ID : MRU_ 431309 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

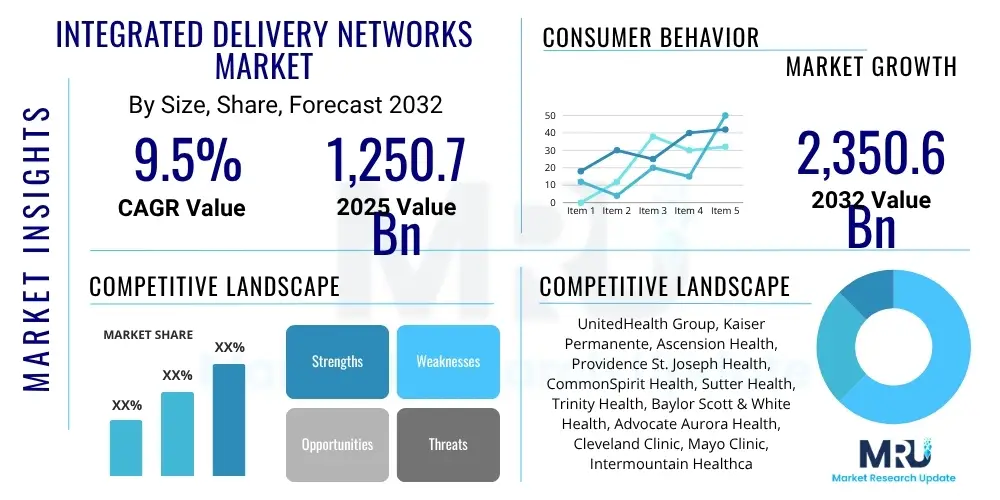

The Integrated Delivery Networks Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at USD 1,250.7 Billion in 2025 and is projected to reach USD 2,350.6 Billion by the end of the forecast period in 2032.

Integrated Delivery Networks (IDNs) represent a strategic organizational model within the healthcare industry that consolidates various healthcare providers, services, and facilities under a unified administrative and operational framework. This comprehensive approach aims to streamline patient care pathways, enhance clinical outcomes, and optimize resource utilization across a continuum of care settings, from primary care clinics and specialist centers to acute care hospitals, diagnostic laboratories, and post-acute facilities. The underlying principle of an IDN is to foster greater collaboration and coordination among disparate healthcare entities, moving away from fragmented service delivery towards a more cohesive, patient-centric system.

The product, in the context of an IDN, encompasses the integrated ecosystem of healthcare services, advanced technologies, and standardized operational protocols designed to deliver high-quality, cost-effective care. Major applications of IDNs include population health management, chronic disease management, preventive care initiatives, and the provision of specialized medical and surgical services, all coordinated through shared electronic health records and data analytics platforms. The primary benefits derived from IDNs include improved care coordination, enhanced patient satisfaction, reduction in preventable readmissions, and significant cost savings through economies of scale and optimized resource allocation. Key driving factors propelling the growth of the IDN market are the escalating demand for value-based care models, the increasing prevalence of chronic diseases requiring integrated management, advancements in health information technology, and the imperative to control spiraling healthcare expenditures while simultaneously improving quality of care delivery.

The Integrated Delivery Networks market is currently experiencing significant transformative business trends, largely driven by the imperative to shift from fee-for-service to value-based care models. This transition is compelling healthcare organizations to consolidate operations, invest heavily in digital health technologies, and focus on population health management to improve patient outcomes and reduce per capita costs. Strategic partnerships and mergers and acquisitions are becoming increasingly common as IDNs seek to expand their geographic reach, service offerings, and competitive advantage, creating a more integrated and efficient healthcare ecosystem capable of addressing complex patient needs comprehensively across the care continuum.

Regional trends indicate that North America continues to lead the IDN market, primarily due to advanced healthcare infrastructure, significant investment in health IT, and a proactive shift towards integrated care models, particularly within the United States. Europe is also showing strong growth, driven by government initiatives promoting integrated care and an aging population requiring coordinated health services. The Asia Pacific region is emerging as a rapidly expanding market, fueled by increasing healthcare expenditure, a growing awareness of integrated care benefits, and the adoption of digital health solutions, although challenges related to infrastructure and regulatory frameworks persist. Latin America, the Middle East, and Africa are also witnessing gradual growth as their healthcare systems mature and seek to emulate more efficient models.

Segmentation trends within the IDN market highlight a robust demand for integrated software solutions, particularly Electronic Health Records (EHRs), telehealth platforms, and predictive analytics tools, which form the technological backbone of coordinated care. Services, including consulting, implementation, and managed services, are also critical for optimizing IDN operations and ensuring effective system integration. From an application perspective, clinical applications focusing on patient management, diagnostics, and treatment coordination dominate, while administrative applications supporting billing, scheduling, and resource management are also gaining traction. End-user segments, particularly large hospital systems and Accountable Care Organizations (ACOs), are the primary adopters, emphasizing the growing need for comprehensive care delivery models.

Common user questions regarding AI's impact on Integrated Delivery Networks frequently revolve around its potential to revolutionize clinical decision-making, enhance operational efficiency, and personalize patient care, while also raising concerns about data privacy, job displacement, and the substantial initial investment required for implementation. Users often inquire about how AI can improve diagnostic accuracy, optimize resource allocation, automate routine tasks, and identify at-risk patient populations, seeking to understand the tangible benefits and return on investment. Furthermore, there is considerable interest in AI's role in advancing precision medicine and population health management within IDN frameworks, alongside questions about the ethical implications and regulatory challenges associated with deploying AI in sensitive healthcare environments.

The Integrated Delivery Networks market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities, all contributing to its evolving trajectory. A primary driver is the global shift towards value-based care models, which incentivize providers for patient outcomes rather than the volume of services, compelling healthcare organizations to integrate services for better coordination and efficiency. Concurrently, the increasing prevalence of chronic diseases worldwide necessitates comprehensive, long-term care management that IDNs are uniquely positioned to deliver. Furthermore, continuous technological advancements in health information technology, including electronic health records, telehealth, and data analytics, provide the foundational tools necessary for effective integration and coordinated care delivery, accelerating IDN adoption across diverse healthcare landscapes.

However, the market also faces considerable restraints that could impede its growth. The substantial upfront capital investment required for establishing and integrating complex IDN infrastructures, including IT systems and facility consolidations, poses a significant barrier for many organizations. Interoperability challenges among disparate legacy IT systems from various acquired entities within an IDN often lead to data silos and hinder seamless information exchange, complicating care coordination. Moreover, stringent data privacy and security regulations, alongside the inherent risks of cyberattacks on extensive patient data networks, demand robust and costly security measures, adding another layer of complexity and expense to IDN operations and management.

Despite these challenges, numerous opportunities exist to propel the IDN market forward. The rapid integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies promises to revolutionize diagnostic capabilities, predictive analytics for population health, and personalized medicine, significantly enhancing the value proposition of IDNs. The expansion of telehealth and remote patient monitoring services, accelerated by recent global health crises, presents a potent opportunity for IDNs to extend their reach, improve accessibility, and manage patient care more efficiently across broader geographic areas. Furthermore, the growing focus on personalized medicine and genomic healthcare allows IDNs to leverage their integrated data capabilities to deliver highly customized treatment plans, thereby improving efficacy and patient satisfaction, and cementing their role as leaders in advanced healthcare delivery.

The Integrated Delivery Networks market is comprehensively segmented to provide a detailed understanding of its diverse components, applications, and end-users, reflecting the multifaceted nature of integrated healthcare delivery. This segmentation helps in analyzing market dynamics, identifying high-growth areas, and understanding the specific needs of various stakeholders. The primary segments include categorization by Component, which delineates the technological and service-based elements of an IDN; by Application, which highlights the specific areas of healthcare operations where IDNs are deployed; by Delivery Model, showcasing the organizational structures adopted for integrated care; and by End-User, identifying the primary beneficiaries and implementers of IDN solutions and services.

The value chain for the Integrated Delivery Networks market is intricate, involving a series of interconnected activities and stakeholders that contribute to the delivery of comprehensive healthcare services. At the upstream level, the chain begins with technology providers specializing in electronic health records (EHR), telehealth platforms, predictive analytics, and cybersecurity solutions. These foundational technology vendors supply the crucial software and hardware infrastructure that enables data integration, communication, and operational efficiency across the IDN. Additionally, medical device manufacturers and pharmaceutical companies represent key upstream partners, supplying essential equipment, diagnostics, and medications that are integral to patient care within the integrated network, often requiring specific integration capabilities with IDN systems.

Moving downstream, the value created by upstream providers and the IDN's internal operations culminates in direct service delivery to patients and other end-users. This involves the provision of primary care, specialist consultations, diagnostic testing, surgical procedures, and post-acute care across various facilities such as hospitals, clinics, and long-term care centers. The integrated nature of the IDN ensures seamless transitions and coordinated care, aiming to improve patient outcomes and experiences. The distribution channel for IDN solutions and services is multifaceted, often relying on direct sales teams for large-scale enterprise software and system integration projects. Furthermore, strategic partnerships with third-party integrators, consultants, and value-added resellers play a crucial role in implementing complex IDN solutions, providing specialized expertise and support to healthcare organizations.

Direct distribution involves IDN entities directly procuring and implementing technologies and services from vendors or developing their in-house solutions. This approach allows for greater customization and control but requires significant internal resources and expertise. Indirect distribution channels encompass relationships with consulting firms that guide IDNs through technology selection and implementation, system integrators who specialize in connecting disparate systems, and managed service providers who handle ongoing IT operations. These indirect channels provide specialized knowledge and can accelerate the adoption and optimization of integrated systems, offering scalability and reducing the operational burden on IDNs, ultimately ensuring that advanced healthcare solutions reach the diverse patient population efficiently and effectively.

The primary potential customers for Integrated Delivery Networks are healthcare organizations seeking to enhance efficiency, improve patient outcomes, and transition to value-based care models. Large hospital systems and multi-hospital networks are among the foremost adopters, driven by the need to consolidate operations, standardize clinical protocols, and leverage economies of scale across multiple facilities. These entities benefit significantly from IDNs by achieving greater coordination in care delivery, reducing redundant services, and strengthening their negotiating position with payers and suppliers. The complexity of managing diverse patient populations and a wide array of specialized services makes IDN solutions indispensable for these large-scale providers.

Beyond traditional hospital systems, Accountable Care Organizations (ACOs) represent a crucial segment of potential customers. ACOs are formed by groups of doctors, hospitals, and other healthcare providers who come together voluntarily to give coordinated high-quality care to their Medicare patients. The inherent goal of an ACO – to provide patient-centered care while reducing unnecessary costs – aligns perfectly with the foundational principles and capabilities of an IDN. For ACOs, IDN frameworks offer the necessary infrastructure for comprehensive patient data management, population health analytics, and care coordination tools essential for meeting their performance metrics and achieving shared savings goals. This synergy makes IDNs a vital enabler for ACOs striving for both quality and cost-effectiveness in healthcare delivery.

Furthermore, large physician groups, community health centers, and governmental health agencies also stand as significant potential customers. Physician groups are increasingly forming larger networks to better manage patient panels, share resources, and negotiate with payers, finding IDN models beneficial for streamlining administrative tasks and enhancing clinical collaboration. Community health centers, often serving underserved populations, can leverage IDNs to improve access to comprehensive care, including preventive services and chronic disease management, by integrating various community resources. Governmental health agencies, tasked with public health initiatives and managing vast healthcare systems, look to IDNs to implement efficient, standardized, and widespread healthcare delivery models that can serve a large populace while ensuring quality and controlling costs across public sector healthcare facilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1,250.7 Billion |

| Market Forecast in 2032 | USD 2,350.6 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | UnitedHealth Group, Kaiser Permanente, Ascension Health, Providence St. Joseph Health, CommonSpirit Health, Sutter Health, Trinity Health, Baylor Scott & White Health, Advocate Aurora Health, Cleveland Clinic, Mayo Clinic, Intermountain Healthcare, Mount Sinai Health System, Partners HealthCare (now Mass General Brigham), Tenet Healthcare, HCA Healthcare, Community Health Systems, Humana, CVS Health (Aetna), Optum |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Integrated Delivery Networks market is characterized by a sophisticated array of digital solutions designed to facilitate seamless data exchange, enhance care coordination, and optimize operational efficiencies across diverse healthcare settings. Central to this landscape are Electronic Health Records (EHR) and Electronic Medical Records (EMR) systems, which serve as the backbone for consolidating patient information, ensuring its accessibility across all points of care within an IDN. These systems are continuously evolving, incorporating advanced features for clinical decision support, secure messaging, and interoperability with external platforms, thereby enabling a holistic view of the patient journey and supporting collaborative care models effectively. The robust functionality of modern EHR/EMR systems is paramount for IDNs seeking to standardize patient data and improve clinical workflows.

Beyond foundational record-keeping, the IDN market heavily leverages telehealth and remote patient monitoring technologies. Telehealth platforms facilitate virtual consultations, remote diagnostics, and patient education, significantly expanding access to care and reducing the burden on physical facilities. Remote patient monitoring devices, often integrated with EHRs, allow for continuous tracking of vital signs and other health metrics for patients with chronic conditions, enabling proactive interventions and reducing hospital readmissions. These technologies are crucial for IDNs focused on population health management and providing convenient, accessible care options, especially for geographically dispersed or underserved populations. The ability to monitor patients outside traditional clinical settings enhances continuous engagement and improves long-term health outcomes.

Furthermore, advanced data analytics, artificial intelligence (AI), and machine learning (ML) are transforming how IDNs manage and utilize vast amounts of clinical and operational data. Predictive analytics tools forecast disease outbreaks, identify at-risk patient populations, and optimize resource allocation, allowing IDNs to make data-driven strategic decisions. AI and ML applications enhance diagnostic accuracy, personalize treatment plans, and automate routine administrative tasks, thereby freeing up healthcare professionals to focus on direct patient care. Cloud computing provides the scalable and secure infrastructure necessary for hosting these complex systems and managing large datasets, while robust cybersecurity measures are essential to protect sensitive patient information from an increasing array of digital threats. The convergence of these technologies enables IDNs to achieve higher levels of clinical excellence, operational efficiency, and patient satisfaction, driving continuous innovation within the integrated healthcare ecosystem.

Integrated Delivery Networks (IDNs) are healthcare systems that consolidate various healthcare providers, facilities, and services under a unified organizational structure to deliver comprehensive, coordinated patient care, aiming for improved outcomes and efficiency.

For patients, IDNs offer improved care coordination, better access to diverse services, and potentially enhanced health outcomes. For providers, benefits include optimized resource utilization, reduced operational costs, standardized clinical protocols, and stronger negotiating power with payers.

Key challenges include high upfront capital investment, complex interoperability issues between disparate IT systems, stringent data privacy and security requirements, resistance to change from staff, and the difficulty of merging diverse organizational cultures.

Technological advancements, particularly in EHR/EMR systems, telehealth, AI/ML, and data analytics, are crucial drivers for IDNs, enabling seamless data exchange, enhancing clinical decision-making, improving patient engagement, and optimizing operational workflows across the integrated network.

The future outlook for the IDN market is positive, driven by the ongoing shift to value-based care, increasing adoption of digital health technologies like AI and telehealth, and the imperative for healthcare systems to deliver more efficient, patient-centric, and cost-effective care solutions globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.