ID : MRU_ 429424 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

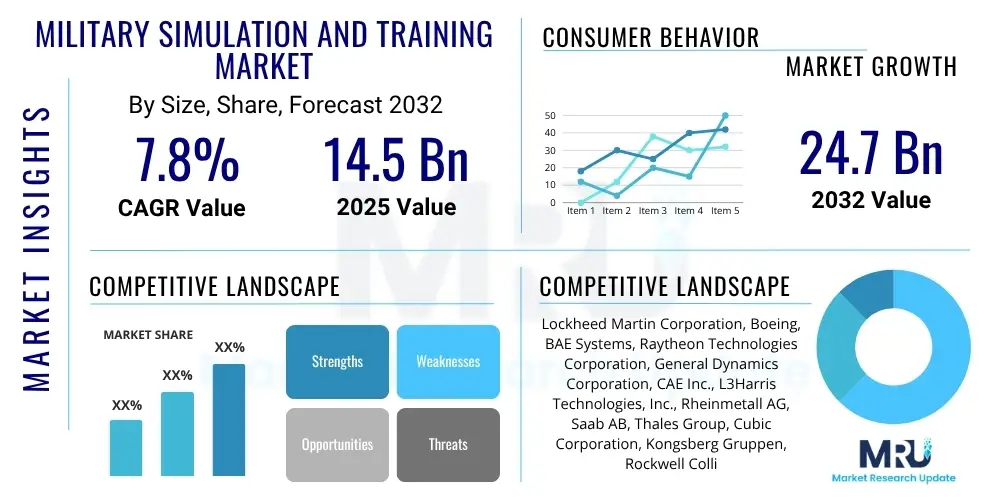

The Military Simulation and Training Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 24.7 Billion by the end of the forecast period in 2032.

The Military Simulation and Training Market encompasses a wide array of advanced technologies and systems designed to equip military personnel with critical skills, enhance operational readiness, and facilitate mission rehearsal in safe, controlled, and cost-effective environments. These systems replicate real-world scenarios, allowing forces to practice complex maneuvers, decision-making, and teamwork without the risks or logistical burdens associated with live training exercises. The product description spans hardware such as full-mission simulators for aircraft, ships, and ground vehicles, as well as sophisticated software platforms for virtual and constructive training, integrated with emerging technologies like virtual reality (VR), augmented reality (AR), and artificial intelligence (AI).

Major applications of military simulation and training extend across air, land, and naval domains, covering everything from pilot training and combat vehicle operation to tactical decision-making, marksmanship, maintenance procedures, and disaster response. The benefits are multifold, including significant cost reductions compared to live training, enhanced safety for personnel and equipment, the ability to train for rare or high-risk scenarios, accelerated skill acquisition, and improved interoperability among different military units. Moreover, these systems provide detailed performance analytics, enabling continuous improvement and adaptive training pathways for individual soldiers and entire units.

The market is primarily driven by escalating global geopolitical tensions, necessitating higher levels of military preparedness and advanced skill sets among defense forces worldwide. Continuous technological advancements, particularly in computing power, sensor technology, and immersive experiences, are enabling increasingly realistic and sophisticated simulation environments. The inherent cost-effectiveness of simulated training compared to traditional live exercises, coupled with the imperative for rapid adaptation to evolving threats, further propels market growth, making it a critical component of modern defense strategies.

The Military Simulation and Training Market is experiencing robust growth, driven by an urgent need for enhanced defense capabilities amidst global instability and the rapid evolution of warfare tactics. Key business trends indicate a significant shift towards integrating advanced digital technologies, including Artificial Intelligence, Virtual Reality, Augmented Reality, and cloud-based platforms, to create highly immersive and adaptive training solutions. There is a growing emphasis on Live, Virtual, and Constructive (LVC) integration, which combines real-world training with simulated environments to achieve unparalleled realism and comprehensive skill development. Furthermore, the modularity and scalability of new systems are becoming paramount, allowing for flexible deployments and customization to diverse training requirements, reflecting a strategic move towards more agile and responsive defense infrastructure.

Regionally, North America remains the dominant market, characterized by substantial defense budgets, robust R&D investment, and a strong presence of key technology providers, driving innovation and adoption of cutting-edge solutions. Europe is also a significant market, with countries focusing on modernizing their armed forces and enhancing interoperability within NATO, leading to investments in advanced training systems. The Asia Pacific region is poised for rapid expansion, fueled by increasing defense spending, particularly in countries like China, India, and South Korea, which are expanding their military capabilities and seeking advanced training solutions. The Middle East and Africa, driven by ongoing conflicts and security concerns, are investing in sophisticated simulation technologies to improve operational readiness, while Latin America exhibits gradual growth as nations modernize their defense postures.

Segment-wise, the market sees strong growth across various platforms and applications. Virtual simulation, offering high realism and repeatability at lower costs, is expanding significantly, especially for flight and combat training. Constructive simulation, used for strategic planning and command-and-control exercises, is also gaining traction due to its ability to model large-scale scenarios. The demand for full-mission simulators across airborne, naval, and ground platforms continues to be strong, essential for comprehensive operational readiness. Additionally, specialized training such as maintenance, tactical, and marksmanship training is increasingly leveraging simulation for efficient and effective skill transfer. The service segment, including maintenance, upgrades, and support, is a critical component, ensuring the longevity and effectiveness of these complex systems.

Users frequently inquire about how Artificial Intelligence will fundamentally transform military training, often focusing on its ability to enhance realism, personalize learning experiences, and analyze performance. Common questions revolve around AI's role in creating intelligent adversaries, adaptive training scenarios, and data-driven feedback mechanisms. Concerns also emerge regarding the ethical implications of AI in simulated combat, data security, and the potential for over-reliance on technology. Expectations center on AI delivering more dynamic, responsive, and effective training solutions that better prepare personnel for the complexities of modern warfare, while also addressing the challenges of integrating these advanced capabilities into existing infrastructure and managing associated costs.

The Military Simulation and Training Market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities. Key drivers include escalating global geopolitical instability, necessitating a higher degree of military readiness and advanced skill development, alongside the inherent cost-effectiveness of simulation compared to traditional live training. Continuous technological advancements, such as the integration of Virtual Reality, Augmented Reality, Artificial Intelligence, and cloud computing, are enabling more immersive, realistic, and adaptive training environments. These technologies facilitate the acquisition of complex skills, enhance decision-making capabilities, and allow for safe rehearsal of high-risk missions, which further propels market expansion.

However, the market also faces notable restraints. The substantial initial investment required for high-fidelity simulation systems, including sophisticated hardware and software development, can be a barrier for some defense organizations. Furthermore, ensuring robust data security and protecting sensitive military information within complex simulation networks presents ongoing challenges. The rapid pace of technological obsolescence necessitates frequent upgrades and maintenance, adding to long-term costs. Integration complexities between disparate systems and legacy infrastructure also pose significant hurdles, affecting the seamless adoption and operation of advanced simulation solutions across different military branches and allied forces.

Opportunities for growth are abundant within this evolving landscape. Emerging markets in Asia Pacific and the Middle East, with increasing defense budgets and modernization initiatives, represent significant potential for market expansion. The development of highly customizable simulation solutions tailored to specific national security threats and operational doctrines offers a niche for specialized providers. Furthermore, the accelerating trend towards Live, Virtual, Constructive (LVC) integration, which combines all forms of training for comprehensive preparedness, presents new avenues for innovation. The increasing demand for advanced cybersecurity training and the adoption of AI and machine learning for predictive analysis and intelligent tutoring systems are also creating new market segments and driving technological evolution within the sector. The impact forces within the market, such as the bargaining power of key defense contractors and the strategic importance of cutting-edge technology, shape the competitive landscape and influence investment decisions.

The Military Simulation and Training Market is intricately segmented across various dimensions to cater to the diverse needs of global defense forces. These segmentations allow for a granular understanding of market dynamics, technology adoption rates, and investment priorities within different operational contexts. The market is primarily categorized by the type of simulation, the platform it serves, its specific application, the components involved, the underlying technologies utilized, and the ultimate end-users. This comprehensive segmentation helps market participants to identify key growth areas and tailor their offerings to specific demands within the defense sector.

The value chain for the Military Simulation and Training Market commences with extensive upstream activities, primarily involving research and development, design, and the sourcing of highly specialized components. This upstream segment includes suppliers of advanced computing hardware, high-fidelity display systems, sophisticated sensors, haptic devices, and complex software development kits. Companies in this stage are critical for pushing the boundaries of realism and technological capability, often requiring significant investment in innovation and highly skilled engineering talent. The quality and availability of these foundational technologies directly impact the performance and effectiveness of the final simulation systems, making supplier relationships strategically vital.

Midstream activities involve the integration and assembly of these components into complete simulation and training systems. This phase is dominated by large defense contractors and specialized simulation companies that design, develop, and manufacture the simulators, integrate various software modules, and ensure interoperability across complex networked environments. It includes system architecture design, software development for scenario generation, instructor operating stations, and performance assessment tools, as well as the physical construction of simulator cabins and control rooms. Value is added through expert system integration, rigorous testing, and customization to meet specific military requirements, ensuring that the assembled systems deliver high-fidelity training experiences.

The downstream segment focuses on the delivery, deployment, and long-term support of these systems to the end-users. This includes installation, ongoing maintenance, technical support, software updates, and training for military instructors and technicians. Distribution channels primarily involve direct sales through long-term government contracts with defense ministries and military branches. These direct relationships are characterized by complex procurement processes, stringent security requirements, and often involve extensive post-sales service agreements. Indirect channels may include partnerships with local defense integrators in international markets or participation in collaborative development programs with allied nations, facilitating broader market penetration and customized solutions. The entire value chain emphasizes close collaboration, security, and long-term commitment due to the strategic nature of military applications.

The primary potential customers for military simulation and training solutions are government defense organizations and their various branches globally. This includes national armies, navies, and air forces, which continuously seek advanced tools to maintain operational readiness, develop new competencies, and ensure the proficiency of their personnel in an ever-evolving threat landscape. The inherent demand from these entities is driven by the need for cost-effective, safe, and realistic training for a wide range of operational roles, from individual soldier skills to large-scale joint force exercises. Their procurement decisions are often influenced by geopolitical factors, national defense budgets, technological superiority, and the desire to reduce the logistical and environmental footprint of live training.

Beyond the core military branches, other significant end-users and buyers include specialized units such as Special Operations Forces, who require highly customized and clandestine training environments to hone unique skills. Homeland Security agencies and paramilitary forces also represent a growing customer segment, particularly for training in counter-terrorism, border security, and emergency response scenarios, where simulation offers a safe way to practice high-stakes operations. Additionally, military academies and educational institutions are increasingly adopting simulation technologies to educate future leaders and technicians, providing foundational knowledge and practical experience in a controlled academic setting, ensuring a pipeline of skilled personnel. International alliances and peacekeeping organizations also invest in simulation to foster interoperability and common operational procedures among diverse national forces, enhancing multilateral cooperation and mission effectiveness.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2032 | USD 24.7 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, Boeing, BAE Systems, Raytheon Technologies Corporation, General Dynamics Corporation, CAE Inc., L3Harris Technologies, Inc., Rheinmetall AG, Saab AB, Thales Group, Cubic Corporation, Kongsberg Gruppen, Rockwell Collins (now Collins Aerospace), Elbit Systems Ltd., Textron Systems, Israel Aerospace Industries (IAI), Fidelity Technologies Corporation, Kratos Defense & Security Solutions, Inc., MetaVR, Inc., Bohemia Interactive Simulations (BISim) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Military Simulation and Training Market is at the forefront of technological innovation, constantly integrating advanced solutions to enhance realism, effectiveness, and efficiency. Virtual Reality (VR), Augmented Reality (AR), and Mixed Reality (MR) are pivotal, offering highly immersive environments that blur the lines between physical and digital training, enabling personnel to interact with virtual objects and scenarios within real-world settings or fully synthetic worlds. These technologies provide sensory-rich experiences crucial for skill development in complex operational contexts, improving spatial awareness and task proficiency. High-fidelity visual systems, coupled with advanced haptic feedback devices, further elevate the realism, allowing trainees to experience visual cues and physical sensations that accurately mimic real equipment operation and environmental conditions.

Artificial Intelligence (AI) and Machine Learning (ML) are transforming simulation by introducing intelligent agents, adaptive adversaries, and personalized training pathways. AI algorithms can analyze trainee performance in real-time, provide intelligent tutoring, and dynamically adjust scenarios to match individual learning curves, significantly enhancing training efficacy. Cloud computing platforms are gaining traction, offering scalable, on-demand infrastructure for distributed simulation, facilitating large-scale joint exercises, and reducing the need for extensive on-premise hardware. This enables greater flexibility, collaboration, and cost-efficiency in delivering training content and managing complex simulation networks across geographical boundaries.

Furthermore, Live, Virtual, and Constructive (LVC) integration frameworks are becoming standard, enabling seamless interaction between real-world military assets, virtual simulators, and computer-generated forces within a unified training environment. This holistic approach provides unparalleled realism for mission rehearsal and tactical decision-making, allowing forces to practice complex scenarios that are impossible or too costly to replicate in live settings. Open architecture systems and Distributed Interactive Simulation (DIS) protocols are also critical, promoting interoperability between different simulation platforms and ensuring that various systems can communicate and cooperate effectively, which is essential for joint force training and international coalition operations. These technological advancements collectively drive the market towards more dynamic, comprehensive, and effective military training solutions.

Military simulation and training refers to the use of technology-driven systems to replicate real-world operational environments, allowing military personnel to practice and hone skills, rehearse missions, and develop tactical proficiency in a safe, controlled, and cost-effective manner. It encompasses virtual reality, augmented reality, and constructive simulation tools.

Key benefits include significant cost reduction compared to live exercises, enhanced safety for personnel and equipment, the ability to train for high-risk or rare scenarios, accelerated skill development, improved decision-making, and detailed performance analytics for continuous improvement and adaptive learning.

AI is transforming military simulation by creating intelligent and adaptive adversaries, enabling personalized training pathways, providing advanced performance analytics, and facilitating dynamic scenario generation. It enhances realism, optimizes learning outcomes, and helps identify areas for improvement more efficiently.

North America currently dominates the military simulation and training market due to high defense spending and strong technological innovation, particularly in the United States. The Asia Pacific region is projected to be the fastest-growing market, driven by increasing defense budgets and military modernization efforts.

The main challenges include the high initial investment required for advanced simulation systems, critical data security concerns within complex networked environments, the rapid pace of technological obsolescence necessitating frequent upgrades, and the complexities involved in integrating disparate systems and legacy infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.