ID : MRU_ 429517 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

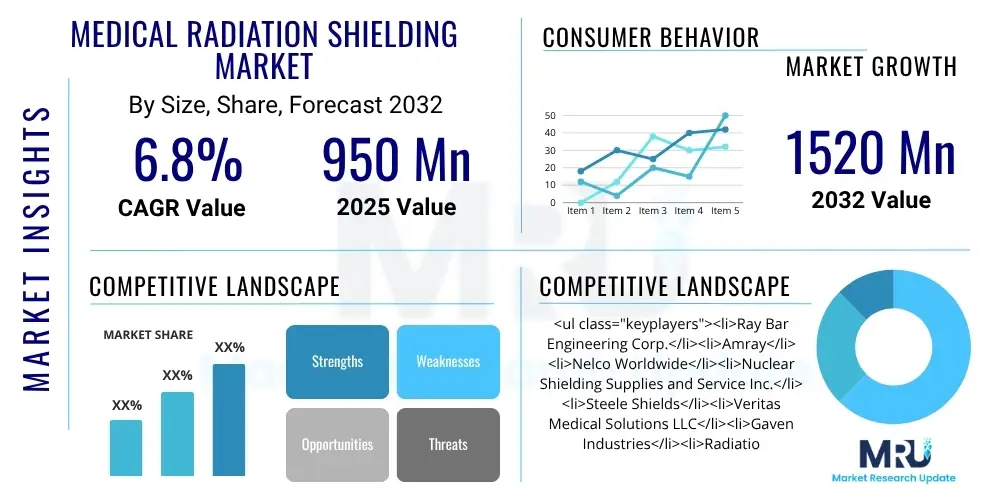

The Medical Radiation Shielding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 950 million in 2025 and is projected to reach USD 1520 million by the end of the forecast period in 2032.

The Medical Radiation Shielding Market encompasses a comprehensive range of products and solutions meticulously designed to mitigate the deleterious effects of ionizing radiation across various medical applications. These critical protective measures are indispensable in environments where diagnostic imaging modalities, such as X-rays, Computed Tomography (CT) scans, and fluoroscopy, are routinely performed, as well as in therapeutic settings like radiation oncology departments utilizing external beam radiation therapy and brachytherapy. The fundamental objective of these shielding solutions is to ensure the utmost safety for patients, healthcare professionals, and the wider public by effectively attenuating radiation to levels that comply with stringent international and national safety standards, thereby preventing acute and chronic radiation-induced injuries.

The product portfolio within this market is remarkably diverse, spanning from permanent structural installations to portable and personal protective equipment. This includes lead-lined walls, doors, windows, and modular shielding rooms that form the foundational protective infrastructure of radiology and oncology departments. Additionally, personal protective gear such as lead aprons, thyroid shields, leaded eyewear, and gloves are vital for medical personnel directly involved in procedures. Specialized materials like high-purity lead, dense concrete, tungsten alloys, and advanced composite materials are carefully selected and employed based on the type, energy, and intensity of radiation emitted, along with specific attenuation requirements and architectural considerations of the healthcare facility. These materials are engineered to offer optimal protection while considering factors such as weight, durability, and environmental impact.

The market’s substantial growth trajectory is underpinned by several compelling factors. Foremost among these is the escalating global incidence of chronic and life-threatening diseases, particularly cancer, which has led to a significant increase in the demand for both diagnostic imaging procedures and radiation therapy treatments. Concurrently, the worldwide demographic shift towards an aging population further contributes to this demand, as older individuals generally require more frequent medical examinations and interventions. Enhanced public awareness regarding radiation safety and the potential risks associated with exposure has also driven healthcare providers to invest proactively in superior shielding technologies. Furthermore, continuous technological advancements in medical imaging and therapeutic equipment, which often involve higher radiation doses or more complex operational environments, necessitate sophisticated and effective shielding solutions to maintain optimal safety parameters. The increasingly stringent regulatory frameworks enacted by health authorities globally serve as a constant impetus, compelling healthcare facilities to upgrade and maintain state-of-the-art radiation shielding to ensure compliance and patient safety.

The Medical Radiation Shielding Market is poised for substantial expansion, driven by the confluence of increasing global healthcare expenditure, a rising prevalence of chronic diseases necessitating advanced medical diagnostics and therapies, and an unwavering focus on enhancing radiation safety protocols. Key business trends underscore a pronounced shift towards customized, modular, and integrated shielding solutions that cater to the unique architectural and operational demands of modern healthcare facilities. Manufacturers are intensely focused on research and development to innovate beyond traditional lead-based materials, exploring and adopting lighter, more environmentally sustainable, and equally effective alternatives, such as tungsten alloys and advanced composites. Strategic collaborations, mergers, and acquisitions are also prominent, enabling companies to expand their geographical footprint, diversify product offerings, and consolidate market share in an increasingly competitive landscape.

From a regional perspective, North America and Europe continue to hold significant market shares, characterized by highly developed healthcare infrastructures, robust adoption rates of cutting-edge medical technologies, and well-established, rigorous regulatory frameworks that mandate comprehensive radiation protection. These regions exhibit a mature demand for sophisticated shielding solutions, driven by ongoing facility upgrades and a strong emphasis on occupational health and safety. Conversely, the Asia Pacific (APAC) region is emerging as the fastest-growing market, propelled by rapid urbanization, significant investments in healthcare infrastructure development, increasing disposable incomes, and a burgeoning medical tourism sector. Countries such as China, India, and Japan are witnessing a surge in the construction of new hospitals and diagnostic centers, which, in turn, fuels an escalating demand for both structural and personal radiation shielding products. Latin America, along with the Middle East and Africa (MEA), also presents promising growth opportunities, albeit from a lower baseline, as their healthcare sectors undergo modernization and expand access to advanced medical services.

Segmentation trends reveal that diagnostic shielding applications currently dominate the market, primarily due to the high volume of routine diagnostic procedures like X-rays and CT scans performed worldwide. Within the material segment, while lead remains a staple owing to its proven efficacy and cost-effectiveness, the demand for lead-free alternatives is steadily climbing, driven by environmental concerns and the desire for lighter, more versatile solutions. Hospitals and specialized diagnostic centers represent the largest end-user segments, consistently requiring comprehensive shielding for their extensive array of radiation-emitting equipment. A notable trend is the increasing demand for integrated solutions that encompass not only the supply of shielding materials but also specialized design, installation, and ongoing maintenance services, reflecting a preference among healthcare providers for turnkey projects that ensure regulatory compliance and operational efficiency.

Common user questions regarding the influence of Artificial Intelligence (AI) on the Medical Radiation Shielding Market frequently center on its potential to enhance safety protocols, optimize shielding design parameters, and improve the overall efficiency of radiation management within clinical environments. There is a palpable curiosity about how advanced AI algorithms and machine learning models could provide more accurate predictions of radiation dose distribution, thereby enabling the creation of more effective and precisely tailored shielding strategies. Users also express interest in the cost implications of integrating AI into existing infrastructure, alongside considerations of how AI might reshape the roles and requisite skill sets for radiation safety officers and medical physicists. A recurring theme is the expectation that AI could facilitate a shift towards more dynamic, adaptive, and personalized shielding solutions, moving beyond traditional static and fixed installations.

Key themes emerging from these inquiries highlight the pervasive expectation that AI will be a transformative force, leading to the development of more intelligent and responsive shielding systems. Stakeholders anticipate that AI can enable real-time monitoring of radiation exposure, offering immediate alerts and adaptive recommendations for optimal protection. Furthermore, there is a strong belief that AI can significantly streamline the complex computational processes involved in determining optimal shielding thickness and placement, particularly in intricate architectural spaces or for novel radiation therapy techniques. The integration of AI is expected to minimize human error in the planning and execution phases, ultimately contributing to a substantially safer environment for both patients undergoing procedures and the medical personnel delivering care, while also potentially simplifying and accelerating regulatory compliance through automated data analysis and comprehensive reporting capabilities.

The Medical Radiation Shielding Market is profoundly shaped by a dynamic interplay of Drivers, Restraints, Opportunities, and a variety of pervasive Impact Forces. A primary driver propelling market expansion is the escalating global prevalence of chronic and life-threatening diseases, most notably cancer, which mandates a significant increase in the volume of diagnostic imaging procedures such as X-rays, CT scans, and PET scans, alongside a rising demand for sophisticated radiation therapy treatments. This surge in medical interventions directly correlates with a heightened requirement for robust and effective radiation protection measures across healthcare facilities. Furthermore, the global demographic trend of an aging population contributes substantially to this demand, as older individuals typically necessitate more frequent diagnostic screenings and medical procedures, consequently expanding the installed base of radiation-emitting equipment and the commensurate need for comprehensive shielding solutions. Stringent government regulations and international safety standards, meticulously formulated by bodies such as the International Atomic Energy Agency (IAEA) and various national health organizations, also serve as formidable drivers, compelling healthcare institutions worldwide to proactively invest in advanced, compliant, and continuously updated shielding technologies to safeguard patients, staff, and the broader community from undue radiation exposure.

However, the market’s growth trajectory is also subject to several significant restraints that can hinder its full potential. The inherently high cost associated with advanced shielding materials, particularly those offering superior attenuation capabilities, lightweight properties, or eco-friendly characteristics, presents a considerable barrier, especially for healthcare providers in developing economies operating under constrained budgets. The complexity involved in accurately designing, fabricating, and implementing custom shielding solutions for diverse and often architecturally challenging medical environments, coupled with the critical need for highly specialized expertise in radiation physics and engineering, adds substantially to overall project costs and extends implementation timelines. Additionally, a persistent lack of widespread awareness regarding the specific benefits, long-term cost-effectiveness, and optimal integration of advanced radiation shielding, particularly within some emerging regions, can impede adoption rates. Moreover, growing environmental concerns pertaining to the production, use, and disposal of traditional lead-based shielding materials, along with increasingly stringent environmental regulations, present a long-term restraint, fostering a push towards the development and widespread adoption of more sustainable and non-toxic alternatives.

Despite these challenges, the Medical Radiation Shielding Market is replete with considerable opportunities for innovation and growth. Emerging economies across the Asia Pacific, Latin America, and the Middle East & Africa regions represent substantial untapped potential, driven by rapidly expanding healthcare infrastructures, increasing national healthcare expenditures, and a growing societal understanding of the critical importance of radiation safety. Technological advancements in material science are continually paving the way for the introduction of innovative, lightweight, and eco-friendly shielding materials that offer superior performance characteristics and facilitate easier installation and maintenance. The ongoing global trend towards personalized medicine and precision radiation therapy also creates unique avenues for the development of specialized, highly customizable, and adaptive shielding solutions tailored to individual patient needs and specific treatment protocols. Furthermore, the increasing integration of smart technologies, real-time remote monitoring systems, and AI-driven design and optimization tools presents transformative opportunities to significantly enhance the efficiency, safety, and regulatory compliance within the entire radiation shielding landscape. The pervasive impact forces, including the dynamic evolution of regulatory frameworks, rapid technological shifts in both medical imaging and therapeutic equipment, prevailing global economic conditions influencing healthcare investment cycles, and heightened public health awareness regarding the long-term effects of radiation exposure, continuously exert profound influence, shaping the market's current dynamics and future direction.

The Medical Radiation Shielding Market is meticulously segmented to provide a granular understanding of its complex dynamics, reflecting the diverse product categories, material preferences, application spectrums, and end-user profiles within the global healthcare industry. This detailed segmentation is instrumental for market participants to identify lucrative growth segments, formulate targeted business strategies, and effectively allocate resources. Each segment's trajectory is critically influenced by technological advancements, evolving regulatory mandates, shifting healthcare priorities, and varying economic conditions across different geographical regions, necessitating a flexible and adaptive market approach.

The market is primarily segmented across several key dimensions. Product type segmentation typically delineates between structural shielding components, such as lead-lined walls, doors, windows, and modular rooms, which form the permanent protective infrastructure of medical facilities, and personal protective equipment (PPE), including lead aprons, thyroid shields, and leaded eyewear, worn by medical professionals. Material type segmentation categorizes shielding based on the composition of protective barriers, ranging from conventional lead to an expanding array of lead-free alternatives like tungsten, bismuth, barium sulfate, and various advanced composite materials, alongside dense concrete and specialized leaded glass. Application-based segmentation differentiates between the specific shielding requirements for diagnostic imaging (e.g., X-ray, CT scan, fluoroscopy, mammography, interventional radiology) and radiation therapy (e.g., external beam radiation therapy, brachytherapy, proton therapy) as well as nuclear medicine. Finally, end-user segmentation classifies the primary consumers of these products and services, predominantly comprising hospitals, diagnostic centers, specialized cancer treatment centers, and various research institutions, each with distinct volume and customization needs.

The value chain for the Medical Radiation Shielding Market commences with crucial upstream activities centered on the procurement and initial processing of raw materials. This foundational stage involves the meticulous sourcing and refining of heavy metals such as lead and tungsten, which are prized for their high radiation attenuation properties. It also encompasses the production of specialized concrete formulations, radiation-resistant glass, and advanced polymer composites that are integral to modern shielding solutions. Key suppliers in this segment bear the significant responsibility of providing high-purity, consistent-quality materials that strictly adhere to exacting industry standards for radiation attenuation, structural integrity, and durability. The reliability and consistent supply of these raw materials are paramount, directly influencing the manufacturing process, the final performance characteristics of shielding products, and the overall cost-effectiveness, thereby necessitating robust supply chain management, rigorous quality control, and strategic supplier relationships from the very genesis of the value chain.

Midstream activities within the value chain focus on the sophisticated manufacturing, fabrication, and assembly of diverse radiation shielding products. This critical stage encompasses precision engineering, detailed design, and the skilled assembly of structural components like lead-lined barriers, modular wall systems, radiation-shielded doors, and windows, as well as the production of personal protective equipment. Manufacturers in this segment often leverage advanced technologies such as Computer-Aided Design (CAD) and Computer-Aided Manufacturing (CAM) to facilitate highly customized designs and ensure precision fabrication, meeting the unique architectural and operational demands of various medical facilities. A significant aspect of value creation at this stage is continuous innovation in material science, with a strong emphasis on developing lighter, more efficient, environmentally friendly, and aesthetically appealing alternatives to traditional shielding materials. This focus on research and development drives product differentiation, enhances competitive advantage, and responds to evolving regulatory and sustainability pressures.

Downstream activities in the value chain primarily involve the distribution, expert installation, and comprehensive after-sales support services. Distribution channels are varied and strategically deployed, ranging from direct sales models where manufacturers engage directly with large healthcare institutions and major construction projects, to indirect channels that utilize third-party distributors, specialized integrators, and expert contractors who possess specific expertise in medical facility construction and outfitting. The installation phase is exceptionally critical, demanding specialized technical expertise and adherence to precise specifications to guarantee that the shielding is correctly implemented, thereby effectively preventing any radiation leakage and ensuring optimal safety. Furthermore, comprehensive after-sales services, including routine maintenance, periodic inspections, regulatory compliance checks, and certification, are essential components that ensure the long-term effectiveness, reliability, and ongoing compliance of installed shielding solutions. The strategic integration of both direct sales teams for key accounts and an extensive network of indirect partners enables comprehensive market penetration and facilitates efficient service delivery to a broad and diverse customer base across the global healthcare landscape.

The primary end-users and key buyers within the Medical Radiation Shielding Market are predominantly institutions and professionals situated across the healthcare sector, particularly those involved in the diagnosis and treatment of diseases utilizing radiation-emitting equipment. These critical customers are driven by an overarching imperative to ensure maximum radiation protection, meticulously adhere to stringent regulatory compliance standards, and guarantee the paramount safety of both their patients and invaluable medical staff. Their purchasing decisions are significantly influenced by a multitude of factors including the specific type and volume of radiation procedures routinely performed, the unique architectural and design requirements of their facilities, prevailing budgetary constraints, and the absolute necessity for durable, long-lasting shielding solutions that can seamlessly integrate with their existing technological infrastructure and operational workflows.

Hospitals, especially those equipped with extensive diagnostic imaging departments (e.g., radiology, nuclear medicine) and dedicated oncology centers, represent the largest and most critical segment of potential customers. This category encompasses a broad spectrum, including large university hospitals, general community hospitals, and highly specialized medical centers that provide comprehensive medical services. Diagnostic imaging centers, which are solely focused on performing procedures such as X-rays, CT scans, MRIs (for facilities where imaging devices are grouped), and fluoroscopy, constitute another major buying group, necessitating extensive structural and personal shielding solutions to manage their high patient throughput. Cancer treatment centers, specializing in advanced radiation therapy modalities like external beam radiation, brachytherapy, and proton therapy, have exceptionally specific and mission-critical shielding requirements due to the high energy levels of radiation frequently employed in their therapeutic protocols.

Beyond these foundational categories, other significant potential customers include a range of specialty clinics, such as cardiology clinics employing interventional procedures, orthopedic practices utilizing imaging, and dental clinics with intraoral and panoramic X-ray capabilities. Ambulatory surgical centers are also increasingly investing in shielding as they expand their service offerings to include procedures requiring radiation. Furthermore, various research institutions and academic laboratories engaged in medical imaging research, nuclear medicine studies, and radiopharmaceutical development represent a vital customer segment, requiring robust and often highly customized radiation shielding to protect their personnel and maintain a safe research environment. The continuous global expansion of healthcare facilities, coupled with the increasing adoption of cutting-edge medical technologies, consistently broadens the potential customer base for advanced medical radiation shielding products and comprehensive associated services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 950 million |

| Market Forecast in 2032 | USD 1520 million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered |

|

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape within the Medical Radiation Shielding Market is characterized by relentless innovation focused on enhancing safety, improving operational efficiency, and promoting environmental sustainability. A significant and ongoing area of technological advancement involves the development of advanced shielding materials that offer superior radiation attenuation properties while simultaneously being lighter, thinner, and increasingly lead-free. These next-generation composite materials, often incorporating elements such as tungsten, bismuth, barium sulfate, and various specialized polymers, are meticulously engineered to provide comparable or even enhanced protection compared to traditional lead, effectively addressing growing concerns related to weight, material toxicity, and complex disposal requirements. Furthermore, pioneering research into nanomaterials and smart polymers holds the promise of revolutionary breakthroughs, potentially enabling the creation of highly flexible, adaptive, and even dynamic shielding solutions that can adjust protection levels based on specific radiation fields and operational needs, representing a significant paradigm shift.

Another pivotal technological advancement significantly impacting the market is the widespread adoption and continuous refinement of modular and highly customizable shielding solutions. Modern healthcare facilities frequently demand designs that offer exceptional flexibility, enabling rapid installation, easy reconfiguration, or convenient relocation to adapt to evolving clinical requirements and technological upgrades. Technologies such as pre-fabricated modular walls, interlocking shielding blocks, and portable barriers are gaining substantial traction, facilitating quicker construction timelines, reducing disruption, and allowing for greater adaptability without compromising radiation safety standards. Computer-aided design (CAD) and computer-aided manufacturing (CAM) technologies play an increasingly vital role in these developments, enabling precise engineering and bespoke fabrication for unique architectural constraints and highly specialized medical equipment, thereby ensuring seamless integration and optimal radiation containment across diverse clinical settings.

Beyond the realm of advanced materials and structural components, digital technologies are increasingly exerting a transformative influence across the market. The implementation of sophisticated remote monitoring systems for real-time radiation levels, often seamlessly integrated with smart building management systems, provides invaluable data on shielding integrity and overall operational safety. This capability allows for proactive maintenance, immediate detection of potential radiation leaks, and rapid response to any emergent issues, significantly bolstering safety protocols. Furthermore, the growing adoption of advanced robotics in certain surgical and interventional medical procedures necessitates the development of specialized shielding solutions tailored specifically for robotic arms, associated equipment, and operating theaters. These collective technological advancements are fundamentally aimed at elevating the efficacy, convenience, and regulatory compliance of medical radiation shielding, firmly establishing it as a highly dynamic, technologically driven, and increasingly specialized field essential to modern healthcare infrastructure.

The Medical Radiation Shielding Market exhibits distinct regional variations in terms of growth rates, adoption patterns, and the stringency of regulatory landscapes, each reflecting unique healthcare infrastructures, varying levels of economic development, and differing public health priorities. These regional dynamics are absolutely critical for market participants to comprehensively understand, as they directly influence strategic investment decisions, shape localized business development initiatives, and highlight both specific market opportunities and prevalent operational challenges. Every major geographical area presents a unique amalgamation of driving forces and restraining factors that collectively contribute to the global market's overarching trajectory and evolutionary path.

North America and Europe currently represent the most mature and dominant markets for medical radiation shielding globally. This preeminence is largely attributable to their highly developed and well-established healthcare systems, significantly high per capita healthcare expenditures, widespread and early adoption of advanced diagnostic and therapeutic medical technologies, and the existence of exceptionally rigorous and comprehensive regulatory frameworks governing radiation safety. The strong presence of leading medical device manufacturers, coupled with a deep-rooted societal emphasis on occupational safety and environmental protection, further reinforces market growth in these regions. Moreover, consistent innovation in lead-free shielding materials and sophisticated modular designs is particularly pronounced in North America and Europe, driven by environmental consciousness, evolving building codes, and a demand for ergonomic and adaptable solutions.

Conversely, the Asia Pacific (APAC) region is unequivocally projected to emerge as the fastest-growing market segment over the forecast period, fueled by rapid urbanization, substantial and continuous investments in expanding healthcare infrastructure, increasing disposable incomes leading to greater healthcare access, and a surging patient population primarily due to the rising incidences of chronic and lifestyle-related diseases. Key countries within APAC, such as China, India, Japan, and South Korea, are experiencing significant investments in the construction of new hospitals, diagnostic centers, and specialized clinics, which directly translates into a substantial and escalating demand for both structural and personal radiation shielding solutions. Similarly, Latin America and the Middle East & Africa (MEA) are also demonstrating promising growth trajectories, albeit from a lower base, propelled by ongoing improvements in healthcare access, proactive government initiatives aimed at upgrading and modernizing medical facilities, and a growing understanding of the critical necessity for robust radiation protection measures as healthcare systems mature and expand their capabilities.

Medical radiation shielding comprises specialized materials and structures engineered to reduce the exposure of individuals to harmful ionizing radiation emitted during diagnostic imaging and therapeutic procedures. Its essentiality stems from its role in safeguarding patients, medical personnel, and the public from radiation-induced health risks, ensuring operational safety, and maintaining strict compliance with global regulatory standards.

The primary materials include traditional lead, highly valued for its exceptional density and effective attenuation properties. Increasingly, the market is adopting advanced lead-free alternatives such as tungsten, bismuth, barium sulfate, and various sophisticated composite materials, alongside dense concrete and specialized leaded glass, driven by enhanced safety, sustainability, and architectural flexibility considerations.

AI is poised to significantly influence the market by enabling highly precise shielding design through advanced simulation and predictive analytics, optimizing material selection for specific applications, and enhancing real-time radiation monitoring systems. It facilitates improved safety protocols, streamlines regulatory compliance, and is expected to drive the development of more adaptive and intelligent shielding solutions.

Key growth drivers include the escalating global incidence of chronic diseases, particularly cancer, which necessitates a higher volume of diagnostic imaging and radiation therapy procedures. Further impetus comes from the aging global population, heightened awareness regarding radiation safety, continuous technological advancements in medical equipment, and increasingly stringent regulatory mandates from health authorities worldwide.

The main end-users and primary buyers of medical radiation shielding products are hospitals (including general, university, and specialty hospitals), dedicated diagnostic imaging centers, specialized cancer treatment centers, and various specialty clinics (e.g., dental, orthopedic, cardiology). These facilities critically rely on comprehensive shielding solutions to ensure a safe environment for both patients and staff during radiation-emitting procedures.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.