ID : MRU_ 430568 | Date : Nov, 2025 | Pages : 249 | Region : Global | Publisher : MRU

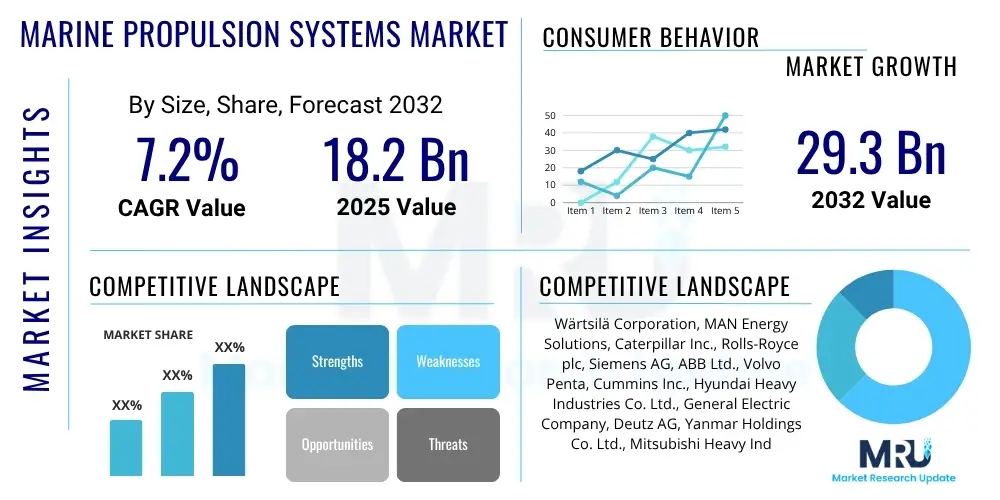

The Marine Propulsion Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2032. The market is estimated at USD 18.2 billion in 2025 and is projected to reach USD 29.3 billion by the end of the forecast period in 2032.

The Marine Propulsion Systems market encompasses a diverse range of technologies and components essential for propelling vessels across various marine applications. These systems provide the necessary thrust and maneuverability for ships, boats, and other maritime craft. They are fundamentally composed of prime movers like engines, motors, or turbines, coupled with transmission systems, shafts, and propulsive devices such as propellers, thrusters, or waterjets, all managed by sophisticated control systems. The market is dynamic, constantly evolving to meet stringent environmental regulations and demands for higher efficiency and reliability.

Products within this market range from conventional diesel engines and gas turbines to advanced electric, hybrid, and alternative fuel systems. Major applications span the entire maritime sector, including commercial shipping (cargo, tankers, bulk carriers), passenger vessels (cruise ships, ferries), naval ships (frigates, submarines), offshore support vessels (supply vessels, drilling rigs), and recreational boats. The primary benefits derived from these systems are reliable power delivery, enhanced operational efficiency, reduced fuel consumption, and increasingly, minimized environmental impact through lower emissions and noise levels. The overarching trend towards decarbonization and digitalization is significantly reshaping the landscape of marine propulsion.

Driving factors for this market's growth are multifaceted, propelled by the expansion of global trade, increasing maritime tourism, and growing investment in offshore energy exploration. Furthermore, the imperative to comply with increasingly stringent international environmental regulations, such as those set by the International Maritime Organization (IMO) regarding sulfur content and greenhouse gas emissions, is a crucial catalyst. Technological advancements, including the development of more efficient engines, hybrid solutions, and viable alternative fuels like LNG, methanol, ammonia, and hydrogen, are also pivotal in driving market expansion and innovation.

The Marine Propulsion Systems market is experiencing robust growth, primarily driven by the expansion of global trade, significant investments in maritime infrastructure, and the urgent need for sustainable shipping solutions. Business trends indicate a strong shift towards decarbonization, with a notable increase in the adoption of alternative fuel-powered vessels and hybrid-electric propulsion systems. Digitalization and automation are also key themes, enhancing operational efficiency, predictive maintenance capabilities, and vessel autonomy. Consolidation among key players and strategic collaborations are prevalent as companies seek to strengthen their technological offerings and market reach.

Regional trends highlight Asia-Pacific as a dominant force in shipbuilding and a significant consumer of marine propulsion systems, fueled by strong economic growth and expanding maritime trade routes. Europe continues to lead in innovation, particularly in the development and adoption of green technologies and advanced propulsion solutions, driven by stringent regional environmental policies. North America is characterized by substantial naval expenditure and investment in offshore energy exploration, which fuels demand for specialized and high-performance propulsion systems. Other regions, including Latin America, the Middle East, and Africa, show potential driven by resource extraction and expanding port infrastructure developments.

Segment trends underscore the burgeoning demand for propulsion systems compatible with alternative fuels, notably LNG, which has seen considerable uptake, and emerging fuels like methanol, ammonia, and hydrogen, which are gaining traction for future vessel designs. The electric and hybrid propulsion segments are also witnessing rapid growth due to their ability to reduce emissions and improve fuel efficiency, especially in coastal and harbor operations. Furthermore, advancements in propeller design and thruster technologies are contributing to enhanced hydrodynamic efficiency and maneuverability, catering to the evolving needs of various vessel types and operational profiles.

User inquiries regarding Artificial Intelligence (AI) in the Marine Propulsion Systems Market frequently revolve around its potential to optimize performance, enhance safety, and drive sustainability. Common questions include how AI can improve fuel efficiency, its role in predictive maintenance for propulsion components, the implications for autonomous vessel operation, and the challenges associated with integrating AI into complex marine engineering systems. There is also significant interest in the cybersecurity risks associated with increasingly connected and AI-driven propulsion systems, alongside the regulatory frameworks required to govern their deployment. The prevailing sentiment is one of cautious optimism, acknowledging AI's transformative potential while recognizing the complexities of implementation in a highly regulated and safety-critical environment.

The key themes emerging from user concerns and expectations center on leveraging AI for operational excellence and environmental compliance. Users anticipate AI will provide real-time data analysis to optimize engine performance, predict equipment failures before they occur, and facilitate more efficient route planning and speed optimization. The integration of AI for autonomous navigation and remote control capabilities is also a significant area of focus, promising reduced human error and enhanced operational safety. However, concerns persist regarding the reliability of AI systems in extreme marine conditions, the need for robust data infrastructure, and the ethical considerations surrounding autonomous decision-making in critical scenarios. Stakeholders are keen to understand how AI can genuinely contribute to decarbonization efforts, not just through efficiency gains but also by enabling the smarter management of alternative fuel systems.

The Marine Propulsion Systems market is fundamentally shaped by a confluence of driving forces, restraining factors, and emerging opportunities, all interacting with various impact forces. Key drivers include the consistent growth in global maritime trade, necessitating larger and more efficient fleets. Simultaneously, increasingly stringent environmental regulations imposed by the International Maritime Organization (IMO) and regional bodies are compelling shipowners to invest in cleaner and more sustainable propulsion technologies, such as hybrid, electric, and alternative fuel systems. Moreover, ongoing technological advancements in engine design, propeller efficiency, and control systems continuously push the boundaries of performance and fuel economy. Rising naval expenditure by countries aiming to modernize and expand their maritime defense capabilities also contributes significantly to market growth.

Despite these strong drivers, the market faces several notable restraints. The substantial initial investment costs associated with advanced propulsion systems, particularly those utilizing alternative fuels or complex hybrid configurations, often deter immediate widespread adoption. The inherent complexity of integrating new technologies into existing vessel designs and the associated infrastructure challenges, especially for bunkering alternative fuels like ammonia or hydrogen on a global scale, present significant hurdles. Furthermore, geopolitical uncertainties and fluctuating raw material prices can impact manufacturing costs and project timelines, adding an element of unpredictability to market planning and investment decisions.

Opportunities within the market are predominantly concentrated around the global drive for decarbonization, fostering the development and commercialization of zero-emission propulsion solutions. The increasing viability of alternative fuels, including LNG, LPG, methanol, ammonia, and hydrogen, alongside advancements in battery technology for full electric propulsion, presents lucrative avenues for innovation and market penetration. The trend towards autonomous shipping and smart vessel operations opens up new possibilities for AI-driven propulsion management and predictive maintenance. Additionally, the vast market for retrofitting existing fleets with more environmentally compliant and efficient propulsion systems offers substantial growth potential for manufacturers and service providers looking to extend the lifespan and improve the sustainability profile of older vessels. The combined effect of these forces creates a dynamic environment for continuous innovation and strategic adaptation within the marine propulsion sector.

The Marine Propulsion Systems market is comprehensively segmented to provide a detailed understanding of its diverse components and applications. This segmentation allows for targeted analysis of market dynamics, identification of key growth areas, and strategic planning for manufacturers, suppliers, and end-users. The market is typically broken down by propulsion type, the type of fuel utilized, various vessel applications, specific system components, and the end-user segments encompassing both original equipment manufacturers and the aftermarket.

Each segment presents unique growth trajectories and technological requirements. For instance, the propulsion type segment differentiates between conventional internal combustion engines and modern electric or hybrid systems, highlighting the shift towards cleaner technologies. Fuel type segmentation underscores the transition from traditional fossil fuels to alternative, lower-emission options. Application-based segmentation helps in understanding the varying demands from commercial, naval, offshore, and recreational sectors, each with distinct power, reliability, and regulatory needs. Component-level analysis provides insights into the technological advancements and supply chain dynamics of engines, propellers, thrusters, and control systems. Finally, the distinction between OEM and aftermarket caters to the initial installation market versus the vast segment of maintenance, repair, and upgrade services.

The value chain for the Marine Propulsion Systems market is intricate, involving various stages from raw material sourcing to end-user deployment and after-sales service. Upstream analysis involves the procurement of essential raw materials such as specialized steel alloys for engine blocks and shafts, composite materials for propellers, and advanced electronics for control systems. Key players at this stage include metallurgical companies, chemical producers, and specialized electronics component manufacturers. These suppliers provide critical inputs that dictate the quality, durability, and performance characteristics of the final propulsion systems. The reliability and efficiency of this upstream segment are crucial for the overall supply chain's resilience and cost-effectiveness.

Midstream activities involve the design, manufacturing, and assembly of the propulsion systems. This includes engine manufacturers, propeller and thruster specialists, and system integrators who combine various components into a complete propulsion solution. These manufacturers often engage in significant research and development to innovate new technologies, improve efficiency, and comply with environmental standards. The downstream segment primarily comprises shipyards, which integrate the propulsion systems into new vessel builds, and vessel owners/operators, who procure and operate the ships. After-sales services, including maintenance, repair, and overhaul (MRO) provided by specialized service companies or the original equipment manufacturers themselves, form a critical part of the downstream value chain, ensuring operational longevity and performance.

Distribution channels for marine propulsion systems can be both direct and indirect. Direct channels typically involve large manufacturers selling directly to major shipyards or significant fleet owners for new builds or large-scale retrofitting projects. This allows for closer collaboration, customization, and technical support. Indirect channels involve a network of distributors, agents, and local service partners who facilitate sales, installation, and support, particularly for smaller vessel operators, recreational boats, or in regions where the manufacturer does not have a direct presence. These indirect channels are vital for market penetration and providing localized expertise and service. The complexity of these channels reflects the diverse nature of the marine industry and the specific needs of its various segments.

The potential customers for Marine Propulsion Systems are diverse, spanning a broad spectrum of the maritime industry, each with unique requirements and purchasing considerations. These end-users and buyers are primarily driven by factors such as operational efficiency, regulatory compliance, vessel type, and specific mission profiles. Commercial shipping companies represent a significant customer base, encompassing operators of cargo ships, tankers, bulk carriers, and container vessels that require powerful, fuel-efficient, and reliable propulsion systems to support global trade routes. The increasing demand for eco-friendly solutions from this segment is a major purchasing driver, leading to investments in LNG, hybrid, and other alternative fuel propulsion technologies to reduce carbon footprints and operating costs.

Another crucial customer segment includes cruise lines and ferry operators, who prioritize passenger comfort, safety, and increasingly, reduced emissions in sensitive coastal and port areas. Their demand leans towards low-noise, low-vibration, and environmentally compliant propulsion systems, often favoring electric and hybrid configurations. Naval forces and defense ministries worldwide constitute a vital market for high-performance, durable, and stealth-capable propulsion systems for frigates, destroyers, submarines, and aircraft carriers. For this segment, reliability, power, and the ability to operate in diverse conditions are paramount, often involving gas turbines and advanced diesel-electric arrangements.

Furthermore, offshore energy companies operating supply vessels, anchor handling tugs, and drilling rigs form a specialized customer group requiring robust and highly maneuverable propulsion systems capable of operating in challenging environments. The recreational boating sector, including yacht owners, sailboat enthusiasts, and motorboat users, represents a growing segment for smaller, often quieter, and more user-friendly propulsion solutions, with a rising trend towards electric and hybrid options for leisure craft. Each of these end-user categories contributes to the overall demand, driving innovation and diversification within the Marine Propulsion Systems market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 18.2 Billion |

| Market Forecast in 2032 | USD 29.3 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Wärtsilä Corporation, MAN Energy Solutions, Caterpillar Inc., Rolls-Royce plc, Siemens AG, ABB Ltd., Volvo Penta, Cummins Inc., Hyundai Heavy Industries Co. Ltd., General Electric Company, Deutz AG, Yanmar Holdings Co. Ltd., Mitsubishi Heavy Industries Ltd., Kawasaki Heavy Industries Ltd., Scania AB, Brunswick Corporation, Torqeedo GmbH, Veth Propulsion, Schottel Group, Berg Propulsion. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Marine Propulsion Systems market is currently undergoing a transformative period, driven by rapid advancements in technology and an unwavering commitment to environmental sustainability. A central element of this evolution is the widespread adoption of dual-fuel engines, which offer the flexibility to operate on traditional marine fuels alongside cleaner alternatives like LNG. This technology provides an immediate pathway for vessels to reduce emissions while global infrastructure for zero-emission fuels continues to develop. Complementing this, hybrid-electric propulsion systems are gaining significant traction, combining conventional engines with electric motors and batteries to optimize fuel consumption, reduce emissions, and enhance operational flexibility, particularly in dynamic operating profiles such as harbor maneuvers and coastal transit.

Further pushing the boundaries of marine propulsion are fully battery-electric systems, primarily suitable for shorter routes, ferries, and smaller vessels, offering zero-emission operation. Fuel cell technology, leveraging hydrogen or other reformers to produce electricity, represents a frontier technology for truly zero-emission long-range shipping, though it still faces challenges regarding hydrogen storage and bunkering infrastructure. Alongside these powertrain innovations, advancements in propeller designs, such as highly skewed propellers and contra-rotating propellers, are significantly improving hydrodynamic efficiency, reducing cavitation, and enhancing thrust. These mechanical innovations are critical for maximizing the effectiveness of various propulsion systems, whether conventional or alternative-fueled.

Digitalization is another paramount trend within the technology landscape, with integrated control and monitoring systems becoming increasingly sophisticated. These systems utilize advanced sensors, data analytics, and connectivity to provide real-time performance optimization, predictive maintenance capabilities, and remote diagnostic services, thereby improving operational reliability and reducing downtime. Exhaust gas treatment systems, including scrubbers and selective catalytic reduction (SCR) units, remain essential for compliance with current emission regulations for vessels still operating on conventional fuels. The convergence of these technological innovations is creating a more efficient, environmentally responsible, and technologically advanced marine propulsion ecosystem, addressing the complex demands of the modern maritime industry.

The Marine Propulsion Systems market is primarily driven by expanding global maritime trade, increasingly stringent environmental regulations mandating cleaner solutions, continuous technological advancements, and rising global naval expenditure for fleet modernization and expansion.

Environmental regulations, particularly those from the IMO (International Maritime Organization) regarding sulfur emissions (IMO 2020) and greenhouse gas reduction (EEXI, CII), are compelling shipowners to adopt alternative fuels like LNG, methanol, ammonia, hydrogen, and invest in hybrid or electric propulsion systems to comply with global decarbonization targets.

Key emerging technologies include dual-fuel engines compatible with various alternative fuels, advanced hybrid-electric and fully battery-electric propulsion systems, fuel cell technology for zero emissions, and highly efficient propeller designs. Digitalization for optimized control and predictive maintenance is also a critical technological trend.

Asia-Pacific is the leading region in the Marine Propulsion Systems market, driven by its robust shipbuilding industry, significant maritime trade volumes, and growing investments in both commercial and naval fleets across countries like China, South Korea, and Japan.

The industry faces challenges such as high initial investment costs for advanced and alternative fuel systems, the complexity of integrating new technologies, the lack of widespread global infrastructure for bunkering emerging alternative fuels, and uncertainties stemming from geopolitical instability and fluctuating energy prices.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.