ID : MRU_ 430508 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

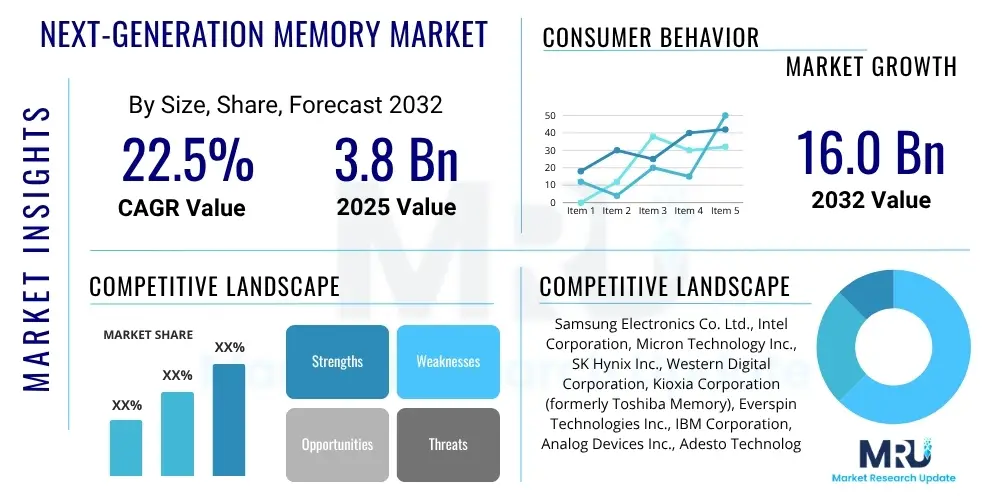

The Next-Generation Memory Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2032. The market is estimated at $3.8 Billion in 2025 and is projected to reach $16.0 Billion by the end of the forecast period in 2032.

The Next-Generation Memory market encompasses a diverse range of innovative memory technologies designed to overcome the limitations of conventional DRAM and NAND flash. These advanced solutions offer improved performance characteristics such as higher speed, lower power consumption, increased endurance, and most critically, non-volatility, allowing them to retain data even without power. This category includes technologies like MRAM, PCM, ReRAM, FeRAM, and 3D XPoint, each with unique advantages tailored for specific computing needs.

The primary applications for these emerging memory types are broad and continually expanding, driven by the escalating demands of data-intensive environments. Major applications include enterprise storage systems, high-performance computing (HPC), artificial intelligence (AI) and machine learning (ML) workloads, the Internet of Things (IoT) devices, and advanced automotive electronics. Their non-volatile nature makes them ideal for embedded systems requiring instant-on capabilities and robust data retention, while their speed positions them as viable alternatives or complements to traditional volatile memory in demanding computational scenarios.

The market is predominantly driven by the increasing need for faster and more energy-efficient memory solutions across various industries. Key benefits include enhanced system performance, reduced power consumption, extended device lifespan due to high endurance, and the ability to integrate memory and storage functionalities into a single component. These factors are crucial for the development of next-generation electronics and computing infrastructures, propelling the rapid growth and adoption of these advanced memory technologies.

The Next-Generation Memory market is experiencing substantial growth, primarily fueled by the burgeoning demand for high-performance computing, artificial intelligence, and sophisticated data center solutions. Business trends indicate a strong focus on research and development, with significant investments from semiconductor giants and government initiatives to accelerate technology maturation. Strategic collaborations and partnerships between memory manufacturers, foundries, and system integrators are becoming increasingly common, aiming to overcome manufacturing complexities and standardize new memory interfaces. This collaborative environment is fostering innovation and facilitating the integration of these advanced memory solutions into commercial products at a faster pace.

Regional trends highlight Asia Pacific as a dominant force in the production and consumption of next-generation memory, driven by its robust semiconductor manufacturing ecosystem and significant growth in consumer electronics and data center infrastructure. North America continues to be a hub for research and development, particularly in AI and HPC applications, leading to early adoption and technological breakthroughs. Europe is also making strides, especially in automotive and industrial applications where reliable and durable memory solutions are paramount. Emerging economies are gradually increasing their adoption rates as their digital infrastructures expand, presenting new growth avenues for memory providers.

Segment trends within the market show distinct trajectories. Magnetoresistive RAM (MRAM) is gaining traction due to its high endurance, speed, and non-volatility, particularly in embedded systems and enterprise storage. Phase Change Memory (PCM) and Resistive RAM (ReRAM) are being explored for their potential in high-density storage class memory and neuromorphic computing. Ferroelectric RAM (FeRAM) continues to find niche applications where ultra-low power consumption and high write endurance are critical. The demand for these diverse memory types is being shaped by specific application requirements, leading to a diversified market landscape rather than a single dominant technology, fostering healthy competition and continuous innovation among developers.

The advent and rapid expansion of artificial intelligence (AI) have profoundly influenced the Next-Generation Memory market, sparking intense user interest regarding how these advanced memory solutions can enhance AI performance and efficiency. Common user questions revolve around the suitability of different next-gen memory types for AI workloads, their ability to handle vast datasets with high throughput, and their contribution to energy efficiency in AI accelerators and edge devices. Users are particularly concerned with finding memory solutions that can overcome the memory wall bottleneck inherent in traditional architectures, which significantly impedes AI training and inference processes. The core themes center on memory speed, density, endurance, and power consumption as critical enablers for next-generation AI systems, driving a significant portion of the innovation and demand in the market.

AI's insatiable demand for rapid data access and processing is a primary driver for next-generation memory adoption. Traditional memory hierarchies often struggle to keep pace with the massive parallel processing requirements of AI algorithms, leading to bottlenecks that limit computational efficiency. Next-generation memories, with their superior speed and non-volatility, offer a compelling solution by providing faster access to parameters and intermediate results, thus accelerating training cycles and improving inference latency. This direct impact on performance makes them indispensable for advancing the capabilities of AI applications, from complex deep learning models to real-time edge AI.

Furthermore, AI workloads often involve frequent data updates and persistent storage of model parameters, which demand memory solutions with high write endurance and data retention. Technologies such as MRAM and ReRAM are particularly well-suited for these requirements, offering a significant advantage over volatile DRAM and flash memory, which have endurance limitations. The integration of next-generation memory into AI accelerators and dedicated AI chips is transforming system architectures, enabling more efficient on-device learning and reduced reliance on cloud-based processing. This shift is critical for developing sophisticated AI systems that are not only powerful but also energy-efficient and capable of operating in diverse, constrained environments.

The Next-Generation Memory market is influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), alongside various impact forces that shape its trajectory. A primary driver is the exponentially increasing demand for high-performance, low-power, and non-volatile memory in applications such as artificial intelligence, machine learning, big data analytics, and the Internet of Things (IoT). The limitations of conventional DRAM and NAND flash in terms of speed, endurance, and power consumption are propelling the adoption of next-gen alternatives. Furthermore, the imperative for faster boot-up times, instant-on capabilities, and robust data retention in edge computing devices and automotive systems significantly contributes to market growth, highlighting the critical role these technologies play in modern digital infrastructure.

Despite these strong drivers, the market faces several significant restraints. High research and development (R&D) costs are a considerable barrier, given the intensive capital investment required for developing and scaling up production of novel memory technologies. Manufacturing complexities, including the integration of new materials and fabrication processes, also pose challenges, often leading to higher production costs compared to established memory types. Additionally, the relatively slower adoption rates in some mainstream applications, due to skepticism about long-term reliability and the need for new ecosystem development, impede faster market penetration. Competition from continually improving traditional memory technologies, which benefit from economies of scale and mature supply chains, further complicates the competitive landscape for emerging solutions.

However, the market is rife with opportunities stemming from the evolving technological landscape. The emergence of new computing paradigms like neuromorphic computing and in-memory computing presents fertile ground for next-generation memories, where their unique characteristics can be fully leveraged. Expansion into niche applications requiring specialized memory features, such as industrial automation, medical devices, and military systems, offers avenues for sustained growth. The increasing focus on energy efficiency in data centers and portable electronics also provides a strong impetus for adopting these low-power solutions. The impact forces include rapid technological advancements, which constantly introduce new capabilities and reduce costs, as well as economic factors influencing R&D investments and market demand. Regulatory landscapes and environmental concerns regarding energy consumption also indirectly influence the market by favoring more efficient memory solutions.

The Next-Generation Memory market is comprehensively segmented by various factors, including technology type, wafer size, application, and end-use, providing a granular view of its diverse landscape. Each segment represents distinct market dynamics, driven by specific technical requirements and industry demands. The technological segmentation, encompassing MRAM, PCM, ReRAM, FeRAM, and 3D XPoint, reflects the ongoing innovation in memory architecture, with each offering unique advantages for speed, density, endurance, and non-volatility. This diversity allows for tailored solutions to address a wide array of computing and storage challenges across different sectors.

Segmentation by wafer size, primarily 200mm and 300mm, indicates the maturity and scalability of manufacturing processes for these advanced memories. While 200mm wafers are often used for specialized or lower-volume production, the transition to 300mm wafers signifies a move towards mass production and cost efficiency, crucial for broader market adoption. The application-based segmentation highlights the widespread utility of next-generation memories, ranging from high-performance enterprise storage and consumer electronics to critical automotive and industrial systems, underscoring their versatility in an increasingly digital world. The growing demand from AI and machine learning applications further emphasizes the market's reliance on these advanced memory types to handle complex computational loads.

The end-use segmentation provides insight into the primary consumers and their specific needs. Data centers and high-performance computing (HPC) environments require memory with extreme speed and density to process vast amounts of information quickly. IoT devices and mobile applications prioritize low power consumption, small form factor, and non-volatility for extended battery life and instant-on functionality. The automotive sector demands rugged, reliable, and high-endurance memory for advanced driver-assistance systems (ADAS) and in-vehicle infotainment. This detailed segmentation is crucial for understanding market trends, identifying growth opportunities, and developing targeted strategies for market penetration and product development within the next-generation memory industry.

The value chain for the Next-Generation Memory market is intricate, involving multiple stages from raw material sourcing to end-product integration, defining the flow of value creation and distribution. At the upstream segment, key activities include the procurement of specialized raw materials such as silicon wafers, rare earth elements, and various chemical precursors essential for fabricating advanced memory structures. This segment also encompasses the design and manufacturing of highly specialized semiconductor equipment, including deposition systems, etching tools, and lithography machines, which are critical for producing next-generation memory devices with high precision and yield. Research and development activities, often conducted by universities, startups, and established semiconductor firms, are foundational to this upstream process, driving innovation in materials science and device physics.

Moving downstream, the value chain involves the memory manufacturers themselves, who design, fabricate, and test the next-generation memory chips. These chips are then assembled into various modules or components. Further downstream, original equipment manufacturers (OEMs) integrate these memory solutions into their final products, which include servers, smartphones, automotive systems, industrial control units, and AI accelerators. Data center operators, cloud service providers, and large enterprises also play a crucial role as direct consumers of these memory technologies, often working closely with manufacturers to customize solutions for their specific infrastructure needs. The efficiency and cost-effectiveness of these downstream processes are vital for widespread market adoption and the overall success of next-generation memory products.

Distribution channels for next-generation memory products vary, often involving a mix of direct and indirect approaches. Direct sales are common for large-volume customers such as major OEMs, data center operators, and government agencies, where direct engagement allows for tailored solutions, technical support, and long-term partnerships. Indirect channels typically involve distributors and value-added resellers (VARs) who reach a broader customer base, including smaller enterprises, embedded system developers, and specialized application developers. These intermediaries play a crucial role in logistics, inventory management, and providing localized support, expanding market reach. The complexity and high-tech nature of next-generation memory often necessitate strong technical expertise within both direct sales teams and indirect channel partners to effectively communicate product benefits and support integration efforts.

The potential customers for Next-Generation Memory are diverse and span across numerous high-growth industries, all seeking superior memory performance to enhance their products and services. A significant segment comprises data center operators and cloud service providers who require memory solutions capable of handling massive data throughput, high transaction rates, and low latency for their ever-expanding server farms and cloud infrastructures. These entities are keen on adopting non-volatile and high-speed memory to improve the efficiency of virtual machines, accelerate database operations, and reduce overall power consumption, driving down operational costs and enhancing service delivery.

Another crucial customer segment includes manufacturers of consumer electronics, particularly those producing high-end smartphones, tablets, and wearable devices. These manufacturers prioritize compact, low-power, and fast memory to enable instant-on functionality, extended battery life, and enhanced user experience for demanding applications like augmented reality (AR) and 5G connectivity. The automotive industry is also a rapidly expanding market for next-generation memory, with autonomous vehicles and advanced driver-assistance systems (ADAS) requiring highly reliable, high-endurance memory for real-time processing of sensor data, navigation, and infotainment systems, often operating in harsh environmental conditions.

Furthermore, companies engaged in artificial intelligence (AI) and machine learning (ML) development represent a key customer base, as these applications critically depend on memory that can swiftly access and process vast datasets for training and inference. Industrial automation and embedded systems designers are also significant buyers, leveraging the non-volatility and endurance of next-generation memory for applications requiring robust data retention in power-off scenarios and reliable operation in challenging industrial environments. The aerospace and defense sector, with its stringent requirements for reliability and performance in extreme conditions, also stands as a strategic market for these advanced memory technologies, making the customer landscape highly diversified and technically demanding.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $3.8 Billion |

| Market Forecast in 2032 | $16.0 Billion |

| Growth Rate | CAGR 22.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics Co. Ltd., Intel Corporation, Micron Technology Inc., SK Hynix Inc., Western Digital Corporation, Kioxia Corporation (formerly Toshiba Memory), Everspin Technologies Inc., IBM Corporation, Analog Devices Inc., Adesto Technologies Corporation (now part of Dialog Semiconductor), Avalanche Technology Inc., Fujitsu Limited, NXP Semiconductors N.V., Renesas Electronics Corporation, STMicroelectronics N.V., Cypress Semiconductor Corporation (now part of Infineon Technologies), Microchip Technology Inc., Crossbar Inc., Spin Transfer Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Next-Generation Memory market is characterized by a dynamic and evolving technology landscape, with several innovative memory types vying for market dominance and specific application niches. Magnetoresistive RAM (MRAM), particularly its Spin-Transfer Torque MRAM (STT-MRAM) and Spin-Orbit Torque MRAM (SOT-MRAM) variants, stands out due to its non-volatility, high speed, and high endurance, making it suitable for both embedded applications and enterprise storage. Phase Change Memory (PCM) offers high density and byte-addressability, positioning it as a strong contender for storage-class memory and persistent memory solutions. Resistive RAM (ReRAM) is attractive for its simple structure, scalability, and potential for high-density storage and neuromorphic computing applications, offering promising avenues for future AI hardware.

Ferroelectric RAM (FeRAM) continues to be utilized in applications requiring extremely low power consumption and very high write endurance, such as smart cards and specific industrial controllers, leveraging its unique ferroelectric properties. Intel's 3D XPoint technology, developed in collaboration with Micron, introduced a new class of memory that bridges the gap between DRAM and NAND flash, offering a combination of high performance, persistence, and density. While initially positioned for data center and high-performance computing applications, its future direction and wider adoption are still evolving. These technologies collectively represent a paradigm shift from traditional memory architectures, addressing the growing performance and efficiency demands of modern computing.

Beyond these established next-generation memory types, the technology landscape also includes emerging innovations such as Nanotube RAM (NRAM), which leverages carbon nanotubes for extremely fast and energy-efficient operations, and Transparent RAM (T-RAM), explored for specific display and optical computing applications. Significant research and development efforts are focused on improving fabrication processes, material science, and interface standards to enhance the commercial viability and widespread adoption of these advanced memories. The ongoing convergence of memory and logic, as seen in in-memory computing architectures, further shapes this landscape, driving the development of memory solutions that can perform computational tasks directly within the memory array, promising unprecedented gains in processing efficiency for data-intensive workloads.

Next-Generation Memory refers to a category of advanced memory technologies designed to offer superior performance characteristics like non-volatility, higher speed, lower power consumption, and increased endurance compared to traditional DRAM and NAND flash. Examples include MRAM, PCM, ReRAM, and FeRAM.

The primary drivers include the escalating demand for high-performance computing, the proliferation of AI and machine learning applications, the expansion of the Internet of Things (IoT), and the critical need for faster and more energy-efficient memory in data centers and automotive electronics.

AI significantly impacts demand by requiring memory that can handle massive datasets at high speeds with low latency and high endurance. Next-generation memories help overcome the "memory wall" bottleneck, accelerating AI training and inference, and enabling more efficient edge AI solutions.

Magnetoresistive RAM (MRAM) is rapidly gaining prominence for its speed and non-volatility in embedded and enterprise applications. Phase Change Memory (PCM) and Resistive RAM (ReRAM) are also highly significant, particularly for high-density storage-class memory and emerging AI architectures.

Key challenges include high research and development costs, complexities in manufacturing and scaling production, the need for new ecosystem development (e.g., interface standards), and competition from continuously improving traditional memory technologies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.