ID : MRU_ 430747 | Date : Nov, 2025 | Pages : 251 | Region : Global | Publisher : MRU

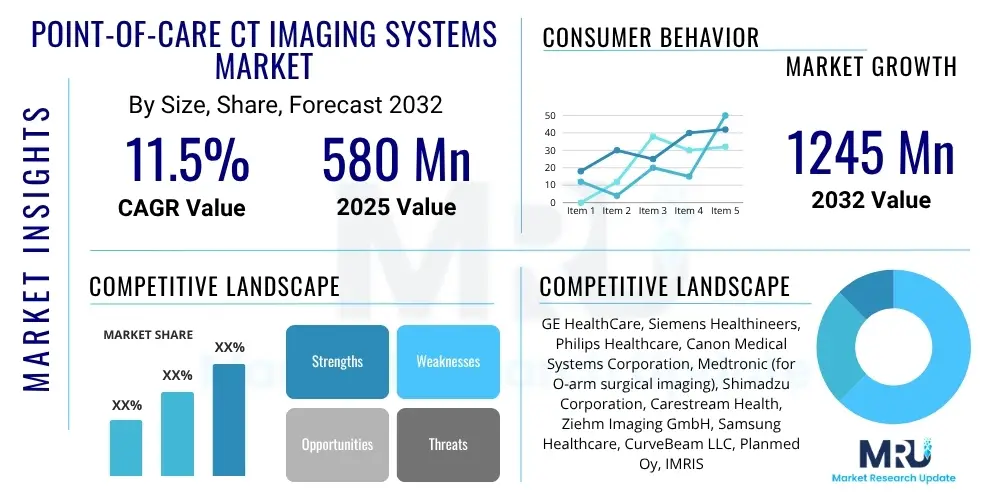

The Point-of-Care CT Imaging Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2032. The market is estimated at $580 million in 2025 and is projected to reach $1245 million by the end of the forecast period in 2032.

The Point-of-Care CT Imaging Systems Market encompasses specialized compact, often mobile, computed tomography (CT) scanners designed for immediate use at the patient's bedside or within clinical settings outside of a centralized radiology department. These systems offer significant advantages by bringing advanced diagnostic imaging directly to the patient, thereby minimizing the need for complex and risky patient transportation, particularly for critically ill or unstable individuals. This innovation addresses a crucial gap in healthcare delivery, providing rapid diagnostic capabilities in urgent and time-sensitive scenarios.

The products within this market range from head and neck specific CT scanners to more versatile extremity and full-body portable systems, all characterized by their smaller footprint and often lower radiation dose compared to conventional fixed CT machines. These systems are engineered for ease of operation in diverse environments, from emergency rooms and intensive care units to operating theaters and even remote field hospitals. Their design prioritizes quick setup and image acquisition, which is vital for improving patient throughput and facilitating quicker clinical decision-making. The inherent mobility and accessibility of these devices are central to their growing adoption across various medical disciplines.

Major applications for Point-of-Care CT imaging span across neurology for stroke and trauma assessment, orthopedics for fracture evaluation, emergency medicine for rapid diagnosis of acute conditions, and intensive care units for monitoring critically ill patients without transferring them. The primary benefits include reduced patient transport risks, accelerated diagnosis leading to improved clinical outcomes, enhanced workflow efficiency for healthcare providers, and the potential for cost savings associated with streamlined care pathways. Key driving factors for market growth include the increasing global incidence of neurological conditions and trauma, the rising demand for efficient and rapid diagnostic tools, technological advancements in miniaturization and image processing, and a growing geriatric population that often requires accessible and specialized care.

The Point-of-Care CT Imaging Systems market is undergoing transformative growth, propelled by a confluence of evolving business trends, significant regional expansion, and dynamic shifts across its various segments. Business trends highlight an intensified focus on innovation, with manufacturers investing heavily in developing more compact, user-friendly, and technologically advanced systems that integrate artificial intelligence and enhanced connectivity features. Strategic partnerships and collaborations between medical device companies and healthcare providers are becoming increasingly prevalent, aiming to optimize product deployment and extend market reach. Furthermore, there is a clear trend towards value-based care, wherein PoC CT systems contribute significantly by improving diagnostic efficiency and patient outcomes, thus driving their adoption in diverse clinical settings.

Regionally, North America and Europe currently dominate the market due to robust healthcare infrastructures, high adoption rates of advanced medical technologies, and significant investments in research and development. However, the Asia Pacific region is poised for substantial growth, driven by rapidly developing healthcare facilities, increasing healthcare expenditure, and a growing patient population with rising awareness of advanced diagnostic capabilities. Latin America and the Middle East and Africa are also emerging as promising markets, albeit from a lower base, fueled by improving healthcare access and government initiatives to modernize medical facilities. These regional trends underscore a global recognition of the inherent value and versatility of point-of-care imaging solutions in enhancing immediate patient care.

Segment-wise, the market is experiencing notable shifts. The neurology segment remains a primary growth driver, particularly for rapid stroke diagnosis, where immediate imaging can critically impact patient prognosis. Orthopedic applications are also expanding due to the convenience of bedside fracture assessment, reducing the need for patient transfers. In terms of product type, head CT systems continue to hold a significant share, but the demand for more versatile extremity and even portable full-body CT scanners is steadily increasing, reflecting the need for broader diagnostic capabilities at the point of care. End-user segments such as hospitals, emergency departments, and intensive care units are the largest adopters, with ambulatory surgical centers and specialty clinics also showing growing interest as they seek to enhance their diagnostic offerings and operational efficiency.

User questions regarding the impact of AI on Point-of-Care CT Imaging Systems frequently revolve around how artificial intelligence can enhance diagnostic accuracy, reduce scan times, simplify operational workflows, and ultimately improve patient outcomes. There is a keen interest in understanding AI's role in image reconstruction, automated lesion detection, and optimizing radiation dosage. Users also express curiosity about the integration challenges and the potential for AI to standardize interpretations across different clinical settings. Based on this analysis, AI is poised to revolutionize Point-of-Care CT imaging by significantly improving image quality through advanced reconstruction algorithms, enabling faster and more precise diagnoses via automated analysis and abnormality detection, and streamlining clinical workflows, thereby addressing key user expectations related to speed, precision, and operational efficiency within critical care environments.

The Point-of-Care CT Imaging Systems market is significantly shaped by a dynamic interplay of driving forces, inherent restraints, and emerging opportunities, all contributing to its overall impact and trajectory. Key drivers include the escalating global incidence of trauma and neurological emergencies like stroke, where rapid diagnosis is paramount to patient survival and recovery, directly benefiting from the immediate availability of PoC CT. Furthermore, the increasing prevalence of the geriatric population, who often require specialized and accessible diagnostic imaging due to mobility challenges and susceptibility to various conditions, fuels the demand for these systems. Technological advancements, particularly in detector technology, iterative reconstruction algorithms, and system miniaturization, have dramatically improved the quality and practicality of portable CT devices, making them more attractive to healthcare providers. The inherent benefits of PoC CT, such as reducing the risks associated with transporting critically ill patients to a centralized radiology department, and the resulting improvement in clinical workflow efficiency, are powerful motivators for adoption across various healthcare settings.

Despite these compelling drivers, the market faces several significant restraints that temper its growth. The high initial capital cost associated with acquiring sophisticated PoC CT imaging systems remains a substantial barrier for many healthcare facilities, particularly smaller hospitals or those in developing regions with limited budgets. Additionally, the need for specialized training for healthcare professionals to operate and interpret images from these advanced devices can impede widespread adoption, requiring ongoing investment in staff development. Regulatory hurdles and the complexities of obtaining approvals for new medical devices in diverse geographical regions add layers of cost and time to market entry for manufacturers. Furthermore, concerns regarding radiation exposure, although often lower with PoC CT compared to traditional systems, necessitate careful consideration and adherence to strict safety protocols, which can sometimes influence purchasing decisions.

Conversely, numerous opportunities are emerging that promise to unlock further growth potential for the PoC CT market. The integration of artificial intelligence and machine learning into these systems presents a transformative opportunity, offering advancements in image quality, automated diagnosis, and workflow optimization, making the devices even more efficient and precise. Expansion into untapped emerging markets, particularly in Asia Pacific and Latin America, where healthcare infrastructure is rapidly developing and there is a growing demand for advanced diagnostics, represents a significant growth avenue. The development of telehealth and remote diagnostic capabilities, enabled by PoC CT, allows for expert interpretations from afar, improving access to high-quality care in underserved areas. Furthermore, continuous innovation in miniaturization and the development of even more versatile, multi-purpose systems for new clinical applications beyond current primary uses (e.g., interventional radiology guidance or veterinary medicine) present exciting prospects. The impact forces collectively dictate the market's evolution, with drivers pushing for innovation and wider adoption, while restraints necessitate strategic development and cost-effectiveness, and opportunities point towards future technological convergence and geographical expansion.

The Point-of-Care CT Imaging Systems market is comprehensively segmented across several key dimensions, providing a detailed understanding of its diverse landscape and growth dynamics. These segments help in dissecting the market based on the type of product, the specific clinical applications where these systems are utilized, the end-user facilities adopting this technology, and the level of portability offered. Analyzing these segments is crucial for identifying distinct market niches, understanding varying customer needs, and formulating targeted marketing and development strategies. Each segment exhibits unique characteristics and growth trajectories, influenced by technological advancements, regulatory environments, and specific healthcare demands.

The value chain for Point-of-Care CT Imaging Systems is intricate, commencing from the upstream activities of raw material and component sourcing, through the manufacturing and assembly processes, and extending to the downstream stages of distribution, sales, installation, and post-sales support. Upstream activities involve a diverse set of suppliers providing critical components such as high-performance X-ray tubes, advanced flat-panel detectors, sophisticated image processing software, specialized power supplies, and precision mechanical parts for gantry construction. The quality and innovation of these components directly influence the performance, reliability, and cost-effectiveness of the final PoC CT system. Strong relationships with these specialized component suppliers are vital for manufacturers to ensure a consistent supply of cutting-edge technology and maintain competitive pricing. Research and development also play a significant role upstream, as manufacturers continuously innovate to enhance imaging capabilities, reduce system size, and improve user interface design.

Midstream activities focus on the actual manufacturing, assembly, and rigorous testing of the PoC CT imaging systems. This stage involves complex engineering processes, stringent quality control measures, and adherence to various international regulatory standards (e.g., FDA, CE Mark). Manufacturers are increasingly adopting lean manufacturing principles and automation to optimize production efficiency and ensure consistency. Downstream activities are centered on getting the finished products to end-users and providing ongoing support. This phase involves establishing robust distribution channels, which can be direct, involving sales teams selling directly to hospitals and clinics, or indirect, through a network of distributors and value-added resellers. Direct sales allow for closer customer relationships and tailored solutions, while indirect channels provide wider market reach and local presence, especially in geographically dispersed markets. Post-sales services, including installation, calibration, maintenance, technical support, and software upgrades, are critical for ensuring customer satisfaction, system longevity, and continued operational excellence. Training for clinical staff on system operation and image interpretation also forms a crucial part of the downstream value delivery.

The distribution channel for Point-of-Care CT Imaging Systems typically involves both direct and indirect models. Direct sales teams are often employed by major manufacturers to engage directly with large hospital networks, academic medical centers, and government healthcare providers, allowing for bespoke solutions, detailed product demonstrations, and comprehensive service contracts. This approach fosters strong client relationships and ensures direct feedback for product improvement. Indirect distribution, leveraging authorized distributors, local agents, and sometimes original equipment manufacturers (OEMs) who integrate the technology into broader solutions, is crucial for reaching smaller clinics, specialized practices, and international markets where local expertise and logistics support are essential. These indirect partners often provide localized sales, marketing, and first-line technical support, extending the manufacturer's reach and providing a localized service experience. Effective management of these diverse channels is key to ensuring broad market penetration and efficient delivery of these specialized imaging solutions.

The primary potential customers for Point-of-Care CT Imaging Systems are diverse healthcare entities that prioritize rapid, accessible, and high-quality diagnostic imaging for immediate patient management, particularly in critical and time-sensitive scenarios. Hospitals represent the largest segment of end-users, with specific departments such as emergency rooms, intensive care units (ICUs), neurological departments, and orthopedic wards being key adopters. In these settings, the ability to perform CT scans directly at the patient's bedside or within the department significantly reduces the logistical complexities and risks associated with transporting critically ill or unstable patients to a centralized radiology suite. The immediate availability of diagnostic results aids clinicians in making faster and more informed treatment decisions, which is crucial for conditions like stroke, severe trauma, or acute respiratory distress in ICU patients. These institutions seek solutions that enhance patient safety, improve workflow efficiency, and contribute to better clinical outcomes.

Beyond traditional hospital settings, specialized diagnostic imaging centers and outpatient clinics are increasingly recognizing the value of PoC CT systems. These centers aim to offer convenient and efficient imaging services to their patient populations, often focusing on specific areas like orthopedics or ENT, where the high-resolution capabilities of compact CT scanners provide significant diagnostic advantages. Ambulatory surgical centers (ASCs) are another growing customer segment, utilizing PoC CT for pre-operative assessment, intra-operative guidance for complex procedures, and post-operative evaluations, thereby streamlining their surgical workflows and enhancing patient care pathways. The integration of such technology allows ASCs to expand their service offerings and maintain a competitive edge by providing advanced diagnostics on-site, reducing the need for patients to travel to multiple facilities for their care journey.

Furthermore, non-traditional healthcare environments, such as military field hospitals, disaster relief organizations, and even specialized sports medicine clinics, represent significant potential customer bases. In military and disaster response scenarios, the portability and ruggedness of PoC CT systems are invaluable for assessing injuries in remote or challenging environments where conventional imaging infrastructure is unavailable or compromised. These systems provide critical diagnostic information quickly, enabling medical personnel to prioritize care and stabilize patients effectively. The demand from these varied end-users is driven by the overarching need for diagnostic flexibility, operational efficiency, and the unwavering commitment to delivering timely and effective patient care, irrespective of the clinical setting.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $580 million |

| Market Forecast in 2032 | $1245 million |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | GE HealthCare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems Corporation, Medtronic (for O-arm surgical imaging), Shimadzu Corporation, Carestream Health, Ziehm Imaging GmbH, Samsung Healthcare, CurveBeam LLC, Planmed Oy, IMRIS (a subsidiary of Deerfield Management), Brainlab AG, Fujifilm Healthcare, KONICA MINOLTA, Inc., Point-of-Care Medical Inc., Xoran Technologies LLC, Hyperfine, Inc., United Imaging Healthcare Co., Ltd., Shenzhen Anke High-tech Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Point-of-Care CT Imaging Systems market is characterized by continuous innovation aimed at enhancing image quality, increasing portability, reducing radiation dose, and improving workflow efficiency. Central to these advancements are next-generation flat-panel detectors, which offer superior spatial resolution, faster data acquisition rates, and improved dose efficiency compared to older detector technologies. These detectors enable manufacturers to produce sharper images with greater detail, crucial for diagnosing subtle pathologies in a compact system. Concurrently, iterative reconstruction algorithms have become a cornerstone, allowing for significant reductions in radiation dose without compromising diagnostic image quality. These advanced algorithms process raw data more efficiently, effectively suppressing noise and artifacts, which is particularly important in the dose-sensitive PoC environment where repeated scans might be necessary for patient monitoring.

The integration of artificial intelligence (AI) and machine learning (ML) is rapidly transforming the PoC CT technology landscape. AI-powered software is being deployed for various functions, including intelligent image reconstruction that can further accelerate processing and improve image fidelity, automated detection of abnormalities such as cerebral hemorrhages or fractures, and optimization of scan parameters to tailor radiation dose to individual patient needs. Furthermore, AI contributes to workflow automation, from patient positioning assistance to automated report generation, thereby enhancing efficiency in fast-paced clinical settings. These AI capabilities not only improve diagnostic accuracy and speed but also reduce the operational burden on clinicians, making PoC CT systems more intuitive and user-friendly, even for non-specialized personnel.

Beyond imaging and AI, other critical technological components include compact and powerful X-ray sources that deliver consistent performance in smaller footprints, advanced robotic assistance for precise patient positioning and gantry movement, and robust connectivity solutions. Cloud connectivity and telemedicine integration are becoming increasingly vital, allowing for remote access to images, expert interpretations from off-site radiologists, and seamless integration with hospital Picture Archiving and Communication Systems (PACS) and Electronic Health Records (EHR). This facilitates real-time data sharing and collaborative care, extending the reach of PoC CT beyond physical proximity. The continuous drive towards miniaturization, improved battery life for truly portable units, and enhanced cybersecurity features to protect patient data further define the evolving and highly dynamic technology landscape of this critical medical imaging market.

Point-of-Care CT Imaging Systems are compact, often mobile, computed tomography scanners designed to perform diagnostic imaging directly at the patient's bedside or within clinical departments like emergency rooms, ICUs, or operating theaters. They are engineered to provide rapid, high-resolution cross-sectional images, eliminating the need to transport critically ill or unstable patients to a centralized radiology department, thereby enhancing diagnostic speed and patient safety.

The main benefits of Point-of-Care CT include significantly reduced patient transport risks, especially for unstable or critical patients, leading to improved safety and comfort. They enable faster diagnosis and immediate clinical decision-making, which is crucial for time-sensitive conditions like stroke or trauma. Furthermore, these systems enhance workflow efficiency by bringing the imaging capability directly to the patient, minimizing logistical complexities and potentially improving overall patient outcomes through expedited care pathways.

Artificial intelligence profoundly impacts Point-of-Care CT by enhancing image quality through advanced reconstruction algorithms, reducing scan times, and optimizing radiation dosage. AI-powered software assists in automated anomaly detection, quickly highlighting potential pathologies such as hemorrhages or fractures, thereby improving diagnostic accuracy and consistency. It also streamlines workflow by automating various operational aspects, making the systems more efficient and user-friendly for healthcare professionals in fast-paced environments.

The Point-of-Care CT market faces several key challenges, including the high initial capital investment required for acquiring these advanced systems, which can be a barrier for smaller healthcare facilities. Additionally, the need for specialized training for operators and interpreting physicians, complex regulatory approval processes, and ongoing concerns about radiation exposure, despite dose optimization efforts, represent significant hurdles to widespread adoption and market growth.

Clinical applications that benefit most from Point-of-Care CT include Neurology, for rapid assessment of stroke, traumatic brain injuries, and intracranial hemorrhage; Orthopedics, for immediate diagnosis of fractures and dislocations; Emergency Medicine, for rapid evaluation of acute conditions in trauma patients; and Intensive Care Units, for monitoring critically ill patients without the risks of transport. ENT applications also leverage PoC CT for detailed imaging of specific anatomical structures.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.