ID : MRU_ 431262 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

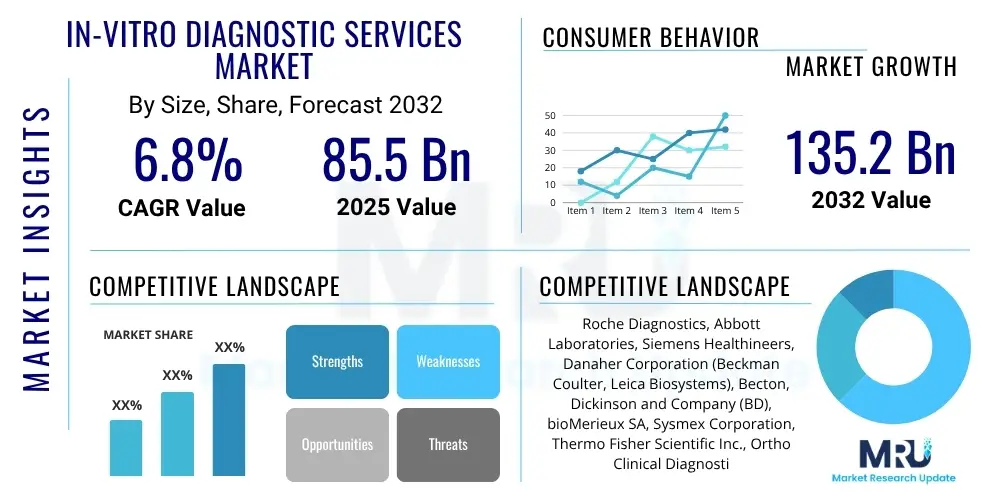

The In-vitro Diagnostic Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 85.5 billion in 2025 and is projected to reach USD 135.2 billion by the end of the forecast period in 2032.

The In-vitro Diagnostic (IVD) Services market encompasses a broad range of medical tests performed on samples such as blood, urine, or tissue, outside of the body, to detect diseases, infections, and medical conditions. These services are crucial for accurate diagnosis, monitoring of treatment effectiveness, and screening for various health disorders, thereby forming the backbone of modern healthcare systems. The primary product offerings include a vast array of reagents, kits, and sophisticated instruments designed for various diagnostic analyses.

Major applications of IVD services span across numerous medical fields, including infectious disease testing, oncology, cardiology, diabetes management, and genetic screening, facilitating early disease detection and personalized treatment approaches. The fundamental benefits derived from these services include enhanced diagnostic precision, expedited disease identification, and improved patient outcomes through timely and appropriate medical interventions. Furthermore, IVD services play a pivotal role in public health surveillance, contributing to the management and control of epidemics.

The market's robust growth is primarily driven by several influential factors. These include the escalating global prevalence of chronic and infectious diseases, a rapidly aging population susceptible to various health conditions, and continuous advancements in diagnostic technologies that offer higher accuracy and efficiency. Additionally, increasing healthcare expenditure worldwide, greater awareness regarding early disease diagnosis, and the rising demand for personalized medicine are significant contributors to the expansion of the In-vitro Diagnostic Services Market.

The In-vitro Diagnostic Services market is experiencing dynamic shifts, driven by evolving business strategies, significant regional developments, and technological advancements across its various segments. Key business trends indicate a strong move towards consolidation among major players seeking to expand their product portfolios and geographical reach, alongside increased investment in research and development for novel diagnostic solutions. Digitalization and automation are also transforming laboratory operations, leading to enhanced efficiency and reduced turnaround times, which are crucial for timely patient care.

Regionally, North America continues to hold a dominant share, propelled by robust healthcare infrastructure, high healthcare spending, and the early adoption of advanced diagnostic technologies. However, the Asia Pacific region is emerging as the fastest-growing market, characterized by improving healthcare access, increasing awareness about early diagnosis, and a large patient population, making it an attractive hub for future investments. Europe maintains a significant market presence, supported by well-established healthcare systems and an aging demographic driving demand for diagnostic services, while regulatory landscapes continually evolve to ensure test quality and safety.

Segmentation trends highlight the increasing importance of molecular diagnostics, driven by the rising prevalence of infectious diseases and genetic disorders, alongside the growing demand for personalized medicine. Immunoassays and clinical chemistry also remain foundational segments, consistently benefiting from automation and the development of high-throughput platforms. Point-of-care testing is gaining considerable traction due to its convenience and potential to improve diagnostic accessibility, particularly in remote or underserved areas, contributing to overall market expansion and diversification.

Common user questions regarding AI's impact on In-vitro Diagnostic Services frequently revolve around the potential for enhanced diagnostic accuracy, the acceleration of testing processes, and the role of AI in personalizing patient care. Users are keen to understand how AI can interpret complex biological data, identify subtle disease markers, and improve predictive analytics for various conditions. Concerns often emerge regarding data privacy and security, the ethical implications of AI-driven diagnostics, the potential for job displacement among laboratory professionals, and the significant regulatory hurdles that new AI-powered diagnostic tools may face before widespread adoption. Users also question the reliability and validation processes for AI algorithms and the integration challenges within existing laboratory infrastructures.

The In-vitro Diagnostic Services market is significantly shaped by a confluence of powerful drivers, challenging restraints, and emerging opportunities, collectively forming its impact forces. The primary drivers include the global surge in chronic and infectious diseases, the expansion of the elderly population requiring more frequent diagnostic screening, and relentless technological innovations that enhance test accuracy and efficiency. These factors collectively push for increased adoption of advanced IVD solutions, fostering market growth and expanding diagnostic capabilities across diverse healthcare settings.

Conversely, the market faces notable restraints such as the high initial cost associated with sophisticated IVD instruments and reagents, which can limit adoption, especially in resource-constrained regions. Stringent regulatory frameworks for new diagnostic product approvals, aimed at ensuring safety and efficacy, can often prolong market entry and increase development costs. Furthermore, challenges related to reimbursement policies and the scarcity of skilled laboratory professionals capable of operating advanced diagnostic platforms also pose significant barriers to market expansion.

Despite these challenges, substantial opportunities exist, particularly in emerging economies where healthcare infrastructure is rapidly developing and patient awareness is growing. The increasing adoption of point-of-care testing offers convenience and accessibility, while the rise of companion diagnostics presents a pathway for personalized medicine by linking diagnostic tests to specific therapies. The integration of artificial intelligence and machine learning promises to revolutionize data analysis, accelerate discovery, and improve diagnostic precision, representing a frontier of growth and innovation within the IVD market.

The In-vitro Diagnostic Services market is comprehensively segmented to provide a detailed understanding of its diverse components and growth trajectories across various dimensions. This segmentation helps in analyzing market dynamics based on product types, technologies employed, application areas, and the end-user demographics, offering granular insights into specific market niches. Each segment reflects unique market demands, technological requirements, and regulatory considerations, thereby influencing strategic decisions for market participants and stakeholders.

The value chain for the In-vitro Diagnostic Services market is intricate, involving multiple stages from raw material procurement to final service delivery to end-users. The upstream segment primarily involves suppliers of crucial raw materials, including specialized chemicals, enzymes, antibodies, and genetic sequences, which are essential for manufacturing diagnostic reagents and kits. This stage also includes manufacturers of the core components and sophisticated hardware systems that form the basis of IVD instruments, requiring high precision and quality control.

Midstream activities encompass the research, development, and manufacturing of IVD products, including reagents, kits, and instruments by major diagnostic companies. This stage is heavily reliant on innovation, regulatory compliance, and robust manufacturing processes to produce reliable and accurate diagnostic tools. Product differentiation through technological advancements and competitive pricing strategies are key factors at this stage.

The downstream segment focuses on the distribution and delivery of IVD products and services to end-users. Distribution channels can be both direct and indirect. Direct distribution often involves large manufacturers selling directly to major hospital networks, reference laboratories, and government healthcare providers, enabling closer customer relationships and tailored support. Indirect distribution utilizes a network of third-party distributors, wholesalers, and specialized logistics providers to reach smaller diagnostic laboratories, clinics, physician offices, and retail pharmacies, ensuring broader market penetration and access to a wider customer base. Both channels are critical for efficient market reach and effective service provision.

The In-vitro Diagnostic Services market caters to a diverse array of end-users and buyers, each with specific diagnostic needs and operational requirements. Hospitals represent a significant customer segment, relying heavily on IVD services for patient admissions, emergency diagnostics, routine health checks, and specialized departmental testing across various medical disciplines. Their demand often includes high-throughput systems and comprehensive test menus to manage a large and varied patient population, making them central to the market's growth.

Diagnostic laboratories, including standalone reference laboratories and those integrated within healthcare systems, are another primary customer group. These facilities specialize in performing a wide range of IVD tests, often acting as intermediaries for smaller clinics and physician offices that outsource their diagnostic testing needs. They typically seek advanced, automated systems that offer high precision, efficiency, and scalability to handle extensive test volumes and complex analyses.

Furthermore, academic and research institutes utilize IVD products and services for various studies, clinical trials, and drug discovery processes, pushing the boundaries of diagnostic innovation. Physician offices and clinics also require convenient and rapid diagnostic solutions, often favoring point-of-care testing for immediate results. Blood banks, public health organizations for disease surveillance, and increasingly, individuals for home-based testing, also constitute significant and growing customer segments within the dynamic In-vitro Diagnostic Services market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 85.5 billion |

| Market Forecast in 2032 | USD 135.2 billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Danaher Corporation (Beckman Coulter, Leica Biosystems), Becton, Dickinson and Company (BD), bioMerieux SA, Sysmex Corporation, Thermo Fisher Scientific Inc., Ortho Clinical Diagnostics (QuidelOrtho), Bio-Rad Laboratories, Inc., Qiagen N.V., Hologic Inc., Illumina, Inc., Agilent Technologies, Inc., Grifols S.A., Mindray Medical International Limited, Eiken Chemical Co., Ltd., Sekisui Diagnostics, Fujirebio, DiaSorin S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The In-vitro Diagnostic Services market is characterized by a rapidly evolving technological landscape that continuously drives innovation and improves diagnostic capabilities. Advanced molecular diagnostic techniques, such as Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), and gene editing technologies like CRISPR, are transforming the detection of genetic disorders, infectious agents, and cancer biomarkers with unprecedented precision and speed. These technologies allow for detailed analysis of nucleic acids, opening new avenues for personalized medicine and early disease intervention.

Immunoassay platforms, including ELISA and chemiluminescence, continue to be foundational technologies for detecting proteins, hormones, and antibodies, with ongoing advancements focusing on miniaturization, higher sensitivity, and multi-analyte detection. Automation and robotics are also pivotal, integrating various analytical stages from sample preparation to result interpretation, significantly enhancing laboratory efficiency, reducing manual errors, and accelerating turnaround times. This automation is critical for managing the increasing volume of tests in large diagnostic laboratories.

Furthermore, the emergence of point-of-care (POC) diagnostic devices is revolutionizing access to testing by enabling rapid results outside of traditional laboratory settings, often using microfluidics and biosensor technologies for ease of use and portability. Alongside these, sophisticated bioinformatics tools and artificial intelligence are becoming indispensable for interpreting complex diagnostic data, particularly in genomics and proteomics, to derive clinically actionable insights and support decision-making, marking a significant leap in diagnostic intelligence.

The market is primarily driven by the increasing global prevalence of chronic and infectious diseases, the expansion of the aging population, continuous advancements in diagnostic technologies, and rising healthcare expenditures worldwide. These factors collectively boost the demand for accurate and efficient diagnostic solutions, leading to sustained market expansion.

Key challenges include the high cost associated with advanced IVD instruments and reagents, stringent regulatory approval processes that can delay market entry, and the ongoing shortage of skilled laboratory professionals. Reimbursement complexities and integration issues for new technologies also pose significant hurdles for market participants.

Technology is revolutionizing IVD through molecular diagnostics (PCR, NGS) for precise disease detection, automation and robotics for enhanced lab efficiency, and the development of point-of-care devices for rapid, accessible testing. Additionally, AI and bioinformatics are improving data interpretation and enabling personalized medicine approaches.

North America currently holds the largest market share due to its advanced healthcare infrastructure, significant investments in research and development, high healthcare spending, and early adoption of innovative diagnostic technologies. The presence of major market players and a focus on preventive medicine further solidifies its dominance.

Emerging opportunities include the rapid growth in developing economies, increasing demand for point-of-care testing, the integration of artificial intelligence and machine learning for enhanced diagnostics, and the expansion of companion diagnostics for personalized therapeutic strategies. These areas promise significant growth and innovation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.