ID : MRU_ 430311 | Date : Nov, 2025 | Pages : 243 | Region : Global | Publisher : MRU

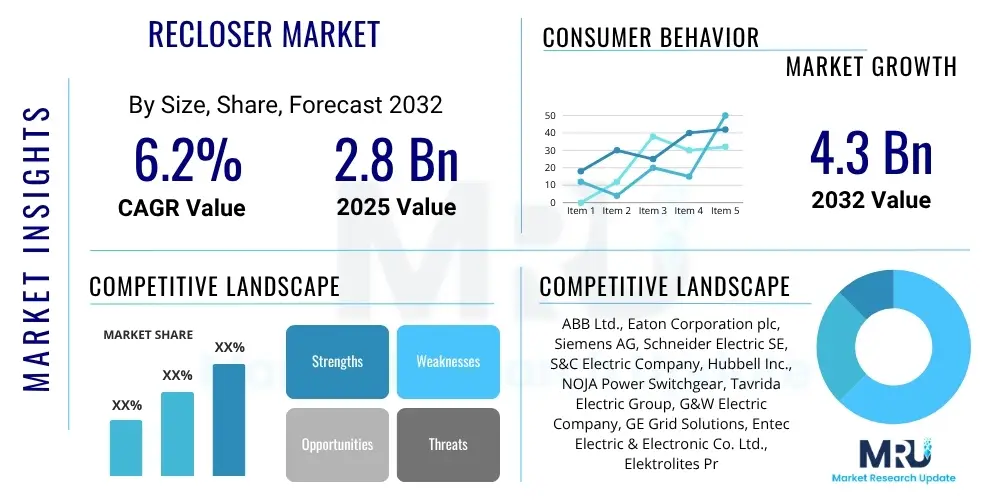

The Recloser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2032. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 4.3 Billion by the end of the forecast period in 2032.

The Recloser Market encompasses devices designed to automatically detect and interrupt fault currents on electrical distribution networks, subsequently reclosing to restore power if the fault is temporary. This capability significantly enhances grid reliability and power quality by minimizing outages, preventing equipment damage, and improving safety for both personnel and public. Reclosers are crucial components in modern power systems, bridging the gap between basic circuit breakers and sophisticated grid automation solutions, playing a pivotal role in maintaining consistent electricity supply across diverse applications.

A recloser is essentially a robust circuit breaker equipped with intelligent control capabilities that allow it to open and close multiple times in a predetermined sequence to clear temporary faults, such as those caused by lightning strikes or momentary contact with tree branches. This automatic operation capability prevents prolonged outages by only locking out after detecting a persistent fault, thereby reducing operational costs for utilities and improving customer satisfaction. Major applications span across overhead distribution lines, underground cables, and substations, serving electric utilities, industrial complexes, and commercial facilities.

The primary benefits of reclosers include enhanced grid resilience, reduced operational downtime, improved safety, and optimized maintenance schedules. The market is primarily driven by the increasing demand for reliable electricity, the urgent need to modernize aging grid infrastructure, the global push towards smart grid implementation, and the escalating integration of renewable energy sources into existing power networks. These factors collectively underscore the indispensable role of reclosers in the evolution of electricity distribution.

The Recloser Market is experiencing robust growth driven by significant business trends focusing on grid modernization, digitalization, and the imperative for enhanced power reliability. Utilities globally are investing heavily in advanced recloser technologies that offer remote monitoring, control, and sophisticated fault detection capabilities, moving away from traditional hydraulic models towards electronic, microprocessor-controlled devices. This shift is also fueled by the increasing adoption of smart grid initiatives which demand interconnected and intelligent grid components capable of rapid response and self-healing functionalities, ultimately leading to more efficient power distribution and reduced operational expenditures.

Regional trends indicate strong growth in emerging economies, particularly across the Asia Pacific, where rapid industrialization, urbanization, and expanding electricity infrastructure create substantial demand for reclosers. North America and Europe, with their mature grids, are primarily focused on replacing aging equipment and integrating smart reclosers to support renewable energy penetration and enhance grid resilience against extreme weather events. Latin America and the Middle East & Africa are also witnessing considerable investments in grid expansion and modernization projects, contributing significantly to market development as they strive to meet rising energy consumption and improve power access.

Segment-wise, the market is seeing a notable trend towards electronic reclosers over hydraulic types, owing to their superior programmability, accuracy, and communication capabilities. Three-phase reclosers are gaining prominence due to their efficiency in managing common distribution network faults, while single-phase units continue to be essential for specific applications. The increasing deployment of reclosers in overhead lines and substations remains dominant, though their application in underground networks is steadily growing. Overall, the market is characterized by technological advancements aimed at improving grid automation, cybersecurity, and seamless integration with broader smart grid architectures.

Common user questions regarding AI's impact on the Recloser Market frequently revolve around how artificial intelligence can enhance fault detection, improve predictive maintenance, optimize grid operations, and what new capabilities AI-driven reclosers can offer compared to conventional models. Users are keen to understand the practical benefits such as reduced outage times, more efficient resource allocation, and the potential for a truly self-healing grid. There are also concerns about the complexity of integrating AI, data privacy, cybersecurity vulnerabilities associated with interconnected intelligent systems, and the skills gap required for managing these advanced technologies.

The key themes emerging from this analysis highlight a strong expectation for AI to transform recloser functionalities from reactive fault isolation to proactive grid management. Users anticipate AI will provide unprecedented levels of intelligence for real-time anomaly detection, precise fault location, and automated decision-making regarding recloser operations, thereby significantly improving grid resilience and performance. The excitement also extends to AI's potential in optimizing energy flow, managing distributed energy resources, and facilitating more dynamic and adaptive power distribution networks.

However, the transition to AI-enabled reclosers brings challenges, including the need for robust data infrastructure, sophisticated algorithms, and stringent cybersecurity measures to protect critical grid assets. Users are seeking assurances that these advanced systems will be reliable, secure, and easily integrated into existing grid management frameworks without extensive overhauls. The long-term implications for maintenance protocols, operational training, and regulatory compliance are also significant points of interest, emphasizing a desire for clear pathways to adoption and scalable solutions.

The Recloser Market is primarily driven by the critical need for enhanced grid reliability and efficiency, propelled by the modernization of aging infrastructure across developed nations and the expansion of electricity networks in developing regions. Increasing global electricity demand, coupled with the rapid integration of renewable energy sources such as solar and wind power, necessitates robust and intelligent fault management solutions like reclosers to maintain grid stability. Furthermore, stringent regulatory mandates emphasizing power quality and continuity are compelling utilities to adopt advanced reclosing technologies, driving market expansion.

However, the market faces significant restraints, including the high initial investment costs associated with advanced electronic reclosers and their complex integration into existing legacy grid systems, which can be a deterrent for some utilities. Cybersecurity concerns arising from the increased connectivity of smart reclosers present another challenge, requiring substantial investment in secure communication protocols and infrastructure. Moreover, the lack of standardized communication protocols across different manufacturers can hinder interoperability and broader adoption, while the need for skilled personnel to operate and maintain these sophisticated devices poses a workforce challenge.

Opportunities for growth are abundant, particularly in untapped markets within rural and remote areas of developing countries where electrification efforts are ongoing. The emergence of microgrids and distributed generation offers new avenues for recloser deployment, as these systems require localized fault protection and management. Advancements in communication technologies, such as 5G and IoT, are enabling more seamless integration and remote control capabilities, further expanding the potential applications of reclosers. Impact forces, including rapid technological advancements in sensors and control electronics, evolving environmental regulations promoting grid resilience, and ongoing economic growth globally, collectively shape the market's trajectory.

The Recloser Market is extensively segmented to reflect the diverse range of product types, control mechanisms, voltage ratings, applications, and end-user industries. This granular segmentation provides a comprehensive view of market dynamics, enabling stakeholders to identify specific growth areas and tailor their strategies. The evolving needs of power utilities, industrial clients, and the commercial sector dictate the demand for particular recloser configurations, emphasizing flexibility and technological sophistication. Understanding these segments is crucial for analyzing current market penetration and forecasting future growth trajectories.

By type, the market differentiates between single-phase and three-phase reclosers, each serving distinct network requirements for fault isolation and power restoration. Control mechanisms categorize reclosers into hydraulic and electronic variants, with the latter gaining significant traction due to its advanced features and compatibility with smart grid technologies. Voltage ratings, ranging from low to high voltage, define the suitability of reclosers for different sections of the power distribution network, from distribution feeders to substations. These classifications are fundamental to matching product capabilities with operational demands.

Applications further segment the market by deployment scenarios, including overhead lines, underground lines, and substations, reflecting varied environmental and operational challenges. Finally, end-users such as electric utilities, industrial facilities, and commercial establishments represent the ultimate consumers, each with unique requirements concerning reliability, automation, and cost-efficiency. This detailed segmentation allows for a nuanced understanding of market trends, technological preferences, and regional adoption patterns, facilitating targeted product development and market penetration strategies.

The value chain for the Recloser Market begins with the upstream analysis, which involves the sourcing of essential raw materials and components. This segment includes suppliers of high-grade metals like copper and aluminum for conductors, steel for structural components, and various polymers and ceramics for insulation. Crucial electronic components such as microprocessors, sensors, communication modules, and control boards are also procured from specialized manufacturers. The quality and availability of these upstream inputs directly influence the final product's performance, cost-efficiency, and manufacturing lead times, making strong supplier relationships vital for recloser manufacturers.

Moving downstream, the value chain progresses through the manufacturing, assembly, and testing phases of reclosers, followed by distribution and eventually, end-user deployment and post-sales services. Manufacturing involves intricate processes for fabricating mechanical parts, assembling the vacuum interrupters, integrating electronic controls, and ensuring rigorous quality assurance. The distribution channel plays a critical role in delivering these complex products to a diverse customer base. This typically involves a combination of direct sales from manufacturers to large utilities and governments, as well as indirect channels through a network of distributors, system integrators, and original equipment manufacturers (OEMs) who bundle reclosers with broader grid solutions. Effective distribution ensures market reach and timely product availability.

The final stages of the value chain encompass installation, commissioning, operation, and maintenance. Specialized contractors or in-house utility teams handle the installation of reclosers on distribution networks. Post-installation, ongoing maintenance, troubleshooting, and eventual replacement services are critical for ensuring the longevity and optimal performance of these devices. Direct sales channels facilitate closer relationships between manufacturers and key utility clients, allowing for tailored solutions and direct technical support. Indirect channels, through distributors and integrators, extend market penetration to smaller utilities and industrial clients, often providing localized support and value-added services. Both channels are essential for comprehensive market coverage and customer satisfaction throughout the recloser's lifecycle.

The primary potential customers for the Recloser Market are diverse entities that operate and manage electrical distribution networks, requiring robust solutions for fault protection and power restoration. Electric utilities, encompassing municipal, public, and investor-owned companies, form the largest segment of end-users. These organizations are responsible for the transmission and distribution of electricity to residential, commercial, and industrial consumers, and thus have a perpetual need for reclosers to ensure grid reliability, minimize outages, and comply with regulatory standards for power quality. The ongoing modernization of aging infrastructure and expansion into new service areas further drives their demand.

Beyond traditional utilities, the industrial sector represents a significant customer base. Large industrial facilities, such as manufacturing plants, mining operations, oil and gas platforms, and data centers, often have their own internal distribution networks that require robust fault protection to prevent costly downtime and equipment damage. Reclosers are vital in these environments to isolate faults quickly, ensuring continuous operation of critical processes. The need for uninterrupted power supply in these high-stakes industrial settings makes them key buyers of advanced recloser solutions, often customized to their specific operational requirements and safety protocols.

Furthermore, the growing number of distributed energy resources (DERs) and microgrid developers are emerging as crucial potential customers. As renewable energy sources like solar and wind become more prevalent, and as communities invest in localized microgrids for enhanced resilience, the demand for reclosers within these decentralized power systems increases. These customers require reclosers that can manage bidirectional power flow, integrate with smart grid controls, and provide rapid fault isolation to maintain stability in complex, interconnected power systems. Other emerging segments include large commercial campuses, smart city infrastructure projects, and rural electrification initiatives in developing economies, all seeking to improve power access and reliability through modern grid components.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2032 | USD 4.3 Billion |

| Growth Rate | 6.2% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Eaton Corporation plc, Siemens AG, Schneider Electric SE, S&C Electric Company, Hubbell Inc., NOJA Power Switchgear, Tavrida Electric Group, G&W Electric Company, GE Grid Solutions, Entec Electric & Electronic Co. Ltd., Elektrolites Private Limited, Iljin Electric Co. Ltd., Lucy Electric, Arteche Group, Beijing Sifang Automation Co. Ltd., Jiangsu Daqo Group Co. Ltd., Jinan Jingdian Electric Co. Ltd., CHINT Group, SEL (Schweitzer Engineering Laboratories). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Recloser Market's key technology landscape is characterized by continuous innovation aimed at enhancing grid automation, reliability, and resilience. At its core, modern reclosers leverage microprocessor-based controls, which offer superior programmability, precise fault detection, and sophisticated operational sequences compared to older hydraulic or electronic relay-based systems. These intelligent controls are critical for enabling advanced functionalities such as adaptive protection schemes, automatic network reconfiguration, and seamless integration into broader smart grid architectures. The shift towards solid dielectric insulation technology over oil-filled or SF6 gas reclosers is also a prominent trend, driven by environmental concerns and a focus on maintenance-free operation.

Communication technologies form another cornerstone of the modern recloser landscape, enabling remote monitoring, control, and data exchange. Protocols like SCADA (Supervisory Control and Data Acquisition), DNP3 (Distributed Network Protocol 3), and IEC 61850 are widely adopted, facilitating real-time communication between reclosers and utility control centers. The integration of IoT (Internet of Things) capabilities, including cellular, fiber optic, and radio frequency communication modules, allows for increased connectivity, enabling reclosers to participate in self-healing grid operations and provide valuable data for grid analytics. These communication advancements are crucial for the development of fully automated distribution systems.

Furthermore, the incorporation of advanced sensing capabilities, such as integrated voltage and current sensors, enhances the accuracy of fault detection and power quality monitoring. Vacuum interrupter technology remains fundamental for arc quenching, ensuring safe and reliable interruption of fault currents. Emerging technologies like artificial intelligence and machine learning are beginning to play a role in predictive maintenance, fault pattern analysis, and optimizing reclosing sequences, pushing reclosers towards more autonomous and adaptive operation. This technological evolution underscores a commitment to creating smarter, more efficient, and sustainable power distribution networks, capable of handling the complexities of modern energy demands and distributed generation.

The Recloser Market exhibits distinct regional dynamics influenced by varying levels of grid infrastructure development, energy policies, and technological adoption rates. North America, comprising the United States and Canada, represents a mature market characterized by significant investments in modernizing aging grid infrastructure and enhancing grid resilience against severe weather events. The region is a pioneer in smart grid initiatives and the integration of distributed energy resources, driving the demand for advanced, electronic reclosers with enhanced communication capabilities. Regulatory mandates and incentives for improving power reliability further stimulate market growth, focusing on replacement and upgrade cycles for existing equipment.

Europe, including key economies like Germany, the UK, France, and Italy, demonstrates a strong commitment to renewable energy integration and grid automation, fostering a robust market for reclosers. The region's focus on energy transition and achieving carbon neutrality necessitates smart grid solutions that can efficiently manage fluctuating renewable generation and ensure stable power delivery. Stringent environmental regulations also favor the adoption of solid dielectric reclosers over traditional oil-insulated types. While infrastructure is well-established, there is a continuous push for technological upgrades and the deployment of intelligent reclosers to support a more sustainable and interconnected energy landscape.

The Asia Pacific region, encompassing countries such as China, India, Japan, and South Korea, is projected to be the fastest-growing market due to rapid industrialization, urbanization, and ambitious rural electrification programs. Massive investments in expanding and building new power infrastructure to meet escalating energy demand are a primary growth driver. Governments in this region are actively promoting smart grid development and renewable energy projects, leading to substantial opportunities for recloser manufacturers. The Middle East & Africa (MEA) and Latin America regions are also experiencing considerable growth, driven by increasing energy consumption, infrastructure development projects, and efforts to improve access to reliable electricity, presenting significant untapped potential for recloser deployment.

Users frequently inquire about the fundamental purpose of reclosers, how they contribute to grid reliability, the distinctions between different types and control mechanisms, and the evolving role of advanced technologies like AI in their functionality. Questions often highlight concerns about market growth drivers, the influence of smart grid trends, and the geographical areas experiencing the most significant expansion. There's also a strong interest in understanding the benefits of modern reclosers over older versions and their operational implications for utility companies and end-users.

A recloser is an automatic circuit breaker designed to detect and interrupt temporary faults on electrical distribution lines, then automatically re-energize the line after a preset time. Its primary function is to restore power quickly following transient faults, significantly enhancing grid reliability and reducing outage durations by only locking out after persistent faults are detected.

Smart reclosers, typically electronic and microprocessor-controlled, offer advanced features such as programmable reclosing sequences, remote monitoring and control, communication capabilities (e.g., SCADA, IoT), and data logging. Traditional reclosers, often hydraulic, have simpler, fixed operating sequences and lack advanced communication, making smart reclosers more adaptable and integral to modern smart grids.

The Recloser market growth is primarily driven by the need to modernize aging grid infrastructure, increasing demand for reliable electricity, the global push towards smart grid implementation, and the growing integration of renewable energy sources into existing power networks. These factors necessitate robust and intelligent fault management solutions.

AI enhances modern reclosers by enabling predictive maintenance, optimizing fault detection and isolation through machine learning algorithms, and improving reclosing sequences based on real-time grid conditions. AI can also facilitate proactive grid management, supporting self-healing functionalities and reducing operational costs by minimizing manual interventions and optimizing maintenance.

The Asia Pacific region is demonstrating the most significant growth due to rapid industrialization, urbanization, and extensive electrification efforts in countries like China and India. North America and Europe also show steady growth driven by grid modernization, aging infrastructure replacement, and the integration of renewable energy sources.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.