ID : MRU_ 430250 | Date : Nov, 2025 | Pages : 253 | Region : Global | Publisher : MRU

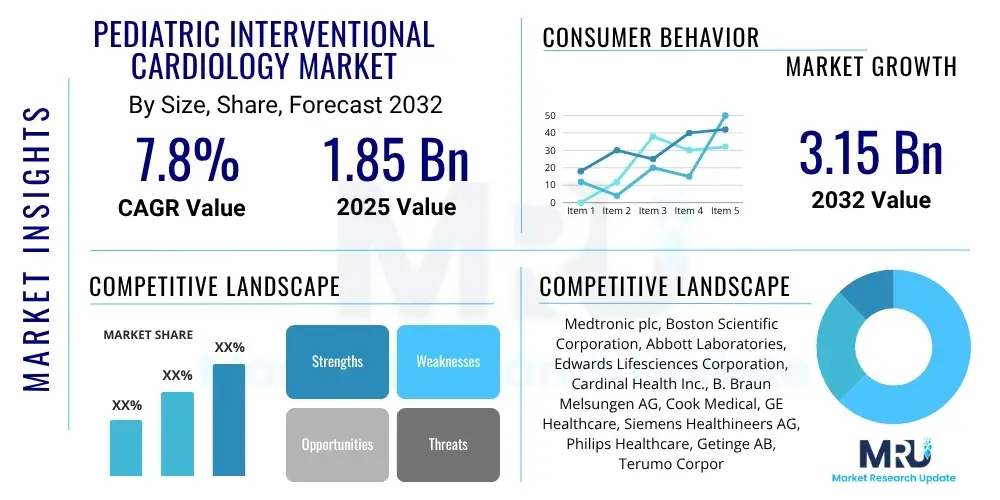

The Pediatric Interventional Cardiology Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.15 Billion by the end of the forecast period in 2032.

The Pediatric Interventional Cardiology Market encompasses a specialized medical field focused on the diagnosis and treatment of congenital heart defects (CHD) and acquired cardiovascular conditions in infants, children, and adolescents using minimally invasive, catheter-based techniques. This advanced approach offers significant advantages over traditional open-heart surgery, including reduced trauma, shorter hospital stays, quicker recovery periods, and improved aesthetic outcomes. The market's growth is intrinsically linked to the increasing global incidence of CHD, alongside continuous innovations in medical device technology and interventional procedures tailored to the unique physiological characteristics of pediatric patients. This sector represents a critical area of modern healthcare, constantly evolving to provide better quality of life and long-term prognosis for young individuals afflicted with complex cardiac anomalies.

Products within this market are diverse, ranging from diagnostic catheters used for hemodynamic assessments and angiography to therapeutic devices like septal occluders for closing defects, balloon catheters for dilating stenotic vessels or valves, and specialized stents for maintaining vessel patency. Major applications include the repair of atrial septal defects (ASD), ventricular septal defects (VSD), patent ductus arteriosus (PDA), pulmonary valve stenosis, aortic valve stenosis, and coarctation of the aorta. The primary benefits of these interventions are clear: they mitigate the risks associated with major surgical procedures, minimize post-operative pain, and accelerate patient rehabilitation, allowing children to return to normal activities much faster. These advantages are propelling the widespread adoption of interventional techniques across various healthcare settings.

Several driving factors are contributing significantly to the expansion of the Pediatric Interventional Cardiology Market. Foremost among these is the escalating prevalence of congenital heart diseases worldwide, leading to a greater demand for effective treatments. Concurrently, rapid technological advancements are yielding more sophisticated, smaller, and safer devices, enabling the treatment of increasingly complex cases in even the tiniest patients. There is also a heightened awareness among healthcare providers and parents regarding the efficacy and benefits of minimally invasive options. Furthermore, government and non-governmental organization initiatives aimed at improving pediatric healthcare infrastructure and increasing access to specialized cardiac care, particularly in developing regions, are playing a crucial role in fostering market growth and expanding treatment accessibility.

The Pediatric Interventional Cardiology Market is experiencing substantial growth, underpinned by a confluence of evolving business trends, distinct regional dynamics, and progressive segmentation shifts. Business trends indicate a marked acceleration in research and development activities, with manufacturers keenly focusing on creating next-generation devices that are even more precise, flexible, and biocompatible for delicate pediatric anatomies. There is also a noticeable trend towards strategic collaborations and partnerships between medical device companies, research institutions, and pediatric hospitals to pool expertise, accelerate innovation, and streamline the regulatory approval process. Furthermore, the market is witnessing increased consolidation through mergers and acquisitions as larger entities seek to broaden their product portfolios and geographical footprint, thereby offering integrated solutions for pediatric cardiac care and enhancing competitive advantage.

Regionally, the market exhibits a differentiated growth landscape. North America and Europe continue to serve as established leaders, characterized by highly developed healthcare infrastructures, significant investment in specialized pediatric cardiac centers, and strong adoption rates of advanced interventional procedures. These regions benefit from robust reimbursement policies and a high concentration of skilled pediatric interventional cardiologists. Conversely, the Asia Pacific region is rapidly emerging as a high-growth frontier, fueled by a large and underserved patient population, increasing healthcare expenditure, improving medical infrastructure, and a growing awareness of modern treatment modalities. Latin America, the Middle East, and Africa are also showing promising, albeit slower, growth driven by government initiatives to enhance pediatric healthcare access and nascent but expanding medical tourism sectors.

Segmentation trends highlight the increasing demand for advanced structural heart defect closure devices and sophisticated balloon and stent technologies. The market for devices addressing conditions such as atrial septal defects (ASD) and patent ductus arteriosus (PDA) remains robust, while innovations for more complex ventricular septal defects (VSD) and specific valvular conditions are gaining traction. Hospitals with dedicated pediatric cardiology departments continue to be the predominant end-users, given the intensive care requirements and specialized equipment needed for these procedures. However, there is an evolving trend towards establishing specialized pediatric cardiac clinics and, for simpler procedures, potentially ambulatory surgical centers, aimed at improving accessibility and reducing healthcare costs. This intricate interplay of trends is collectively shaping a dynamic and expanding global market for pediatric interventional cardiology.

User inquiries concerning the influence of Artificial Intelligence (AI) on the Pediatric Interventional Cardiology Market frequently highlight its potential to revolutionize diagnostic accuracy, optimize procedural planning, and personalize treatment protocols for the nuanced needs of young patients with complex congenital heart conditions. A central theme is the expectation that AI can significantly enhance the interpretation of advanced imaging data, predict long-term patient outcomes with greater precision, and provide real-time guidance during intricate catheter-based interventions. While there is considerable optimism regarding efficiency and safety improvements, concerns are also raised regarding the validation and explainability of AI algorithms across diverse pediatric demographics, data privacy implications, and the seamless integration of these sophisticated tools into existing clinical workflows and training programs for specialized clinicians.

The integration of AI technologies is poised to profoundly impact various stages of pediatric cardiac care, from initial screening to post-procedural monitoring. In diagnostics, machine learning algorithms excel at analyzing vast quantities of medical imaging data, including echocardiograms, cardiac MRI, and CT scans, to identify subtle anatomical anomalies and functional impairments indicative of congenital heart defects. This capability can lead to earlier and more accurate diagnoses, enabling timely interventions that are critical for improved patient outcomes. AI-driven predictive analytics can also assess individual patient risk factors and disease progression, empowering clinicians to make proactive treatment decisions and develop highly personalized care plans tailored to each child's specific condition and developmental stage.

During interventional procedures, AI contributes significantly to pre-procedural planning by generating patient-specific 3D anatomical models from imaging data. These models allow interventional cardiologists to virtually simulate procedures, identify potential challenges, and determine the optimal device size and placement before entering the cath lab. This meticulous planning minimizes procedural time, reduces radiation exposure for both patient and staff, and enhances the overall safety and efficacy of the intervention. Furthermore, AI-powered systems can provide real-time image analysis and navigation assistance, helping cardiologists precisely guide catheters and devices through complex cardiac structures. Post-procedure, AI algorithms can continuously monitor physiological data, detecting early signs of complications or anomalies and alerting care teams, thereby ensuring vigilant follow-up and optimizing long-term patient management. AI also promises to transform professional training by offering realistic simulation environments and access to vast case databases for learning.

The Pediatric Interventional Cardiology Market operates within a complex ecosystem where various drivers, restraints, and opportunities exert significant influence, collectively shaping its trajectory and overall impact. A primary driving force is the consistently high global incidence of congenital heart defects (CHD), which necessitates a sustained and growing demand for specialized diagnostic and therapeutic interventions. This intrinsic demand is further amplified by continuous and rapid technological advancements in medical devices, including the development of smaller, more flexible, and safer catheters, stents, and closure devices specifically engineered for the unique anatomical challenges presented by pediatric patients. Moreover, the increasing preference for minimally invasive procedures among both healthcare providers and parents, owing to their benefits of reduced recovery times, less pain, and lower complication rates compared to traditional open-heart surgery, significantly propels market expansion. Concurrently, government and private sector investments in improving pediatric healthcare infrastructure and increasing awareness campaigns contribute to the broader adoption of these advanced cardiac solutions.

Despite the robust growth drivers, the market faces several notable restraints that temper its expansion. A significant barrier is the inherently high cost associated with advanced interventional devices and the complex procedures themselves, which can be prohibitive for healthcare systems in resource-limited settings or for patients without adequate insurance coverage. Another critical restraint is the global scarcity of highly specialized pediatric interventional cardiologists, anesthesiologists, and support staff, whose expertise is indispensable for safely and effectively performing these intricate procedures. Furthermore, the stringent and lengthy regulatory approval processes for novel medical devices, coupled with the complexities of reimbursement policies that vary significantly across different countries and healthcare payers, can delay market entry for innovative products and limit their widespread accessibility, thus impeding the market's full potential.

However, substantial opportunities exist that promise to unlock further growth and address current unmet needs within the pediatric interventional cardiology landscape. Emerging economies, particularly in Asia Pacific, Latin America, and parts of Africa, represent vast untapped markets where improving healthcare access, increasing disposable incomes, and growing awareness are creating significant demand for advanced cardiac care. The burgeoning field of personalized medicine, leveraging advanced manufacturing techniques such as 3D printing for patient-specific implants and tailored procedural planning, presents a transformative opportunity to enhance treatment efficacy and reduce complications. Additionally, the increasing integration of artificial intelligence and machine learning for predictive diagnostics, real-time procedural guidance, and optimized patient management offers revolutionary avenues for improving outcomes and operational efficiency. Continued innovation in bioresorbable materials for implants, advanced imaging fusion technologies, and telemedicine solutions for remote consultation and follow-up care are also pivotal in expanding market reach and enhancing the quality of pediatric cardiac interventions.

The Pediatric Interventional Cardiology Market is comprehensively segmented to provide granular insights into its multifaceted structure, allowing for a thorough understanding of product demand, application areas, and end-user adoption patterns. These segmentations are critical for market players to identify specific growth avenues, develop targeted strategies, and innovate in areas that address pressing clinical needs. The unique physiological characteristics of pediatric patients, including varying sizes from neonates to adolescents and the wide spectrum of congenital heart defects, necessitate a highly specialized approach to market segmentation, reflecting the precision and customization required in device design and procedural execution. This detailed analysis ensures that market trends and opportunities are captured effectively across all relevant dimensions.

Segmentation by product type typically includes diagnostic catheters, therapeutic catheters, septal occluders, stents, balloons, and guidewires. Diagnostic catheters are essential for accurately assessing cardiac anatomy and function, providing critical information before intervention. Therapeutic catheters, which encompass balloon dilation catheters for opening narrowed vessels or valves, embolization coils for closing abnormal connections, and biopsy devices, are crucial for corrective procedures. Septal occluders, specifically designed for closing conditions like Atrial Septal Defect (ASD), Ventricular Septal Defect (VSD), and Patent Ductus Arteriosus (PDA), hold a significant market share due to the prevalence of these defects. Stents, including specialized pulmonary artery and aortic stents, are vital for maintaining vessel patency, while various types of balloons are used for valvuloplasty and angioplasty. Continuous innovation in these product categories focuses on miniaturization, enhanced flexibility, improved biocompatibility, and advanced imaging compatibility to meet the specific requirements of pediatric patients.

Further segmentation by indication categorizes the market based on the specific congenital heart defects treated, such as Atrial Septal Defect (ASD), Ventricular Septal Defect (VSD), Patent Ductus Arteriosus (PDA), Pulmonary Stenosis (PS), Aortic Stenosis (AS), Coarctation of Aorta, and other complex anomalies. The prevalence rates and typical age of intervention for each condition directly influence the demand for specific devices. For example, PDA and ASD closures are among the most common interventional procedures. End-user segmentation largely comprises hospitals, specialized pediatric cardiology clinics, and a growing, albeit smaller, segment of ambulatory surgical centers. Hospitals, particularly those equipped with dedicated pediatric cardiac catheterization laboratories and intensive care units, remain the primary end-users due to the requirement for extensive infrastructure, multidisciplinary teams, and advanced support systems necessary for managing the critical and often complex cases encountered in pediatric interventional cardiology. The expanding role of specialized clinics for diagnostics and follow-up, and the potential for ASCs in less complex interventions, reflects an evolving landscape aimed at optimizing patient care pathways.

The value chain for the Pediatric Interventional Cardiology Market intricately maps the journey of specialized medical devices from fundamental raw materials through to their ultimate application in patient care, highlighting the interdependent relationships among various stakeholders. At the upstream segment, the process begins with the sourcing of highly specialized, medical-grade raw materials such, as advanced polymers like silicone and fluoropolymers, biocompatible metals such as nitinol and stainless steel, and various textile components. These materials must meet exceptionally stringent quality and safety standards to ensure they are suitable for implantation and prolonged contact with human tissues, particularly in vulnerable pediatric populations. Research and development activities, often involving collaborations with universities and clinical experts, are critical at this initial stage to innovate new materials and designs that optimize device performance, reduce invasiveness, and enhance safety, addressing the unique physiological demands of growing children.

The midstream segment of the value chain is dominated by medical device manufacturers who transform these raw materials and components into finished pediatric interventional cardiology products. This phase involves sophisticated engineering, precision manufacturing, assembly, and rigorous quality control processes. Specialized techniques are employed to create miniaturized devices with intricate designs, ensuring flexibility, durability, and atraumatic navigation within delicate cardiac structures. Extensive pre-clinical testing and clinical trials are conducted to validate the safety and efficacy of these devices, a prerequisite for obtaining necessary regulatory approvals from authoritative bodies such as the FDA, European Medicines Agency (EMA), and other national health ministries. Branding, marketing, and medical education initiatives also commence here, aimed at informing and training pediatric cardiologists and healthcare providers about the proper use, benefits, and technical specifications of these specialized products.

Downstream activities focus on the distribution, sales, and end-use of these advanced medical devices. Distribution channels are typically a hybrid model, utilizing direct sales forces for major hospital networks and key opinion leaders to facilitate personalized engagement, product training, and technical support. Indirect distribution, through specialized medical distributors, is crucial for broader market penetration, particularly in reaching smaller clinics and expanding into international markets where direct presence may be challenging. Hospitals, especially those with dedicated pediatric cardiology departments and state-of-the-art catheterization laboratories, represent the primary end-users, acquiring and deploying these devices for diagnostic and therapeutic procedures. The culmination of the value chain occurs when skilled pediatric interventional cardiologists utilize these devices to successfully treat complex congenital heart defects, improving the health and prognosis of young patients, followed by comprehensive post-procedural care and long-term monitoring.

The core potential customers and primary end-users within the Pediatric Interventional Cardiology Market are highly specialized healthcare institutions and medical professionals dedicated to the diagnosis, treatment, and management of cardiovascular conditions in pediatric populations. Foremost among these are large hospitals and academic medical centers that house comprehensive pediatric cardiology departments, equipped with advanced cardiac catheterization laboratories, specialized imaging facilities, and dedicated pediatric intensive care units. These institutions require a full spectrum of interventional devices, ranging from diagnostic catheters to therapeutic implants, alongside ongoing technical support and training for their highly specialized medical teams. Their purchasing decisions are critically influenced by factors such as clinical evidence of device efficacy and safety, technological advancements, ease of use, and the availability of robust after-sales service and educational programs for complex procedures.

Beyond major hospital systems, specialized pediatric cardiology clinics also represent a significant, albeit often secondary, customer segment. While these clinics may not possess the full interventional capabilities of larger hospitals, they play a crucial role in early diagnosis, patient assessment, pre-procedural evaluation, and long-term post-procedural follow-up care. Consequently, they are key consumers of diagnostic tools, non-invasive monitoring equipment, and educational resources related to pediatric cardiac conditions. These clinics frequently serve as referral centers, directing patients requiring interventional procedures to larger, more equipped hospital facilities. Their growing number, particularly in urban and suburban areas, indicates an expanding network of care that influences market demand for specialized pediatric cardiac products.

Furthermore, ambulatory surgical centers (ASCs) are gradually emerging as potential customers, primarily for less complex and well-established pediatric interventional procedures that can be performed safely in an outpatient setting, reducing hospital stay costs. As device technology continues to advance, leading to smaller profiles and enhanced safety, and as procedural protocols become more standardized, the scope of procedures feasible in ASCs may expand. Government healthcare programs and private health insurance providers also act as influential indirect customers, as their reimbursement policies and funding allocations significantly dictate the accessibility and affordability of pediatric interventional cardiology procedures and devices. Engaging with these diverse customer segments requires a nuanced approach, understanding their specific needs, procurement processes, and patient care models to ensure successful market penetration and sustained growth.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2032 | USD 3.15 Billion |

| Growth Rate | CAGR 7.8% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Edwards Lifesciences Corporation, Cardinal Health Inc., B. Braun Melsungen AG, Cook Medical, GE Healthcare, Siemens Healthineers AG, Philips Healthcare, Getinge AB, Terumo Corporation, Teleflex Incorporated, Becton, Dickinson and Company (BD), Merit Medical Systems Inc., LivaNova PLC, CryoLife, Inc., W. L. Gore & Associates, Inc., Biosense Webster, Inc. (Johnson & Johnson), NuMED, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Pediatric Interventional Cardiology Market is fundamentally driven by a dynamic and continuously evolving technological landscape, where innovation is paramount to improving diagnostic accuracy, enhancing procedural safety, and expanding treatment possibilities for young patients with complex heart conditions. Central to this landscape are advanced medical imaging technologies, including high-resolution 3D echocardiography, cardiac Magnetic Resonance Imaging (MRI), and multidetector Computed Tomography (CT) angiography. These modalities provide extraordinarily detailed anatomical and functional assessments of the heart and great vessels, which are indispensable for precise diagnosis, comprehensive pre-procedural planning, and real-time guidance during interventions. The ability to visualize intricate congenital defects with exceptional clarity aids interventional cardiologists in navigating delicate cardiac structures, optimizing device selection, and minimizing radiation exposure, a crucial consideration in the pediatric population.

Beyond imaging, the development of specialized and miniaturized interventional devices constitutes another critical pillar of the technology landscape. This includes a new generation of smaller profile catheters, guidewires, and delivery systems meticulously engineered to navigate the delicate and often smaller vascular pathways of neonates, infants, and children without causing trauma. Significant advancements are observed in the design of septal occluders, focusing on enhanced conformability to tissue, superior biocompatibility, and improved retrievability to allow for repositioning. Similarly, innovations in stents for pediatric use emphasize greater flexibility, longer durability, and the exploration of bioresorbable materials that dissolve naturally over time, eliminating the need for future interventions and minimizing long-term foreign body presence. Furthermore, drug-eluting stents are being investigated for their potential to prevent restenosis in specific pediatric arterial segments, although their clinical application requires extensive validation for this unique patient group.

Emerging and disruptive technologies are also increasingly shaping the future of pediatric interventional cardiology. Robotic assistance systems are beginning to be explored for their potential to offer enhanced dexterity, stability, and precision during complex catheter-based procedures, potentially reducing operator fatigue and increasing procedural consistency. Artificial intelligence and machine learning algorithms are transforming diagnostics through automated image analysis and predictive modeling, as well as optimizing procedural planning by generating patient-specific 3D printed heart models for simulation. Telemedicine and remote monitoring technologies are improving access to specialized care, particularly for follow-up appointments and chronic condition management in geographically dispersed pediatric populations, ensuring continuity of care. These technological advancements collectively drive the market towards safer, more effective, and increasingly accessible solutions, continually pushing the boundaries of what is possible in treating congenital and acquired heart diseases in children.

The market is projected to experience a robust Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032, driven by continuous innovation and increasing demand for minimally invasive treatments for pediatric heart conditions.

Key growth drivers include the rising global incidence of congenital heart defects, significant technological advancements in interventional devices, and a growing preference for less invasive procedures that offer quicker recovery and fewer complications for young patients.

The Asia Pacific region is anticipated to be the fastest-growing market due to improving healthcare infrastructure, rising awareness, and a large patient population, while North America and Europe will continue to hold substantial market shares as established leaders.

AI is profoundly impacting the market by enhancing diagnostic accuracy, optimizing pre-procedural planning through 3D modeling, providing real-time guidance during interventions, and improving patient outcome predictions, leading to safer and more precise treatments for children.

Major challenges include the high cost of advanced interventional devices and procedures, the scarcity of highly skilled pediatric interventional cardiologists, and complex regulatory approval processes that can hinder market entry and widespread adoption of new technologies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.