ID : MRU_ 430610 | Date : Nov, 2025 | Pages : 249 | Region : Global | Publisher : MRU

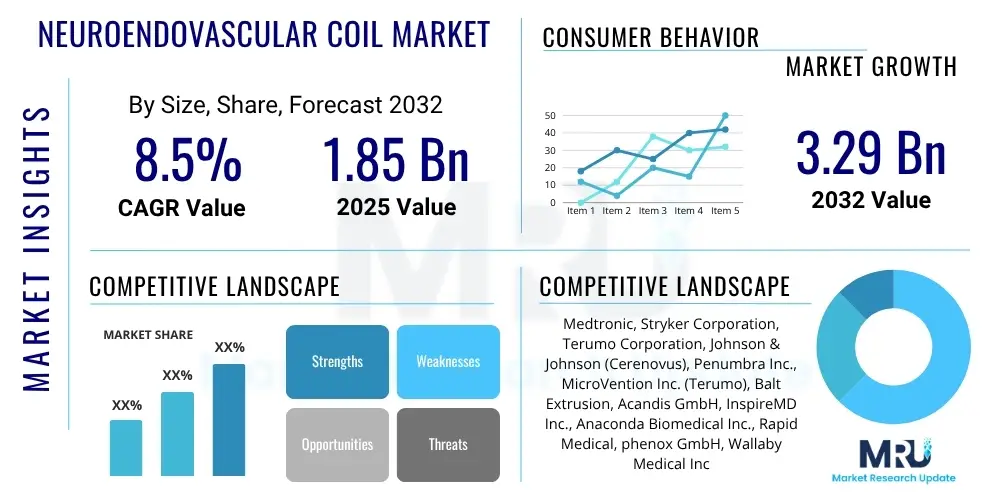

The Neuroendovascular Coil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2032. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.29 Billion by the end of the forecast period in 2032.

The Neuroendovascular Coil Market is dedicated to the advancement and commercialization of specialized medical devices designed for the minimally invasive treatment of complex neurovascular pathologies. These critical devices are primarily utilized to manage conditions such as intracranial aneurysms and arteriovenous malformations (AVMs), which pose significant risks of hemorrhage and neurological damage. The coils, typically crafted from ultra-fine platinum wire or other advanced biocompatible materials, are meticulously deployed into the affected vessels or aneurysm sacs through a catheter-based system. Their inherent flexibility allows them to conform precisely to the lesion's unique anatomy, initiating a thrombotic response that effectively occludes the abnormal vascular structure and safeguards against rupture or further bleeding, thereby preserving normal cerebral circulation.

The product portfolio within this market segment is diverse, featuring various coil designs optimized for different clinical scenarios. These include helical, complex, and spherical configurations, each engineered to address specific anatomical challenges related to aneurysm size, shape, and neck morphology. Furthermore, technological innovation has led to the development of advanced coil types, such as hydrogel-coated coils that expand upon deployment to achieve denser packing and promote enhanced thrombogenicity, and bioactive coils embedded with materials designed to stimulate a natural healing response and reduce recurrence rates. Major applications of these neuroendovascular coils extend across both ruptured and unruptured intracranial aneurysms, aiming to prevent life-threatening subarachnoid hemorrhage, and also in the embolization of AVMs, often as a pre-surgical adjunct or definitive therapy. The overarching benefits of these procedures emphasize their minimally invasive nature, leading to reduced patient morbidity, accelerated recovery times, and often superior clinical outcomes when compared to traditional open neurosurgery.

Several significant driving factors are propelling the sustained growth of the neuroendovascular coil market. A paramount driver is the rising global incidence and prevalence of neurological disorders, particularly intracranial aneurysms, which demand increasingly sophisticated and accessible treatment modalities. The rapidly expanding elderly population worldwide, a demographic segment inherently more susceptible to these cerebrovascular conditions, further amplifies the need for effective interventions. Continuous and rapid advancements in materials science, imaging technologies, and delivery system mechanics have made neuroendovascular coiling procedures considerably safer, more precise, and broadly applicable to a wider range of patients. This technological evolution, coupled with a growing preference among both clinicians and patients for less invasive therapeutic options that promise quicker rehabilitation and improved quality of life, robustly supports market expansion. Additionally, supportive regulatory frameworks and evolving reimbursement policies in key healthcare economies facilitate broader access to these innovative treatments.

The Neuroendovascular Coil Market is experiencing a period of dynamic growth, underscored by profound technological innovation and an escalating global demand for advanced neurovascular interventions. Key business trends indicate an intense competitive landscape characterized by leading medical device manufacturers heavily investing in research and development to introduce next-generation coil systems. These innovations focus on improving coil deliverability, enhancing long-term occlusion rates, and reducing procedural complications, leading to a steady pipeline of advanced products like platinum alloy coils with optimized softness, hydrogel-coated coils for dense packing, and bioactive coils designed to promote endothelial healing. Strategic partnerships, mergers, and acquisitions remain crucial strategies for companies aiming to expand their geographic footprint, diversify product offerings, and integrate complementary technologies such as AI-powered planning tools and robotic assistance into their solutions, thereby consolidating market leadership and fostering innovation.

Regionally, the market exhibits varied growth trajectories and maturity levels. North America and Europe currently represent the largest and most established markets, primarily due to their sophisticated healthcare infrastructures, high levels of patient awareness, substantial healthcare expenditure, and the early adoption of advanced medical technologies. These regions benefit from a high concentration of specialized neurovascular centers and favorable reimbursement scenarios that support the widespread use of neuroendovascular coiling. Conversely, the Asia Pacific (APAC) region is projected to register the most accelerated growth throughout the forecast period. This rapid expansion is fueled by improving healthcare accessibility, a burgeoning aging population, increasing disposable incomes, and significant government and private sector investments aimed at enhancing medical facilities and adopting modern treatment modalities in populous nations such as China, India, and Japan. Latin America and the Middle East & Africa (MEA) are also emerging as promising markets, driven by a rising prevalence of neurovascular diseases and growing efforts to upgrade healthcare systems, albeit from a relatively smaller base.

Segment-wise, the market demonstrates distinct patterns. The intracranial aneurysm indication segment continues to hold the largest market share, driven by the high incidence and critical need for urgent treatment of both ruptured and unruptured aneurysms. Within product types, while traditional bare platinum coils maintain a dominant position due to their proven efficacy and long clinical history, the adoption of advanced hydrogel and bioactive coils is rapidly increasing. These newer generations offer enhanced thrombogenicity and lower recurrence rates, positioning them for significant future growth. Hospitals, particularly specialized neurological and university hospitals, remain the predominant end-users, given the complex nature of the procedures and the prerequisite for specialized infrastructure and highly trained medical professionals. However, a gradual shift towards ambulatory surgical centers for less complex cases or follow-up procedures is also being observed, indicating an evolving landscape for service delivery and market access.

User inquiries concerning the influence of Artificial Intelligence on the Neuroendovascular Coil Market frequently center on its potential to revolutionize diagnostic precision, optimize personalized treatment planning, bolster procedural safety, and predict long-term patient outcomes with greater accuracy. Users are particularly interested in how AI can navigate the inherent complexities of neurovascular anatomy and pathologies, aiding in the intricate decision-making processes required for successful neuroendovascular interventions. Significant curiosity exists around AI's capabilities in advanced medical image analysis, expecting it to provide superior visualization of aneurysms and arteriovenous malformations, and to offer real-time guidance during catheter navigation and coil deployment. Common user concerns often include the validation and reliability of AI algorithms in clinical settings, data security and privacy implications, and the necessity for comprehensive regulatory oversight to ensure safe and effective integration, as well as the potential implications for the roles of human specialists.

AI is strategically positioned to profoundly transform multiple facets of the neuroendovascular coil market, spanning the entire patient journey from initial diagnosis to long-term post-operative care. In the diagnostic phase, sophisticated AI algorithms are capable of analyzing high-resolution medical images, such as CT angiography and MR angiography, with unparalleled speed and a heightened level of precision. This allows for the earlier and more accurate identification of subtle aneurysms, vascular anomalies, and other critical lesions that might otherwise be overlooked or challenging for human interpretation, thus facilitating timely intervention and significantly improving patient prognoses. For the crucial stage of treatment planning, AI platforms can perform intricate simulations of various coiling strategies. By processing extensive data on aneurysm morphology, size, location, and patient-specific characteristics, AI assists neurosurgeons in selecting the most optimal coil type, size, and configuration, thereby enhancing procedural efficiency, minimizing risks, and optimizing therapeutic efficacy for each unique case.

Moreover, during the neuroendovascular procedure itself, AI-powered tools are emerging as invaluable assets, offering real-time guidance and augmented visualization. These systems can seamlessly integrate data from multiple intraoperative imaging modalities, including fluoroscopy, 3D imaging, and even robotic guidance systems, to provide a comprehensive, dynamic view of the surgical field. This enhanced situational awareness and navigation assistance contribute significantly to the precision of coil placement, drastically reducing the likelihood of complications such as vessel perforation, coil prolapse, or incomplete occlusion. Post-operatively, AI algorithms hold immense promise for predicting long-term patient outcomes, identifying potential recurrence risks, and customizing follow-up schedules based on an individual's unique response to treatment. This integration of AI also promises to streamline clinical workflows, automate repetitive data analysis tasks, and accelerate the research and development cycle for novel, more intelligent coil designs, fostering a new era of innovation and personalized care within the market.

The Neuroendovascular Coil Market operates within a complex framework influenced by distinct driving forces, inherent restraints, and compelling opportunities that collectively shape its growth trajectory and competitive landscape. The market's expansion is significantly propelled by the escalating global prevalence of neurovascular disorders, notably intracranial aneurysms and arteriovenous malformations (AVMs), which necessitate advanced, less invasive treatment options. Continuous and rapid advancements in neuroimaging techniques have empowered earlier and more accurate diagnoses, expanding the patient pool eligible for coiling procedures. Furthermore, the global demographic shift towards an aging population, inherently more susceptible to these cerebrovascular conditions, acts as a powerful demand driver. The increasing adoption of minimally invasive surgical interventions, favored for their advantages such as reduced hospital stays, quicker patient recovery times, and lower rates of perioperative complications compared to traditional open surgery, substantially boosts the market. Additionally, supportive government policies and improving reimbursement scenarios in key healthcare economies facilitate greater access and adoption of these sophisticated treatments.

Despite these robust drivers, the market faces several formidable restraints. The high overall cost associated with neuroendovascular procedures, encompassing not only the specialized coils but also advanced imaging equipment, operating room setup, and highly skilled personnel, can be a significant barrier to widespread adoption, particularly in developing regions with constrained healthcare budgets. Stringent and often protracted regulatory approval processes for new medical devices, which demand extensive preclinical and clinical validation, frequently delay the market introduction of innovative products and elevate R&D costs. Moreover, while generally safe, neuroendovascular procedures carry inherent risks of complications such as post-procedural hemorrhage, ischemic stroke, coil compaction, or migration. Though their incidence is relatively low, these potential adverse events remain a critical concern for both patients and clinicians. A persistent global shortage of highly specialized neurosurgeons and interventional neuroradiologists, coupled with a lack of adequate training infrastructure in many regions, further limits the broad accessibility and expansion of these advanced therapies.

Amidst these challenges, the Neuroendovascular Coil Market is rich with compelling opportunities. Emerging economies, particularly those in the Asia Pacific and Latin American regions, present substantial untapped market potential due to their vast and growing patient populations, rapidly developing healthcare infrastructure, and increasing disposable incomes. These regions are witnessing a surge in medical tourism and government initiatives aimed at modernizing healthcare systems, creating fertile ground for market expansion. Technological innovation continues to be a primary opportunity, with ongoing research into next-generation coil systems that offer enhanced biocompatibility, improved long-term stability, and even drug-eluting properties. The integration of cutting-edge technologies like artificial intelligence for improved diagnostic accuracy and personalized treatment planning, along with robotic assistance for enhanced procedural precision and reduced operator fatigue, promises to redefine the landscape of neuroendovascular interventions. These innovations are expected to expand the indications for coiling, improve patient outcomes, and drive significant future market growth by addressing current unmet clinical needs and refining existing therapeutic paradigms.

The Neuroendovascular Coil Market is characterized by a multi-faceted segmentation strategy, essential for gaining a granular understanding of market dynamics, identifying specific growth avenues, and formulating targeted business strategies. This comprehensive analysis breaks down the market across various critical dimensions, including product type, the specific disease indication being treated, the materials utilized in coil manufacturing, and the primary end-users or healthcare settings where these procedures are performed. Each segmentation provides unique insights into demand patterns, technological preferences, and regional adoption rates, allowing stakeholders to make informed decisions regarding product development, marketing, and distribution. Understanding these distinct segments is paramount for accurately assessing the competitive landscape and pinpointing lucrative niche markets.

Segmentation by product type is a fundamental differentiator within the market. This category typically includes bare platinum coils, which represent the long-standing gold standard due to their proven efficacy and extensive clinical track record. However, significant growth is observed in advanced coil types such as hydrogel-coated coils, which absorb water and expand within the aneurysm sac to achieve higher packing densities and more stable occlusion, and bioactive coils, designed with advanced polymer coatings that actively promote endothelial cell growth and accelerate long-term healing, thereby reducing the risk of aneurysm recurrence. Further distinctions are made between detachable coils, which allow for precise, controlled release after optimal positioning, and non-detachable coils, typically used in simpler cases or for vessel sacrifice. The choice of coil type is often dictated by the specific aneurysm morphology, location, and the neurosurgeon's preference and experience.

Disease indication forms another critical segmentation, predominantly featuring intracranial aneurysms as the largest application area, encompassing both ruptured and unruptured cases that demand immediate or prophylactic intervention. Arteriovenous malformations (AVMs), complex tangles of abnormal blood vessels, also constitute a significant segment, often requiring endovascular embolization as a standalone treatment or in conjunction with surgery or radiosurgery. Other vascular lesions, though less common, also represent a niche application. Material segmentation highlights the use of medical-grade platinum and various biocompatible polymers, including hydrogels and other bioactive agents. Lastly, end-user segmentation predominantly identifies hospitals, especially tertiary care and academic medical centers with specialized neurovascular units, as the primary consumers. However, the increasing proliferation of ambulatory surgical centers and dedicated specialty clinics equipped to handle neuroendovascular procedures is expanding this customer base, particularly for routine follow-ups or less complex cases. This detailed segmentation enables a more nuanced market analysis and strategic planning.

The value chain of the Neuroendovascular Coil Market is an intricate network of interconnected activities, meticulously orchestrated to ensure the development, production, and delivery of high-quality neurovascular devices to patients worldwide. The upstream segment of this chain is characterized by intensive research and development (R&D) and the strategic sourcing of highly specialized raw materials. R&D efforts are paramount, involving substantial investments in designing novel coil geometries, enhancing material properties such as flexibility, thrombogenicity, and biocompatibility, and innovating advanced microcatheter delivery systems. Concurrently, the procurement of medical-grade platinum alloys, advanced biocompatible polymers, and other specialized components demands stringent quality control, adherence to global regulatory standards, and strong supplier relationships to guarantee the foundational integrity and safety of the final product. Suppliers in this segment must meet rigorous specifications to ensure the subsequent manufacturing stages proceed without compromise.

Moving downstream, the manufacturing phase constitutes a critical midstream segment where raw materials are transformed into finished neuroendovascular coils. This process requires state-of-the-art manufacturing facilities, cleanroom environments, precision engineering techniques, and highly specialized automation to produce these intricate devices. Rigorous quality assurance (QA) and quality control (QC) protocols are embedded throughout the manufacturing process to ensure every coil meets the strictest safety, efficacy, and performance standards stipulated by regulatory bodies such globally. Companies in this stage focus intensely on optimizing production efficiency, minimizing waste, and scaling operations to fulfill the ever-growing global demand for neurovascular intervention devices. The complexity of these devices necessitates highly skilled labor and advanced technological capabilities in their production, distinguishing this segment from more generalized medical device manufacturing.

The final downstream activities encompass the comprehensive distribution, sales, and post-sales support, directly linking manufacturers to end-users. Distribution channels are often multifaceted, involving both direct and indirect strategies. Major manufacturers frequently establish direct sales forces to engage directly with large hospitals, university medical centers, and specialized neurovascular clinics, allowing for greater control over product messaging, pricing, and fostering deep customer relationships. This direct approach ensures that highly technical product information and clinical support can be effectively conveyed. Indirect distribution involves leveraging specialized distributors, wholesalers, and Group Purchasing Organizations (GPOs), particularly in regions where manufacturers lack a direct presence or where local market penetration requires specific expertise and established networks. These partners are crucial for extending market reach into diverse geographic areas, navigating local regulatory nuances, and managing inventory logistics. Post-sales support, including training for clinicians on new devices and technical assistance, is also a vital component, ensuring optimal product utilization and contributing significantly to customer satisfaction and loyalty across both direct and indirect channels.

The primary potential customers for neuroendovascular coils are healthcare institutions that possess the requisite infrastructure and specialized medical expertise to perform complex neurovascular interventions. These prominently include large university hospitals, academic medical centers, and highly specialized neurological hospitals. Such facilities are typically equipped with advanced interventional suites, state-of-the-art imaging technologies such as biplane angiography, and a multidisciplinary team comprising highly skilled neurosurgeons, interventional neuroradiologists, neurologists, and specialized nursing staff. These leading institutions are at the forefront of adopting cutting-edge medical technologies, participating in clinical trials, and treating the most intricate neurovascular cases, making them significant and consistent purchasers of advanced neuroendovascular coil systems. Their procurement decisions are heavily influenced by demonstrated clinical efficacy, robust safety profiles, the extent of technological innovation, and the overall cost-effectiveness of the devices, alongside the manufacturer's reputation, comprehensive clinical support, and training programs.

Beyond these major tertiary care centers, a growing segment of potential customers includes smaller community hospitals that have developed dedicated neurosurgical or interventional radiology units. As neuroendovascular procedures become more standardized and their benefits more widely recognized, these facilities are increasingly investing in the capabilities to perform certain interventions, particularly for less complex or emergent cases. Furthermore, specialized ambulatory surgical centers (ASCs) and dedicated specialty clinics are emerging as significant end-users, especially for diagnostic procedures, elective cases suitable for outpatient settings, or follow-up care for patients who have undergone coiling. These facilities may prioritize coils that offer ease of use, require less extensive capital equipment, and provide consistently reliable clinical outcomes for a range of common neurovascular pathologies, contributing to a broadening customer base beyond the traditional academic hospital setting.

While direct purchasers, government healthcare programs and private insurance providers exert a profound, albeit indirect, influence as major stakeholders. Their evolving reimbursement policies and coverage decisions are critical determinants of patient access and the overall adoption rates of neuroendovascular coiling procedures. Favorable and consistent reimbursement ensures that healthcare providers can afford to offer these advanced treatments and that patients can access them without prohibitive financial burden, thereby directly driving market demand. Additionally, prominent research institutions and medical universities are also key potential customers. They utilize neuroendovascular coils for educational purposes, training the next generation of specialists, conducting pivotal clinical trials for new devices, and advancing research into novel therapeutic approaches for neurovascular diseases. Ultimately, the entire ecosystem of end-users and buyers is composed of entities and professionals deeply committed to enhancing neurovascular patient care through safe, effective, and minimally invasive interventional techniques.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2032 | USD 3.29 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Stryker Corporation, Terumo Corporation, Johnson & Johnson (Cerenovus), Penumbra Inc., MicroVention Inc. (Terumo), Balt Extrusion, Acandis GmbH, InspireMD Inc., Anaconda Biomedical Inc., Rapid Medical, phenox GmbH, Wallaby Medical Inc., MicroPort Scientific Corporation, Boston Scientific Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Neuroendovascular Coil Market is intrinsically driven by a sophisticated and rapidly advancing technological landscape, continuously evolving to enhance clinical outcomes, improve patient safety, and expand the therapeutic scope for complex neurovascular conditions. Central to this evolution are breakthroughs in advanced material science, with a primary focus on refining platinum alloys to achieve optimal balance between flexibility, radiopacity for clear visualization under fluoroscopy, and superior biocompatibility within the delicate cerebral vasculature. Innovations also encompass the development of cutting-edge coating technologies, such as hydrogel polymers that absorb bodily fluids to expand and achieve denser coil packing, and specialized bioactive coatings engineered to actively promote endothelial cell growth and accelerate natural healing processes, thereby minimizing aneurysm recurrence and ensuring robust, long-term occlusion stability. These material advancements are crucial for tailoring coils to the highly variable and intricate anatomies of neurovascular lesions, moving progressively towards precision medicine.

A second, equally pivotal aspect of the technological landscape involves continuous improvements in microcatheter and delivery system design. The development of ultra-soft, highly flexible, and supremely trackable microcatheters enables neurosurgeons and interventional neuroradiologists to navigate through the tortuous and fragile cerebral arterial network with unprecedented safety and precision, reaching even the most distal and challenging lesions. Innovations in advanced detachment mechanisms are paramount, ensuring precise and controlled deployment of coils exactly at the target site, which significantly mitigates the risks of premature release, coil prolapse into the parent vessel, or distal migration. Furthermore, sophisticated imaging modalities are absolutely integral to guiding these complex procedures. High-resolution digital subtraction angiography (DSA) and advanced 3D rotational angiography provide exceptionally clear, real-time visualization of the aneurysm and surrounding vasculature, allowing for meticulous procedural guidance and immediate confirmation of coil placement. Real-time imaging feedback is indispensable for maximizing procedural success and ensuring optimal patient safety.

The market is also witnessing the transformative impact of emerging technologies, particularly in areas like computational fluid dynamics (CFD) and artificial intelligence (AI). CFD is increasingly employed during pre-procedural planning to simulate complex blood flow dynamics within aneurysms and predict the hemodynamic impact of various coiling and flow diversion strategies, thus enabling more informed and personalized treatment decisions. Robotic assistance systems are gaining significant traction, offering enhanced precision, stability, and dexterity during microcatheter manipulation. These systems have the potential to reduce operator fatigue, improve reproducibility for highly complex interventions, and potentially expand access to specialized procedures. The imminent integration of AI for advanced image analysis, automated surgical planning, and sophisticated outcome prediction is poised to revolutionize diagnostic accuracy, optimize treatment personalization, and enhance post-operative monitoring. These multifaceted technological advancements collectively drive the continuous improvement in efficacy, safety, and broad adoption of neuroendovascular coiling procedures, continually pushing the frontiers of neurovascular care and expanding the therapeutic possibilities for patients worldwide.

Neuroendovascular coils are highly specialized medical devices predominantly used in minimally invasive procedures to treat critical neurovascular conditions, most notably intracranial aneurysms and arteriovenous malformations (AVMs), by safely occluding these lesions to prevent rupture and associated bleeding.

During a neuroendovascular coiling procedure, a very fine, flexible microcatheter is carefully guided through the patient's blood vessels, typically from a femoral artery, up to the precise location of the aneurysm or AVM within the brain. Tiny, platinum coils are then precisely deployed through this microcatheter into the lesion, filling the sac and initiating a thrombotic response that effectively seals it off from normal blood flow, thereby preventing its rupture.

The key advantages of neuroendovascular coiling procedures include their minimally invasive nature, eliminating the need for open skull surgery. This leads to significantly faster patient recovery times, shorter hospital stays, reduced post-operative pain, and a lower incidence of certain surgical complications, making it a preferred and often safer treatment alternative for many eligible patients.

The market primarily offers several categories of neuroendovascular coils. These include conventional bare platinum coils, renowned for their flexibility and radiopacity; advanced hydrogel-coated coils, which expand upon hydration to achieve superior packing density; and bioactive coils, featuring specialized coatings designed to promote rapid endothelialization and long-term stability. Coils are also categorized by their deployment mechanism, such as detachable and non-detachable variations.

North America and Europe currently represent the leading geographical regions in the Neuroendovascular Coil Market, primarily due to their well-developed healthcare infrastructures, high incidence of neurovascular diseases, and significant technological adoption. However, the Asia Pacific region is rapidly emerging as the fastest-growing market, driven by substantial improvements in healthcare access, increasing investments, and a large, aging patient population.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.