ID : MRU_ 430613 | Date : Nov, 2025 | Pages : 248 | Region : Global | Publisher : MRU

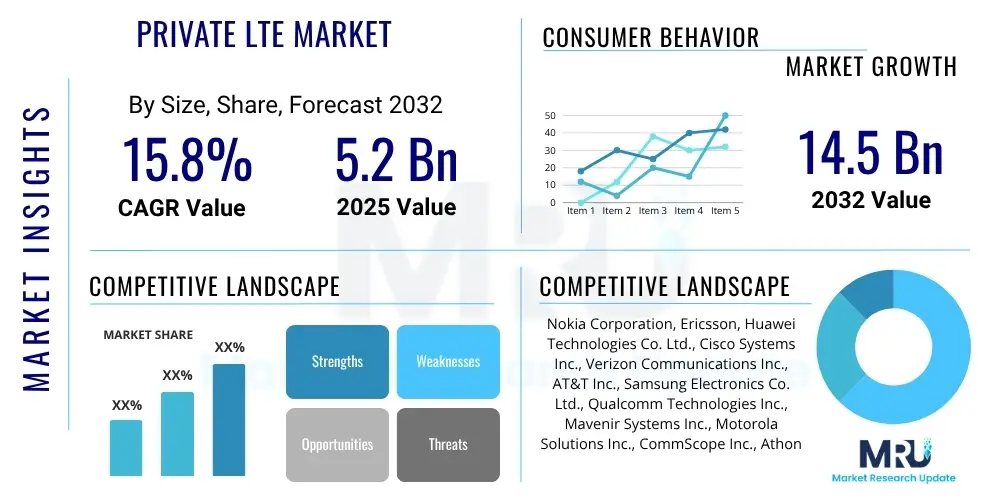

The Private LTE Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2032. The market is estimated at USD 5.2 Billion in 2025 and is projected to reach USD 14.5 Billion by the end of the forecast period in 2032.

The Private LTE Market signifies the deployment of dedicated, localized cellular networks designed for specific enterprises or organizations, offering enhanced security, reliability, and control over traditional public networks or Wi-Fi. These networks leverage established LTE technology, providing high-performance, low-latency connectivity crucial for mission-critical applications and industrial automation. Unlike public cellular networks, Private LTE deployments allow organizations to own and operate their infrastructure, tailoring network parameters to their unique operational requirements, ensuring robust performance even in challenging environments such as remote mining sites or bustling factory floors. This dedicated approach fosters superior data privacy and throughput, making it an indispensable asset for digital transformation initiatives across diverse sectors.

The core of a Private LTE system comprises a radio access network (RAN), including base stations and antennas, and a compact evolved packet core (EPC), alongside specialized user equipment (UE). These components work in unison to provide secure, robust communication. Major applications span industrial IoT (IIoT), critical communications for public safety, smart manufacturing, logistics, and resource extraction, where reliable connectivity is paramount. Benefits include superior coverage in challenging indoor and outdoor environments, enhanced security through dedicated infrastructure and encryption, predictable performance with guaranteed bandwidth, and the ability to prioritize specific traffic. The market is primarily driven by the escalating demand for secure, high-capacity, and low-latency connectivity to support the proliferation of IoT devices, the imperatives of Industry 4.0, and the need for operational resilience in critical infrastructure, positioning Private LTE as a foundational technology for modern enterprise connectivity.

The Private LTE Market is experiencing robust expansion driven by global industrial digitalization and the increasing sophistication of enterprise operational requirements. Business trends highlight a significant shift towards hybrid cloud and edge computing architectures, with Private LTE serving as the foundational connectivity layer for these distributed environments. Enterprises are increasingly seeking solutions that offer greater control over their network infrastructure, leading to a surge in direct deployments and partnerships with specialized service providers. Furthermore, the market is characterized by a growing interest in private network-as-a-service models, which reduce upfront capital expenditure and simplify network management for end-users, thereby accelerating adoption across various industries. This trend is complemented by the integration of artificial intelligence and machine learning for network optimization, predictive maintenance, and enhanced security.

Regional trends indicate North America and Europe as early adopters, propelled by supportive regulatory frameworks, such as the Citizens Broadband Radio Service (CBRS) in the US, and a strong impetus for Industry 4.0 in European manufacturing sectors. The Asia Pacific region is rapidly emerging as a significant growth hub, fueled by extensive industrialization, smart city initiatives, and substantial investments in advanced manufacturing and logistics infrastructure, particularly in countries like China, Japan, and India. Latin America and the Middle East & Africa regions are also witnessing increasing interest, driven by digital transformation agendas in oil and gas, mining, and public safety sectors, though adoption here is still in nascent stages. Governments in these regions are increasingly exploring private networks for public safety and critical national infrastructure projects.

Segment trends reveal that the manufacturing sector remains a dominant end-user, leveraging Private LTE for automation, real-time asset tracking, and remote control of machinery. The mining, oil & gas, and utilities sectors are also critical, relying on these networks for communication in harsh and remote environments, enhancing worker safety, and improving operational efficiency. Public safety agencies are adopting Private LTE for secure, resilient communication capabilities during emergencies. In terms of technology, the market is gradually transitioning towards Private 5G, as enterprises seek even lower latency and higher bandwidth capabilities, alongside exploring spectrum options including licensed, unlicensed, and shared access. Services and software components are gaining prominence as companies look for comprehensive solutions that include network design, deployment, and ongoing management, often seeking specialized system integrators and managed service providers.

Users frequently inquire about how artificial intelligence can optimize the performance, security, and operational efficiency of Private LTE networks, and how it can enable new applications. There are significant expectations regarding AI's role in automating complex network management tasks, enhancing predictive capabilities for maintenance and anomaly detection, and providing deeper insights into network usage and potential vulnerabilities. Common concerns revolve around the integration complexity of AI tools with existing Private LTE infrastructure, the data privacy implications of AI-driven analytics, and the need for specialized skills to deploy and manage AI-enhanced private networks. The overarching theme is a strong belief that AI will be a transformative force, enabling Private LTE to reach its full potential in supporting advanced industrial and enterprise applications.

The Private LTE Market is primarily driven by the escalating demands of Industry 4.0 and the pervasive proliferation of IoT devices across industrial and enterprise environments. The need for secure, reliable, and low-latency connectivity to support critical applications such as autonomous guided vehicles (AGVs), remote controlled machinery, and real-time sensor data analytics is a significant catalyst. Enterprises are increasingly seeking dedicated network solutions that offer superior control over their data, enhanced security features, and predictable performance, which traditional public networks or Wi-Fi struggle to provide consistently. This demand is further amplified by digital transformation initiatives globally, pushing organizations to adopt private networks for operational resilience and competitive advantage.

Despite strong drivers, the market faces several restraints. High initial investment costs for deploying Private LTE infrastructure can be a barrier for smaller enterprises or those with limited budgets. The complexity associated with spectrum acquisition and management, particularly in regions without established shared spectrum frameworks, presents a significant hurdle. Furthermore, a shortage of skilled personnel proficient in designing, deploying, and maintaining private cellular networks can impede adoption. Interoperability challenges between equipment from different vendors and concerns regarding potential vendor lock-in also contribute to market hesitation, requiring careful planning and standardization efforts to mitigate these issues.

Significant opportunities exist in the integration of Private LTE with emerging technologies like 5G New Radio (NR) and edge computing, which promise even greater performance enhancements and new application possibilities. The expansion into new vertical markets, including healthcare, smart cities, and agriculture, represents substantial untapped potential. Furthermore, the development of 'network-as-a-service' models is lowering the barrier to entry for many organizations, enabling them to leverage Private LTE benefits without extensive capital outlay. Regulatory initiatives supporting shared or unlicensed spectrum access, such as CBRS in the US, are opening new avenues for deployment, making Private LTE more accessible and cost-effective. These opportunities, coupled with ongoing technological advancements, are poised to accelerate market growth and foster innovation.

The Private LTE market is comprehensively segmented to reflect the diverse technological implementations, deployment models, and varied end-user applications that characterize this rapidly evolving domain. This segmentation helps to understand the market dynamics across different facets, providing granular insights into where growth is most prominent and what specific solutions are gaining traction. The key segments analyze the market based on its core components, the types of deployment, the frequency bands utilized, and the specific industries that are adopting these dedicated networks, thereby offering a multi-dimensional view of the market landscape.

The value chain for the Private LTE Market is intricate, involving a diverse set of stakeholders from raw material suppliers to end-users. At the upstream level, the chain begins with component manufacturers responsible for producing critical hardware such as chipsets, antennas, radio units (eNodeBs), and core network elements (EPCs). These suppliers often specialize in particular aspects of telecommunications technology, providing the foundational building blocks for private network infrastructure. Additionally, specialized software developers contribute core network software, network management systems, and security applications that are essential for the operation and optimization of Private LTE networks, ensuring functionality and robustness. Spectrum providers, whether national regulators or shared spectrum entities, also play a crucial upstream role by making the necessary frequencies available for deployment, thereby dictating market access and geographical reach for network operators.

Moving downstream, the value chain encompasses system integrators and network deployment specialists who are responsible for designing, installing, and configuring the Private LTE networks to meet specific enterprise requirements. These integrators often work closely with technology vendors to ensure seamless integration of hardware and software components. Managed service providers (MSPs) form another critical part of the downstream segment, offering ongoing operational support, maintenance, and network optimization services, which allow enterprises to focus on their core business operations without managing complex network infrastructure. These service providers ensure that the private network remains operational, secure, and performs optimally, offering a compelling proposition for organizations that lack in-house telecommunications expertise. The distribution channels play a pivotal role in connecting these technology providers and service integrators with the end-users.

The distribution channel primarily involves both direct and indirect models. Direct sales are often employed for large-scale enterprise clients or government entities where complex, bespoke solutions are required, involving direct engagement with technology vendors or major system integrators. This allows for highly customized network designs and close collaboration throughout the project lifecycle. Indirect channels, on the other hand, include partnerships with mobile network operators (MNOs) who leverage their spectrum and expertise to offer private network solutions as part of their enterprise portfolio. Additionally, value-added resellers (VARs) and independent system integrators serve as crucial indirect channels, packaging hardware, software, and services into comprehensive solutions for a broader range of enterprises, particularly small to medium-sized businesses (SMBs) that might prefer a single point of contact for their entire network deployment. This multi-faceted approach ensures market reach and caters to diverse customer needs, from self-managed deployments to fully outsourced solutions.

The primary potential customers for Private LTE solutions are end-user enterprises and organizations that require highly secure, reliable, and high-performance wireless connectivity for their operational technology (OT) and mission-critical applications. These buyers are typically characterized by a need for localized coverage, precise control over network parameters, and robust security protocols that exceed the capabilities of public cellular networks or standard Wi-Fi. Industries such as manufacturing, where automation and real-time data exchange are paramount, form a significant customer base, alongside sectors that operate in challenging or remote environments where public network infrastructure is inadequate or unreliable. These customers are driven by the imperative to enhance operational efficiency, ensure worker safety, and facilitate digital transformation initiatives.

Specific target segments include large industrial complexes like smart factories, where Private LTE facilitates real-time communication between automated machinery, AGVs, and production line sensors. Mining operations and oil & gas facilities are also key buyers, leveraging these networks for critical voice and data communications, remote equipment monitoring, and enhanced safety systems in hazardous conditions. Ports and logistics hubs utilize Private LTE for container tracking, autonomous vehicle communication, and efficient cargo management. Public safety agencies and government organizations represent another vital customer segment, deploying private networks for secure emergency communications, tactical operations, and reliable connectivity in disaster relief scenarios. The healthcare sector is emerging as a potential customer, seeking secure, dedicated networks for critical patient monitoring, mobile health applications, and seamless connectivity within large hospital campuses.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2032 | USD 14.5 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Nokia Corporation, Ericsson, Huawei Technologies Co. Ltd., Cisco Systems Inc., Verizon Communications Inc., AT&T Inc., Samsung Electronics Co. Ltd., Qualcomm Technologies Inc., Mavenir Systems Inc., Motorola Solutions Inc., CommScope Inc., Athonet S.r.l., Druid Software, Cradlepoint (a subsidiary of Ericsson), Sierra Wireless Inc., General Dynamics Mission Systems, Inc., Capgemini, Fujitsu Limited, NEC Corporation, ZTE Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Private LTE market fundamentally leverages Fourth Generation (4G) Long Term Evolution (LTE) cellular technology, renowned for its high capacity, low latency, and robust security features, making it ideal for critical enterprise applications. This technology forms the backbone, providing a dedicated, isolated network that offers superior performance and reliability compared to public mobile networks or Wi-Fi in demanding industrial environments. The core of this landscape includes the Evolved Packet Core (EPC), which handles subscriber management, mobility, and data routing, and the Radio Access Network (RAN), comprising base stations (eNodeBs) and antennas responsible for wireless connectivity to user equipment (UE). These elements are designed to operate autonomously within an enterprise's premises, ensuring localized control and data sovereignty.

The technological evolution within the Private LTE market is increasingly witnessing the integration of 5G New Radio (NR) capabilities, paving the way for Private 5G networks. While Private LTE provides a solid foundation, Private 5G extends these benefits with ultra-low latency, massive connectivity for IoT devices, and significantly higher bandwidth, enabling advanced applications such as real-time augmented reality, tactile internet, and pervasive automation. Furthermore, the reliance on various spectrum options forms a crucial part of the technology landscape. This includes licensed spectrum, which offers exclusive access and guaranteed performance; unlicensed spectrum (e.g., in Europe); and increasingly, shared spectrum models such as Citizens Broadband Radio Service (CBRS) in the United States, which democratizes access to mid-band spectrum for private deployments, fostering innovation and reducing entry barriers for enterprises seeking to deploy their own private networks.

Beyond the core cellular components, the Private LTE technology landscape is heavily influenced by supporting and complementary technologies. Edge computing plays a pivotal role by bringing computational power and data storage closer to the source of data generation, significantly reducing latency and enhancing real-time processing capabilities for industrial IoT applications. Network Function Virtualization (NFV) and Software Defined Networking (SDN) are critical for flexible and scalable network deployments, allowing for the virtualization of network functions and centralized network management. Security technologies, including advanced encryption and authentication protocols, are integrated to protect sensitive enterprise data. The market also sees a strong interplay with IoT platforms, which facilitate device management, data ingestion, and analytics, enabling enterprises to derive actionable insights from their private network data. These combined technologies create a powerful ecosystem for next-generation industrial and enterprise connectivity.

Private LTE is a dedicated cellular network, similar to a public mobile network but designed for exclusive use by a single organization. It comprises its own base stations (eNodeBs), core network (EPC), and uses licensed, unlicensed, or shared spectrum to provide secure, high-performance connectivity within a defined geographical area, offering greater control and reliability than Wi-Fi or public cellular.

The primary benefits include enhanced security through network isolation and encryption, superior reliability and predictable performance with guaranteed bandwidth, extensive coverage both indoors and outdoors, low latency for critical applications, and complete control over network data and resources, leading to improved operational efficiency and worker safety.

Private LTE offers several advantages over Wi-Fi, including greater coverage range, better penetration through obstacles, seamless mobility without re-authentication, superior security, and more robust performance in challenging industrial environments. Wi-Fi is generally less reliable for mission-critical applications requiring guaranteed Quality of Service and extensive outdoor coverage.

Key industries adopting Private LTE include manufacturing (for smart factories and automation), mining, oil & gas (for remote operations and safety), transportation & logistics (for port automation and asset tracking), utilities (for smart grid communication), and public safety & government (for critical communications and emergency response).

5G New Radio (NR) is the next evolution of Private LTE, offering even lower latency, higher bandwidth, and massive connectivity for IoT devices. Private 5G networks build upon LTE's foundation to enable more advanced use cases like real-time robotics, augmented reality, and enhanced industrial automation, representing a significant technological advancement for dedicated enterprise networks.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.