ID : MRU_ 429394 | Date : Nov, 2025 | Pages : 242 | Region : Global | Publisher : MRU

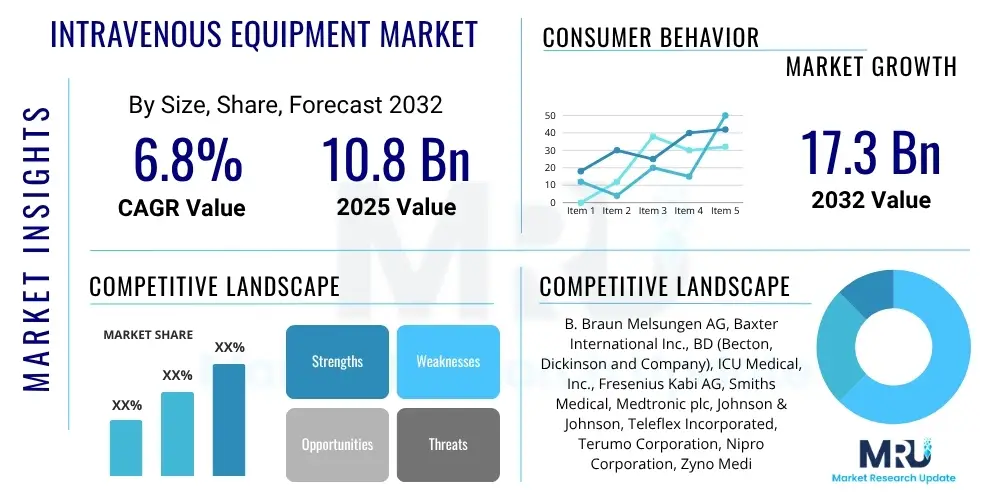

The Intravenous Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 10.8 Billion in 2025 and is projected to reach USD 17.3 Billion by the end of the forecast period in 2032.

The Intravenous (IV) Equipment Market encompasses a comprehensive array of medical devices and solutions vital for the direct administration of fluids, medications, nutrients, and blood products into a patient's circulatory system. This critical sector of healthcare technology includes fundamental components such as sophisticated infusion pumps, diverse IV administration sets, various types of intravenous catheters, and a wide range of specialized IV solutions. These products are indispensable across the entire spectrum of medical environments, playing a pivotal role in hospitals, specialized clinics, evolving home care settings, and emergency medical services, ensuring the provision of rapid, precise, and highly effective therapeutic interventions when oral administration is not feasible or sufficiently expeditious. The core functionality of intravenous delivery systems is to bypass the digestive system, allowing for immediate systemic availability of therapeutic agents and vital fluids, which is crucial for managing acute conditions, providing ongoing hydration, and delivering essential nutritional support.

The primary benefits inherent in the utilization of intravenous equipment are multifaceted, extending from ensuring rapid drug action and achieving highly precise dosage control to facilitating the administration of substances that cannot be effectively absorbed through oral routes. These advantages contribute significantly to enhanced patient outcomes and improved overall care efficacy, particularly in critical care scenarios and for patients requiring long-term treatments. The sustained and robust growth trajectory of the intravenous equipment market is fundamentally underpinned by several compelling driving factors. These include the escalating global prevalence of chronic diseases such as cancer, diabetes, and cardiovascular conditions, which frequently necessitate prolonged and consistent intravenous therapies. Furthermore, the rapidly expanding global geriatric population, inherently more susceptible to multiple comorbidities and requiring sustained medical interventions, significantly contributes to the demand for these essential medical devices. The increasing volume of complex surgical procedures performed worldwide also drives market expansion, as these interventions invariably require meticulous perioperative fluid management and precise medication delivery via IV access. Lastly, continuous technological advancements, particularly in the development of smart pumps and safer catheter designs, alongside the burgeoning trend towards patient-centric home healthcare models that rely heavily on portable and user-friendly IV equipment for extended patient management outside traditional clinical settings, further propel market growth and innovation.

The Intravenous Equipment Market is currently undergoing significant transformation, marked by dynamic business trends centered on technological innovation, strategic industry collaborations, and an intensified focus on enhancing patient safety and operational efficiencies across diverse healthcare settings. A prominent business trend involves the rapid development and adoption of smart infusion pumps, which incorporate advanced connectivity features, predictive analytics capabilities, and sophisticated dose error reduction systems. These innovations are specifically designed to mitigate medication errors, improve precision in drug delivery, and streamline clinical workflows, thereby addressing critical challenges in patient care. Concurrently, the market is experiencing a notable trend towards consolidation, with larger, established players strategically acquiring specialized companies that offer niche products or advanced technological solutions. These acquisitions aim to expand product portfolios, enhance technological capabilities, and strengthen market penetration, particularly within the highly competitive infusion pump and IV catheter segments, driving a more concentrated market structure.

From a regional perspective, mature markets such as North America and Europe continue to hold dominant positions within the global Intravenous Equipment Market. This sustained dominance is attributable to their well-established and sophisticated healthcare infrastructures, high rates of adoption for advanced medical technologies, substantial healthcare expenditures, and stringent regulatory environments that prioritize patient safety and innovation. In stark contrast, the Asia Pacific (APAC) region is rapidly emerging as a high-growth market, distinguished by its accelerating pace of healthcare infrastructure development, increasing per capita healthcare expenditure, and a burgeoning patient population. These factors collectively create a fertile ground for market expansion and increased demand for IV equipment. Furthermore, countries within Latin America and the Middle East & Africa (MEA) are also exhibiting considerable growth potential, driven by improving economic conditions, government initiatives aimed at modernizing healthcare facilities, and a rising awareness regarding advanced medical treatments.

Analyzing market segmentation reveals distinct trends that are shaping the competitive landscape. The demand for advanced infusion pumps, particularly smart pumps equipped with integrated safety features, comprehensive drug libraries, and seamless data management capabilities, is experiencing significant and sustained uptake. This surge is driven by a strong emphasis on preventing medication errors and improving patient safety protocols. Simultaneously, the market for various types of IV catheters, including both peripheral and central venous catheters, is undergoing substantial expansion. This growth is predominantly propelled by the increasing global incidence of hospital-acquired infections (HAIs), which has spurred intensive research and development efforts into designing innovative antimicrobial and safety-engineered catheter designs that minimize infection risks. Moreover, the home healthcare segment is witnessing remarkable growth, fueled by a growing societal preference for receiving long-term care and therapy outside traditional hospital environments. This shift necessitates the development of more portable, user-friendly, and technologically advanced IV equipment specifically tailored for home use. These converging business, regional, and segment-specific trends collectively underscore a vibrant and expanding market, poised for continuous innovation and strategic evolution in response to global healthcare needs and technological advancements.

The strategic integration of Artificial Intelligence (AI) into the Intravenous Equipment Market is set to catalyze a transformative shift in patient care, promising to significantly enhance the precision, safety, and operational efficiency of IV therapy delivery. Healthcare providers and end-users are intensely interested in understanding how AI can be leveraged to dramatically minimize medication administration errors, precisely optimize dosage regimens based on individual patient parameters, predict potential complications before they manifest, and autonomously streamline numerous administrative and logistical tasks associated with IV therapy management. There is a strong collective desire for AI-powered solutions capable of intelligently monitoring real-time infusion parameters, providing immediate alerts for critical events such as occlusions or disconnections, and ensuring seamless integration with existing electronic health records (EHRs) and hospital information systems. This integration aims to create a more cohesive, intelligent, and proactive healthcare ecosystem, thereby reducing manual oversight and improving overall patient outcomes. Furthermore, a significant expectation revolves around AI's capacity to profoundly contribute to the advancement of personalized medicine, enabling the development of highly tailored IV treatment plans that are dynamically adjusted based on individual patient data, physiological responses, and genetic profiles, leading to optimized therapeutic efficacy.

Despite the immense potential, common user questions and concerns frequently address critical aspects such as the robustness of data security and patient privacy protocols when handling sensitive medical information within AI systems. There are also ethical considerations surrounding the autonomous decision-making capabilities of AI in critical care settings, the cost-effectiveness of implementing and maintaining sophisticated AI-powered IV systems, and the imperative need for rigorous validation protocols to ensure the unwavering reliability and accuracy of AI-driven interventions. The overarching themes articulated by users underscore a strong desire for AI to function as an indispensable decision-support tool, not as a replacement for human clinical judgment, fundamentally transforming the conventional approach to IV administration into a highly intelligent, predictive, and intensely patient-centric intervention. This transition is expected to lead to unprecedented levels of safety, efficiency, and individualized care within the intravenous therapy domain, profoundly reshaping how medical fluids and medications are delivered.

The Intravenous Equipment Market operates within a dynamic environment significantly shaped by a complex interplay of driving forces, inherent restraints, promising opportunities, and broader impactful factors that collectively dictate its growth trajectory and evolutionary path. Foremost among the key drivers is the escalating global prevalence of chronic diseases, including but not limited to cancer, diabetes, and various cardiovascular conditions. These debilitating ailments frequently necessitate regular and often long-term intravenous therapies for medication administration, fluid management, and nutritional support, thereby creating a sustained and increasing demand for reliable IV equipment. Furthermore, the rapidly expanding global geriatric population, which is inherently more susceptible to developing multiple comorbidities and requiring continuous medical attention, significantly fuels the need for IV equipment across both acute care and long-term care facilities. The increasing global volume of complex surgical procedures also directly correlates with a heightened requirement for meticulous perioperative fluid management and precise medication delivery via intravenous routes, further stimulating market expansion. Lastly, continuous and rapid technological advancements in medical device manufacturing, particularly in the realm of smart pumps and innovative catheter designs, are enhancing safety, efficiency, and user-friendliness, thereby acting as a powerful market accelerator.

Despite these robust growth drivers, the market faces several formidable restraints that temper its expansion. A primary concern revolves around the inherent risks associated with IV administration, which include the potential for hospital-acquired infections (HAIs), local site complications such as phlebitis and extravasation, and other adverse patient outcomes. These complications not only pose significant health risks to patients but also contribute to increased healthcare costs and extended hospital stays, prompting a continuous need for safer devices. Additionally, the market is constrained by increasingly stringent regulatory frameworks and protracted approval processes for new medical devices across various jurisdictions. These rigorous regulations often result in substantial delays in market entry for innovative products and necessitate considerable investment in compliance, thereby impacting development timelines and costs. Moreover, the relatively high acquisition costs associated with advanced infusion pumps and specialized, technologically enhanced catheters can serve as a significant barrier to widespread adoption, particularly in healthcare systems with limited budgets or in developing economies, restricting access to cutting-edge IV technologies.

Conversely, the Intravenous Equipment Market is brimming with substantial opportunities that promise future growth and innovation. Emerging economies, characterized by their rapidly developing healthcare infrastructures, increasing per capita healthcare expenditure, and expanding access to medical services, represent highly lucrative and untapped markets for IV equipment manufacturers. The ongoing and accelerated development of next-generation smart infusion pumps, which integrate advanced features like dose error reduction systems, seamless wireless connectivity, and robust Electronic Medical Record (EMR) integration capabilities, offers a compelling pathway to unparalleled improvements in patient safety and clinical efficiency. Furthermore, the burgeoning global trend towards personalized medicine, which tailors treatments to individual patient needs, and the significant expansion of home infusion therapy services, are creating entirely new avenues for the development and adoption of specialized, portable, and user-friendly IV equipment. Broader impact forces, such as the evolving healthcare reimbursement landscape, which increasingly emphasizes value-based care models and demonstrable patient outcomes, compel manufacturers to innovate solutions that not only reduce complications but also enhance overall therapeutic efficacy. The continuous development of advanced biocompatible materials for catheters, coupled with the profound integration of Internet of Things (IoT) technologies and Artificial Intelligence (AI) for real-time monitoring, predictive analytics, and proactive intervention, are also transformative factors poised to redefine the future of intravenous care, creating a complex yet opportunity-rich market environment.

The Intravenous Equipment Market is meticulously segmented across several critical dimensions, providing a granular and comprehensive understanding of its intricate structure, underlying dynamics, and diverse operational facets within the expansive healthcare ecosystem. This detailed approach to segmentation is crucial for stakeholders, as it enables a precise and nuanced analysis of prevailing market trends, facilitates the accurate identification of high-growth segments and emerging opportunities, and supports robust strategic planning for market entry, product development, and resource allocation. The primary segmentation categories are inherently designed to capture the full breadth of the market: by product type, which delineates the specific medical devices and therapeutic solutions integral to IV therapy; by application, which identifies the various clinical scenarios and medical conditions where these devices are predominantly utilized; and by end-user, which pinpoints the key healthcare settings and professional groups that are the ultimate consumers and beneficiaries of intravenous equipment.

Each distinct market segment exhibits unique characteristics, growth patterns, and influencing factors, largely driven by continuous technological advancements, evolving patient demographics, changing disease prevalence, and the dynamic landscape of clinical practices and guidelines. For instance, innovations in smart pump technology primarily influence the product type segment, while the rising incidence of chronic diseases significantly impacts the application segment, driving demand for long-term infusion therapies. Understanding these distinct and interconnected segments is paramount for various market participants. For manufacturers, it is essential for tailoring their product offerings to meet specific clinical needs and preferences, optimizing their research and development investments, and crafting effective marketing strategies. For healthcare providers, such an analysis informs optimal procurement strategies, ensuring the acquisition of equipment that aligns with their patient populations and operational efficiencies. For market analysts and investors, it offers an invaluable framework for accurately forecasting future market trajectories, identifying potential investment opportunities, and assessing the competitive landscape with greater precision, thereby ensuring informed decision-making across the entire value chain of the intravenous equipment market.

The value chain for the Intravenous Equipment Market represents a sophisticated and interconnected series of activities, beginning with upstream raw material sourcing and culminating in the end-use of specialized medical products, designed to ensure safety, efficacy, and widespread availability. The upstream segment of this value chain is characterized by the procurement of high-quality, medical-grade raw materials. This includes specialized polymers and plastics essential for the manufacturing of tubing, catheters, and administration sets, along with precision-engineered stainless steel for needles and various metal components. Additionally, advanced electronic components are sourced for the sophisticated internal mechanisms of infusion pumps, and pharmaceutical-grade chemicals are procured for the formulation of intravenous solutions. Crucially, component manufacturers specialize in producing intricate pump mechanisms, incorporating advanced safety features, and developing connectivity modules, all of which are pivotal for the functionality and safety of the final product. At this foundational stage, strict adherence to global quality control standards and stringent regulatory requirements is absolutely paramount to prevent contamination, ensure biocompatibility, and guarantee the structural integrity of all components, laying the groundwork for reliable and safe medical devices.

Moving downstream, the distribution and ultimate end-use of intravenous equipment form the subsequent critical phases of the value chain. Manufacturers typically employ a multi-channel distribution strategy, leveraging both direct sales forces and an extensive network of authorized distributors. Direct sales engagement is frequently utilized for major institutional clients, such as large hospital systems and academic medical centers, particularly for high-value and technologically advanced products like smart infusion pumps that require specialized installation, comprehensive training, and ongoing technical support. This direct approach allows manufacturers greater control over product messaging, branding, and the cultivation of long-term customer relationships. Concurrently, a robust network of authorized distributors plays a crucial role in reaching a broader and more diverse market, including smaller clinics, retail pharmacies, and the rapidly expanding segment of home healthcare providers. The complexity of these distribution channels often varies depending on the product type, with more specialized and regulated devices demanding a more controlled and direct pathway to market, while standard consumables may utilize broader, more efficient indirect channels.

The efficiency and effectiveness of the entire distribution network are vital for ensuring the timely and uninterrupted supply of these essential medical resources to end-users across diverse geographical regions. Both direct and indirect distribution channels are indispensable for maintaining widespread product availability, responsiveness to evolving market demands, and delivering comprehensive post-purchase support. The ultimate beneficiaries and primary purchasers of intravenous equipment are a wide array of healthcare entities, including general and specialized hospitals, outpatient clinics, ambulatory surgical centers, home healthcare agencies, emergency medical services providers, and long-term care facilities. The procurement decisions made by these end-users are influenced by a multitude of factors, such as the paramount importance of patient safety features, the overall cost-effectiveness of the equipment over its lifecycle, the ease of use and ergonomic design, seamless compatibility with existing Electronic Medical Record (EMR) systems, and strict adherence to established clinical guidelines and regulatory mandates. The seamless functioning of the entire value chain, from the initial sourcing of raw materials to efficient distribution and comprehensive post-purchase support, directly impacts patient outcomes, operational efficiencies, and overall healthcare costs, underscoring the critical necessity of robust supply chain management and collaborative partnerships among all stakeholders involved in the intravenous equipment market.

The Intravenous Equipment Market caters to a diverse and expansive array of potential customers, all of whom are critical healthcare entities requiring reliable, safe, and efficient methods for delivering fluids, medications, and nutrients directly to patients. Hospitals represent the largest and most significant segment of these potential customers, encompassing a wide spectrum of institutions including general hospitals, specialized hospitals (e.g., oncology, cardiology, pediatric), and academic medical centers. These facilities utilize an extensive range of IV equipment daily across numerous departments, including emergency rooms, operating theaters, intensive care units, general wards, and specialized clinics. Hospitals demand high volumes of consumable products, a broad assortment of catheter types to address diverse patient needs, and advanced infusion pumps capable of managing complex patient conditions with precision and safety. The sheer scale of operations and the critical nature of care provided in hospitals drive a consistent and substantial demand for the latest and most dependable IV technologies.

Beyond the traditional hospital framework, specialized clinics, such as oncology treatment centers, dialysis clinics, and cardiology outpatient facilities, also constitute a substantial and growing segment of potential buyers. These clinics rely heavily on IV equipment for specific diagnostic procedures, the meticulous administration of chemotherapy agents, and the long-term management of chronic diseases requiring regular intravenous therapies. The procurement drivers for clinics often emphasize efficiency, patient comfort during routine treatments, and the integration of equipment with specialized treatment protocols. The demand from these specialized settings is characterized by a need for equipment that is both highly effective for targeted treatments and also streamlined for quick patient turnover, while maintaining the highest safety standards to protect vulnerable patient populations receiving ongoing care.

Furthermore, the rapidly expanding landscape of home healthcare services and ambulatory surgical centers (ASCs) represents another critical and burgeoning customer segment within the intravenous equipment market. Home care agencies and individual patients managing chronic conditions in their homes are increasingly in need of user-friendly, portable, and highly reliable IV equipment for sustained long-term therapy, nutritional support, and medication administration. This segment places a premium on devices that offer ease of use, robust patient education support, and effective remote monitoring capabilities, enabling safe and effective care outside clinical environments. Ambulatory Surgical Centers (ASCs) are key consumers of IV equipment for perioperative fluid management and anesthesia administration during outpatient surgical procedures, where equipment must facilitate rapid patient turnover, ensure stringent safety protocols, and minimize recovery times. Additionally, long-term care facilities, rehabilitation centers, and emergency medical services (EMS) providers consistently procure a broad spectrum of intravenous equipment for ongoing patient care, maintaining hydration, and delivering immediate life-saving interventions in critical situations. Each of these diverse customer segments possesses unique procurement criteria, specific clinical demands, and varying preferences for certain features, compelling manufacturers to continually innovate and diversify their product lines to cater effectively to the distinct needs across the entire continuum of healthcare delivery.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 10.8 Billion |

| Market Forecast in 2032 | USD 17.3 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | B. Braun Melsungen AG, Baxter International Inc., BD (Becton, Dickinson and Company), ICU Medical, Inc., Fresenius Kabi AG, Smiths Medical, Medtronic plc, Johnson & Johnson, Teleflex Incorporated, Terumo Corporation, Nipro Corporation, Zyno Medical, Moog Inc., Argon Medical Devices, Vygon S.A., Ambu A/S, Advanced Medical Solutions Group plc, Chengdu Fuli Technology Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Intravenous Equipment Market is in a continuous state of evolution, driven by relentless technological advancements aimed at fundamentally enhancing patient safety, improving clinical efficiency, and ultimately reducing the overall costs associated with healthcare delivery. A pivotal development that has profoundly reshaped this landscape is the widespread proliferation of smart infusion pumps. These cutting-edge devices integrate an array of advanced features, including comprehensive drug libraries equipped with dose error reduction systems (DERS), robust wireless connectivity capabilities, and seamless integration with Electronic Health Records (EHRs). These intelligent pumps are meticulously designed to proactively prevent medication errors by flagging potentially unsafe doses or administration rates, thereby significantly bolstering patient outcomes and mitigating adverse drug events. The inherent connectivity features facilitate real-time data transfer, empowering clinicians to remotely monitor infusion parameters, access critical patient data, and contribute valuable information for ongoing quality improvement initiatives and predictive analytics, ushering in an era of data-driven IV therapy management.

Another crucial area of relentless innovation within the IV equipment market lies in advanced IV catheter technology, with a concerted focus on improving insertion success rates, drastically reducing the pervasive risk of infections, and significantly enhancing patient comfort throughout the duration of therapy. This encompasses the ongoing development of state-of-the-art safety-engineered peripheral intravenous catheters (PIVCs) that incorporate sophisticated needle-stick prevention mechanisms, specialized anti-microbial coatings designed to effectively mitigate catheter-related bloodstream infections (CRBSIs), and novel materials engineered for extended dwell times, thereby reducing the frequency of catheter changes and associated complications. Furthermore, the strategic integration of advanced imaging technologies, most notably ultrasound guidance for IV insertion procedures, is dramatically improving first-attempt success rates, particularly in challenging patient populations with difficult venous access. This not only reduces procedural pain and patient anxiety but also optimizes resource utilization within healthcare settings, marking a significant stride towards more efficient and patient-friendly IV access protocols.

Beyond the significant advancements in hardware, the pervasive digital transformation sweeping through the global healthcare industry is profoundly influencing the intravenous equipment landscape. The increasing adoption of Internet of Things (IoT) sensors for continuous, real-time monitoring of infusion parameters, coupled with concurrent tracking of patient physiological responses, is becoming increasingly prevalent. These sophisticated sensor networks provide clinicians with an unparalleled, comprehensive view of a patient's status, enabling proactive intervention and timely adjustments to therapy. Artificial Intelligence (AI) and machine learning (ML) algorithms are being rigorously applied to analyze this vast and complex stream of data, intelligently identifying subtle patterns that can accurately predict potential complications, precisely optimize fluid balance, and even dynamically personalize medication regimens based on individual patient needs. For example, AI-driven systems can assist clinicians in determining optimal infusion rates or pinpointing patients at a higher risk of adverse events well in advance. Telemedicine and remote monitoring platforms are also gaining considerable traction and relevance, especially with the accelerated expansion of home infusion therapy services. These platforms empower healthcare providers to effectively oversee patients receiving IV therapy outside the traditional hospital environment, ensuring unwavering adherence to treatment plans and providing timely, critical support, thereby extending the reach of high-quality IV care beyond conventional boundaries. The strategic convergence of these advanced technologies is not merely making IV therapy safer and more efficient; it is fundamentally expanding its reach into novel care settings, ultimately fostering a more connected, data-driven, highly predictive, and intensely patient-centric approach to intravenous care globally.

Intravenous equipment's primary function is to deliver fluids, critical medications, essential nutrients, and vital blood products directly into a patient's bloodstream. This method ensures rapid absorption, systemic action, and precise control over therapeutic administration, making it indispensable for critical care, hydration, drug delivery, and nutritional support in diverse medical scenarios where oral routes are insufficient or inappropriate.

Smart infusion pumps significantly enhance patient safety through integrated dose error reduction systems (DERS), comprehensive drug libraries with pre-programmed limits, and seamless wireless connectivity to electronic health records (EHRs). These advanced features proactively minimize medication errors, ensure the accurate delivery of prescribed dosages, and provide real-time alerts for any deviations from established parameters, thereby substantially improving patient outcomes and reducing adverse events.

The growth of the IV equipment market is propelled by several robust factors, including the escalating global prevalence of chronic diseases requiring long-term therapies, the rapidly expanding geriatric population necessitating continuous medical care, an increasing global volume of surgical procedures, the growing demand for convenient and accessible home healthcare services, and continuous technological advancements in IV administration devices that enhance safety and efficiency, all collectively driving a heightened demand for reliable intravenous therapies worldwide.

Key challenges confronting the IV equipment market include the persistent risk of complications such as hospital-acquired infections (HAIs), local site extravasation, and phlebitis, stringent and complex regulatory requirements that delay product innovation and market entry, the high acquisition and maintenance costs associated with advanced IV equipment, and a widespread shortage of skilled healthcare professionals adequately trained in efficient and safe IV administration and management techniques across various clinical settings.

Artificial intelligence (AI) is profoundly impacting IV equipment by enabling more precise and personalized dosage calculations, significantly reducing medication errors through predictive analytics, facilitating real-time and continuous monitoring of infusions with anomaly detection, and offering highly tailored treatment protocols based on individual patient data. AI also plays a crucial role in optimizing inventory management and ensuring seamless integration with broader hospital information systems, leading to enhanced overall efficiency and elevated patient safety standards in intravenous therapy.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.