ID : MRU_ 429326 | Date : Oct, 2025 | Pages : 241 | Region : Global | Publisher : MRU

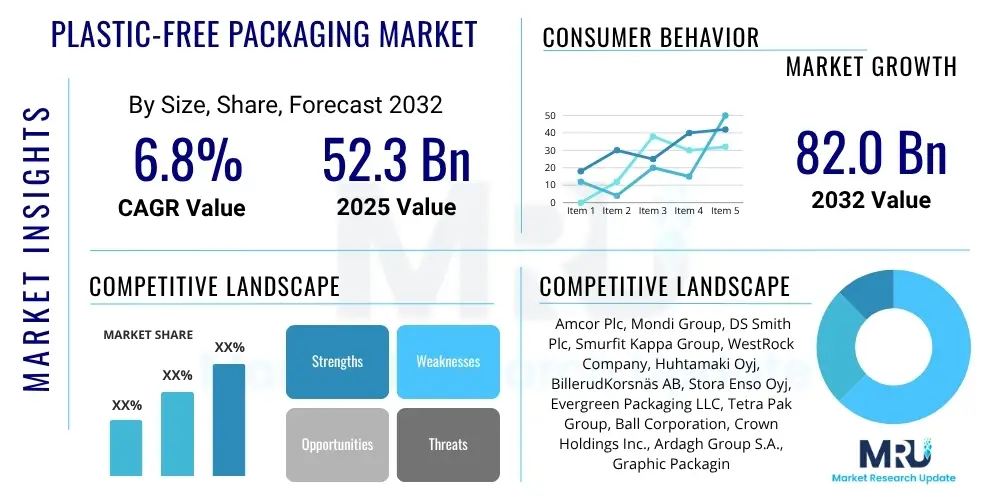

The Plastic-free Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 52.3 billion in 2025 and is projected to reach USD 82.0 billion by the end of the forecast period in 2032.

The Plastic-free Packaging Market encompasses the development, production, and adoption of packaging solutions that do not contain conventional plastics, aiming to reduce environmental pollution and promote circular economy principles. These solutions primarily include materials like paper and paperboard, glass, metal, and innovative bioplastics or compostable materials. Major applications span across diverse industries such as food and beverages, personal care and cosmetics, pharmaceuticals, and e-commerce, driven by escalating consumer demand for sustainable products and increasingly stringent environmental regulations. The core benefit of plastic-free packaging is its reduced ecological footprint, contributing to lower plastic waste in landfills and oceans, often offering biodegradability or enhanced recyclability. This market growth is significantly propelled by rising environmental consciousness among consumers and corporations, alongside global legislative actions pushing for plastic reduction.

The Plastic-free Packaging Market is experiencing robust expansion, fundamentally reshaped by global sustainability imperatives and a concerted shift away from traditional plastics. Business trends indicate a strong emphasis on research and development into novel, high-performance alternative materials, alongside strategic collaborations between packaging manufacturers and consumer goods brands to integrate these solutions into their product lines. There is also a notable trend towards lightweighting and optimizing existing plastic-free materials for cost-effectiveness and scalability. Regionally, Europe and North America lead in adoption, driven by progressive regulations and high consumer awareness, while the Asia Pacific market is poised for significant growth, spurred by rapid economic development and increasing environmental concerns. Segment-wise, the food and beverage industry remains the largest application area, demanding versatile and safe packaging, while materials such as paper and paperboard continue to dominate due to their established infrastructure and cost-efficiency, though advanced bioplastics are gaining traction for specialized applications.

Users frequently inquire about the transformative potential of Artificial intelligence (AI) in revolutionizing the plastic-free packaging sector, focusing on how AI can accelerate sustainable innovation, optimize production processes, and enhance end-of-life management for these materials. Common questions revolve around AI's ability to identify and develop new bio-based polymers, improve the barrier properties of paper-based packaging, or predict the shelf-life impacts of novel sustainable materials. Furthermore, there is significant interest in how AI can streamline supply chain logistics for plastic-free components, minimize waste during manufacturing, and even empower consumers through intelligent recycling guidance. The overarching expectation is that AI will serve as a critical enabler, addressing current limitations in material science, cost, and infrastructure, thereby making plastic-free solutions more viable and widespread.

AI's influence extends across the entire lifecycle of plastic-free packaging, from initial design and material selection to manufacturing and waste management. Its analytical capabilities allow for rapid screening and simulation of new material compositions, predicting performance characteristics and environmental impact before costly physical prototypes are developed. This significantly accelerates the pace of innovation for compostable, biodegradable, and recyclable alternatives, helping overcome technical hurdles such as moisture barriers or structural integrity. Moreover, AI-driven optimization in production lines can reduce material waste, energy consumption, and operational costs, making plastic-free options more economically competitive.

The Plastic-free Packaging Market is dynamically shaped by a confluence of driving forces, significant restraints, and emerging opportunities, all underpinned by various impact forces. Key drivers include heightened consumer awareness and demand for eco-friendly products, increasingly stringent governmental regulations worldwide aiming to curb plastic pollution, and the ambitious corporate sustainability goals adopted by major brands. These factors collectively push industries to innovate and adopt alternatives to conventional plastic. However, the market faces considerable restraints such as the often higher cost of alternative materials compared to plastics, the performance limitations of some sustainable options (e.g., shelf-life, barrier properties), and the lack of comprehensive recycling or composting infrastructure for novel materials. Overcoming these challenges requires continuous innovation and investment.

Opportunities in this market are abundant, particularly in the development of advanced bio-based and compostable materials that offer comparable performance to plastics, the expansion of plastic-free solutions into fast-growing sectors like e-commerce and ready-to-eat foods, and the implementation of circular economy models that emphasize reuse and refill. Innovations in coating technologies for paper and paperboard, alongside lightweighting techniques for glass and metal packaging, also present significant growth avenues. The interplay of these drivers and opportunities suggests a robust trajectory for the market, provided the existing restraints can be effectively managed through technological advancements and policy support.

Impact forces such as regulatory pressure from governments imposing plastic bans and taxes, evolving consumer preferences dictating purchasing decisions, and technological breakthroughs in material science are constantly reshaping the competitive landscape. Economic factors influencing the cost of raw materials and manufacturing, alongside global supply chain stability, also play a crucial role in the market's development and adoption rates of plastic-free solutions. Furthermore, brand reputation and corporate social responsibility initiatives are increasingly becoming powerful drivers for companies to adopt sustainable packaging, recognizing its positive impact on consumer perception and brand loyalty.

The Plastic-free Packaging Market is comprehensively segmented by material type, application, and packaging type, providing a granular view of its diverse dynamics and growth areas. Material segmentation is crucial as it defines the core components of plastic-free solutions, encompassing everything from traditional paper and glass to innovative bioplastics. Application segmentation highlights the various end-use industries driving demand, indicating where the most significant shifts from plastic are occurring. Packaging type segmentation differentiates between rigid and flexible formats, reflecting the varied functional requirements across product categories and consumer needs.

Understanding these segments is vital for stakeholders to identify specific market niches, tailor product development, and formulate targeted marketing strategies. Each segment exhibits unique growth patterns influenced by factors such as regulatory environments, consumer preferences, and technological advancements specific to that material or application. The interplay between these segments often dictates the overall pace and direction of market evolution, with cross-segment innovations frequently emerging to address multifaceted sustainability and performance demands. This detailed segmentation enables a more precise analysis of market opportunities and challenges, facilitating informed strategic decision-making across the value chain.

The value chain of the Plastic-free Packaging Market begins with upstream activities focused on the sourcing and processing of raw materials. This segment includes suppliers of pulp and timber for paper and paperboard, silica for glass, various metal ores for aluminum and steel, and agricultural feedstocks or microorganisms for bioplastics. These raw material producers are crucial foundational elements, dictating the initial cost, sustainability profile, and availability of resources for plastic-free alternatives. Innovations at this stage, such as sustainable forestry practices or advancements in biopolymer synthesis, directly influence the downstream capabilities and overall market viability. Efficient and ethical sourcing practices are increasingly scrutinized by consumers and regulators, adding complexity to this foundational layer.

Moving downstream, the value chain involves converters and packaging manufacturers who transform these raw materials into finished packaging products. This stage encompasses design, printing, forming, and assembly of various packaging formats, from rigid containers to flexible films. Key players here invest heavily in manufacturing technologies that can handle diverse plastic-free materials, ensuring functional integrity, barrier properties, and aesthetic appeal. The distribution channel then facilitates the movement of these finished packaging products to end-user industries, including direct sales from manufacturers to large consumer goods companies, through distributors serving smaller brands, and increasingly via specialized e-commerce platforms for sustainable packaging solutions. Both direct and indirect distribution channels play vital roles in ensuring market penetration and accessibility.

The final stage involves the adoption and integration of plastic-free packaging by consumer packaged goods (CPG) companies, retailers, and other end-users, who then present their products to the ultimate consumers. Post-consumption, the value chain extends to waste management infrastructure, including collection, sorting, recycling, and composting facilities. The effectiveness of this end-of-life stage is critical for truly closing the loop on plastic-free packaging and realizing its full environmental benefits. Challenges often arise from the lack of standardized infrastructure for novel plastic-free materials, underscoring the need for collaborative efforts across the entire value chain to ensure circularity.

The potential customers for plastic-free packaging solutions are highly diverse, spanning numerous industries driven by consumer demand for sustainability and evolving regulatory landscapes. End-users, or buyers, primarily include manufacturers of consumer packaged goods (CPG) across various sectors. The food and beverage industry represents a significant segment, with companies seeking plastic-free options for everything from beverages and dairy to snacks and fresh produce, aiming to meet consumer expectations for healthier and more environmentally responsible products. The shift towards plastic-free is particularly strong in premium and organic food categories, where sustainability aligns with brand values.

Beyond food and beverages, the personal care and cosmetics industry is a rapidly expanding customer base, with brands adopting plastic-free containers for shampoos, lotions, makeup, and other beauty products to appeal to eco-conscious consumers. Pharmaceutical companies are also exploring alternatives for primary and secondary packaging to enhance their environmental credentials, though this segment often requires solutions that meet stringent safety and regulatory standards. Additionally, the homecare sector, including cleaning supplies and detergents, is increasingly incorporating plastic-free packaging, driven by a growing awareness of household chemical impacts and plastic waste.

E-commerce platforms and their associated brands constitute another crucial customer segment. As online shopping continues to surge, the demand for lightweight, protective, and sustainable shipping packaging (e.g., paper-based mailers, void fill alternatives) is intensifying. Other industrial and electronics manufacturers are also integrating plastic-free packaging for components and finished goods, recognizing the broader environmental and brand perception benefits. Ultimately, any business seeking to enhance its sustainability profile, comply with environmental mandates, or cater to a growing segment of eco-aware consumers represents a potential customer for plastic-free packaging solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 52.3 Billion |

| Market Forecast in 2032 | USD 82.0 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amcor Plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group, WestRock Company, Huhtamaki Oyj, BillerudKorsnäs AB, Stora Enso Oyj, Evergreen Packaging LLC, Tetra Pak Group, Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., Graphic Packaging International LLC, Elopak ASA, SIG Combibloc Group AG, Sealed Air Corporation, Berry Global Group Inc., Novamont S.p.A., AptarGroup Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Plastic-free Packaging Market is rapidly evolving, driven by the imperative to create sustainable alternatives that match or exceed the performance of traditional plastics. Significant advancements are being made in material science, particularly in the development of advanced bio-polymers derived from renewable resources such as starch, cellulose, lactic acid, and agricultural waste. These next-generation bioplastics are engineered to offer improved barrier properties against moisture and oxygen, enhanced mechanical strength, and biodegradability or compostability, addressing some of the historical limitations of early bioplastic formulations. Furthermore, research into novel materials like mycelium-based packaging, seaweed films, and other plant-derived fibers is pushing the boundaries of what is possible in fully compostable and naturally sourced solutions.

Beyond material innovation, packaging design and manufacturing technologies are undergoing a transformation. This includes the development of sophisticated barrier coatings for paper and paperboard, which allow these fiber-based materials to be used in applications previously dominated by plastic, such as liquid containers and grease-resistant food packaging. Precision manufacturing techniques for glass and metal packaging are focused on lightweighting to reduce carbon footprint during transport, while maintaining structural integrity and product protection. Digital printing technologies enable greater customization and flexibility in smaller batch runs, supporting brands in their transition to diverse plastic-free formats without excessive setup costs.

Moreover, smart packaging technologies are being integrated into plastic-free solutions, leveraging QR codes and NFC tags to provide consumers with detailed information on product origin, disposal instructions, and circular economy initiatives. These digital tools enhance transparency and educate consumers on proper waste sorting, which is crucial for the effective recycling and composting of plastic-free materials. The synergy between new material science, advanced manufacturing processes, and digital engagement tools is critical in creating a robust and scalable ecosystem for plastic-free packaging, ensuring both environmental benefits and functional performance for a wide array of applications.

The Plastic-free Packaging Market exhibits distinct regional dynamics, influenced by varying regulatory landscapes, consumer awareness levels, and industrial infrastructures. Europe stands as a frontrunner in the adoption of plastic-free packaging, largely due to stringent environmental regulations such as the EU Single-Use Plastics Directive and high consumer demand for sustainable products. Countries like Germany, France, and the UK have seen significant investments in circular economy initiatives and infrastructure for recycling and composting alternative materials, fostering a mature market for plastic-free solutions across multiple sectors.

North America, particularly the United States and Canada, is also witnessing substantial growth, driven by increasing corporate sustainability commitments and evolving state-level regulations, especially in coastal regions. Consumer awareness regarding plastic pollution is high, pushing brands to innovate and offer plastic-free options, particularly in food service, personal care, and e-commerce. The region benefits from a robust innovation ecosystem, with significant research and development efforts in bio-based materials and advanced recycling technologies.

The Asia Pacific region represents a rapidly expanding market for plastic-free packaging, fueled by a large population, growing urbanization, and increasing environmental concerns in countries like China, India, and Japan. While traditional plastic consumption remains high, government initiatives and a rising middle class with greater purchasing power are driving a gradual shift towards more sustainable alternatives, particularly in urban centers. This region also presents unique opportunities for novel, locally sourced plastic-free materials. Latin America, the Middle East, and Africa are emerging markets, characterized by growing awareness and nascent regulatory frameworks, with increasing investment in sustainable packaging solutions across key industries.

Plastic-free packaging refers to any packaging solution that does not contain conventional petroleum-based plastics. It typically utilizes materials such as paper, paperboard, glass, metal, or advanced bio-based and compostable polymers to minimize environmental impact and promote circularity.

It is crucial for reducing plastic pollution in oceans and landfills, mitigating climate change by lowering reliance on fossil fuels, and meeting growing consumer demand for sustainable products. It supports circular economy principles by promoting recyclable, compostable, or reusable materials.

Key materials include paper and paperboard (cardboard, molded fiber), glass (bottles, jars), metal (aluminum cans, steel containers), and innovative bioplastics (PLA, PHA, starch-based). Newer materials like bamboo, wood, seaweed, and mycelium are also emerging.

Significant challenges include the higher cost of alternative materials, limitations in performance (e.g., barrier properties, shelf-life for some products), and the need for robust infrastructure for recycling and composting these diverse new materials effectively at scale.

The food and beverage industry is a primary driver, alongside personal care and cosmetics, and the e-commerce sector. Pharmaceuticals and homecare products are also rapidly increasing their adoption, driven by regulatory pressures and consumer preferences for sustainability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.