydrogen production hubs, particularly for green hydrogen, necessitates extensive pipeline connectivity to reach diverse end-users, creating new investment avenues. Furthermore, cross-border projects like the European Hydrogen Backbone exemplify the potential for large-scale international collaboration and the establishment of interconnected energy grids. Impact forces such as evolving regulatory landscapes, geopolitical shifts affecting energy supply, and continuous technological advancements in materials and monitoring systems will continue to shape the market’s trajectory. The increasing focus on carbon capture and storage (CCS) and hydrogen blending with natural gas also provides near-term growth catalysts, influencing the scope and scale of pipeline projects.

The Hydrogen Pipeline Market is segmented based on several key characteristics that reflect the diverse aspects of its infrastructure, operational requirements, and end-use applications. This segmentation provides a structured view of the market, allowing for a detailed analysis of growth drivers, challenges, and opportunities within specific niches. Understanding these segments is crucial for stakeholders to tailor their strategies, optimize investments, and effectively contribute to the development of a global hydrogen economy.

The value chain for the Hydrogen Pipeline Market commences with upstream activities focused on the production and conditioning of hydrogen. This involves various methods such as electrolysis (green hydrogen), steam methane reforming with carbon capture (blue hydrogen), and other emerging production technologies. Post-production, hydrogen is typically compressed to high pressures to increase its energy density and facilitate efficient transport. This stage includes purification processes to meet specific end-use requirements, as impurities can impact pipeline integrity and downstream applications. Key players in this segment are often large energy companies, chemical producers, and renewable energy developers investing in large-scale hydrogen generation facilities.

Downstream activities encompass the distribution and ultimate consumption of hydrogen. Once transported through pipelines, hydrogen reaches various end-users including industrial sites, hydrogen fueling stations, power generation facilities, and facilities for grid injection. At this stage, pressure reduction and further purification might be necessary depending on the application. The distribution channel structure can be bifurcated into direct and indirect methods. Direct distribution involves hydrogen flowing directly from a production source through a dedicated pipeline to a large industrial consumer, such as an ammonia plant or a refinery, where demand is consistent and high volume. This model often involves bilateral agreements and specialized infrastructure.

Indirect distribution, on the other hand, involves hydrogen being transported through broader network pipelines to regional hubs or distribution centers, from which it is then supplied to multiple, smaller-scale end-users. This could include hydrogen being delivered to public fueling stations, smaller industrial users, or blended into local natural gas grids. This indirect approach requires more extensive network planning, potential intermediate storage solutions, and a more complex logistics chain involving gas transmission system operators and local distribution companies. Both direct and indirect channels are critical for market growth, with direct channels supporting established industrial demand and indirect channels facilitating broader market penetration and the development of new applications.

Potential customers for hydrogen pipeline infrastructure primarily comprise large-scale industrial consumers that utilize hydrogen as a critical feedstock or energy source in their manufacturing processes. The chemical industry, particularly for ammonia and methanol production, represents a significant end-user segment due to its high and continuous demand for hydrogen. Similarly, petroleum refineries rely heavily on hydrogen for various hydrotreating and hydrocracking processes to produce cleaner fuels. These industries often require dedicated, high-volume supplies of hydrogen, making direct pipeline connections a highly efficient and cost-effective solution.

Beyond traditional industrial applications, the burgeoning clean energy sector presents a rapidly expanding customer base. Power generation companies are increasingly exploring hydrogen as a fuel for gas turbines or in fuel cells to generate electricity, especially as part of strategies to integrate renewable energy and balance grid fluctuations. The transportation sector, including heavy-duty vehicles, maritime, and rail, is also emerging as a substantial future customer segment, requiring pipeline networks to supply hydrogen to refueling stations and depots. Furthermore, utilities and gas network operators are potential customers as they look to inject hydrogen into existing natural gas grids or convert sections for pure hydrogen distribution for heating and industrial use, signaling a diversified and growing demand landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $1.5 Billion |

| Market Forecast in 2032 | $2.7 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | GAZNATURAL FENOSA, Snam S.p.A., Enagás S.A., GRTgaz S.A., Fluxys Belgium NV/SA, Open Grid Europe GmbH, N.V. Nederlandse Gasunie, Woodside Energy Group Ltd, Linde plc, Air Liquide S.A., Sempra Energy, Kinder Morgan, Inc., Williams Companies, TC Energy Corporation, Saudi Aramco, ADNOC, Baker Hughes Company, Siemens Energy AG, Cummins Inc., Equinor ASA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Hydrogen Pipeline Market relies on a sophisticated and continuously evolving technology landscape to ensure the safe, efficient, and cost-effective transportation of hydrogen. Material science plays a pivotal role, with ongoing research and development focused on pipeline materials that can withstand hydrogen embrittlement, a phenomenon where hydrogen atoms diffuse into metals, leading to reduced ductility and increased susceptibility to cracking. This includes advancements in high-strength steels, stainless steel alloys, and composite materials, as well as internal coatings and liners designed to protect pipeline integrity and minimize hydrogen interaction with the pipe wall. The selection of appropriate materials is critical for both new pipeline construction and the repurposing of existing natural gas infrastructure, where modifications to mitigate embrittlement risks are essential.

Compression technologies are another cornerstone of the hydrogen pipeline market, as hydrogen needs to be highly compressed to achieve economically viable transportation volumes and pressures. Advanced compressor designs, including centrifugal, reciprocating, and ionic liquid compressors, are being developed to enhance efficiency and reduce energy consumption. Leak detection and monitoring systems are also undergoing rapid innovation, incorporating technologies such as fiber optic sensing, acoustic sensors, and advanced gas chromatographs that can detect minute hydrogen leaks with high precision and speed. These systems are crucial for operational safety and environmental protection, often integrated with Supervisory Control and Data Acquisition (SCADA) systems for real-time data analysis and remote control.

Furthermore, digital technologies like the Industrial Internet of Things (IIoT), artificial intelligence (AI), and digital twin modeling are transforming pipeline operations. IIoT sensors provide continuous data on pressure, temperature, flow rates, and material integrity, which AI algorithms then analyze to predict maintenance needs, optimize flow paths, and identify potential anomalies. Digital twin technology creates virtual replicas of physical pipelines, allowing operators to simulate various scenarios, test operational changes, and train personnel in a risk-free environment. These advanced technologies collectively aim to enhance the reliability, safety, and overall performance of hydrogen pipeline networks, making them more resilient and adaptive to the demands of a growing hydrogen economy.

The primary challenges include high upfront capital costs for construction and repurposing, technical complexities related to hydrogen embrittlement and leak detection, ensuring public safety, and overcoming regulatory hurdles. Public acceptance and establishing a robust demand-side economy also present significant obstacles.

Hydrogen pipelines are designed with extensive safety measures, leveraging advanced materials, robust monitoring systems, and strict operational protocols. While hydrogen has unique characteristics like flammability, continuous advancements in engineering, leak detection, and regulatory oversight aim to ensure their safe operation comparable to natural gas pipelines.

Yes, many existing natural gas pipelines can be repurposed for hydrogen transport, either as pure hydrogen or in blends. However, this often requires extensive evaluation for material compatibility, internal coatings, and modifications to compression stations, valves, and other ancillary equipment to ensure integrity and safety.

The cost of building new hydrogen pipelines varies significantly based on length, diameter, pressure, terrain, and material. Repurposing existing natural gas pipelines is generally less expensive than new construction but still involves substantial investment for modifications, typically ranging from a fraction to a significant percentage of new pipeline costs.

Governments play a crucial role through policy setting, offering financial incentives (grants, tax credits), funding research and development, establishing safety standards, and facilitating international cooperation. Their support is essential for de-risking investments and accelerating the build-out of a comprehensive hydrogen infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.