ID : MRU_ 429875 | Date : Nov, 2025 | Pages : 255 | Region : Global | Publisher : MRU

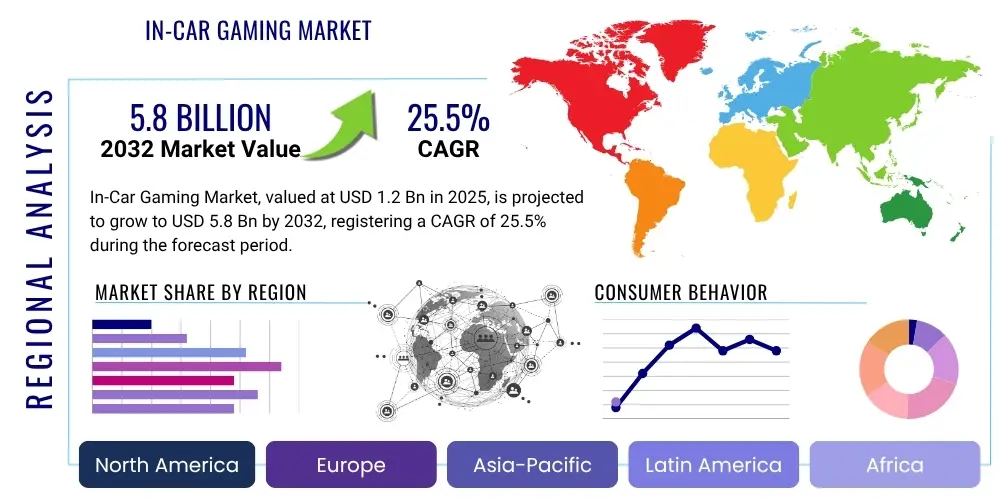

The In-Car Gaming Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2032. This substantial growth trajectory reflects the burgeoning demand for integrated digital entertainment solutions within the automotive sector, driven by evolving consumer lifestyles, rapid technological advancements in vehicle platforms, and the increasing convergence of mobility with digital experiences. The market is estimated at USD 1.2 billion in 2025, representing a foundational stage as automotive manufacturers and technology providers increasingly collaborate to embed sophisticated gaming capabilities into modern vehicles. This initial valuation underscores the nascent but rapidly accelerating adoption of interactive entertainment systems, moving beyond basic infotainment to offer rich, immersive digital worlds within the car cabin. The market's early phase is characterized by significant investment in research and development, aiming to overcome technical hurdles and establish robust gaming ecosystems.

By the end of the forecast period in 2032, the market is projected to reach USD 5.8 billion. This significant increase highlights the anticipated maturation and widespread proliferation of in-car gaming ecosystems across various vehicle segments globally. The growth will be fueled by the continued development of connected and autonomous vehicles, which inherently free up occupant attention, thereby creating a natural demand for engaging entertainment. Furthermore, advancements in in-car hardware, such as larger and higher-resolution displays, more powerful processors, and enhanced connectivity solutions (like 5G), will facilitate the delivery of console-quality gaming experiences. The widespread acceptance of vehicles as extensions of personal digital spaces, combined with the growing consumer expectation for seamless, on-demand entertainment, will foster a new era of in-transit engagement for occupants worldwide. This growth will also be supported by innovative business models, including subscription services and partnerships between automotive OEMs and leading game developers, ensuring a continuous influx of fresh and compelling content for the in-car gaming environment.

The In-Car Gaming Market defines a transformative segment within the automotive and entertainment industries, focusing on the seamless integration of interactive digital entertainment experiences directly into vehicle infotainment systems, passenger displays, and control interfaces. This innovative product category is fundamentally reshaping the conventional understanding of a vehicle's cabin, transitioning it from a mere mode of transport into a dynamic, personalized entertainment hub, thereby offering occupants new forms of engagement during transit and idle times. It encompasses a broad spectrum of digital games, ranging from lightweight casual applications optimized for quick play sessions to more graphically intensive and complex titles leveraging advanced in-car hardware and cloud-based processing. The product description emphasizes the convergence of high-performance computing, advanced display technologies, and robust connectivity to deliver immersive gaming, setting new benchmarks for in-vehicle digital experiences. Major applications are diverse and growing, including enhancing the passenger experience in long-haul journeys, providing engaging diversions for children, offering entertainment during charging stops for electric vehicles, and crucially, preparing for the future where occupants of autonomous vehicles will have significantly more leisure time and a desire for meaningful interaction. The inherent benefits are manifold: improved journey satisfaction, reduced passenger boredom, enhanced vehicle differentiation for manufacturers seeking unique selling propositions in a competitive market, and the creation of a more personalized, comfortable, and enjoyable in-cabin environment that caters to modern digital lifestyles and expectations for omnipresent entertainment.

The market's rapid ascent is profoundly influenced by a confluence of powerful driving factors, creating a fertile ground for unprecedented growth and innovation. Firstly, significant advancements in automotive technology, particularly the exponential development of more powerful central processing units (CPUs) and graphics processing units (GPUs) embedded within vehicles, enable higher fidelity gaming experiences that were once confined to dedicated gaming consoles. These robust onboard computing capabilities are crucial for rendering complex visuals and managing sophisticated game mechanics. Secondly, the pervasive increase in vehicle connectivity, spearheaded by the widespread rollout of 5G networks and sophisticated in-car Wi-Fi hotspots, facilitates seamless cloud gaming and real-time multiplayer interactions, effectively overcoming previous latency and download barriers that limited in-car entertainment. Thirdly, the accelerating trajectory towards higher levels of autonomous driving (L3, L4, L5) is a pivotal driver; as vehicles assume more control over driving tasks, human occupants, particularly those not actively driving, will gain unprecedented free time and attention, naturally creating a substantial demand for engaging and immersive entertainment options within the cabin. Finally, the overarching shift in global consumer behavior, marked by a pervasive desire for seamless digital integration across all personal devices and environments, extends naturally to the automotive space, positioning in-car gaming as an anticipated and desired feature rather than a mere novelty. These interconnected elements collectively coalesce to form a robust foundation for sustained market expansion and continuous innovation in the coming years, promising a future where the vehicle is a true digital extension of home and office entertainment.

The In-Car Gaming Market is currently navigating a period of accelerated evolution, characterized by significant shifts across business models, geographical landscapes, and segment dynamics, indicating a robust future for in-vehicle entertainment. In terms of business trends, the industry is witnessing a pronounced strategic pivot towards collaborative ecosystems. Automotive Original Equipment Manufacturers (OEMs) are increasingly forging intricate partnerships with established game developers, innovative software companies, and leading technology providers to co-create robust in-car gaming platforms. This involves substantial investment in developing vehicle-optimized hardware architectures capable of supporting advanced graphics and complex game logic, alongside efforts to curate extensive, car-friendly game libraries that cater to diverse tastes and demographics. Content licensing agreements, subscription-based service models for recurring revenue, and integrated app stores are becoming central to monetization strategies, fostering customer loyalty and enhancing the overall value proposition. The competitive landscape is also seeing a rise in specialized startups focusing solely on in-car entertainment solutions, alongside traditional gaming giants exploring this new frontier, driving a healthy cycle of innovation and differentiation.

Regionally, the market exhibits distinct patterns of adoption and growth, reflecting varying stages of technological maturity and consumer readiness. North America and Europe currently represent the vanguard in market penetration, attributable to their mature automotive infrastructures, high consumer disposable incomes, and a strong predisposition towards early adoption of advanced in-car technologies. These regions are also hubs for luxury and electric vehicle manufacturers who are often at the forefront of integrating premium digital experiences and cutting-edge infotainment systems. Concurrently, Asia Pacific, with China at its epicenter, is rapidly emerging as the predominant growth engine. This surge is fueled by China’s massive automotive production and sales volumes, rapid technological advancement, widespread 5G deployment, and a vast, digitally native consumer base eager for cutting-edge entertainment solutions. Other Asian markets like Japan and South Korea also contribute significantly through their advanced telecommunications infrastructure and innovative local automotive players, solidifying the region's position as a critical future growth area. Latin America and the Middle East & Africa regions are showing promising, albeit nascent, growth driven by improving economic conditions and increasing urbanization, signifying future expansion opportunities for adaptable market entrants.

Segmentation trends within the In-Car Gaming Market underscore a multi-faceted approach to meeting diverse consumer needs and technological requirements. The market observes a strong demand for casual, family-friendly, and educational games, particularly tailored for rear-seat entertainment, effectively addressing the common need to engage younger passengers during travel and alleviate boredom. However, with the progressive shift towards autonomous vehicles, there is an escalating interest in more sophisticated, console-quality gaming experiences designed for front-seat occupants who will no longer be solely focused on driving. Connectivity-dependent segments, such as cloud gaming and multiplayer options, are gaining significant traction, enabled by faster and more reliable in-car internet infrastructure. Platform integration is also a critical trend, with OEMs choosing between developing proprietary systems, leveraging existing mobile ecosystems like Android Automotive OS, or integrating with broader cloud gaming services to maximize content availability and user familiarity. These distinct segment dynamics collectively influence product development, marketing strategies, and investment decisions across the value chain, pushing the boundaries of what is possible within the confined but increasingly capable vehicle environment and pointing towards a highly diversified market future.

User questions surrounding the influence of Artificial Intelligence on the In-Car Gaming Market predominantly center on several key themes: the extent to which AI can personalize and enhance gameplay, its role in creating more immersive and realistic experiences, the paramount concern for safety and driver distraction, and the potential for AI to unlock entirely novel forms of interactive entertainment within the vehicle cabin. There is a palpable curiosity about how AI can adapt game content dynamically to passenger preferences, journey conditions, or even real-time vehicle data, moving beyond static, pre-programmed narratives to offer truly responsive and tailored experiences. Users also express concerns regarding data privacy implications of AI systems collecting personal usage patterns and in-car behavior, and the ethical considerations around AI-generated content or autonomous decision-making within games, particularly if integrated with vehicle controls. The overarching expectation is that AI will not merely optimize existing gaming paradigms but will fundamentally revolutionize the in-car entertainment landscape, making it more intuitive, responsive, and deeply integrated with the automotive environment, ultimately transforming passive travel time into an active, engaging digital experience.

This analysis reveals a strong desire for AI to address both current limitations and future possibilities in in-car gaming, indicating a demand for intelligent, context-aware systems. The key themes emerging include the demand for intelligent systems that can learn and adapt, thereby overcoming the monotony often associated with repetitive gaming and providing endless variety. There is also an emphasis on AI's potential to elevate the sensory experience through advanced rendering, adaptive sound design, and intelligent haptic feedback, bringing console-like quality to the car's interior. Balancing these sophisticated enhancements with uncompromising safety standards remains a central concern, pushing for AI solutions that can intelligently manage potential distractions for the driver while providing rich entertainment for passengers. Furthermore, the anticipation of generative AI capabilities suggests a future where game content is not just consumed but dynamically created or customized for each unique journey, ensuring fresh and relevant experiences every time a passenger engages with the system. The market is thus keenly watching how AI can deliver on these high expectations, shaping the next generation of automotive entertainment and defining new frontiers for in-vehicle digital engagement.

The In-Car Gaming Market is currently shaped by a dynamic interplay of Drivers, Restraints, and Opportunities, collectively influenced by various impact forces that dictate its growth trajectory and adoption rates, offering a comprehensive view of its potential and challenges. A primary driver is the pervasive technological advancement within the automotive sector, specifically the exponential increase in computational power of in-vehicle infotainment systems and the sophistication of digital displays. Modern cars are increasingly equipped with processors and GPUs capable of handling complex graphics, significantly enhancing the potential for high-fidelity gaming. Concurrently, the global rollout and increasing ubiquity of high-speed vehicle connectivity, particularly 5G networks and advanced Wi-Fi capabilities, are pivotal, enabling robust cloud gaming services and real-time multiplayer interactions that were previously unfeasible due to latency or bandwidth limitations. The progressive development towards higher levels of autonomous driving (Level 3 and above) acts as a significant catalyst, as it profoundly frees up passenger attention and, eventually, driver engagement, creating a substantial demand for engaging in-cabin entertainment options that fill this newly acquired leisure time. Furthermore, evolving consumer expectations, which increasingly view vehicles as extensions of their digital lifestyle, contribute significantly to the market's expansion, driving demand for seamless integration of gaming and multimedia content into their daily commutes and long journeys, making the car an extension of their home entertainment system.

Despite these potent drivers, the market faces notable restraints that require careful navigation and innovative solutions to overcome. The substantial developmental and integration costs associated with embedding high-performance gaming hardware and sophisticated software into vehicles represent a significant barrier for automotive OEMs, requiring considerable upfront investment, complex engineering efforts, and specialized supply chain management. Concerns over potential driver distraction, even in semi-autonomous or passenger-centric scenarios, remain a critical regulatory and public perception challenge, necessitating advanced safety mechanisms, robust software interlocks, and clear design guidelines that prioritize road safety above entertainment. Stringent regulatory frameworks pertaining to in-car display content and interactive systems, which vary significantly across different jurisdictions and often lag behind technological advancements, add another layer of complexity for manufacturers and content providers, requiring constant adaptation and compliance. Additionally, optimizing games for the unique in-car environment – considering factors such as varying screen sizes, limited physical input methods, potential motion sickness, power consumption, and thermal management within a confined space – presents technical hurdles that demand specialized development efforts and innovative solutions, preventing direct porting of existing games.

Amidst these challenges, considerable opportunities are emerging that promise to redefine and expand the In-Car Gaming Market, charting new pathways for growth and value creation. Strategic partnerships between automotive original equipment manufacturers (OEMs) and leading game developers, technology companies (e.g., semiconductor firms, software houses), and cloud gaming providers are crucial for fostering innovation, sharing development costs, mitigating risks, and creating compelling content ecosystems that are both diverse and deeply integrated. The increasing viability of subscription-based content models for in-car entertainment offers a pathway to recurring revenue streams, sustained consumer engagement, and a continuous delivery of fresh content, moving beyond one-time purchases. The development of unique, car-specific gaming experiences that intelligently leverage vehicle sensors (like GPS, accelerometer, cameras), external environment data, and internal haptic feedback systems presents a powerful differentiator, offering gameplay that cannot be replicated outside a vehicle and creating novel forms of entertainment. Moreover, the integration of advanced immersive technologies like Augmented Reality (AR) and Virtual Reality (VR) into the car cabin, potentially synchronized with the external environment or providing fully encapsulated virtual worlds, holds immense potential for delivering truly novel and captivating experiences. The underlying impact forces, including rapid hardware innovation, decreasing component costs over time due to economies of scale, and a growing global appetite for interactive digital entertainment, will continuously reshape the competitive landscape, pushing boundaries and driving sustained market evolution towards a future where the car is a primary entertainment venue.

The In-Car Gaming Market is characterized by a granular segmentation based on a multitude of factors, each providing distinct insights into its operational dynamics, target demographics, and technological requirements. This detailed categorization enables market participants, from automotive OEMs to game developers and technology suppliers, to precisely identify nascent growth opportunities, understand evolving consumer preferences, and craft highly targeted product development and marketing strategies. The segmentation approach encompasses technical components that define the core infrastructure, vehicle categories that delineate adoption patterns, game genres appealing to diverse tastes, underlying software platforms, and methods of content delivery based on connectivity. Each segment's performance is intrinsically linked to broader trends in automotive technology, consumer electronics, and regulatory frameworks, making this comprehensive analysis vital for strategic planning and competitive positioning within this rapidly evolving industry landscape, ensuring offerings are both relevant and innovative.

Understanding these distinct segments is paramount for effective market penetration and innovation, as they highlight the diverse needs and expectations across the automotive ecosystem. For instance, the choice of component directly influences the performance and immersion capabilities of the gaming system, dictating graphics fidelity, processing speed, and interactivity. Similarly, the specific vehicle type dictates the available space, power budget, target user profile (e.g., family vs. individual), and integration challenges. Different game types cater to varying age groups and preferences, from quick casual distractions to deep, narrative-driven experiences that can occupy hours of travel time. The platform chosen affects ecosystem compatibility, developer access, and the ease of content updates, while connectivity options determine the scope for online multiplayer, cloud streaming, and regular content acquisition. Furthermore, considering end-users provides critical insight into behavioral patterns, specific needs for safety and parental controls, and monetization potential, whereas sales channels inform go-to-market strategies and distribution models. By dissecting the market through these comprehensive lenses, stakeholders can gain a granular and actionable understanding of the diverse forces shaping the future of in-car entertainment, allowing for the creation of solutions that are both technologically advanced and commercially viable, driving sustainable growth and fostering innovation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.2 billion |

| Market Forecast in 2032 | USD 5.8 billion |

| Growth Rate | 25.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tesla Inc., Audi AG, Mercedes-Benz Group AG, BMW AG, Volvo Cars, Hyundai Motor Company, General Motors Company, Ford Motor Company, Stellantis N.V., Toyota Motor Corporation, Unity Technologies, Epic Games, NVIDIA Corporation, Qualcomm Technologies Inc., Harman International (Samsung), Visteon Corporation, Bosch Group, WayRay, Google LLC, Apple Inc., Microsoft Corporation (Xbox Game Studios), Sony Group Corporation (PlayStation), Tencent Holdings Ltd., Roborace, BlackBerry Limited. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The In-Car Gaming Market is fundamentally driven and defined by a sophisticated and rapidly evolving technological landscape, engineered to provide seamless, engaging, and safe entertainment experiences within the confines of a vehicle cabin. At its core are advancements in high-performance automotive-grade computing hardware. This includes powerful System-on-Chips (SoCs) integrating multi-core Central Processing Units (CPUs) and Graphics Processing Units (GPUs) capable of rendering complex 3D graphics and supporting demanding game engines, effectively rivaling the capabilities of dedicated home consoles in terms of visual fidelity and processing power. These processors are specifically designed and rigorously tested to withstand extreme automotive environmental conditions, such as wide temperature variations, persistent vibrations, and electromagnetic interference, while consistently maintaining optimal performance and reliability. Complementing this, sophisticated infotainment systems serve as the primary interface, featuring large, high-resolution, multi-touch displays (often utilizing advanced technologies like OLED or mini-LED for superior contrast, color accuracy, and responsiveness) that provide intuitive user interaction, sometimes augmented with haptic feedback for tactile responses that enhance immersion and usability.

In-car gaming refers to the integration of interactive digital games directly into a vehicle's infotainment system, screens, or other displays, providing entertainment to occupants during travel or idle times. While sharing a common digital foundation with mobile gaming, it differentiates significantly by leveraging the car's unique hardware, such as larger, fixed displays, dedicated automotive-grade processors, advanced multi-speaker audio systems, and robust vehicle connectivity. Crucially, in-car gaming can integrate vehicle-specific data (like GPS coordinates, vehicle speed, or motion sensors) directly into gameplay, offering deeply contextual and immersive experiences that are optimized for the automotive environment and often designed for multiple passengers simultaneously, contrasting with the typically personal, smaller-screen, and less integrated experience of traditional mobile gaming on smartphones or tablets.

Safety is a paramount concern for in-car gaming, particularly regarding its potential impact on driver attention. To mitigate distraction risks, most in-car gaming systems are engineered with robust safety protocols designed to prevent gameplay on the main driver-facing screen or any display within the driver's direct line of sight when the vehicle is in motion. Passenger screens, especially those in the rear, typically remain fully functional and are safe for use. Regulations concerning in-car displays and interactive features vary significantly by region and jurisdiction, but generally prohibit driver engagement with games while operating the vehicle. As autonomous driving capabilities advance, these regulations may evolve to reflect the reduced need for human intervention, but current designs prioritize non-distracting entertainment solely for passengers. Implementing robust software interlocks, clear user interfaces, and adhering to legal guidelines are critical to ensure road safety and responsible integration of gaming features.

Several forward-thinking automotive manufacturers are spearheading the integration of advanced in-car gaming features, positioning themselves at the forefront of this emerging market. Tesla Inc. is widely recognized as a pioneer, offering a comprehensive and continuously updated suite of games accessible via their large central touchscreen, leveraging their powerful infotainment system. Luxury brands such as Mercedes-Benz Group AG, BMW AG, and Audi AG are also investing heavily in this space, often through strategic partnerships with established game developers and technology providers, to embed sophisticated gaming experiences into their premium infotainment systems. Additionally, manufacturers like Volvo Cars and Hyundai Motor Company are actively exploring and implementing gaming options, particularly in their electric vehicle lineups, recognizing the potential for entertainment during charging stops and enhanced passenger experience. This trend highlights a growing industry-wide shift towards making the car a versatile digital entertainment hub.

The types of games best suited for the unique in-car entertainment environment typically lean towards those that are easily digestible, family-friendly, or offer immersive experiences without requiring complex physical controls or highly demanding attention. Casual games such as puzzles, arcade classics, and hyper-casual mobile adaptations are highly popular due to their instant accessibility, short play sessions, and ability to engage younger passengers or adults during brief stops. Educational games designed for children are also in significant demand, blending learning with entertainment during commutes. As in-car technology advances, mid-core games like adventure titles, strategy games, and racing simulations optimized for vehicle-specific controls or cloud streaming are gaining traction. The expansion of cloud gaming platforms is also enabling access to a broader range of graphically intense and console-quality titles, further diversifying the spectrum of available genres for passengers, ensuring there is content for nearly every preference within the vehicle cabin.

Autonomous vehicle technology is poised to be the most significant catalyst for the profound transformation of the in-car gaming market. As vehicles achieve higher levels of autonomy (Level 3 and beyond), the need for human drivers to remain actively engaged in operating the car will diminish, eventually freeing up all occupants, including the former 'driver', for other activities. This fundamental shift will unlock a vast, unprecedented opportunity for more complex, time-consuming, and deeply immersive gaming experiences. The car cabin will evolve from a functional space into a dedicated mobile entertainment lounge or a third living space, fostering immense demand for advanced hardware, rich content libraries, and innovative game designs that leverage the unique context of a moving environment. This transformation will significantly accelerate market growth and innovation, allowing for console-quality gaming, virtual reality experiences, and context-aware interactive narratives that redefine how leisure time is spent during travel, making the autonomous vehicle a prime venue for next-generation digital entertainment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.