ID : MRU_ 428619 | Date : Oct, 2025 | Pages : 246 | Region : Global | Publisher : MRU

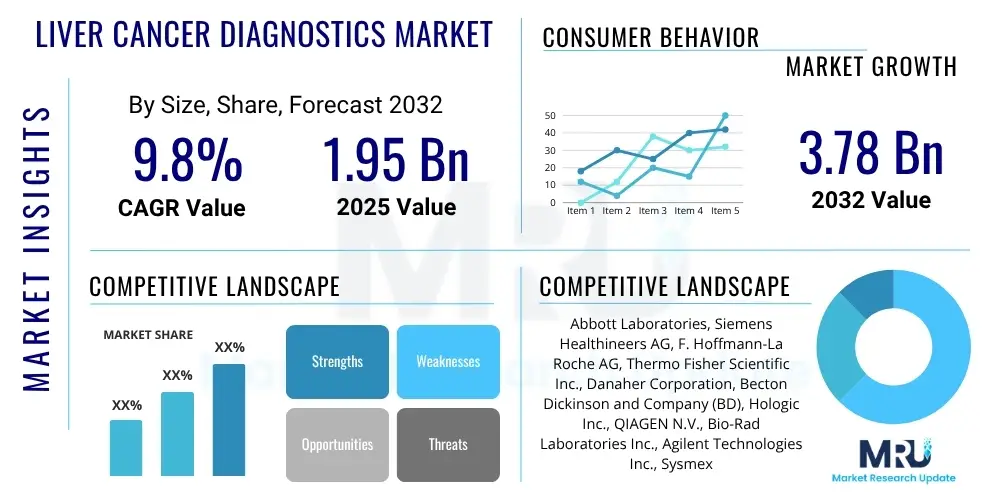

The Liver Cancer Diagnostics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2032. The market is estimated at USD 1.95 billion in 2025 and is projected to reach USD 3.78 billion by the end of the forecast period in 2032.

The Liver Cancer Diagnostics Market encompasses a broad range of technologies and services designed for the early detection, diagnosis, staging, and monitoring of hepatocellular carcinoma (HCC) and other primary liver cancers. This crucial segment of the healthcare industry addresses the growing global burden of liver cancer, a leading cause of cancer-related mortality worldwide. The products within this market include advanced imaging modalities such as ultrasound, computed tomography (CT), magnetic resonance imaging (MRI), and positron emission tomography (PET), alongside sophisticated biomarker tests, including alpha-fetoprotein (AFP) and emerging liquid biopsy panels. Furthermore, minimally invasive procedures like targeted biopsies (e.g., core needle biopsy, fine-needle aspiration) remain integral for definitive diagnosis and molecular profiling. Major applications span screening programs for at-risk populations (e.g., chronic hepatitis B/C patients, cirrhotic patients), confirmatory diagnosis of suspicious lesions, precise staging to guide treatment decisions, and continuous monitoring for disease recurrence or progression post-therapy. The primary benefits of these diagnostic advancements include significantly improving patient outcomes through earlier intervention, enabling more personalized and effective treatment strategies, reducing the need for invasive exploratory procedures, and enhancing the overall quality of life for individuals affected by liver cancer. Key driving factors propelling market expansion include the rising global incidence and prevalence of liver cancer, particularly in Asia Pacific, an aging population more susceptible to chronic liver diseases, continuous technological innovations in diagnostic tools, increased awareness campaigns, and substantial investments in research and development aimed at less invasive and more accurate diagnostic solutions. The demand for robust diagnostic pathways is further fueled by the imperative to differentiate malignant from benign liver lesions and to identify actionable mutations for targeted therapies, thereby reinforcing the market's critical role in modern oncology.

The Liver Cancer Diagnostics Market is experiencing robust growth, driven by an escalating global incidence of liver cancer, particularly hepatocellular carcinoma (HCC), coupled with significant advancements in diagnostic technologies. Key business trends underscore a strong emphasis on strategic partnerships, mergers, and acquisitions aimed at consolidating market share and leveraging synergistic technological capabilities, especially in artificial intelligence (AI) and machine learning (ML) integration for image analysis and biomarker discovery. Research and development investments are heavily concentrated on non-invasive diagnostic methods like liquid biopsies and highly specific molecular biomarkers to improve early detection rates and enhance prognostic accuracy. Furthermore, there there is a growing trend towards point-of-care testing solutions that promise to increase accessibility and reduce diagnostic turnaround times. Regionally, the Asia Pacific market is poised for exceptional growth, attributed to the high prevalence of chronic hepatitis infections (HBV and HCV) which are primary risk factors for liver cancer, rapidly improving healthcare infrastructure, and increasing disposable incomes supporting advanced diagnostic adoption. North America and Europe continue to represent substantial market shares due to established healthcare systems, significant R&D spending, and a large aging population with a high prevalence of metabolic risk factors. From a segmentation perspective, the imaging diagnostics segment, particularly advanced MRI and CT techniques, retains a dominant share due driven by their indispensable role in initial detection and staging. However, the molecular diagnostics segment, fueled by innovations in circulating tumor DNA (ctDNA) and microRNA (miRNA) detection, is projected to witness the fastest growth, propelled by its potential for non-invasive screening, early recurrence monitoring, and guiding precision medicine approaches. End-user trends indicate a sustained demand from hospital oncology departments and specialized diagnostic laboratories, with a burgeoning interest from research institutions and academic centers for novel biomarker validation and personalized diagnostic applications, all contributing to a dynamic and evolving market landscape.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Liver Cancer Diagnostics Market predominantly revolve around the potential for enhanced diagnostic accuracy, improved efficiency in image analysis, and the development of more personalized risk assessment tools. Common questions frequently explore how AI can assist in the early detection of subtle lesions, differentiate malignant from benign tumors with greater precision, and integrate diverse patient data points (imaging, clinical, genomic) for comprehensive diagnostic insights. There is significant interest in AI's role in automating repetitive tasks, thereby reducing radiologist workload and potentially mitigating human error. Concerns often include the reliability and interpretability of AI algorithms, the ethical implications of AI-driven diagnoses, data privacy and security, and the necessity for extensive validation studies to gain clinician trust and regulatory approval. Users also question the accessibility of advanced AI solutions, particularly in resource-limited settings, and the potential impact on the job roles of healthcare professionals. Overall, the prevailing sentiment is one of cautious optimism, acknowledging AI's transformative potential while seeking clarity on its practical implementation and long-term integration into clinical workflows.

AI is set to revolutionize liver cancer diagnostics by augmenting human capabilities, driving efficiency, and enabling previously unattainable levels of precision. Its applications extend from image interpretation to predictive analytics, promising to redefine the diagnostic pathway. Machine learning algorithms, trained on vast datasets of radiological images, pathology slides, and clinical records, can identify subtle patterns indicative of malignancy that might be missed by the human eye. This capability is particularly critical for early-stage liver cancer, where timely intervention significantly impacts patient prognosis. AI-powered systems can also analyze complex genomic and proteomic data from liquid biopsies to identify novel biomarkers, offering non-invasive screening and monitoring tools with enhanced specificity and sensitivity. The integration of AI tools is expected to streamline workflows in diagnostic labs and radiology departments, reducing turnaround times and potentially lowering the overall cost of diagnosis by optimizing resource allocation and minimizing unnecessary invasive procedures.

The integration of AI into liver cancer diagnostics presents profound opportunities for innovation, moving beyond simple image analysis to create truly intelligent diagnostic platforms. Beyond basic detection, AI algorithms are being developed to predict treatment response, stratify patient risk for recurrence, and recommend personalized therapeutic strategies based on a patient's unique molecular profile. These advanced capabilities are crucial for managing the heterogeneous nature of liver cancer, where one-size-fits-all approaches often fall short. Furthermore, AI can facilitate the aggregation and analysis of real-world evidence from electronic health records, accelerating the discovery of new insights into disease progression and treatment efficacy. While challenges related to data standardization, algorithm validation, and regulatory frameworks persist, the continuous evolution of AI technologies, coupled with increasing interdisciplinary collaboration between AI specialists, oncologists, and pathologists, indicates a promising trajectory for its widespread adoption and transformative impact on improving liver cancer patient care.

The Liver Cancer Diagnostics Market is significantly influenced by a confluence of interconnected drivers, restraints, and opportunities that collectively define its growth trajectory and competitive landscape. A primary driver is the alarming global increase in the incidence and prevalence of liver cancer, largely attributed to rising rates of chronic hepatitis B and C infections, non-alcoholic fatty liver disease (NAFLD), non-alcoholic steatohepatitis (NASH), and alcohol-related liver disease. The aging global population, which is more susceptible to these chronic conditions, further exacerbates the demand for effective diagnostic solutions. Technological advancements, particularly in advanced imaging techniques (e.g., contrast-enhanced ultrasound, multiparametric MRI) and molecular diagnostics (e.g., liquid biopsy, next-generation sequencing), represent another critical driver, offering improved accuracy, reduced invasiveness, and earlier detection capabilities. Growing awareness campaigns by governmental and non-governmental organizations regarding risk factors and the importance of early screening also contribute to market expansion. However, several restraints impede market acceleration, including the high cost associated with advanced diagnostic procedures and equipment, which can limit accessibility, especially in developing economies. The scarcity of skilled professionals, such as experienced radiologists and pathologists specializing in liver cancer, poses a significant challenge. Furthermore, the complexity of regulatory approval pathways for novel diagnostic assays and devices, coupled with issues pertaining to reimbursement policies, can hinder market entry and adoption. Despite these challenges, substantial opportunities abound, particularly in emerging economies with rapidly improving healthcare infrastructure and a large, underserved patient population. The increasing adoption of artificial intelligence and machine learning for image analysis and biomarker discovery offers a transformative opportunity to enhance diagnostic precision and efficiency. The development of companion diagnostics for targeted liver cancer therapies, alongside the growing emphasis on personalized medicine, creates new avenues for market growth. Moreover, the shift towards non-invasive diagnostic modalities, such as liquid biopsies for circulating tumor DNA (ctDNA) and circulating tumor cells (CTCs), presents a lucrative opportunity to redefine screening and monitoring paradigms. The cumulative impact of these forces underscores a dynamic market environment where innovation and strategic adaptation are crucial for sustainable growth and addressing the unmet clinical needs in liver cancer diagnosis.

The Liver Cancer Diagnostics Market is extensively segmented to provide a granular understanding of its diverse components and evolving dynamics. This segmentation allows for targeted market analysis, identifying high-growth areas and informing strategic decision-making for stakeholders across the diagnostic value chain. The market is primarily categorized by product type, application, and end-user, with further geographical segmentation highlighting regional disparities in disease prevalence, healthcare infrastructure, and diagnostic adoption rates. Understanding these segments is crucial for manufacturers to tailor their product offerings, for healthcare providers to optimize diagnostic workflows, and for investors to identify promising investment opportunities within this critical oncology diagnostics sector.

The value chain for the Liver Cancer Diagnostics Market is a complex ecosystem involving multiple stages, from initial research and development to the final delivery of diagnostic services to patients, with each stage adding significant value and contributing to the overall market efficiency and accessibility. The upstream segment primarily involves fundamental research into disease mechanisms, biomarker discovery, and the development of novel diagnostic technologies, where academic institutions, biotechnology firms, and pharmaceutical companies play pivotal roles. This stage also includes the sourcing and manufacturing of raw materials, such as reagents for molecular assays, components for imaging equipment, and specialized instruments, often supplied by a niche group of chemical and medical device manufacturers. Midstream activities encompass the development, manufacturing, and rigorous testing of diagnostic products, including imaging machines, immunoassay kits, PCR systems, and liquid biopsy platforms, followed by regulatory approval processes that ensure safety and efficacy. Key players in this stage are large medical device companies and specialized diagnostic kit manufacturers. The downstream segment focuses on the distribution and delivery of these diagnostic tools and services. Distribution channels are varied, including direct sales forces from manufacturers, third-party distributors, and increasingly, online procurement platforms, all aiming to reach end-users efficiently. Direct channels involve manufacturers selling directly to large hospitals or national health systems, allowing for closer client relationships and technical support. Indirect channels leverage regional distributors and wholesalers to penetrate broader markets, including smaller clinics and diagnostic laboratories. Finally, the ultimate delivery involves the use of these diagnostics by healthcare providers—hospitals, diagnostic laboratories, oncology clinics, and specialty centers—to screen, diagnose, stage, and monitor liver cancer patients. Effective collaboration across all these stages, from innovative research to efficient distribution and clinical application, is critical for enhancing diagnostic accuracy, reducing turnaround times, and ultimately improving patient outcomes in liver cancer management.

The primary potential customers and end-users of liver cancer diagnostic products and services are diverse, reflecting the broad spectrum of clinical settings and research environments involved in cancer care and discovery. Hospitals, particularly those with comprehensive cancer centers, gastroenterology departments, and radiology units, represent a significant customer segment. These institutions require a full range of diagnostic tools, from advanced imaging modalities like MRI and CT to pathology services for tissue biopsies and molecular testing capabilities. Standalone diagnostic laboratories and pathology centers are also crucial customers, as they often specialize in high-throughput biomarker testing, molecular diagnostics, and histopathological analysis, serving as referral sites for clinics and smaller hospitals. Oncology clinics, both public and private, frequently utilize diagnostic services for initial patient assessment, staging, and ongoing monitoring of treatment efficacy and disease recurrence. Furthermore, academic and research institutes constitute a vital segment, particularly for cutting-edge diagnostic technologies and novel biomarker assays, as they are actively involved in preclinical and clinical research to discover and validate new diagnostic markers and methods. Pharmaceutical and biotechnology companies also form a customer base, leveraging advanced diagnostics as companion diagnostics for their therapeutic agents, or for patient stratification in clinical trials. Given the rising global incidence of liver cancer, the increasing emphasis on early detection, and the continuous evolution of diagnostic technologies, these diverse end-users collectively drive the demand within the Liver Cancer Diagnostics Market, constantly seeking more accurate, less invasive, and more cost-effective solutions to improve patient management.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.95 billion |

| Market Forecast in 2032 | USD 3.78 billion |

| Growth Rate | 9.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Abbott Laboratories, Siemens Healthineers AG, F. Hoffmann-La Roche AG, Thermo Fisher Scientific Inc., Danaher Corporation, Becton Dickinson and Company (BD), Hologic Inc., QIAGEN N.V., Bio-Rad Laboratories Inc., Agilent Technologies Inc., Sysmex Corporation, Fujifilm Holdings Corporation, Canon Medical Systems Corporation, General Electric Company (GE Healthcare), Philips Healthcare, Exact Sciences Corporation, Guardant Health Inc., Illumina Inc., Quest Diagnostics Incorporated, LabCorp Holdings. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Liver Cancer Diagnostics Market is characterized by a dynamic and continuously evolving technology landscape, where innovation is central to improving detection accuracy, reducing invasiveness, and enabling personalized patient management. Advanced imaging technologies form a cornerstone of this landscape, with innovations in ultrasound (e.g., contrast-enhanced ultrasound for better lesion characterization), computed tomography (CT) with multi-detector arrays and perfusion imaging, and magnetic resonance imaging (MRI), particularly multiparametric MRI (mpMRI) with diffusion-weighted imaging (DWI) and hepatobiliary phase imaging, offering superior soft tissue contrast and functional information for lesion detection and characterization. Positron Emission Tomography (PET) scans, often combined with CT (PET-CT) or MRI (PET-MRI), provide crucial metabolic information for staging and assessing treatment response. Parallel to imaging advancements, the field of molecular diagnostics is rapidly expanding, driven by technologies such as next-generation sequencing (NGS) for comprehensive genomic profiling of tumor tissue, real-time polymerase chain reaction (RT-PCR) for detecting viral markers and specific mutations, and immunohistochemistry (IHC) for protein expression analysis. A particularly transformative area is liquid biopsy, which utilizes advanced techniques to analyze circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), microRNAs (miRNAs), and exosomes from peripheral blood samples. These non-invasive methods hold immense promise for early cancer detection, monitoring minimal residual disease, and tracking tumor evolution in real-time. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) algorithms is revolutionizing image analysis, pathology interpretation, and data integration, enhancing diagnostic precision and efficiency. AI-powered platforms are increasingly used to detect subtle lesions, differentiate benign from malignant tumors, and predict treatment response by analyzing complex datasets. Emerging technologies like proteomics and metabolomics are also gaining traction, offering new avenues for biomarker discovery and development. The convergence of these diverse technologies is creating a more comprehensive, accurate, and patient-friendly diagnostic ecosystem, driving the market towards more precise and personalized approaches to liver cancer diagnosis and management.

North America holds a substantial share in the Liver Cancer Diagnostics Market, primarily driven by a robust healthcare infrastructure, high prevalence of chronic liver diseases such as NAFLD and NASH stemming from lifestyle factors, significant healthcare expenditure, and a strong emphasis on early cancer detection and advanced treatment modalities. The region benefits from the presence of numerous key market players, extensive research and development activities, and favorable reimbursement policies for advanced diagnostic procedures. The U.S. leads the market in North America due to its high adoption of sophisticated diagnostic technologies, a large patient pool, and a proactive approach to oncology research and clinical trials. Canada also contributes significantly, with a growing awareness of liver cancer risk factors and increasing access to advanced diagnostic imaging and molecular testing facilities.

Europe represents another major market for liver cancer diagnostics, characterized by well-established healthcare systems, an aging population, and a rising incidence of liver cancer, particularly in countries with higher rates of hepatitis C infection and alcohol consumption. Countries like Germany, the UK, France, and Italy are at the forefront of adopting advanced diagnostic technologies and implementing national screening programs. The European market is further supported by collaborative research initiatives, significant funding for cancer research, and increasing patient access to innovative diagnostic tools through national health services. Emphasis on personalized medicine and precision diagnostics is also boosting the demand for molecular and genetic testing across the region.

The Asia Pacific (APAC) region is projected to witness the fastest and most significant growth in the Liver Cancer Diagnostics Market during the forecast period. This accelerated growth is primarily attributed to the exceptionally high prevalence of chronic hepatitis B and C infections, which are major risk factors for liver cancer, particularly in populous countries like China, India, and Southeast Asian nations. Rapid economic development, improving healthcare infrastructure, increasing awareness among the population and healthcare professionals, and a growing medical tourism sector are further propelling market expansion. Governments in APAC are increasingly investing in public health initiatives and cancer screening programs, leading to greater adoption of both traditional imaging and emerging molecular diagnostic techniques. Japan, with its advanced technological landscape and aging population, also plays a crucial role in driving innovation and market uptake in the region.

The Liver Cancer Diagnostics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2032, driven by increasing disease incidence and

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.