ID : MRU_ 428118 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

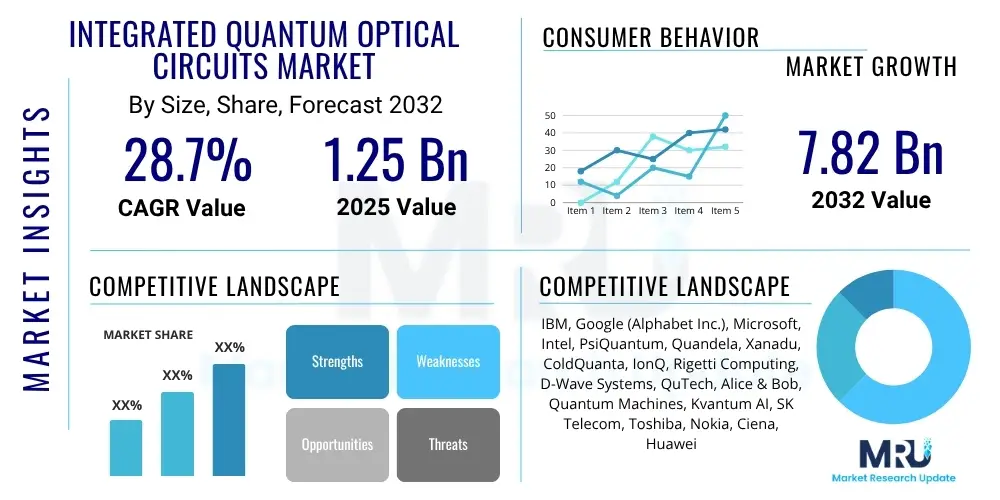

The Integrated Quantum Optical Circuits Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.7% between 2025 and 2032. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 7.82 Billion by the end of the forecast period in 2032.

Integrated Quantum Optical Circuits (IQOCs) represent a foundational technological advancement at the intersection of quantum mechanics and photonic integration, enabling the manipulation of light at a quantum level within a compact, scalable platform. These circuits are designed to process quantum information using photons as carriers, offering unparalleled speed, security, and efficiency compared to classical electronic circuits. Their architecture involves the integration of various optical components such as waveguides, modulators, detectors, and quantum light sources onto a single chip, facilitating the creation of robust and miniaturized quantum systems. The core innovation lies in their ability to maintain quantum coherence and entanglement of photons over extended pathways, crucial for advanced quantum applications. This integration not only reduces the physical footprint and power consumption but also enhances stability and performance, mitigating the challenges associated with bulk optical setups.

The product description of IQOCs encompasses a wide range of functionalities, from generating and manipulating single photons to implementing complex quantum gates and performing quantum measurements. These circuits leverage diverse material platforms, including silicon photonics, lithium niobate, and indium phosphide, each offering distinct advantages in terms of light confinement, electro-optic modulation, and compatibility with classical electronics. The design and fabrication processes involve advanced lithography and etching techniques to create precise optical pathways and resonant structures that guide and control photons with high fidelity. The sophistication of IQOCs enables them to perform tasks that are classically intractable, marking a significant paradigm shift in computational and communication capabilities. Their development is a testament to ongoing research and engineering efforts aimed at harnessing the full potential of quantum mechanics for practical technological solutions.

Major applications for Integrated Quantum Optical Circuits span critical sectors, most notably quantum computing, quantum communication, and quantum sensing. In quantum computing, IQOCs are vital for building scalable quantum processors capable of executing complex algorithms, offering a pathway to solve problems currently beyond the reach of supercomputers. For quantum communication, they are indispensable for secure information transfer through quantum key distribution (QKD) and for establishing future quantum internet infrastructure, ensuring unbreakable encryption. Furthermore, in quantum sensing and metrology, IQOCs enhance the precision of measurements for various physical quantities, finding utility in medical imaging, navigation, and environmental monitoring. The benefits derived from IQOCs include significant improvements in data security, computational power, and measurement accuracy, alongside reduced latency and energy consumption. Key driving factors propelling this market include massive investments in quantum research by governments and private entities, rapid advancements in photonic integration technologies, and the escalating demand for ultra-secure communication networks and high-performance computing solutions across industries. These factors collectively underscore the transformative potential and growing strategic importance of Integrated Quantum Optical Circuits.

The Integrated Quantum Optical Circuits (IQOCs) market is experiencing dynamic growth, driven by an escalating global interest in quantum technologies and substantial investments in research and development. Business trends indicate a surge in strategic collaborations between academic institutions, government agencies, and private corporations aimed at accelerating the commercialization of quantum solutions. Major technology companies are actively acquiring or partnering with quantum startups to integrate advanced quantum capabilities into their offerings, fostering an ecosystem ripe for innovation. There is a clear focus on overcoming the technical complexities associated with scaling quantum systems and achieving fault tolerance, prompting significant R&D expenditures in advanced material science and fabrication techniques. Furthermore, the market is characterized by a push towards standardization, as stakeholders recognize the necessity for interoperability to ensure broader adoption and seamless integration of IQOCs into existing technological infrastructures. This collaborative and competitive landscape is propelling rapid progress, transforming theoretical quantum concepts into tangible applications and market-ready products.

Regional trends highlight North America and Europe as the leading powerhouses in the IQOC market, primarily due to robust government funding initiatives, the presence of prominent research universities, and a high concentration of key players and technology innovators. Countries like the United States, Canada, the United Kingdom, Germany, and France are at the forefront, driving significant advancements in quantum computing and secure quantum communication infrastructure. Asia-Pacific, particularly China, Japan, and South Korea, is rapidly emerging as a critical region, demonstrating aggressive investment strategies and an ambitious national agenda to lead in quantum technologies. These countries are not only investing in fundamental research but also focusing on developing practical applications and building quantum-ready ecosystems. Latin America and the Middle East and Africa regions are still in nascent stages, but show growing interest with localized R&D efforts and international partnerships aimed at exploring the potential of quantum technologies for specific regional challenges. The global distribution of R&D centers and manufacturing capabilities is also shifting, reflecting a broad-based, international commitment to advancing IQOCs.

Segment trends within the IQOC market reveal a strong emphasis on material platforms that offer superior performance and scalability. Silicon photonics continues to be a dominant segment due to its compatibility with existing semiconductor manufacturing processes, allowing for cost-effective and large-scale integration. However, other materials like lithium niobate and indium phosphide are gaining traction for their distinct advantages in electro-optic modulation and quantum light generation, respectively, enabling specialized high-performance applications. The application segment is witnessing significant traction in quantum communication, driven by increasing cybersecurity concerns and the imperative for unhackable encryption methods. Quantum computing, while still in its early stages of commercialization, attracts the largest share of R&D investments, with a long-term vision for disruptive computational power. Quantum sensing and metrology are also experiencing growth, offering ultra-precise measurement capabilities for industries ranging from healthcare to defense. The market is thus diversifying, catering to a broad spectrum of needs while continuously innovating across its foundational components and applications to realize the full potential of integrated quantum optics.

Common user questions regarding AI's impact on Integrated Quantum Optical Circuits (IQOCs) frequently revolve around how artificial intelligence can accelerate their design and manufacturing, enhance their performance, and contribute to the broader quantum ecosystem. Users are keen to understand if AI can help overcome current challenges like error correction, scalability, and thermal management, while also exploring the potential for AI-driven quantum algorithm optimization and the synthesis of novel quantum materials. Concerns often surface about the integration complexity, the need for specialized AI expertise in quantum domains, and the ethical implications of intertwining two highly advanced and potentially transformative technologies. The prevailing expectation is that AI will act as a powerful catalyst, streamlining the development pipeline for IQOCs and unlocking unprecedented capabilities, ultimately speeding up the journey towards practical quantum advantage across various applications, from complex drug discovery to financial modeling and secure communication protocols.

The Integrated Quantum Optical Circuits (IQOCs) market is propelled by a robust set of drivers, primarily centered around the increasing global demand for advanced quantum technologies. A significant driver is the unparalleled quest for enhanced computational power, with quantum computing promising to solve problems intractable for classical supercomputers, thereby necessitating the development of scalable and stable quantum processors built on IQOCs. Concurrently, the escalating need for ultra-secure communication in an increasingly digital world fuels the demand for quantum communication technologies, particularly quantum key distribution (QKD), where IQOCs offer compact and efficient solutions. Furthermore, substantial investments by governments and private sectors in quantum research and development, coupled with growing national strategic interests in quantum supremacy, provide critical funding and infrastructure for market growth. Rapid advancements in photonic integration techniques, alongside breakthroughs in quantum material science, are continually expanding the capabilities and manufacturability of IQOCs, further accelerating their adoption and market expansion across various high-tech sectors.

Despite the optimistic outlook, several significant restraints challenge the widespread adoption and commercialization of Integrated Quantum Optical Circuits. The prohibitively high development and manufacturing costs associated with quantum technologies, particularly the specialized fabrication facilities and intricate processes required for IQOCs, act as a major barrier for entry and scalability. Technical complexities inherent in maintaining quantum coherence, achieving high fidelity in quantum operations, and integrating diverse quantum components onto a single chip pose substantial engineering hurdles. A critical restraint is the acute shortage of a skilled workforce, encompassing quantum physicists, photonic engineers, and specialized technicians, which impedes research progress and limits deployment capabilities. Moreover, the nascent stage of standardization across different quantum platforms and material systems creates interoperability challenges, hindering seamless integration and broad market acceptance. The environmental sensitivity of quantum devices, often requiring cryogenic temperatures and vibration isolation, adds to operational costs and complexity, restricting the practical deployment of IQOCs outside specialized laboratory settings.

Opportunities for growth within the IQOC market are vast and multifaceted, emerging from the continuous innovation in quantum science and engineering. The exploration of new quantum algorithms and applications, extending beyond initial use cases in computing and communication, presents significant avenues for market expansion into areas like drug discovery, materials science, and artificial intelligence optimization. Strategic collaborations and partnerships between established technology giants, agile quantum startups, and academic research institutions are fostering a dynamic ecosystem, accelerating technological advancements and facilitating knowledge transfer. Ongoing efforts in miniaturization and performance improvements, driven by advances in nanofabrication and novel material integration, promise to make IQOCs more compact, efficient, and versatile. The burgeoning field of quantum sensing and metrology, with its potential for ultra-precise measurements in various industries from medical diagnostics to geological surveys, offers substantial opportunities for specialized IQOC solutions. As global digital transformation continues, the expansion of IQOCs into new industrial sectors such as automotive, finance, and energy, seeking quantum-enhanced solutions for complex problems, further underscores the immense market potential. These interwoven dynamics of drivers, restraints, and opportunities shape a complex yet highly promising future for the Integrated Quantum Optical Circuits market.

The Integrated Quantum Optical Circuits market is comprehensively segmented to provide a detailed understanding of its diverse components, material platforms, application areas, and end-user industries. This segmentation helps in analyzing market dynamics, identifying growth opportunities, and understanding the competitive landscape. Each segment represents distinct technological approaches or market demands, contributing uniquely to the overall growth trajectory of quantum optical technologies. The diverse nature of quantum applications requires specialized circuit designs and material choices, driving the need for granular market analysis across these categories. Understanding these distinctions is crucial for stakeholders to tailor their product development, marketing strategies, and investment decisions effectively, navigating the complexities of this rapidly evolving high-technology domain.

The value chain for the Integrated Quantum Optical Circuits (IQOCs) market is complex, beginning with the foundational upstream segment focused on raw material procurement and specialized component manufacturing. This initial stage involves the sourcing of high-purity semiconductor materials such as silicon, lithium niobate, indium phosphide, and gallium arsenide, which are critical for various photonic platforms. Key players in this segment include chemical and materials suppliers, as well as specialized foundries capable of producing optical-grade wafers and substrates with extreme precision. Furthermore, the development and manufacturing of discrete optical components like advanced lasers, single-photon detectors, and modulators, often requiring custom designs and fabrication processes, form an essential part of the upstream activities. Research and development institutions also play a pivotal role here, contributing innovative material science and fundamental component designs that feed into the production pipeline. The quality and availability of these foundational elements directly impact the performance, scalability, and cost-effectiveness of the final integrated quantum optical circuits.

Moving further along the value chain, the core manufacturing and integration phase encompasses the design, fabrication, and assembly of the integrated quantum optical chips themselves. This highly specialized segment involves advanced nanofabrication techniques, including lithography, etching, and thin-film deposition, to create precise photonic structures on the chosen material platforms. Companies specializing in photonic integrated circuit (PIC) design, quantum circuit engineering, and advanced packaging solutions are central to this stage. These entities are responsible for integrating various optical and electronic components onto a single chip, ensuring quantum coherence and operational fidelity. Rigorous testing and characterization of the fabricated circuits are also crucial at this stage to ensure they meet the stringent performance requirements for quantum applications. The complexity of these processes often necessitates significant capital investment in cleanroom facilities and highly skilled personnel, making this a high-barrier-to-entry segment of the value chain.

The downstream segment of the IQOC value chain focuses on the distribution, system integration, and deployment of quantum optical circuits into end-user applications. This involves converting the bare IQOCs into functional quantum systems, such as quantum computers, quantum communication devices, or advanced quantum sensors. System integrators play a vital role here, designing the complete hardware and software stacks that incorporate the IQOCs, along with cryogenic cooling, control electronics, and user interfaces. Distribution channels can be direct, where IQOC manufacturers sell directly to large enterprises, government agencies, or research institutions that have the in-house expertise to integrate these components. Alternatively, indirect channels involve specialized distributors or value-added resellers who provide integration services and support to a broader range of end-users who may lack the specific technical capabilities. The final stage involves providing ongoing technical support, maintenance, and software updates to ensure the sustained performance and evolution of deployed quantum optical systems, catering to the diverse and demanding requirements of the aerospace, healthcare, IT & telecommunications, and financial sectors. This intricate interplay across upstream material suppliers, core manufacturers, and downstream integrators defines the robust and evolving market for integrated quantum optical circuits.

The Integrated Quantum Optical Circuits (IQOCs) market targets a diverse array of potential customers across various high-tech and strategically critical sectors, driven by the unique advantages these circuits offer in quantum information processing, secure communication, and ultra-precise sensing. At the forefront are government agencies and defense organizations, which are increasingly investing in quantum technologies for national security applications, including unhackable communication networks, advanced cryptography, and enhanced surveillance capabilities. Their demand stems from the imperative to maintain a technological edge and protect sensitive data from emerging cyber threats. Research institutions and academic bodies also constitute a significant customer segment, as they are actively involved in fundamental quantum research, developing new algorithms, and prototyping future quantum applications, requiring state-of-the-art IQOCs for their experimental setups and theoretical validations. These institutions often serve as incubators for innovation, driving the early adoption and refinement of quantum optical technologies.

Another prominent group of potential customers comprises large technology companies and IT & telecommunications giants. These enterprises are exploring IQOCs to enhance their cloud computing infrastructure with quantum capabilities, improve data center efficiency, and develop next-generation communication networks that offer superior speed and security. Their interest is rooted in competitive advantage, aiming to offer quantum-as-a-service (QaaS) or integrate quantum-safe solutions into their existing product portfolios. The financial services sector is also emerging as a key end-user, seeking to leverage quantum computing for complex financial modeling, risk analysis, fraud detection, and optimizing high-frequency trading strategies that require immense computational power and data processing speed. The ability of IQOCs to accelerate these computationally intensive tasks is a significant draw, promising transformative improvements in efficiency and accuracy within a highly competitive industry.

Furthermore, the healthcare and pharmaceutical industries represent a substantial market for IQOCs, primarily for advanced drug discovery, personalized medicine, and medical imaging applications. Quantum simulations enabled by IQOCs can drastically reduce the time and cost associated with developing new drugs by accurately modeling molecular interactions and protein folding. In medical imaging, the enhanced sensitivity and resolution offered by quantum sensors can lead to earlier and more precise diagnoses. The automotive sector is also showing interest, particularly in the development of advanced sensors for autonomous vehicles that require high precision and robustness, and for securing in-car communication systems. The aerospace sector is investigating IQOCs for navigational systems that are immune to GPS spoofing and for secure satellite communications. As quantum technology matures, these diverse end-users are poised to drive substantial demand for Integrated Quantum Optical Circuits, underpinning a broad spectrum of innovation and strategic advantage across industries.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2032 | USD 7.82 Billion |

| Growth Rate | 28.7% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | IBM, Google (Alphabet Inc.), Microsoft, Intel, PsiQuantum, Quandela, Xanadu, ColdQuanta, IonQ, Rigetti Computing, D-Wave Systems, QuTech, Alice & Bob, Quantum Machines, Kvantum AI, SK Telecom, Toshiba, Nokia, Ciena, Huawei |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Integrated Quantum Optical Circuits (IQOCs) market is underpinned by a dynamic and rapidly evolving technology landscape, characterized by continuous innovation in material science, fabrication processes, and quantum engineering principles. At its core, photonic integration remains a crucial technology, enabling the miniaturization and scalable fabrication of complex optical circuits on a single chip, leveraging techniques originally developed for classical silicon photonics but adapted for quantum coherence. This allows for the high-density integration of various passive and active optical components, such as waveguides, couplers, splitters, modulators, and single-photon detectors, significantly reducing the footprint and increasing the stability of quantum systems. Advancements in wafer-scale manufacturing and packaging are also vital, facilitating cost-effective mass production and robust protection of sensitive quantum components from environmental interference. These processes ensure that IQOCs can transition from laboratory prototypes to commercially viable products, meeting the rigorous demands of industrial applications while maintaining quantum performance at scale.

Key technological advancements also include the development of novel material platforms optimized for quantum applications. While silicon photonics offers scalability due to its compatibility with CMOS processes, research into alternative materials like lithium niobate, indium phosphide, and superconducting materials is expanding the functional capabilities of IQOCs. Lithium niobate, for instance, offers superior electro-optic modulation properties, crucial for high-speed quantum gates and reconfigurable circuits. Indium phosphide is preferred for on-chip light sources and detectors due to its direct bandgap. Furthermore, the integration of quantum emitters, such as quantum dots and color centers in diamond, directly into photonic circuits is a transformative technology, enabling the on-chip generation of high-quality single photons and entangled photon pairs, which are fundamental building blocks for quantum computation and communication. These material-specific innovations are crucial for tailoring IQOCs to specific quantum tasks, optimizing for metrics such as photon indistinguishability, entanglement fidelity, and operational speed, pushing the boundaries of what is achievable in quantum optics.

Beyond material and fabrication, the technological landscape of IQOCs is deeply intertwined with advancements in auxiliary quantum technologies. Cryogenic systems are often indispensable for maintaining the ultra-low temperatures required by certain quantum components, such as superconducting single-photon detectors and some qubit architectures. Advanced control electronics and sophisticated software platforms are essential for precise manipulation of quantum states, implementing complex quantum algorithms, and managing the vast amounts of data generated by quantum experiments. Moreover, the synergy between classical computing and quantum hardware is increasingly important, with hybrid quantum-classical architectures emerging to leverage the strengths of both paradigms. Technologies like cold atom systems, while not directly integrated into IQOCs, inform fundamental quantum physics and sensing applications that may eventually interface with integrated optical platforms. The ongoing research into error correction codes and fault-tolerant quantum computing is also a critical technological area, addressing the inherent fragility of quantum information and paving the way for truly robust and scalable quantum optical processors, signifying a holistic approach to advancing the entire quantum technology ecosystem.

Integrated Quantum Optical Circuits are miniaturized photonic devices that manipulate light at a quantum level on a single chip, utilizing photons to process and transmit quantum information. They integrate various optical components such as waveguides, modulators, and detectors, offering enhanced scalability, stability, and efficiency for quantum applications compared to bulk optical systems.

The primary applications of IQOCs include quantum computing, where they enable scalable quantum processors; quantum communication, facilitating ultra-secure quantum key distribution and the future quantum internet; and quantum sensing & metrology, providing highly precise measurements for diverse fields like medical imaging and navigation.

Common materials used in IQOCs include silicon photonics (for CMOS compatibility and scalability), lithium niobate (for strong electro-optic effects), indium phosphide (for active components like lasers and detectors), gallium arsenide (for quantum dot integration), and silica (for low-loss waveguides). Emerging superconducting materials are also being explored for integration with superconducting qubits.

Key challenges include high development and manufacturing costs, significant technical complexities in achieving quantum coherence and scalability, a shortage of skilled quantum engineers and physicists, lack of standardization across different quantum platforms, and the environmental sensitivity of quantum devices often requiring cryogenic operating conditions.

AI is significantly impacting IQOCs by accelerating design automation and optimization, enhancing simulation accuracy, improving error correction and mitigation, and optimizing quantum algorithms for specific hardware. AI also aids in the discovery of novel quantum materials and the intelligent control of complex quantum experiments, thereby speeding up the overall development and deployment of quantum optical circuits.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.