ID : MRU_ 429638 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

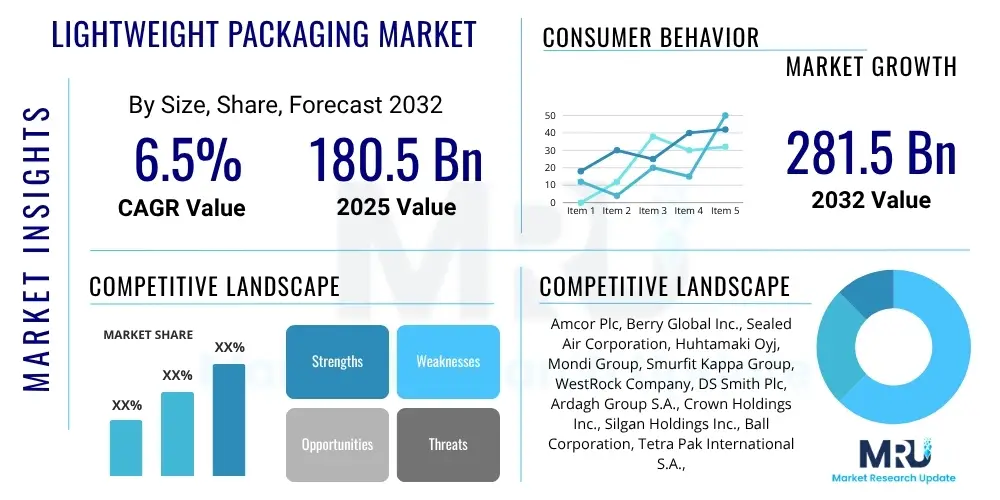

The Lightweight Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at $180.5 Billion in 2025 and is projected to reach $281.5 Billion by the end of the forecast period in 2032.

Lightweight packaging fundamentally represents a strategic advancement in material science and design, aimed at significantly reducing the weight and volume of packaging materials without compromising the critical functions of product protection, preservation, and presentation. This innovative approach encompasses a broad spectrum of packaging formats, from flexible films and pouches to rigid bottles and cartons, all engineered to utilize fewer raw materials per unit while maintaining or enhancing performance. The core objective is to minimize the environmental footprint associated with packaging production, transportation, and disposal, thereby contributing substantially to global sustainability goals and resource conservation. This shift is driven by a collective industry effort to optimize resource utilization and reduce carbon emissions across the value chain, responding to both regulatory pressures and evolving consumer expectations for eco-friendly products.

The product description of lightweight packaging involves an array of advanced materials and design principles. Common materials include high-performance plastics such as polyethylene terephthalate (PET), polypropylene (PP), and polyethylene (PE), often engineered into thinner gauges or multi-layered structures to achieve superior barrier properties and strength. Optimized paper and paperboard, including corrugated and folding cartons, are designed with improved fiber strength and structural integrity while reducing overall board weight. Lighter-gauge metals, particularly aluminum, are used for beverage cans and food containers, and emerging bioplastics like polylactic acid (PLA) and polyhydroxyalkanoates (PHA) are gaining traction for their renewable origins and compostability. Major applications span a broad spectrum of industries, including food and beverages, pharmaceuticals, personal care and cosmetics, and various industrial goods. The primary benefits derived from adopting lightweight packaging include significant cost savings in raw materials and logistics, reduced carbon footprint, enhanced brand image through sustainability initiatives, and improved operational efficiencies in manufacturing and transport.

The robust growth of the lightweight packaging market is propelled by multifaceted and deeply interconnected driving factors. Paramount among these is the escalating global imperative for environmental sustainability, fueled by stringent government regulations, such as bans on single-use plastics and mandates for recycled content, and increasing consumer demand for eco-friendly products. Economic benefits also serve as powerful drivers; lightweight packaging directly translates to significant cost reductions in raw material procurement, manufacturing processes, and especially in transportation, where lower package weight reduces fuel consumption and logistics expenses. The relentless expansion of e-commerce further fuels this demand, as efficient, protective, and minimal-weight packaging is crucial for optimizing shipping costs and delivery speed. Advances in material science and packaging technology, enabling the creation of high-performance, ultra-light materials, continue to underpin and accelerate market innovation and adoption.

The Lightweight Packaging Market is poised for substantial expansion, underpinned by an overarching global transition towards resource efficiency and environmental stewardship. Emerging business trends highlight a profound commitment to circular economy principles, manifested through a heightened emphasis on designing for recyclability, integrating post-consumer recycled (PCR) content, and accelerating the development of bio-based and compostable packaging materials. Automation and digitalization of packaging lines are gaining traction, not only to enhance production efficiency but also to optimize material usage with greater precision. Furthermore, the persistent surge in e-commerce necessitates packaging solutions that are not only robust enough to protect products during complex shipping logistics but also light enough to significantly reduce freight costs and carbon emissions, thereby acting as a critical enabler for online retail growth.

Regional dynamics are playing a pivotal role in shaping the market’s trajectory. The Asia Pacific region is anticipated to demonstrate the most vigorous growth, propelled by its enormous population base, rapid industrialization, burgeoning middle class, and the explosive expansion of digital commerce in countries such as China, India, and Southeast Asian nations. This region is witnessing substantial investments in manufacturing capabilities and infrastructure, driving the demand for efficient and sustainable packaging. Europe, characterized by its mature regulatory landscape and a strong emphasis on environmental protection, continues to lead in innovative sustainable lightweight packaging solutions, driven by stringent directives like the EU Packaging and Packaging Waste Directive. North America is characterized by high consumer demand for convenience and a growing corporate commitment to sustainability, fostering advancements in both flexible and rigid lightweight formats and substantial investments in advanced packaging technologies.

Segmentation trends within the lightweight packaging market reveal distinct areas of growth and innovation. Flexible packaging, encompassing pouches, films, and bags, consistently holds the largest market share due to its inherent material efficiency, versatility, and cost-effectiveness, making it ideal for a vast array of food, beverage, and personal care products. Within materials, plastics, particularly PET and PP, remain dominant due to their excellent barrier properties and design flexibility, although thereatorial shift towards sustainable plastic alternatives, including thinner gauges and those with higher recycled content. Paper and paperboard solutions are also experiencing a resurgence, driven by their recyclability and renewable nature, particularly in carton and corrugated lightweight applications. The food and beverage sector remains the foremost end-use segment, continually innovating to meet consumer demands for fresh, safe, and conveniently packaged products with extended shelf life. The pharmaceutical and personal care industries are also increasing their adoption, valuing the dual benefits of product protection and enhanced brand image through sustainable packaging choices.

Common user questions regarding the impact of Artificial Intelligence on the Lightweight Packaging Market frequently explore how AI can revolutionize packaging design, streamline manufacturing processes, enhance supply chain efficiency, and ultimately bolster sustainability efforts. Users are keenly interested in the practical applications of AI, such as its capacity for predictive analytics in demand forecasting, intelligent automation in production lines, and the potential for personalized packaging solutions. Concerns often include the initial capital investment required for AI implementation, the need for specialized technical expertise, and how to effectively integrate AI with existing legacy systems. Nevertheless, there are strong expectations for AI to deliver tangible benefits, including significant waste reduction, optimized material usage, improved quality control, and a more responsive and resilient supply chain for lightweight packaging. This indicates a strong desire among stakeholders to understand AI's transformative potential across the entire packaging lifecycle.

AI's influence extends across multiple facets of the lightweight packaging ecosystem, fundamentally altering how materials are conceived, produced, and managed. In the design phase, generative AI tools can rapidly iterate through thousands of design variations, identifying optimal geometries and material compositions that drastically reduce weight while maintaining or improving structural integrity and protective qualities. This minimizes trial-and-error, accelerates time-to-market for innovative lightweight designs, and ensures material efficiency from conception. Furthermore, machine learning algorithms can analyze vast datasets from past packaging performance, environmental conditions, and consumer feedback to predict the ideal material properties and design features required for specific product applications, ensuring both lightweight characteristics and robust protection.

Within manufacturing and supply chain operations, AI plays a crucial role in enhancing efficiency and sustainability. AI-powered predictive maintenance systems can monitor packaging machinery, forecasting potential breakdowns and enabling proactive interventions, thereby reducing downtime and material waste. Automated quality inspection systems, leveraging computer vision and deep learning, can identify defects in lightweight materials and finished packages with unparalleled accuracy and speed, ensuring consistent product quality and preventing the distribution of substandard packaging. For the supply chain, AI algorithms optimize logistics routes, inventory management, and warehousing, reducing the energy consumption associated with transport and storage. By accurately forecasting demand, AI helps prevent overproduction and subsequent waste of lightweight materials, further aligning with the market's sustainability objectives. The integration of AI also facilitates the development of smart packaging, where embedded sensors and identifiers can track products in real-time, providing data that can inform future lightweight design iterations and enhance consumer engagement.

The Lightweight Packaging Market is propelled by several key drivers, primarily the escalating global emphasis on sustainability and environmental protection. Consumers, brand owners, and governments are increasingly demanding packaging solutions that reduce waste, conserve resources, and lower carbon emissions. This demand is further amplified by stringent regulations imposing extended producer responsibility and promoting recycling initiatives. Cost efficiency is another significant driver, as lighter packaging translates to reduced material consumption, lower transportation costs due to decreased weight, and optimized storage, offering substantial economic benefits across the supply chain. The burgeoning e-commerce sector also necessitates lightweight, durable, and protective packaging to minimize shipping expenses and product damage, while continuous advancements in material science and packaging technologies enable the creation of increasingly efficient and high-performance lightweight alternatives.

Despite these compelling drivers, the market faces notable restraints and simultaneously presents significant opportunities. A primary restraint includes ensuring that lightweight materials maintain sufficient structural integrity and barrier properties for sensitive products, alongside high initial investment costs for advanced manufacturing technologies and the complexity of recycling certain multi-layered lightweight structures. However, significant opportunities exist in the development and commercialization of innovative sustainable materials such as advanced bioplastics, compostable polymers, and high-performance recycled content. The expansion into emerging markets, where rapid industrialization and increasing consumer purchasing power are driving demand for packaged goods, offers substantial growth prospects. Furthermore, integrating smart packaging technologies, such as RFID tags and QR codes for enhanced traceability and consumer engagement, presents a unique opportunity to add value beyond mere weight reduction, unlocking new possibilities for ultralight, highly protective packaging.

The Lightweight Packaging Market is profoundly influenced by a complex interplay of impact forces. Environmental impact forces are paramount, with escalating global concerns over climate change, plastic pollution, and resource depletion directly shaping public opinion, corporate strategies, and regulatory agendas. This pressure drives demand for packaging with minimal ecological footprint. Regulatory impact forces, including evolving national and international legislation on plastic bans, recycled content mandates, and extended producer responsibility (EPR) schemes, are compelling industries to accelerate their adoption of lightweight and more sustainable packaging alternatives to ensure compliance. Economic impact forces, such as global supply chain disruptions, fluctuating energy prices, and increasing operational costs, consistently push companies to seek cost-effective solutions. Finally, technological impact forces, encompassing breakthroughs in material science, additive manufacturing, and digital design tools, enable the creation of increasingly efficient, high-performance lightweight packaging designs, continuously evolving the market's capabilities.

The Lightweight Packaging Market is meticulously segmented across various dimensions to provide a detailed understanding of its complex structure, growth drivers, and evolving preferences within different categories. This comprehensive analysis allows stakeholders to identify specific market niches, assess competitive landscapes, and formulate targeted strategies for development and expansion. The segmentation typically considers the primary material used in packaging, ranging from diverse plastic polymers to paper, glass, and metal, reflecting the wide array of options available for weight reduction. Furthermore, the distinction between flexible and rigid packaging types highlights the functional differences and application suitability of various lightweight solutions. Finally, the categorization by end-use industry provides crucial insights into how different sectors, such as food and beverage, pharmaceuticals, and personal care, are adopting and innovating with lightweight packaging to meet their distinct product protection, logistical, and brand requirements, underscoring the market’s versatility and broad applicability.

Segmentation by material is crucial as it dictates the inherent properties, cost structure, and recyclability of lightweight packaging. Plastics, particularly PET, PP, and PE, dominate due to their excellent barrier properties, flexibility, and cost-effectiveness when engineered for minimal thickness. These materials are widely used in bottles, films, and pouches for numerous consumer goods. Paper and paperboard segments, including corrugated and folding cartons, are experiencing a resurgence driven by their renewable nature and recyclability, often optimized for strength-to-weight ratio in applications like food boxes and consumer product packaging. Glass and metal (aluminum, steel) also contribute to the lightweight market through design optimizations that reduce material usage while maintaining structural integrity, especially for beverages and high-value goods. The rapidly growing bioplastics segment, comprising materials like PLA and PHA, offers innovative, environmentally friendly alternatives that are both lightweight and derived from renewable sources, catering to increasing demand for sustainable options.

Further segmentation by type distinguishes between flexible and rigid packaging, each serving specific functions and market needs. Flexible packaging, encompassing pouches, films, wraps, and bags, is inherently lightweight due to its minimal material usage and conforms to product shapes, making it ideal for snacks, personal care refills, and pre-packaged meals. Its efficiency in transportation and storage, coupled with design versatility, drives its significant market share. Rigid packaging, although typically heavier than flexible options, is also undergoing lightweighting through design innovations in bottles, jars, containers, trays, and cans. This involves reducing wall thickness, optimizing structural geometry, and utilizing advanced lightweight materials to achieve substantial weight savings while maintaining the necessary protection, stackability, and shelf appeal for products ranging from beverages to cosmetics. The end-use industry segmentation then reveals the varied applications and specific demands across sectors like food & beverage (for freshness, safety, and convenience), pharmaceutical (for sterility, tamper-evidence, and patient safety), personal care (for brand aesthetics and eco-credentials), and industrial (for durability and logistics efficiency).

The value chain for the Lightweight Packaging Market is a complex and interconnected network that begins with the fundamental sourcing and processing of raw materials. This upstream segment is dominated by specialized chemical companies that produce polymers (such as PET, PP, PE), pulp and paper mills that supply paperboard, glass manufacturers, and metal producers. These entities are critical in developing and refining the base materials to meet the rigorous demands of lightweighting, which often includes engineering specific properties like improved strength-to-weight ratios, advanced barrier functionalities against gases and moisture, or enhanced compatibility with recycling streams. Innovation at this initial stage is paramount, focusing on sustainable sourcing, developing bio-based alternatives, and enhancing the intrinsic properties of materials to support reduced gauge and overall weight in final packaging applications. This stage sets the foundation for the entire value proposition of lightweight packaging.

Moving further along the value chain, midstream activities involve the extensive network of packaging converters and manufacturers. These are the companies that transform the raw materials into finished or semi-finished lightweight packaging products through a variety of sophisticated processes. This includes extrusion for films, injection molding for bottles and caps, blow molding for containers, thermoforming for trays, and advanced printing and laminating techniques. Packaging converters play a crucial role in design optimization, employing CAD/CAM software and simulation tools to create packaging structures that are both minimal in material use and robust in performance. Their expertise lies in balancing weight reduction with functional requirements such as product protection, shelf appeal, user convenience, and compliance with strict industry-specific regulations. Continuous investment in advanced manufacturing technologies, automation, and precision engineering is characteristic of this segment, ensuring high-volume production of consistently high-quality lightweight solutions.

The downstream segment of the value chain is composed of brand owners, co-packers, and fillers, who are the ultimate users of lightweight packaging for their diverse product portfolios. These stakeholders make critical purchasing decisions that directly influence the demand for specific lightweight solutions across industries like food and beverage, pharmaceuticals, and personal care. Their focus is on ensuring product integrity, maximizing shelf appeal, meeting consumer sustainability expectations, and optimizing their own supply chain costs. The distribution channel for lightweight packaging involves a multi-faceted approach. Large enterprise clients often engage in direct procurement relationships with packaging manufacturers to ensure custom solutions and economies of scale. Conversely, smaller businesses, or those requiring more diverse and specialized packaging options, frequently rely on indirect channels, utilizing distributors, wholesalers, and packaging brokers who provide a broader range of products, inventory management, and logistical support. The growing complexity of global supply chains, coupled with the exponential rise of e-commerce, increasingly emphasizes the necessity for efficient, agile, and strategically located distribution networks to ensure lightweight packaging materials and finished products reach end-users effectively and sustainably across various geographical markets.

Potential customers for lightweight packaging solutions represent an incredibly diverse and expansive array of industries, each driven by a shared imperative for increased efficiency, enhanced sustainability, and optimized operational costs. The food and beverage sector stands as the predominant end-user segment, encompassing multinational corporations producing everything from dairy products, juices, and carbonated drinks to snack foods, confectionery, and ready-to-eat meals. These clients are constantly seeking packaging innovations that not only extend product shelf life and ensure food safety but also offer consumer convenience, reduce transportation expenses for high-volume goods, and align with growing public demand for environmentally responsible packaging materials, making lightweight options indispensable for both flexible pouches and rigid bottles and cartons.

The pharmaceutical industry constitutes another critical customer base, where the adoption of lightweight packaging is driven by stringent regulatory requirements, the need for product integrity, and the high value-to-weight ratio of many medications. Pharmaceutical companies utilize lightweight blister packs, bottles, vials, and specialized sterile pouches to protect sensitive drugs, vaccines, and medical devices from contamination, degradation, and tampering. The benefits extend to reduced shipping costs for global distribution, an important factor in an industry with complex supply chains and a focus on patient safety and cost-effectiveness. The personal care and cosmetics sector also heavily relies on lightweight packaging, not only to reduce material consumption and meet sustainability targets but also to enhance product aesthetics and brand differentiation through innovative designs for lotions, shampoos, makeup, and perfumes, appealing directly to environmentally conscious consumers.

Beyond these major consumer-facing sectors, a wide range of industrial goods manufacturers are increasingly turning to lightweight packaging for its protective qualities and logistical advantages. This includes producers of automotive components, chemicals, building materials, and electronics, who seek durable yet lighter packaging solutions to reduce freight costs for bulk goods, improve handling efficiency, and minimize their overall environmental footprint throughout the supply chain. Furthermore, the burgeoning e-commerce sector represents a rapidly expanding and uniquely critical customer group. Online retailers and fulfillment centers require lightweight, robust, and often customizable packaging that can withstand the rigors of multi-leg shipping, protect products during transit, and simultaneously minimize dimensional weight charges, which are a significant cost factor in online logistics. In essence, any business involved in the manufacturing, distribution, or sale of physical products stands as a significant potential customer for lightweight packaging, as the inherent benefits of reduced weight translate directly into substantial economic advantages, operational efficiencies, and improved environmental performance across virtually all commercial activities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $180.5 Billion |

| Market Forecast in 2032 | $281.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amcor Plc, Berry Global Inc., Sealed Air Corporation, Huhtamaki Oyj, Mondi Group, Smurfit Kappa Group, WestRock Company, DS Smith Plc, Ardagh Group S.A., Crown Holdings Inc., Silgan Holdings Inc., Ball Corporation, Tetra Pak International S.A., UFlex Ltd., Sonoco Products Company, Coveris Holdings S.A., Constantia Flexibles Group GmbH, Aluflexpack AG, Greif, Inc., Printpack Inc., Gerresheimer AG, AptarGroup Inc., Pactiv Evergreen Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Lightweight Packaging Market is continuously shaped by a dynamic and evolving key technology landscape, primarily driven by relentless innovation aimed at significantly reducing material usage while simultaneously enhancing packaging performance and sustainability. Paramount among these advancements are breakthroughs in material science. This includes the development of next-generation polymers with superior strength-to-weight ratios, allowing for the creation of ultra-thin films and containers that maintain structural integrity. Innovations also extend to advanced barrier coatings and multi-layer co-extrusion technologies, which enable thinner material gauges to provide robust protection against moisture, oxygen, and light, critical for extending product shelf life without increasing package weight. Furthermore, the proliferation of bio-based and compostable polymers, alongside high-performance recycled content (e.g., PCR plastics), represents a significant technological frontier, addressing both weight reduction and the critical imperative for environmentally responsible end-of-life solutions, moving towards a more circular economy model.

Complementing material innovations are significant advancements in manufacturing and processing technologies that enable the precise and efficient production of lightweight packaging. Modern injection molding, blow molding, and thermoforming techniques have evolved to allow for unprecedented control over material distribution, enabling the creation of thinner walls, optimized geometries, and reduced material use in rigid packaging formats without compromising durability. Advanced extrusion processes for flexible films produce thinner yet stronger multi-layered structures. Automation and robotics on packaging lines are increasingly sophisticated, handling delicate lightweight materials at high speeds with precision, minimizing waste, and improving overall operational efficiency. Furthermore, the integration of digital manufacturing, including advanced computer-aided design (CAD) and simulation software, allows for virtual prototyping and optimization of lightweight designs, significantly shortening development cycles and reducing physical material consumption during the design phase.

Beyond the physical materials and manufacturing processes, the integration of smart packaging technologies is rapidly transforming the lightweight sector by adding enhanced functionality and intelligence. This encompasses the embedment of RFID tags (Radio Frequency Identification), NFC (Near Field Communication) chips, and sophisticated QR codes into lightweight packaging, enabling advanced product traceability throughout the supply chain, facilitating anti-counterfeiting measures, and fostering direct, interactive consumer engagement. Furthermore, advancements in integrated sensors allow for real-time monitoring of product conditions such as temperature, humidity, and freshness, providing crucial data that enhances product safety and reduces spoilage. These sensors are increasingly designed to be minimal in weight and seamlessly integrated into the packaging structure. These technological advancements collectively contribute to making packaging not only lighter and more sustainable but also significantly more functional, intelligent, and responsive, addressing the evolving demands of both industry stakeholders and informed consumers for high-performance, eco-friendly, and value-added packaging solutions.

The primary benefits of lightweight packaging include substantial cost reductions through decreased raw material consumption and lower transportation expenses due to reduced freight weight. It also significantly enhances environmental sustainability by minimizing carbon footprint, conserving resources, and promoting easier recyclability, aligning with global eco-friendly initiatives and consumer preferences.

The food and beverage sector is the most prominent end-user, utilizing lightweight packaging for freshness, convenience, and cost-effective distribution of high-volume products. The pharmaceutical industry heavily relies on it for product protection and reduced global shipping costs. Personal care and cosmetics also adopt it for brand appeal, sustainability, and material reduction, while e-commerce values it for optimal shipping efficiency and reduced dimensional weight charges.

Lightweight packaging contributes to sustainability by drastically reducing the amount of virgin raw materials needed for production, thus conserving natural resources. Its lower weight directly translates to decreased fuel consumption and greenhouse gas emissions during transport. Furthermore, many lightweight designs are engineered for improved recyclability or incorporate recycled and bio-based materials, supporting circular economy principles and reducing landfill waste.

Key challenges include ensuring that reduced material thickness maintains adequate product protection and barrier properties, requiring significant R&D. High initial investment costs for advanced manufacturing technologies and machinery pose a barrier. Additionally, the complexity of recycling certain multi-layered lightweight structures and volatile raw material prices remain significant operational and environmental hurdles for manufacturers.

AI is profoundly influencing lightweight packaging by enabling generative design for optimal material use and structural integrity, accelerating the development of innovative, ultra-light solutions. It powers predictive analytics for precise demand forecasting and supply chain optimization, minimizing waste and enhancing logistical efficiency. AI also drives automated quality control and facilitates the integration of smart packaging features, making future lightweight solutions more intelligent, sustainable, and responsive to market needs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.