ID : MRU_ 430619 | Date : Nov, 2025 | Pages : 243 | Region : Global | Publisher : MRU

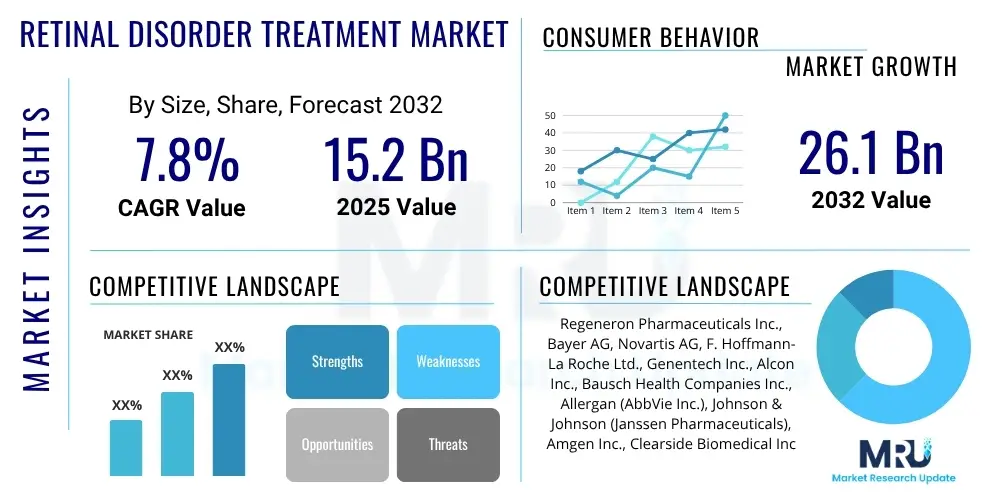

The Retinal Disorder Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 26.1 Billion by the end of the forecast period in 2032.

The Retinal Disorder Treatment Market encompasses a broad spectrum of pharmaceutical, surgical, and therapeutic interventions aimed at managing and treating various conditions affecting the retina, the light-sensitive tissue at the back of the eye. Retinal disorders, including age-related macular degeneration (AMD), diabetic retinopathy (DR), retinal vein occlusion (RVO), and inherited retinal diseases, represent significant causes of vision impairment and blindness globally. The market is driven by an increasing global geriatric population, a rising prevalence of diabetes and other chronic diseases contributing to retinal damage, and continuous advancements in diagnostic imaging and therapeutic modalities.

Products within this market range from anti-vascular endothelial growth factor (anti-VEGF) agents, corticosteroids, and non-steroidal anti-inflammatory drugs (NSAIDs) administered through intravitreal injections, to advanced surgical procedures such as vitrectomy and scleral buckling, and groundbreaking gene and cell therapies. These treatments are designed to preserve vision, prevent further retinal damage, and in some cases, restore lost visual function. The primary applications include the management of wet AMD, proliferative diabetic retinopathy, macular edema, and the correction of retinal detachments. The core benefits extend beyond vision preservation to significantly improving patients' quality of life, reducing the burden on healthcare systems by mitigating severe disability, and enabling individuals to maintain independence.

The market's growth trajectory is significantly influenced by several key driving factors. The demographic shift towards an older global population inherently increases the incidence of age-related retinal conditions like AMD. Furthermore, the surging prevalence of diabetes worldwide directly fuels the diabetic retinopathy segment. Technological innovation plays a crucial role, with ongoing research and development leading to more effective and less invasive treatments, advanced drug delivery systems, and enhanced diagnostic capabilities. Increased awareness among both patients and healthcare providers regarding early detection and the importance of timely intervention for retinal health also contributes to market expansion, fostering proactive treatment-seeking behaviors and improving patient outcomes.

The Retinal Disorder Treatment Market is characterized by dynamic business trends, evolving regional landscapes, and significant segment-specific growth, all contributing to its robust expansion. Business trends prominently include strategic collaborations, mergers, and acquisitions among pharmaceutical and biotechnology companies aimed at consolidating market share and pooling R&D resources for novel therapies. There is a strong emphasis on personalized medicine, with companies investing in genetic screening and biomarkers to tailor treatments more precisely to individual patient needs, thereby optimizing efficacy and reducing adverse effects. Furthermore, the pipeline for retinal disorder treatments remains vibrant, with numerous innovative drug candidates and advanced surgical techniques currently undergoing clinical trials, indicating a sustained commitment to addressing unmet medical needs.

From a regional perspective, North America and Europe currently hold significant market shares, largely due to established healthcare infrastructures, high healthcare expenditure, favorable reimbursement policies, and a greater awareness of retinal disorders. These regions are also at the forefront of adopting advanced treatment modalities and conducting extensive clinical research. However, the Asia Pacific region is rapidly emerging as a high-growth market, driven by its large and aging population, increasing prevalence of chronic diseases like diabetes, improving healthcare accessibility, and rising disposable incomes. Latin America, the Middle East, and Africa are also expected to witness substantial growth, propelled by expanding healthcare access, increasing governmental initiatives to combat vision impairment, and a growing recognition of the economic burden associated with untreated retinal conditions.

Segmentation trends within the market highlight the continued dominance of anti-VEGF therapies, which remain the first-line treatment for various neovascular retinal disorders due to their proven efficacy. However, the market is also witnessing a burgeoning interest and investment in gene and cell therapies, representing a paradigm shift towards potentially curative treatments for inherited retinal dystrophies and advanced forms of AMD. There is also a growing focus on longer-acting formulations and sustained-release drug delivery systems, which aim to reduce the frequency of intravitreal injections, thereby improving patient compliance and convenience. Diagnostic advancements, particularly in optical coherence tomography (OCT) and artificial intelligence-powered imaging analysis, are further enhancing the precision of diagnosis and monitoring, enabling earlier intervention and better therapeutic management across all segments.

User inquiries regarding the impact of Artificial Intelligence on the Retinal Disorder Treatment Market frequently revolve around AI's capabilities in enhancing diagnostic accuracy, personalizing treatment plans, accelerating drug discovery, and improving patient management. Common questions explore how AI algorithms can analyze complex retinal images for early disease detection, predict treatment responses, optimize surgical outcomes, and facilitate remote monitoring. Concerns often touch upon data privacy, the potential for algorithmic bias, and the necessity of robust validation for AI-powered tools before widespread clinical adoption. Users also seek to understand the practical integration challenges and the ethical implications of relying on AI for critical medical decisions, while maintaining an optimistic outlook on AI's potential to revolutionize ophthalmological care by increasing efficiency and improving patient outcomes.

The Retinal Disorder Treatment Market is significantly influenced by a complex interplay of drivers, restraints, opportunities, and broader impact forces that collectively shape its growth trajectory and competitive landscape. Key drivers include the escalating global prevalence of retinal diseases, predominantly fueled by an aging population and the widespread increase in chronic conditions such as diabetes, which directly contribute to conditions like age-related macular degeneration and diabetic retinopathy. Continuous innovation in therapeutic modalities, particularly the development of more effective anti-VEGF agents, gene therapies, and sustained-release drug delivery systems, further propels market expansion by offering improved patient outcomes and convenience. Moreover, rising awareness about eye health and early disease detection among the general public and healthcare professionals contributes to higher diagnosis rates and a greater demand for advanced treatments.

Conversely, several restraints impede the market’s full potential. The high cost associated with advanced retinal disorder treatments, especially novel gene therapies and repeated anti-VEGF injections, poses a significant financial burden on patients and healthcare systems, often leading to access disparities. Stringent regulatory approval processes for new drugs and devices can delay market entry and increase development costs. Furthermore, the potential side effects associated with certain treatments, patient non-compliance with long-term therapy regimens, and a shortage of retina specialists in certain regions limit the widespread adoption and optimal management of these conditions. Competition from biosimilars and generics also introduces pricing pressures, impacting the profitability of innovator companies.

Despite these challenges, substantial opportunities exist within the market. Emerging economies in Asia Pacific, Latin America, and the Middle East offer untapped growth potential due to their large populations, improving healthcare infrastructures, and increasing healthcare spending. The advancement of novel treatment approaches, such as CRISPR-based gene editing, optogenetics, and stem cell therapies, presents transformative possibilities for currently untreatable or poorly managed conditions. The adoption of telemedicine and digital health solutions is expanding access to care, particularly for remote monitoring and follow-up consultations. Additionally, a growing focus on precision medicine and personalized treatment strategies, driven by genetic insights and advanced diagnostics, promises to optimize therapeutic efficacy and enhance patient satisfaction.

The Retinal Disorder Treatment Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates comprehensive analysis of treatment adoption rates, market penetration, and growth opportunities across different disease types, therapeutic approaches, and end-user demographics. The market's structure reflects the varied clinical needs and technological advancements applied to ophthalmological care, encompassing both established and emerging treatment paradigms. Understanding these segments is crucial for stakeholders to tailor strategies, identify lucrative niches, and allocate resources effectively in this rapidly evolving healthcare sector.

The value chain for the Retinal Disorder Treatment Market is a complex and interconnected network involving various stakeholders from research and development to patient care. It begins with upstream activities focused on drug discovery and ingredient sourcing. This stage involves pharmaceutical and biotechnology companies investing heavily in R&D to identify novel therapeutic targets and develop innovative compounds. Contract Research Organizations (CROs) play a crucial role in preclinical and clinical trials, ensuring the safety and efficacy of new treatments. Concurrently, specialized manufacturers supply active pharmaceutical ingredients (APIs), excipients, and advanced medical device components required for drug formulation and surgical instruments. Quality control and regulatory compliance are paramount at this foundational stage, as all materials and early-stage products must meet stringent industry and health authority standards before proceeding to manufacturing.

Midstream activities primarily encompass the manufacturing, formulation, and commercialization of retinal disorder treatments. This involves large-scale production of anti-VEGF biologics, corticosteroids, gene therapy vectors, and surgical instruments. Pharmaceutical companies are responsible for the sterile manufacturing, packaging, and quality assurance of injectable drugs and implants, ensuring their stability and potency. For medical devices, this includes the precision engineering and assembly of laser systems, vitrectomy machines, and diagnostic imaging equipment. Extensive marketing and sales efforts are then deployed to educate healthcare providers about the benefits and appropriate use of these treatments. Regulatory submissions and approvals from bodies like the FDA and EMA are critical milestones in this stage, determining market access and commercial viability for new and existing products.

Downstream activities focus on the distribution and delivery of these treatments to end-users, primarily patients. The distribution channel is multifaceted, comprising direct sales from manufacturers to large hospital systems, as well as indirect channels involving wholesalers, distributors, and specialized pharmacies. Hospital pharmacies and specialty clinics serve as primary points of dispensing for intravitreal injections and surgical supplies, given the specialized nature of administration. Retail and online pharmacies also play a role in providing adjunctive medications and post-operative care products. Direct interaction with patients occurs through ophthalmologists, retina specialists, and surgical teams who diagnose, prescribe, and administer treatments. Effective patient education and support programs, often facilitated by healthcare providers and patient advocacy groups, are vital in ensuring treatment adherence and optimal outcomes, completing the value chain by connecting product to patient care.

The potential customers for the Retinal Disorder Treatment Market are diverse, encompassing various segments of the healthcare ecosystem, all driven by the critical need to address vision-threatening retinal conditions. Primary among these are patients suffering from a wide range of retinal disorders, including age-related macular degeneration (AMD), diabetic retinopathy (DR), retinal vein occlusion (RVO), and inherited retinal diseases. These patients, often characterized by an aging demographic or co-morbidities like diabetes, seek treatments to preserve, restore, or improve their vision and enhance their overall quality of life. Their purchasing decisions are heavily influenced by the severity of their condition, the efficacy and safety profiles of available treatments, accessibility, and the advice of their ophthalmologists. The growing global burden of these diseases ensures a continuously expanding patient pool as a core customer base.

Healthcare providers constitute another critical segment of potential customers. This includes a vast network of ophthalmologists, retina specialists, optometrists, and general practitioners who diagnose, refer, and administer retinal treatments. Hospitals, specialty eye clinics, and ambulatory surgical centers are key institutional buyers, investing in advanced diagnostic equipment, surgical instruments, and pharmaceutical supplies to offer comprehensive retinal care services. These institutions make purchasing decisions based on clinical effectiveness, cost-efficiency, technological integration with existing infrastructure, and the ability to attract and retain highly skilled retina specialists. The demand from these professional and institutional customers is driven by the need to provide cutting-edge care, manage patient flow effectively, and maintain their reputation for excellence in ophthalmology.

Furthermore, government healthcare programs, private insurance providers, and public health organizations represent significant indirect customers. These entities play a crucial role in determining the market's accessibility and reimbursement landscape, influencing which treatments are covered and at what cost. Their decisions impact patient access and the financial viability of therapeutic innovations. Research institutes and academic medical centers also act as potential customers, utilizing specialized technologies and treatments for clinical trials, research into disease mechanisms, and the development of future therapies. Finally, pharmaceutical distributors and wholesalers are essential intermediaries, facilitating the efficient movement of products from manufacturers to various healthcare delivery points, making them vital partners in the overall market ecosystem. Each customer segment contributes uniquely to the market's dynamics, influencing product development, distribution strategies, and pricing structures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2032 | USD 26.1 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Regeneron Pharmaceuticals Inc., Bayer AG, Novartis AG, F. Hoffmann-La Roche Ltd., Genentech Inc., Alcon Inc., Bausch Health Companies Inc., Allergan (AbbVie Inc.), Johnson & Johnson (Janssen Pharmaceuticals), Amgen Inc., Clearside Biomedical Inc., Kodiak Sciences Inc., Apellis Pharmaceuticals Inc., Opthea Ltd., Lineage Cell Therapeutics Inc., Adverum Biotechnologies Inc., Nightstar Therapeutics (Biogen Inc.), Eyevance Pharmaceuticals (CVS Health), Santen Pharmaceutical Co. Ltd., Gilead Sciences Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Retinal Disorder Treatment Market is at the forefront of medical innovation, characterized by a dynamic technology landscape continually evolving to provide more effective, less invasive, and longer-lasting solutions for patients. A cornerstone of modern retinal therapy is the development and widespread adoption of anti-vascular endothelial growth factor (anti-VEGF) agents. These biologic drugs, such as ranibizumab (Lucentis), aflibercept (Eylea), and brolucizumab (Beovu), revolutionized the treatment of wet age-related macular degeneration (AMD), diabetic macular edema (DME), and retinal vein occlusion (RVO) by targeting the molecular pathways responsible for abnormal blood vessel growth and leakage. Ongoing research in this area focuses on developing longer-acting formulations and novel anti-VEGF compounds with improved binding affinities and sustained therapeutic effects, aiming to reduce the frequency of intravitreal injections and enhance patient convenience and adherence.

Beyond anti-VEGF therapies, the technological landscape is expanding rapidly with groundbreaking advancements in gene and cell therapies. Gene therapy, exemplified by voretigene neparvovec (Luxturna) for inherited retinal dystrophies, offers the potential for a one-time treatment to correct genetic defects causing blindness. Numerous other gene therapy candidates are in various stages of clinical development for conditions like wet AMD and retinitis pigmentosa, utilizing viral vectors to deliver therapeutic genes to retinal cells. Similarly, cell therapy approaches, including the transplantation of retinal pigment epithelial (RPE) cells or photoreceptor precursors derived from induced pluripotent stem cells, are being explored for their potential to replace damaged retinal cells and restore function, particularly in advanced forms of AMD and inherited retinal diseases, representing a significant long-term therapeutic promise.

Complementing these pharmaceutical innovations are significant technological strides in diagnostic imaging and surgical techniques. Optical Coherence Tomography (OCT) and OCT Angiography (OCTA) have become indispensable for non-invasive, high-resolution imaging of retinal layers and vascular networks, enabling early detection, precise diagnosis, and meticulous monitoring of treatment response. The integration of Artificial Intelligence (AI) with these imaging modalities is enhancing diagnostic accuracy and efficiency, allowing for automated detection of biomarkers and disease progression. Surgically, advancements in micro-incisional vitrectomy systems, intraoperative OCT, and robotic assistance are improving the safety and precision of delicate retinal surgeries, minimizing trauma and optimizing outcomes for complex conditions like retinal detachment and proliferative diabetic retinopathy. Furthermore, sustained-release drug delivery systems, such as intravitreal implants and subretinal devices, are emerging to provide continuous drug release over extended periods, reducing the need for frequent injections and improving patient quality of life.

The primary retinal disorders treated include age-related macular degeneration (AMD), diabetic retinopathy (DR) including diabetic macular edema (DME), retinal vein occlusion (RVO), retinal detachment, and various forms of uveitis and inherited retinal diseases. These conditions collectively represent the major causes of vision loss requiring advanced therapeutic interventions.

The market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2032. This expansion is driven by factors such as an aging global population, increasing prevalence of chronic diseases like diabetes, continuous advancements in therapeutic options, and rising awareness about early detection and treatment.

Key challenges include the high cost of advanced treatments, particularly novel gene therapies and repeated intravitreal injections, which can lead to accessibility issues. Other significant restraints are stringent regulatory approval processes, potential side effects associated with therapies, and a shortage of specialized retina care professionals in various regions.

AI is increasingly vital in the retinal disorder treatment market, primarily by enhancing diagnostic accuracy through automated image analysis for early detection. It also aids in predicting disease progression, personalizing treatment strategies, accelerating drug discovery, and improving surgical precision, thus optimizing patient outcomes and clinical efficiency.

North America and Europe currently lead the market due to advanced healthcare infrastructure, high disease prevalence, substantial R&D investments, and favorable reimbursement policies. However, the Asia Pacific region is rapidly emerging as a high-growth market, driven by its large aging population and improving healthcare accessibility.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.