ID : MRU_ 430538 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

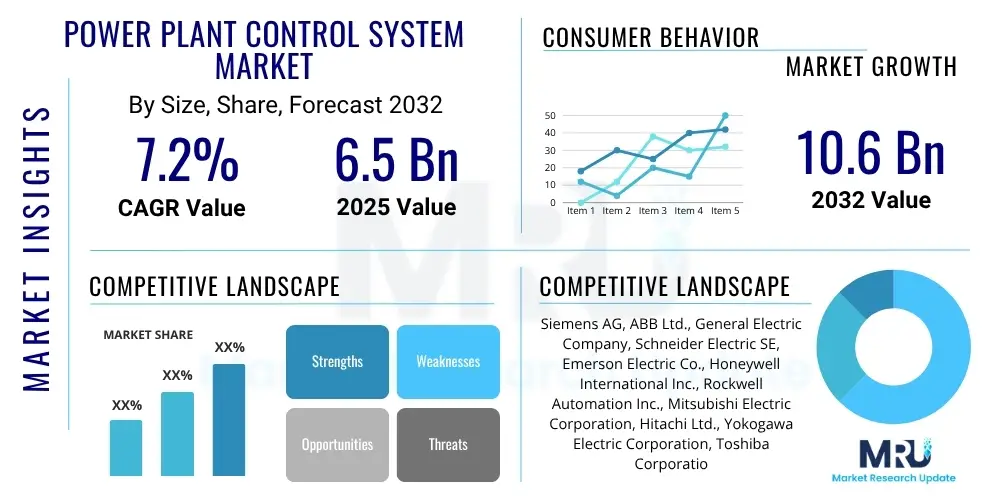

The Power Plant Control System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2032. The market is estimated at USD 6.5 Billion in 2025 and is projected to reach USD 10.6 Billion by the end of the forecast period in 2032.

The Power Plant Control System (PPCS) Market encompasses a sophisticated array of technologies and solutions that are indispensable for the efficient, safe, and reliable operation of diverse power generation facilities globally. These highly integrated systems are the nerve center of any power plant, coordinating and automating complex processes from fuel management and combustion dynamics to turbine governance, generator synchronization, and seamless integration with the electrical grid. A typical PPCS product portfolio includes advanced Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA) systems, and Programmable Logic Controllers (PLCs), intricately linked with a network of sensors, actuators, and intelligent software to precisely monitor and control critical parameters like temperature, pressure, flow rates, and rotational speeds. This intricate interplay ensures optimal operational stability and maximal energy output while adhering to strict performance benchmarks.

Major applications for Power Plant Control Systems span across the entire spectrum of electricity generation methods. This includes traditional thermal power plants, such as those fueled by coal, natural gas, or oil, where precise combustion control and turbine regulation are paramount. Hydroelectric power plants rely on PPCS for managing water flow, turbine speed, and generator output to optimize energy production. Nuclear power facilities employ highly redundant and secure control systems for critical safety functions and operational efficiency. Furthermore, with the accelerating global energy transition, PPCS are increasingly vital for renewable energy installations, including large-scale solar farms, expansive wind parks, geothermal plants, and biomass facilities, where they manage the inherent intermittency and ensure stable grid integration. The core benefits derived from implementing robust PPCS are manifold, significantly enhancing operational efficiency, substantially reducing fuel consumption, minimizing unplanned downtime through predictive capabilities, bolstering safety protocols for both personnel and equipment, and ensuring crucial compliance with increasingly stringent environmental regulations regarding emissions and pollution control.

The market is experiencing significant growth propelled by several influential driving factors. A primary catalyst is the persistent need to modernize aging power infrastructure, particularly within mature economies, where legacy control systems are becoming inefficient and difficult to maintain. This necessitates upgrades to advanced digital control solutions that offer enhanced capabilities and longevity. Concurrently, the relentless global demand for electricity, fueled by rapid industrialization, urbanization, and population growth in emerging economies, drives the construction of new power plants and mandates the optimization of existing assets. The accelerating global shift towards renewable energy sources presents a substantial market driver, as these variable generation methods require highly sophisticated and adaptable control systems to manage their intermittency and ensure stable, reliable integration into national grids. Moreover, the worldwide push for decarbonization and increasingly stringent environmental regulations compel power plant operators to invest in advanced control technologies that optimize combustion processes, reduce harmful emissions, and improve overall ecological footprints, thus positioning PPCS as a critical component for sustainable and compliant energy production.

The Power Plant Control System market is exhibiting a robust growth trajectory, shaped by a confluence of rapid technological advancements, evolving global energy policies, and an unyielding demand for greater operational efficiency and sustainability within the power sector. Current business trends underscore a profound shift towards digitalization and data-driven operations, with the pervasive integration of Industrial Internet of Things (IIoT) capabilities, advanced artificial intelligence (AI), and machine learning (ML) algorithms. These innovations are becoming critical enablers for predictive maintenance, real-time operational optimization, and fortifying cybersecurity defenses against escalating threats to critical infrastructure. System integrators and solution providers are strategically prioritizing the development of modular, scalable, and interoperable platforms designed to cater to a diverse range of plant requirements, from extensive legacy plant modernizations to the deployment of entirely new greenfield renewable energy projects. This focus on adaptable solutions reflects the dynamic nature of the energy landscape.

Geographically, the Asia Pacific (APAC) region is projected to lead market expansion, demonstrating the fastest growth rates driven by unprecedented industrialization, rapid urbanization, and massive government and private sector investments in new power generation capacities. Countries like China, India, and various Southeast Asian nations are at the forefront of this growth, fueling demand across both traditional and renewable energy sectors. North America and Europe, while representing more mature markets, exhibit stable and consistent demand primarily propelled by the imperative to modernize aging power infrastructure, strategically decommission fossil fuel plants, and aggressively integrate renewable energy sources into their grids. These regions also place a strong emphasis on enhancing energy efficiency, reducing carbon footprints, and bolstering grid resilience. Emerging markets across Latin America, the Middle East, and Africa (MEA) are also experiencing promising growth, largely attributed to ongoing infrastructure development initiatives and escalating energy demands, particularly within critical sectors such as oil and gas, mining, and manufacturing, which require dedicated and robust power solutions.

Analysis of market segmentation trends reveals a significant upswing in the software and services components of the PPCS market, a reflection of the increasing complexity, data-intensity, and advanced analytical requirements of modern power plant operations. While hardware continues to form the foundational infrastructure, the industry's strategic emphasis is progressively shifting towards sophisticated control algorithms, comprehensive analytics platforms, and end-to-end lifecycle services, encompassing installation, ongoing maintenance, essential upgrades, and advanced cybersecurity support. The Distributed Control System (DCS) segment maintains its dominant position due to its unparalleled capabilities for managing large-scale, highly complex power generation facilities. Concurrently, the Supervisory Control and Data Acquisition (SCADA) segment is gaining considerable traction, driven by its extensive utility in monitoring and controlling geographically dispersed assets, particularly prevalent within the rapidly expanding renewable energy sectors. From a plant type perspective, the most substantial growth is observed in control systems tailored for renewable energy plants, directly mirroring the global energy portfolio's decisive shift towards sustainable and environmentally friendly sources, while traditional thermal and nuclear power plants continue to drive demand for efficiency and safety enhancements.

Common user inquiries concerning the impact of Artificial Intelligence (AI) on Power Plant Control Systems frequently revolve around several critical areas: the potential for AI to dramatically enhance operational efficiency, its role in improving predictive maintenance capabilities to prevent costly outages, the optimization of energy production across diverse plant types, and its contribution to ensuring robust grid stability. Users are particularly keen to understand how AI can leverage vast streams of sensor data to detect subtle anomalies and incipient equipment failures long before they escalate into critical issues, thereby significantly reducing unplanned downtime and operational expenditure. Additionally, there is considerable interest in AI's capacity to optimize fuel combustion processes, intelligently manage the inherent intermittency of renewable energy sources, and enable autonomous, real-time responses to dynamic grid fluctuations. Alongside these transformative potentials, significant concerns are often raised regarding the cybersecurity implications of integrating AI into highly critical national infrastructure, the practical complexities associated with its implementation, and the imperative need for a highly skilled and adaptable workforce to effectively manage these increasingly sophisticated and autonomous systems.

Artificial Intelligence is unequivocally set to revolutionize Power Plant Control Systems by fundamentally transforming raw operational data into highly actionable insights, thereby initiating a paradigm shift from traditional reactive plant management to a proactive and even prescriptive approach. Through the application of sophisticated machine learning algorithms, AI possesses the unprecedented capability to analyze real-time operational data streaming from thousands of sensors across a power plant. This enables the identification of minute, often imperceptible, patterns indicative of impending equipment failures or operational inefficiencies, often long before conventional monitoring systems could detect them. This advanced predictive capability empowers operators to schedule maintenance precisely when needed, dramatically reducing unexpected outages, extending the operational lifespan of critical assets, and optimizing resource allocation. Furthermore, AI-driven optimization algorithms can meticulously fine-tune combustion processes in thermal plants, dynamically balance power output from multiple diverse sources within hybrid grids, and intelligently optimize renewable energy harvest based on advanced weather predictions, leading to substantial gains in overall efficiency and a significantly reduced environmental impact. The strategic integration of AI also promises to substantially enhance grid resilience by facilitating faster, more intelligent, and highly coordinated responses to sudden demand fluctuations and unforeseen supply interruptions, thereby ensuring significantly greater reliability and stability of electricity supply across the network.

While the benefits of AI integration into PPCS are profound, its adoption also introduces a new set of challenges that require careful consideration and strategic planning. Primarily, the enormous volume of sensitive operational data processed by AI systems becomes an attractive and vulnerable target for sophisticated cyber threats, necessitating the implementation of exceptionally robust and multi-layered cybersecurity measures. Moreover, the successful deployment and effective utilization of AI solutions demand significant upfront investment in advanced data infrastructure, substantial computational power, and the recruitment or training of specialized expertise in data science, AI engineering, and industrial automation. Integrating cutting-edge AI functionalities with existing, often proprietary, legacy control infrastructure can also present considerable compatibility issues, requiring complex engineering solutions and careful project management. Despite these complexities and investment requirements, the transformative potential for AI to unlock unprecedented levels of operational efficiency, enhance system reliability, and drive greater environmental sustainability firmly positions it as a pivotal and transformative force, poised to define the next generation of power plant operations and management. Stakeholders are keenly focused on understanding the tangible return on investment and the practical, phased steps required for seamless and secure AI integration into both existing and future control architectures.

The Power Plant Control System (PPCS) market is profoundly shaped by an intricate interplay of drivers, restraints, opportunities, and external impact forces that collectively dictate its growth trajectory and strategic evolution. A primary and persistent driver is the unceasing global demand for electricity, which is continuously propelled by burgeoning population growth, rapid industrialization, and accelerating urbanization, particularly prevalent in developing nations. This escalating demand necessitates both the development of new power generation capacities and the continuous optimization of existing facilities to meet energy requirements reliably. This is further complemented by the critical imperative to modernize aging power infrastructure within established economies, where legacy control systems are increasingly inefficient and prone to failure. The global energy transition towards decarbonization and the exponential growth in renewable energy installations, including solar, wind, and hydro, act as potent drivers, as these inherently intermittent sources demand highly sophisticated control systems for stable grid integration and optimized energy harvesting. Finally, increasingly stringent environmental regulations on emissions and pollution control compel power plant operators worldwide to adopt advanced control technologies that meticulously optimize combustion processes, significantly reduce the ecological footprint, and foster sustainable operational practices, thereby positioning PPCS as essential for regulatory compliance and environmental stewardship.

Despite the robust influence of these drivers, the market faces several significant restraints that challenge its expansion. The substantial initial capital investment required for the implementation, upgrading, and integration of sophisticated Power Plant Control Systems can act as a considerable barrier to entry and adoption, particularly for smaller operators or in economies facing budgetary constraints. The inherent complexity of seamlessly integrating new, advanced digital control systems with heterogeneous existing legacy infrastructure often leads to unforeseen compatibility issues, protracted project timelines, and consequently, inflated costs. A paramount concern is the escalating and evolving threat of cybersecurity breaches, as power plants represent critical national infrastructure; any vulnerability in their control systems can lead to catastrophic operational failures, grid instability, and potentially widespread disruption. This necessitates the integration of exceptionally robust and continuously updated cybersecurity measures, which are both technically challenging and financially intensive. Furthermore, a persistent shortage of highly skilled personnel capable of proficiently operating, maintaining, and troubleshooting these increasingly sophisticated digital control systems poses a significant operational challenge, potentially impacting adoption rates and the efficient utilization of advanced functionalities.

Conversely, numerous opportunities exist that promise substantial growth within the PPCS market. The deep integration of cutting-edge technologies such as Artificial Intelligence (AI) and Machine Learning (ML) for advanced predictive analytics, precise anomaly detection, and real-time operational optimization presents a transformative opportunity to dramatically enhance operational intelligence and efficiency across all power plant types. The continuous development and expansion of smart grids, which inherently require highly responsive, interconnected, and intelligent control systems, open entirely new avenues for innovation, market penetration, and value creation. A significant and economically viable potential lies in retrofitting existing power plants with modern control systems, offering a compelling alternative to new constructions while simultaneously achieving substantial improvements in performance, reliability, and regulatory compliance. Moreover, the burgeoning energy markets in the rapidly developing economies of the Asia Pacific, Latin America, and Africa offer substantial greenfield opportunities for the deployment of new power plant control solutions as these regions vigorously expand their power generation capacities to support economic growth. External impact forces play a critical role; rapid technological advancements in sensor technology, communication networks (e.g., 5G, industrial Ethernet), and data processing capabilities continuously push the boundaries of what PPCS can achieve. Global regulatory shifts towards stringent decarbonization targets and enhanced grid reliability worldwide fundamentally reshape investment priorities and technological adoption. Macroeconomic factors, including global economic conditions and geopolitical stability, can significantly influence investment cycles, project timelines, and market confidence. Finally, profound environmental concerns, particularly related to climate change mitigation and the imperative for sustainable development, remain a pivotal force, actively driving the demand for innovative and eco-friendly control system solutions.

The Power Plant Control System market is meticulously segmented to offer a granular and comprehensive understanding of its diverse components, the various technologies employed, the specific types of power plants they serve, and their distinct applications within these facilities. This detailed segmentation framework is crucial for a precise and nuanced analysis of prevailing market dynamics, enabling stakeholders to accurately identify specific growth pockets, pinpoint emerging trends, and understand evolving consumer preferences across different categories. The inherent structure of the market segmentation profoundly reflects the increasing complexity and technological sophistication required in modern power generation, encompassing a wide array of specialized solutions meticulously tailored to meet unique operational demands, comply with stringent regulatory requirements, and integrate the latest technological advancements within the dynamic energy sector. Gaining a thorough understanding of these intricate segments is paramount for all market participants, including technology providers, system integrators, and end-users, to formulate effective strategies, develop highly targeted solutions, and adeptly capitalize on both existing and nascent market opportunities.

The segmentation schema primarily categorizes the market based on several fundamental criteria: the constituent components that form a complete control system, the specific control system types (e.g., DCS, SCADA, PLC) that are predominantly employed, the wide range of power plant types (e.g., coal, gas, nuclear, renewable) that these systems are designed to serve, and their distinct functional applications (e.g., boiler control, turbine control, generator control) within these power generation facilities. This multi-faceted and exhaustive approach ensures that both solution suppliers and end-users can accurately identify, procure, and implement the most relevant, efficient, and technologically advanced solutions precisely suited for their particular operational needs and strategic objectives. The continuous evolution and transformation of these market segments are intrinsically linked to overarching technological innovation, significant shifts in global energy policies and regulatory frameworks, and the relentless industry-wide drive for enhanced efficiency, improved reliability, and greater sustainability in power generation infrastructure worldwide. Each defined segment and its nested sub-segments present a unique combination of growth drivers and specific challenges, collectively reflecting the profoundly dynamic and rapidly evolving nature of the global power sector and its intricate technological requirements.

The value chain for the Power Plant Control System market is an intricate and multi-layered ecosystem, meticulously orchestrated from the initial sourcing of raw materials to the final deployment and continuous operational maintenance of sophisticated control solutions. This complex chain commences with crucial upstream activities, which are primarily focused on the rigorous procurement of highly specialized raw materials, electronic components, and advanced semiconductors essential for the manufacturing of control system hardware. This stage is followed by the meticulous design and precision manufacturing of various hardware elements, including robust controllers, intelligent sensors, precision actuators, and reliable communication devices. Concurrently, specialized software development houses contribute invaluable intellectual property through the creation of cutting-edge SCADA, DCS, HMI, and advanced analytics platforms, which form the intelligent core of these systems. Key players operating within this upstream segment typically include highly specialized component manufacturers, global semiconductor companies, and innovative software developers who collectively provide the foundational technologies and critical intellectual property necessary for building robust and high-performing control systems.

Moving along the value chain, midstream activities predominantly involve the sophisticated integration and careful assembly of these diverse components into comprehensive and fully functional control systems. This critical stage is typically performed by large-scale Original Equipment Manufacturers (OEMs) and highly specialized system integrators who possess deep engineering expertise. These entities leverage their technical prowess to meticulously customize solutions, ensuring seamless compatibility, optimal performance, and robust reliability specifically tailored for a wide array of power plant configurations, operational requirements, and regulatory environments. The distribution channel within this market is multifaceted and highly adaptable, encompassing both direct and indirect sales approaches. Direct sales strategies are commonly employed for large-scale, complex projects involving major utility companies and new greenfield power plant constructions, where leading global control system vendors engage directly with the end-users to provide bespoke solutions. Conversely, indirect channels involve strategic partnerships with reputable engineering, procurement, and construction (EPC) firms, as well as a network of third-party distributors and local system integrators who effectively serve smaller projects, provide essential regional support, and offer value-added services such as local customization and post-installation support.

The downstream activities represent the culmination of the value chain, primarily focusing on the actual deployment, precise commissioning, and long-term operational support of the Power Plant Control Systems at the end-user facilities. This crucial stage is predominantly driven by power plant operators, national and regional utility companies, and Independent Power Producers (IPPs) who actively utilize these sophisticated systems for their daily operational management, continuous performance monitoring, and ensuring stringent regulatory compliance. A particularly critical part of the downstream value chain is dedicated to comprehensive post-sales services, which include routine and corrective maintenance, proactive troubleshooting, essential software updates, rigorous cybersecurity patches, and specialized operator training programs. These services are vital for ensuring the sustained efficiency, reliability, and security of the control infrastructure throughout its entire operational lifecycle, thereby maximizing the return on investment for end-users. The overall effectiveness and efficiency of the entire value chain are critically dependent on strong, transparent collaboration and seamless information flow among all participants, from the initial component suppliers to the ultimate end-users, ensuring that the delivered control solutions consistently meet and exceed stringent industry standards and complex operational demands.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2032 | USD 10.6 Billion |

| Growth Rate | 7.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., General Electric Company, Schneider Electric SE, Emerson Electric Co., Honeywell International Inc., Rockwell Automation Inc., Mitsubishi Electric Corporation, Hitachi Ltd., Yokogawa Electric Corporation, Toshiba Corporation, Eaton Corporation plc, Valmet Corporation, Fuji Electric Co. Ltd., Wood Group PLC, Capstone Green Energy Corporation, PowerSecure International Inc., Wartsila Corporation, Delta Controls, L&T Technology Services, Fuji Electric Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Power Plant Control System (PPCS) market is characterized by a rapidly evolving and highly dynamic technology landscape, consistently integrating cutting-edge advancements to effectively meet the escalating demands for superior efficiency, enhanced reliability, and fortified security in modern power generation. At its foundational core, the landscape relies heavily on established and proven technologies such as Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA) systems, and Programmable Logic Controllers (PLCs). These form the robust backbone of contemporary power plant operations, enabling precise monitoring, intricate control, and sophisticated automation of critical processes. DCS provides comprehensive plant-wide control for large-scale and complex operations, SCADA excels in monitoring and controlling geographically dispersed assets and collecting real-time operational data, while PLCs offer highly rugged and reliable control for discrete tasks and localized automation within larger facilities. These foundational systems are subject to continuous upgrades, incorporating improved processing power, advanced communication capabilities, and modular architectures to significantly enhance their scalability, flexibility, and overall performance.

A transformative trend profoundly influencing the technology landscape is the pervasive and expanding integration of the Industrial Internet of Things (IIoT). The deployment of IIoT sensors, smart devices, and interconnected equipment throughout power plants enables unprecedented levels of real-time data collection from a multitude of operational components, thereby facilitating immediate operational insights and highly effective condition monitoring. This voluminous influx of data is subsequently processed and rigorously analyzed using advanced analytics platforms, which increasingly incorporate sophisticated Artificial Intelligence (AI) and Machine Learning (ML) algorithms. AI and ML are instrumental in enabling highly accurate predictive maintenance by forecasting potential equipment failures, meticulously optimizing fuel consumption, precisely fine-tuning generation parameters for peak efficiency, and providing intelligent, proactive alerts. This technological evolution marks a significant shift from traditional reactive control to a more proactive, predictive, and ultimately prescriptive approach to plant management. These smart technologies are absolutely crucial for substantially improving overall equipment effectiveness (OEE), significantly reducing unplanned downtime, and optimizing operational expenditures across the entire power generation lifecycle.

Furthermore, robust and continuously evolving cybersecurity solutions have become an absolutely indispensable component of the PPCS technology landscape, given the critical national importance and inherent vulnerability of power infrastructure to malicious cyber threats. Advanced encryption protocols, sophisticated intrusion detection and prevention systems, secure remote access methodologies, and rigorous network segmentation are paramount to effectively protect sensitive control systems from an ever-increasing array of cyberattacks and ensure the fundamental resilience and uninterrupted operation of the electricity grid. Human Machine Interface (HMI) technologies are also rapidly advancing, offering more intuitive, highly graphical, and mobile-friendly interfaces that empower plant operators with enhanced visualization capabilities, real-time data access, and more effective control over complex processes. The judicious adoption of cloud computing for secure data storage, advanced analytical processing, and remote management is also steadily growing, offering considerable benefits in terms of scalability, flexibility, and cost efficiency, albeit with careful and continuous consideration of data sovereignty, security, and regulatory compliance. These myriad technological advancements collectively drive innovation within the PPCS market, making power generation operations smarter, more efficient, significantly more reliable, and inherently more secure against an increasingly complex threat landscape.

A Power Plant Control System (PPCS) is an integrated solution of hardware, software, and communication networks designed to monitor, control, and automate the intricate operations of a power generation facility. It is essential for ensuring efficient, safe, and reliable electricity production, optimizing performance, and maintaining grid stability by precisely managing all plant parameters.

Implementing advanced PPCS offers numerous benefits including significantly enhanced operational efficiency, substantial reductions in fuel consumption, minimized unplanned downtime through sophisticated predictive maintenance, improved safety protocols for both personnel and equipment, and crucial compliance with stringent environmental regulations, ultimately leading to lower operational costs and greater plant reliability.

AI is profoundly transforming PPCS by enabling advanced predictive maintenance and anomaly detection, optimizing energy output and fuel efficiency through intelligent algorithms, enhancing grid stability and the integration of intermittent renewables, and improving cybersecurity resilience, thereby shifting towards more autonomous and proactive plant management.

The Asia Pacific region is currently the fastest-growing market due to rapid industrialization, urbanization, and substantial investments in new power plant constructions. North America and Europe also demonstrate consistent demand, primarily driven by the imperative for infrastructure modernization, aggressive renewable energy integration efforts, and a strong focus on energy efficiency and environmental compliance.

The Power Plant Control System market faces several significant challenges, including the high initial capital investment required for implementation and upgrades, the inherent complexities associated with integrating new, advanced systems with existing legacy infrastructure, the escalating threat of sophisticated cybersecurity breaches targeting critical infrastructure, and a persistent shortage of highly skilled personnel capable of effectively operating and maintaining these advanced digital control systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.